Finance

What Is An Insurance Certificate Holder?

Published: November 19, 2023

Learn the importance of insurance certificate holders in the world of finance and how they play a crucial role in protecting your financial interests.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Definition of an Insurance Certificate Holder

- Importance of Insurance Certificate Holders

- Roles and Responsibilities of Insurance Certificate Holders

- Types of Insurance Certificate Holders

- Benefits of Being an Insurance Certificate Holder

- Limitations and Considerations for Insurance Certificate Holders

- Key Differences between Insurance Certificate Holders and Named Insured

- Conclusion

Introduction

Welcome to the world of insurance, where protection and peace of mind are paramount. When it comes to insurance policies, there are various parties involved, including the insured, insurance agents, and insurance companies. However, one key player that often goes unnoticed but holds significant importance is the insurance certificate holder.

An insurance certificate holder is a party who is named as an additional interested party on the insurance certificate. They may not be the policyholder or the primary insured, but they have a vested interest in the policy’s coverage. The insurance certificate holder is entitled to receive updates and notifications regarding the insurance policy, ensuring that they are informed and protected.

Insurance certificate holders can be individuals, organizations, or businesses that have a legal or financial interest in the insured property or project. They could be landlords, lenders, contractors, or anyone else who wants to safeguard their investment.

In this article, we will explore the role of insurance certificate holders, their responsibilities, the benefits they enjoy, and the key differences between insurance certificate holders and named insured. So, let’s dive in and learn more about the importance and significance of insurance certificate holders in the realm of insurance.

Definition of an Insurance Certificate Holder

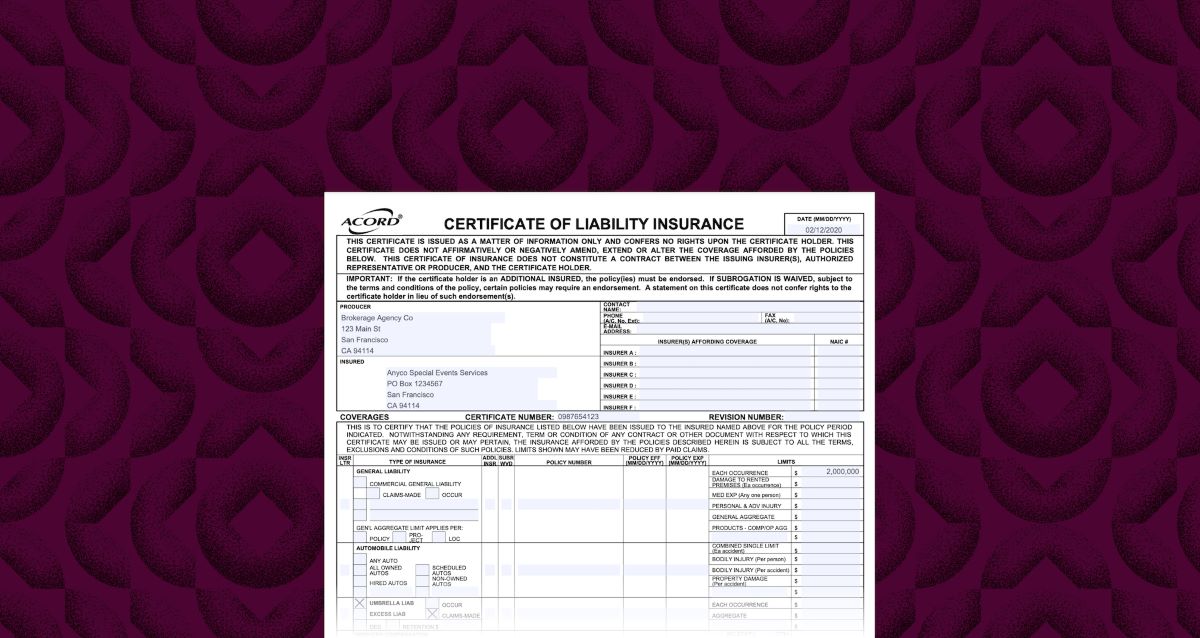

Before delving deeper into the world of insurance certificate holders, let’s start by understanding the concept and definition. An insurance certificate holder refers to a party, whether an individual or an organization, that is named as an additional interested party on an insurance policy’s certificate. This certificate serves as proof of insurance coverage and outlines the policy details, including coverage limits and effective dates.

The insurance certificate is typically issued by the insurance company to the policyholder, who is the primary insured. However, the certificate can also include additional parties known as insurance certificate holders. These certificate holders are not the policyholders, but they have a vested interest in the insurance coverage.

The inclusion of insurance certificate holders on the certificate is essential as it helps establish a legal relationship between the primary insured and the certificate holder. It ensures that the certificate holder receives important notifications, updates, and access to information regarding the insurance policy. This empowers them to protect their interests and ensure that they are adequately covered.

Insurance certificate holders can be individuals, businesses, or organizations that have a financial or legal stake in the insured property or project. For example, a landlord may require their tenants to name them as an insurance certificate holder to ensure that they are notified in case of any changes or cancellations to the insurance policy covering the rented property.

In summary, an insurance certificate holder is a party named on an insurance policy’s certificate who has a vested interest in the policy’s coverage. They are entitled to receive updates and notifications regarding the policy to ensure that they are adequately protected and informed.

Importance of Insurance Certificate Holders

Insurance certificate holders play a vital role in the insurance ecosystem, providing an additional layer of protection and accountability. Their inclusion in insurance policies offers several benefits and ensures that all parties involved are adequately informed and safeguarded. Let’s explore the importance of insurance certificate holders in more detail.

1. Risk Mitigation: Insurance certificate holders help mitigate risks by ensuring that they are notified of any changes or cancellations to the insurance policy. By staying informed, they can take appropriate action to protect their interests and ensure that they are adequately covered. This is particularly important for parties like landlords, lenders, or contractors, whose financial well-being may be tied to the insured property or project.

2. Compliance Requirements: Many industries and regulatory bodies require businesses and organizations to have specific insurance coverage. Insurance certificate holders help facilitate compliance with these requirements by ensuring that they have proof of insurance coverage and are named on the insurance certificate. This helps these entities avoid potential legal issues, disputes, and penalties.

3. Contractual Obligations: Insurance certificate holders are often named in contracts or agreements to ensure that all parties are adequately protected. For example, a contractor may be required to name the property owner as a certificate holder to assure them that they have the necessary insurance coverage in case of any damage or liability during the project. This helps establish trust and accountability between the parties involved.

4. Access to Policy Information: By being named as certificate holders, individuals or organizations have access to important policy information and updates. This includes details about coverage limits, deductibles, and policy expiration dates. This allows them to make informed decisions and take appropriate action based on the policy’s terms and conditions.

5. Verification of Insurance: Insurance certificate holders act as a verification tool for third parties, such as clients, vendors, or partners. By being named on the certificate, they can demonstrate that the primary insured holds the required insurance coverage, giving peace of mind to those conducting business with them.

Overall, insurance certificate holders are crucial in ensuring that all parties involved in an insurance policy are adequately protected, informed, and compliant. By actively participating in the process, they contribute to a more transparent and accountable insurance ecosystem.

Roles and Responsibilities of Insurance Certificate Holders

As active participants in the insurance process, insurance certificate holders have distinct roles and responsibilities. These responsibilities help ensure that their interests are protected and that they fulfill their obligations as stakeholders in the insurance policy. Let’s take a closer look at the roles and responsibilities of insurance certificate holders:

1. Reviewing the Insurance Certificate: Insurance certificate holders should carefully review the insurance certificate provided by the policyholder. They must ensure that their information is accurately reflected on the certificate, including their name, contact details, and any specific requirements or endorsements they have requested.

2. Monitoring Policy Updates: It is the responsibility of insurance certificate holders to stay informed about any updates or changes to the insurance policy. They should regularly review the policy documents and communicate with the policyholder or their insurance agent to ensure that they are aware of any modifications in coverage, policy limits, or exclusions.

3. Notifying of Policy Cancellations or Expirations: Insurance certificate holders must be notified promptly in case of policy cancellations or expirations. This is crucial to avoid any gaps in coverage and allow them to take necessary actions, such as arranging for alternative coverage or updating contracts and agreements that require proof of insurance.

4. Requesting Certificate Amendments or Endorsements: If insurance certificate holders require additional coverage or specific endorsements, it is their responsibility to communicate these requirements to the policyholder or insurance agent. They should request certificate amendments or endorsements to ensure that their interests are adequately protected under the insurance policy.

5. Maintaining Proof of Insurance: Insurance certificate holders should keep a record of the insurance certificate and any additional documents necessary to prove their interest in the policy. This documentation may be required when entering into contracts, obtaining permits for certain activities, or during legal proceedings.

6. Cooperating in Claims Process: In the event of a claim, insurance certificate holders may be required to cooperate with the insurance company. This includes providing necessary documentation, statements, or evidence to support the claim process. Timely and accurate cooperation is essential to facilitate the smooth resolution of any insurance claims.

7. Understanding Policy Coverage and Limitations: Insurance certificate holders should have a clear understanding of the policy’s coverage limits, exclusions, and limitations. This knowledge allows them to make informed decisions regarding their risk exposure and take appropriate actions to mitigate any potential gaps or vulnerabilities.

By fulfilling these roles and responsibilities, insurance certificate holders actively participate in the insurance process and help protect their interests in the policy. Clear communication, proactive monitoring, and staying informed are key to successfully navigating the responsibilities associated with being an insurance certificate holder.

Types of Insurance Certificate Holders

Insurance certificate holders can come in various forms, depending on the nature of the insured property or project and the parties involved. The type of insurance certificate holder determines their role, responsibility, and the level of interest they have in the insurance policy. Let’s explore some common types of insurance certificate holders:

1. Landlords: Landlords often require tenants to name them as insurance certificate holders. This arrangement ensures that the landlord is notified of any changes or cancellations to the insurance policy covering the rented property. It helps protect the landlord’s investment and provides them with proof of coverage in case of any claims or liability issues.

2. Lenders: When a property is financed, lenders typically require the borrower to have insurance coverage and name them as an insurance certificate holder. This ensures that the lender’s interest in the property is protected in case of any damage or loss. The insurance certificate holder status provides the lender with important updates on the insurance policy, giving them peace of mind that the property is adequately insured.

3. Contractors and Subcontractors: In construction projects, contractors and subcontractors may be required to name other parties, such as project owners or general contractors, as insurance certificate holders. This arrangement ensures that all parties involved are notified of any changes or cancellations to the insurance policy, and it helps manage the risk and liability associated with the project.

4. Vendors and Suppliers: Vendors and suppliers who provide goods or services to a business may be requested to name the business as an insurance certificate holder. This allows the business to be notified in case of any changes or cancellations to the vendor’s or supplier’s insurance coverage, protecting them from potential risks or liabilities associated with the products or services provided.

5. Event Organizers: When organizing events, such as conferences, concerts, or weddings, event organizers may require vendors, venues, or performers to name them as insurance certificate holders. This ensures that the event organizer is notified in case of any changes or cancellations to the insurance coverage, protecting them from potential issues or claims arising from the event.

6. Government Agencies: Government agencies often require contractors or businesses working on public projects to name them as certificate holders. This arrangement ensures that the government agency is informed of any changes or cancellations to the insurance coverage and that their interests are protected in case of any liability or damage claims.

These are just a few examples of common types of insurance certificate holders. The specific parties involved and the level of interest may vary depending on the industry, project, or contractual agreements. The inclusion of insurance certificate holders helps establish transparency, accountability, and risk mitigation among all parties involved in an insured property or project.

Benefits of Being an Insurance Certificate Holder

Being an insurance certificate holder comes with numerous benefits, providing individuals or organizations with added protection, peace of mind, and legal recognition. Let’s explore some of the key benefits that come with being an insurance certificate holder:

1. Enhanced Awareness: As an insurance certificate holder, you receive updates, notifications, and important information about the insurance policy. This ensures that you are aware of any changes, cancellations, or modifications to the coverage, enabling you to take necessary actions to safeguard your interests.

2. Risk Mitigation: By being named as an insurance certificate holder, you have a vested interest in the insured property or project. This allows you to proactively manage and mitigate risks associated with the property or project, ensuring that you are adequately protected from potential liabilities or losses.

3. Legal Recognition: Being named as an insurance certificate holder establishes a legal relationship between you and the primary insured. This recognition provides you with certain rights and protections, giving you a voice in the insurance process and ensuring that your interests are taken into consideration.

4. Compliance with Requirements: Many industries or contractual agreements require specific insurance coverage. By being an insurance certificate holder, you can meet these compliance requirements and demonstrate to clients, vendors, or partners that you have the necessary insurance coverage in place. This enhances your credibility and opens doors for business opportunities.

5. Proof of Insurance: As an insurance certificate holder, you have access to the insurance certificate, which serves as proof of insurance coverage. This document can be used to demonstrate to third parties, such as clients or regulatory authorities, that you are adequately insured, building trust and confidence in your operations.

6. Increased Accountability: Being an insurance certificate holder fosters a sense of accountability among all parties involved in the insurance policy. It ensures that the primary insured is aware of their responsibilities and obligations towards you as a certificate holder, promoting transparency and alignment between the parties.

7. Quick Response to Claims: In the event of a claim, as an insurance certificate holder, you have a direct line of communication with the insurance company. This can streamline the claims process and facilitate a quicker response, ensuring that your interests are protected and any potential losses are covered promptly.

These benefits highlight the value and importance of being an insurance certificate holder. Whether you are a landlord, lender, contractor, or any other party with a vested interest in an insured property or project, being named as an insurance certificate holder provides you with added protection, rights, and peace of mind.

Limitations and Considerations for Insurance Certificate Holders

While being an insurance certificate holder comes with its benefits, it is important to be aware of the limitations and considerations that come with this role. Understanding these factors will help you navigate the insurance process effectively and make informed decisions. Let’s delve into the limitations and considerations for insurance certificate holders:

1. No Control over Policy: As an insurance certificate holder, you do not have direct control over the insurance policy. The policy terms, coverage limits, and exclusions are determined by the primary insured in consultation with the insurance company. It’s crucial to understand the policy terms to ensure that it aligns with your needs and risk exposures.

2. Reliance on Primary Insured: Insurance certificate holders rely on the primary insured to maintain and update the insurance policy. Any lapses or changes in coverage made by the primary insured can directly impact the certificate holder’s level of protection. Regular communication and a strong partnership with the primary insured are essential to ensure continued coverage.

3. No Direct Claim Settlement: Insurance certificate holders typically do not have the authority to directly settle claims with the insurance company. In case of a claim, the primary insured is responsible for initiating the claims process. However, as a certificate holder, you may provide necessary documentation or evidence to support the claim and work closely with the primary insured to ensure a fair and timely settlement.

4. Limited Control over Policy Changes: Insurance certificate holders have limited control over changes to the insurance policy. Any modifications or endorsements to the policy may require the agreement and cooperation of both the primary insured and the insurance company. It’s important to maintain open lines of communication and address any concerns or necessary changes regarding the policy promptly.

5. Reliance on Accurate Information: Insurance certificate holders rely on the primary insured to provide accurate and up-to-date information regarding the policy. It’s crucial to review the insurance certificate and verify that your details are correctly mentioned. Any inaccuracies or omissions may affect the certificate holder’s ability to receive relevant updates and notifications from the insurance company.

6. Contractual Obligations: Insurance certificate holders should be mindful of any contractual obligations tied to the insurance policy. Depending on the agreements in place, there may be specific requirements or responsibilities that the certificate holder must fulfill. It’s important to review and understand the contract terms to ensure compliance and avoid any disputes or penalties.

7. Consider Individual Risk Exposure: While being an insurance certificate holder offers certain protections, it’s essential to evaluate your individual risk exposure. Additional insurance coverage beyond what is provided by the primary insured’s policy may be necessary to fully protect your interests. Consult with an insurance professional to assess your unique risk profile and determine if additional coverage is required.

By considering these limitations and factors, insurance certificate holders can navigate their role effectively and ensure that their interests are adequately protected. Open communication, a clear understanding of the policy terms, and proactive risk management are key to successfully managing the responsibilities of an insurance certificate holder.

Key Differences between Insurance Certificate Holders and Named Insured

While both insurance certificate holders and named insured are important elements in insurance policies, there are significant differences between them in terms of their roles, responsibilities, and level of involvement. Understanding these differences is crucial to grasp the dynamics and obligations associated with each party. Let’s explore the key differences between insurance certificate holders and named insured:

1. Policy Ownership: The named insured is the primary owner of the insurance policy. They are the individual or organization that purchases the policy, pays the premiums, and has the authority to make changes, renewals, or cancellations to the policy. On the other hand, insurance certificate holders do not have ownership rights to the policy but are listed as additional interested parties with a financial or legal interest in the insured property or project.

2. Decision-Making Authority: The named insured has the authority to make decisions regarding the policy, including choosing the coverage types, limits, and endorsements. They have the flexibility to tailor the policy to meet their specific needs. Insurance certificate holders, on the other hand, have minimal decision-making authority over the policy. They rely on the named insured to secure and maintain appropriate coverage.

3. Premium Payments: The named insured is responsible for paying the premiums associated with the insurance policy. They receive the invoices and bear the financial responsibility for ensuring that the policy remains in force. In contrast, insurance certificate holders are not obligated to pay any premiums or ongoing costs related to the policy.

4. Policy Updates and Notifications: The named insured receives updates, notifications, and policy-related documents directly from the insurance company. They are responsible for communicating any changes or important information to the insurance certificate holders. Insurance certificate holders, on the other hand, rely on the named insured or the insurance agent to inform them about policy updates, cancellations, or modifications that may impact their interests.

5. Rights and Obligations: The named insured has the rights and obligations outlined in the insurance policy. They enjoy the benefits of coverage and have the duty to comply with policy terms, including reporting claims within specified timeframes and providing accurate information to the insurance company. Insurance certificate holders have fewer rights and obligations, primarily revolving around being notified of policy changes or cancellations and potentially cooperating in the claims process.

6. Legal Relationship: The named insured has a direct legal relationship with the insurance company. They can directly initiate claims, negotiate settlements, and communicate with the insurer regarding policy matters. Insurance certificate holders have a legal relationship with the named insured, established through their inclusion on the insurance certificate. Their relationship with the insurer is generally limited to receiving important information and updates.

Understanding the distinctions between insurance certificate holders and named insured is crucial for all parties involved in an insurance policy. Clear communication, transparency, and collaboration between these two entities ensure that policy information is accurately shared, risks are adequately mitigated, and the interests of all stakeholders are protected.

Conclusion

Insurance certificate holders play a vital role in the realm of insurance, acting as additional interested parties with a financial or legal stake in the insured property or project. They offer an extra layer of protection, ensuring that their interests are safeguarded and that they are informed of any changes or cancellations to the insurance policy.

Throughout this article, we have explored the definition of insurance certificate holders, their importance, roles, responsibilities, and the benefits they enjoy. We have also discussed the limitations and considerations that come with being an insurance certificate holder, as well as the key differences between insurance certificate holders and named insured.

Being an insurance certificate holder grants individuals or organizations with a level of security, accountability, and compliance. It allows them to actively participate in the insurance process, make informed decisions, and mitigate risks associated with the insured property or project. By staying informed about policy updates, understanding policy coverage, and cooperating in the claims process, insurance certificate holders contribute to a transparent and accountable insurance ecosystem.

Ultimately, the inclusion of insurance certificate holders ensures that all parties involved have a vested interest in the insurance policy and work together to protect their respective interests. Clear communication, cooperation, and understanding of the roles and responsibilities associated with being an insurance certificate holder are essential for a successful and effective insurance partnership.

In conclusion, insurance certificate holders play a crucial role in the insurance landscape, providing additional protection, compliance, and accountability. Whether landlords, lenders, contractors, or any other party with a vested interest in an insured property or project, being a certificate holder offers distinct advantages and responsibilities. By embracing these responsibilities, staying engaged in the insurance process, and working closely with the named insured and insurance company, insurance certificate holders can ensure their interests are effectively protected in an ever-changing world of risk and insurance.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance