Home>Finance>Microcredit: Definition, How It Works, Loan Terms

Finance

Microcredit: Definition, How It Works, Loan Terms

Published: December 25, 2023

Learn about microcredit in finance, including its definition, how it works, and loan terms. Find out how this form of lending empowers individuals and spurs economic growth.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Microcredit: Definition, How It Works, Loan Terms

Welcome to our “Finance” category blog post, where we delve into various aspects of the world of finance. In this article, we will be exploring microcredit – a financial tool that has gained significant popularity in recent years. We will define microcredit, explain how it works, and provide an overview of common loan terms associated with it. So, let’s dive in!

Key Takeaways:

- Microcredit provides small loans to low-income individuals or underserved communities.

- These loans often help individuals start or expand small businesses, improving their financial well-being.

What is Microcredit?

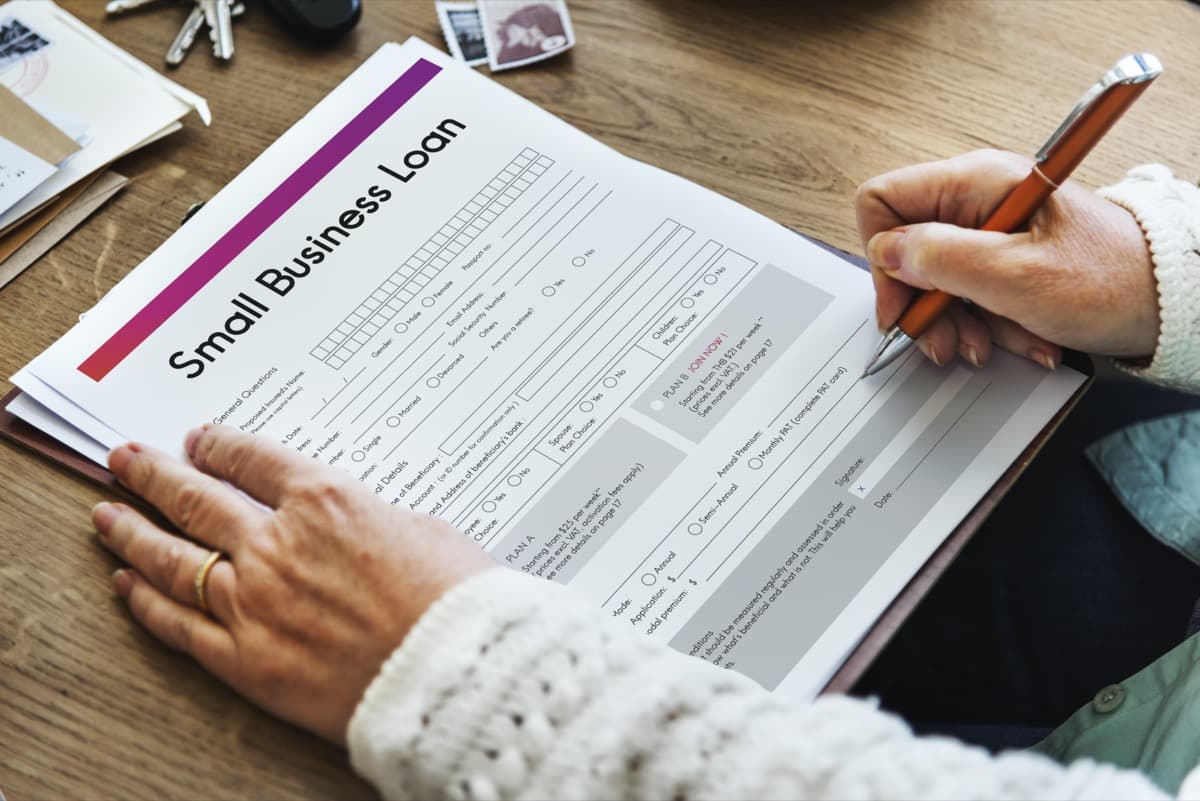

Microcredit is a financial service that aims to provide small loans to individuals who wouldn’t typically have access to traditional banking services. It is primarily targeted at low-income individuals or those living in underserved communities. The loans offered through microcredit programs are often relatively small, ranging from a few hundred to a few thousand dollars.

The concept of microcredit was popularized by Nobel Peace Prize laureate Muhammad Yunus, who believed that providing small loans to the poor could empower them to create sustainable income and lift themselves out of poverty. Microcredit programs operate around the world, with many operating in developing countries where access to credit is limited.

How Does Microcredit Work?

The process of obtaining a microcredit loan is generally more straightforward compared to traditional loan applications. Microcredit institutions typically offer loans without requiring extensive credit checks or collateral. Instead, they rely on other factors such as character and business potential to assess an applicant’s eligibility.

Microcredit loans often target aspiring entrepreneurs or individuals looking to expand their existing small businesses. The funds obtained through microcredit can be used for various purposes, such as purchasing equipment, raw materials, or inventory. Some borrowers even use the funds to invest in skills training or educational opportunities to enhance their business prospects.

To ensure repayment, microcredit institutions often require borrowers to form a group or join a lending circle. These groups provide social collateral, as members hold each other accountable for timely repayments. Additionally, microcredit loans may have shorter terms, typically ranging from a few months to a few years, making them more accessible and manageable for borrowers.

Loan Terms in Microcredit

Microcredit loans typically have unique terms and conditions tailored to meet the needs of low-income borrowers. Here are some common loan terms associated with microcredit:

- Loan Amount: Microcredit loans are relatively small, ranging from a few hundred to a few thousand dollars.

- Interest Rates: Microcredit loans often carry higher interest rates compared to traditional loans. This is due to the higher risk associated with lending to individuals with limited financial resources and limited credit history.

- Repayment Period: The repayment period for microcredit loans is generally shorter, typically ranging from a few months to a few years.

- Collateral: Microcredit loans are often issued without requiring collateral. This allows borrowers without valuable assets to access much-needed funds.

- Borrower Support: Microcredit institutions often provide additional support to borrowers, such as business training, mentorship, and assistance in creating a business plan.

Microcredit has proven to be an effective tool in promoting financial inclusion and empowering low-income individuals to improve their economic situation. By providing access to capital and support, microcredit enables borrowers to pursue their business aspirations, generate sustainable income, and ultimately break the cycle of poverty.

In conclusion, microcredit offers a lifeline to individuals and communities that lack access to traditional banking services. It unlocks opportunities, fosters entrepreneurship, and drives economic growth. Whether you’re a borrower or simply interested in understanding the dynamics of microcredit, we hope this article has shed some light on this impactful financial tool.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance