Finance

What Documents Are Needed For A Business Loan

Modified: December 30, 2023

Find out the essential documents required for a business loan in finance. Ensure a successful loan application with our helpful guide.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When starting or growing a business, having access to capital is crucial. Many business owners turn to business loans as a viable financing option to meet their financial needs. However, the loan application process can be complex and requires the submission of various documents to support the loan request.

In this article, we will explore the documents typically required for a business loan application. Understanding the necessary paperwork will help you prepare in advance and streamline the application process.

Securing a business loan can provide the necessary funds to invest in equipment, expand operations, hire additional staff, or even launch a new product. But lenders need to assess the risk involved in lending money, which is why they require specific documents to evaluate your business’s financial stability and ability to repay the loan.

By submitting the required documents, you demonstrate your commitment to transparency and credibility, increasing your chances of securing the loan.

It’s important to note that the specific documents required may vary depending on the lender and the type of loan you are applying for. However, there are common documents that most lenders typically request. Let’s delve into the key documents you should be prepared to provide when applying for a business loan.

Purpose of Article

The purpose of this article is to guide business owners and entrepreneurs on the documents they will need to gather and submit when applying for a business loan. By understanding the required documentation, individuals can be better prepared and increase their chances of securing the financing they need to grow their business.

Applying for a business loan can be a daunting task, especially for first-time borrowers. Many lenders have specific requirements and procedures that can vary, making it essential to have a clear understanding of what documents are needed.

By providing an overview of the common documents required for a business loan application, this article aims to provide clarity and help borrowers navigate the loan application process with confidence. It will also help borrowers avoid potential delays or rejections by ensuring they have all the necessary documentation ready.

Additionally, the article will highlight the importance of each document in the loan evaluation process. Lenders use these documents to assess the creditworthiness and financial stability of the business. By understanding why each document is necessary, business owners can better prepare and present their case to prospective lenders.

Furthermore, the article will emphasize the significance of proper organization and attention to detail when submitting the required documents. This will help borrowers present a professional and well-prepared loan application, instilling confidence in the lender’s decision-making process.

Ultimately, the goal of this article is to empower business owners and entrepreneurs by equipping them with the knowledge and understanding necessary to navigate the business loan application process successfully.

Understanding Business Loans

Before diving into the specific documents required for a business loan, it’s important to have a basic understanding of what a business loan entails. A business loan is a financial product that provides funds to businesses for various purposes, such as starting a new venture, expanding operations, purchasing equipment, or managing cash flow.

Business loans can be obtained from various sources, including traditional banks, online lenders, credit unions, and government-backed loan programs. The terms and conditions of the loan, including interest rates, repayment periods, and eligibility criteria, can vary depending on the lender and the type of loan.

Business loans are typically categorized into two main types: secured and unsecured. Secured loans require collateral, such as real estate, inventory, or equipment, which the lender can claim if the borrower defaults on the loan. Unsecured loans, on the other hand, do not require collateral but often have stricter eligibility criteria and higher interest rates.

Lenders evaluate several factors when considering a business loan application, including the business’s credit history, financial statements, industry performance, and the borrower’s personal credit score. The documents required for a business loan help provide lenders with the necessary information to evaluate the risk involved in lending to a particular business.

It’s important to note that securing a business loan is not solely based on the documents provided. Lenders also consider other factors, such as the business owner’s experience, industry outlook, and the overall viability of the business. However, submitting the required documents in a timely and organized manner is a crucial step in the loan application process.

Now that we have a basic understanding of business loans, let’s explore the common documents that lenders typically require when applying for financing.

Common Documents Required for Business Loans

When applying for a business loan, it’s important to be prepared with the necessary documents to support your loan application. While the specific requirements may vary depending on the lender and the type of loan, there are several common documents typically requested by lenders. These documents provide lenders with the information they need to assess the financial health of your business and make an informed decision about granting the loan.

Here are seven common documents you will likely need when applying for a business loan:

- Personal Identification Documents: Lenders often require personal identification documents, such as driver’s license, passport, or social security number, to verify your identity.

- Business Entity Documents: These documents establish the legal structure of your business and may include articles of incorporation, partnership agreement, or business registration documents.

- Financial Statements: Lenders typically request financial statements, including balance sheets, income statements, and cash flow statements, to evaluate your business’s financial performance and stability.

- Tax Returns: Providing personal and business tax returns for the past few years helps lenders assess your tax compliance and evaluate your business’s profitability.

- Business Plan: A well-prepared business plan outlines your company’s goals, strategies, market analysis, and financial projections. This document demonstrates your understanding of your industry and provides insight into your business’s potential for success.

- Collateral Documents: If you are applying for a secured loan, you will likely need to provide documents related to the collateral you are offering, such as property deeds, vehicle titles, or inventory lists.

- Legal and Regulatory Documents: Depending on your industry and business type, lenders may request licenses, permits, certifications, or other legal and regulatory documents to ensure your business is compliant and operating within the required guidelines.

It’s important to note that these are general documents commonly requested by lenders. The specific requirements may vary based on the lender’s policies and the nature of your business. It’s crucial to review the lender’s guidelines and ask for clarification if you have any doubts about the required documents.

By ensuring you have these documents readily available and organized, you can streamline the loan application process and improve your chances of securing the financing you need for your business.

Personal Identification Documents

When applying for a business loan, lenders typically require personal identification documents to verify your identity and ensure that you are authorized to represent the business. These documents help establish your personal background and credibility, and they play a crucial role in the loan application process.

The specific personal identification documents that lenders typically request may include:

- Driver’s license

- Passport

- Social security number

- Birth certificate

These documents serve as proof of your identity, address, and legal status. Lenders need this information to validate your personal information and ensure that you are a responsible borrower.

Personal identification documents are essential because lenders want to confirm that you are who you say you are. These documents also help prevent identity theft and fraud, protecting both you and the lender.

When submitting personal identification documents, it’s important to ensure that they are current, valid, and not expired. Any discrepancies or inconsistencies in your personal information can raise concerns for lenders, so it’s crucial to double-check the accuracy of the information provided.

By having these personal identification documents readily available when applying for a business loan, you can expedite the application process and demonstrate your commitment to transparency and credibility. It’s essential to keep copies of these documents for your own records, as they may be required for other business-related activities such as signing contracts or leasing agreements.

Remember, the specific personal identification documents required may vary depending on the lender and the type of loan. It’s always a good idea to review the lender’s guidelines and ask for clarification if you have any questions or concerns about the required documents.

Now that you understand the importance of personal identification documents let’s move on to the next set of documents commonly required for a business loan: business entity documents.

Business Entity Documents

When applying for a business loan, it’s important to provide the necessary business entity documents to establish the legal structure of your business. These documents help lenders verify the existence and legitimacy of your business, as well as understand the ownership and organizational structure.

The specific business entity documents that lenders typically request may depend on the legal structure of your business, such as:

- Articles of incorporation: This document is required for businesses that are registered as corporations. It includes important details about the company, such as its name, purpose, shareholders, and registered agent.

- Partnership agreement: For businesses operating as partnerships, lenders may request a partnership agreement that outlines the responsibilities, profit-sharing, and decision-making processes among the partners.

- Business registration documents: If your business is a sole proprietorship or a limited liability company (LLC), lenders may require registration documents that prove the existence and registration of your business with the appropriate government authorities.

- Operating agreement: This document is typically needed for LLCs and outlines how the business is managed and the responsibilities of the members or managers.

These business entity documents are crucial because they provide information about the legal structure of your business and who has the authority to enter into financial agreements. Lenders need this information to ensure that they are entering into a loan agreement with a legitimate and properly established entity.

It’s important to keep these business entity documents up to date and readily available when applying for a business loan. They may need to be notarized or certified, depending on the lender’s requirements.

Remember, the specific business entity documents required may vary depending on your business’s legal structure and the lender’s policies. It’s always a good idea to review the lender’s guidelines and ask for clarification if you have any questions or concerns about the required documents.

Next, we’ll explore the financial statements that lenders typically request for a business loan application.

Financial Statements

Financial statements are vital documents that lenders require when evaluating a business loan application. These statements provide a comprehensive snapshot of your business’s financial health and performance. Lenders carefully analyze these statements to assess your ability to repay the loan and manage your finances effectively.

The specific financial statements that lenders typically request may include:

- Balance Sheet: A balance sheet presents your business’s assets, liabilities, and equity at a specific point in time. It provides a clear picture of your business’s financial position.

- Income Statement: Also known as a profit and loss statement, the income statement shows your business’s revenues, expenses, and net income or loss over a specific period. It helps lenders evaluate your business’s profitability.

- Cash Flow Statement: The cash flow statement shows the sources and uses of cash within your business over a specific period. It demonstrates the ability to generate cash and manage expenses.

- Statement of Retained Earnings: This statement outlines the changes in your business’s retained earnings during a specific period. It shows how profits and dividends affect the accumulated earnings of the business.

These financial statements should be prepared in accordance with generally accepted accounting principles (GAAP) and accurately reflect your business’s financial performance and position. They provide vital information about your revenue, expenses, assets, and debts, allowing lenders to assess your ability to generate income and manage your liabilities.

It’s essential to ensure that your financial statements are up to date and accurately prepared. Lenders may request financial statements for the current year as well as the past two to three years to assess your business’s historical financial performance.

Preparing financial statements can be complex, especially if you are not familiar with accounting principles. It’s advisable to work with a certified public accountant (CPA) or an experienced financial professional to ensure the accuracy and completeness of your financial statements.

By providing well-prepared and accurate financial statements, you demonstrate transparency and financial stability, increasing your credibility as a borrower. These statements showcase your business’s ability to meet loan repayment obligations and manage future financial responsibilities.

Next, we’ll discuss another essential document that lenders typically require: tax returns.

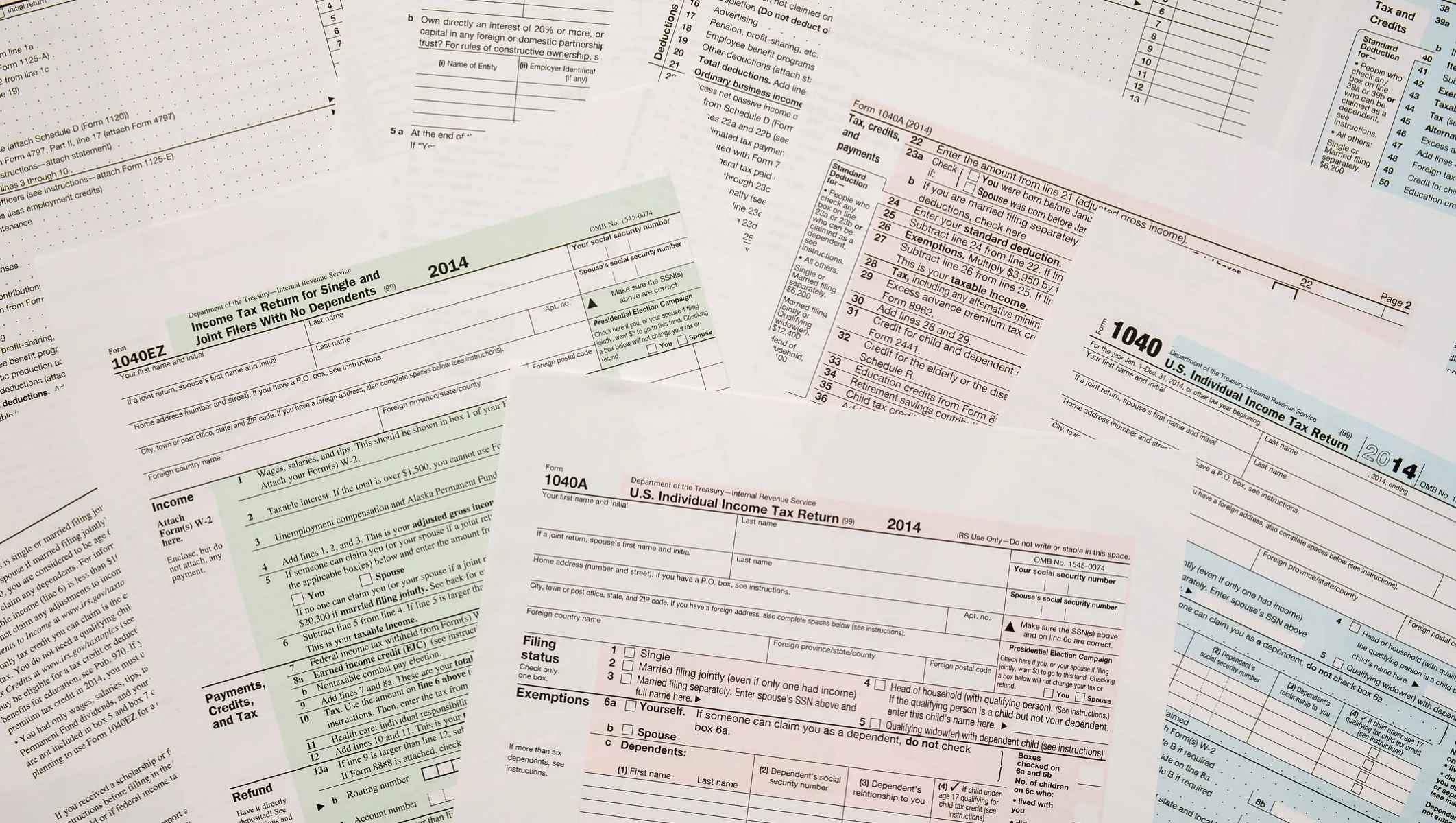

Tax Returns

When applying for a business loan, lenders typically request both personal and business tax returns for a specific period. Tax returns are essential documents that provide valuable insights into your business’s financial stability, tax compliance, and profitability.

The specific tax returns that lenders typically request may include:

- Personal Tax Returns: Lenders often require personal tax returns, including Form 1040, to assess your personal financial situation and determine your overall income.

- Business Tax Returns: Business tax returns, such as Form 1120 for corporations or Form 1065 for partnerships, help lenders evaluate your business’s financial performance, profitability, and tax compliance.

By reviewing your tax returns, lenders can verify the accuracy of the financial information you have provided and assess your consistency in reporting income and expenses. Tax returns also provide insights into your business’s historical financial performance, allowing lenders to evaluate its stability and capacity to generate profits.

Lenders typically request tax returns for the past two to three years, although this may vary depending on the lender’s requirements. It’s essential to ensure that your tax returns are accurately prepared and up to date.

It’s advisable to work with a qualified tax professional or certified public accountant (CPA) to complete your tax returns accurately and leverage any available deductions or tax benefits. This can help you maximize your business’s profitability and positively impact your loan application.

Keep in mind that lenders may also request additional documents related to your tax returns, such as schedules, W-2 forms, or 1099 forms. Be prepared to provide these supplementary documents if required.

By providing complete and accurate tax returns, you demonstrate your business’s tax compliance, financial stability, and ability to meet loan repayment obligations. This instills confidence in the lender and increases your chances of securing the business loan you need.

As we move forward, we will explore another crucial document that lenders typically require: the business plan.

Business Plan

One important document that lenders typically require when applying for a business loan is a well-prepared business plan. A business plan is a comprehensive document that outlines your company’s goals, strategies, market analysis, and financial projections.

A business plan serves as a roadmap for your business’s future and helps lenders evaluate the viability and potential profitability of your venture. It demonstrates your understanding of your industry, market conditions, and target audience. Additionally, it showcases your ability to strategize and effectively manage resources.

The key components of a business plan typically include:

- Executive Summary: A concise overview of your business and its objectives.

- Business Description: A detailed description of your company, including its products or services, target market, and competitive advantages.

- Market Analysis: An assessment of your industry, target market, competitors, and market trends.

- Organization and Management: Details about your company’s organizational structure, key personnel, and management team.

- Product or Service Line: A description of your offerings, including features, benefits, and any intellectual property rights.

- Sales and Marketing Strategy: Your approach to reaching customers, acquiring market share, and growing sales.

- Financial Projections: Projected financial statements, such as income statements, balance sheets, and cash flow statements, for a specific period.

- Funding Request and Repayment Plan: A clear explanation of the loan amount you are seeking and how you plan to repay it, including a discussion of collateral (if applicable).

A well-prepared business plan demonstrates your commitment to your business’s success and provides lenders with critical insights into its potential. It allows lenders to assess the overall financial health of your business, including revenue projections, profitability, and cash flow management.

When preparing your business plan, it’s important to be realistic and back up your claims with relevant market research and data. Be sure to highlight your competitive edge, unique selling propositions, and marketing strategies. Additionally, include any relevant industry experience or track record that showcases your ability to execute your business plan successfully.

A business plan can be an extensive document, so it’s crucial to organize the content effectively, use clear and concise language, and include supporting visuals and data where appropriate. Consider reviewing sample business plans or consulting with business advisors or mentors to ensure a comprehensive and professional presentation.

By providing a well-crafted business plan, you demonstrate your preparedness and strategic thinking, increasing your chances of securing the business loan you need to fuel growth and success.

Next, we will explore another set of documents that may be required for certain types of business loans: collateral documents.

Collateral Documents

When applying for a secured business loan, lenders may require you to provide collateral to secure the loan. Collateral is an asset or property that you pledge as security against the loan. If you default on the loan, the lender can seize and sell the collateral to recover their funds.

The specific collateral documents that lenders typically request may depend on the type of collateral you are offering. Common types of collateral can include real estate, equipment, inventory, or accounts receivable. The documents required may include:

- Property Deeds: If you are pledging real estate as collateral, lenders may request property deeds or titles to prove ownership and establish the value of the property.

- Vehicle Titles: If you are pledging vehicles as collateral, lenders may ask for vehicle titles to verify ownership and determine their value.

- Inventory Lists: If you are using inventory as collateral, lenders may require detailed inventory lists, including descriptions, quantities, and estimated values.

- Accounts Receivable Aging Reports: If you are using accounts receivable as collateral, lenders may request aging reports to assess the value and collectability of outstanding invoices.

Collateral documents are necessary to validate the existence, value, and ownership of the collateral being pledged. These documents provide lenders with a clear understanding of the assets securing the loan and their potential value if the loan goes into default.

It’s crucial to ensure that your collateral documents are complete, accurate, and up to date. Lenders may require appraisals or inspections to determine the value of the collateral, so be prepared to provide any supporting documentation related to the collateral’s condition and market value.

Additionally, it’s important to note that the value of the collateral typically determines the loan amount you can borrow. Lenders may offer a loan amount that is a percentage of the collateral’s appraised value, ensuring that there is sufficient security in case of default.

Remember, collateral is a risk mitigation measure for the lender and provides reassurance in the event of a loan default. By providing the required collateral documents, you demonstrate your commitment to repay the loan and protect the lender’s interests.

As we approach the end of our discussion on common documents required for a business loan, let’s explore the final section: legal and regulatory documents.

Legal and Regulatory Documents

When applying for a business loan, lenders may request certain legal and regulatory documents to ensure your business is compliant with applicable laws and regulations. These documents provide lenders with assurance that your business is operating within the legal framework and abiding by industry-specific rules and requirements.

The specific legal and regulatory documents that lenders commonly request may vary depending on the nature of your business and the industry you operate in. Some examples of these documents include:

- Business Licenses and Permits: Lenders may require copies of any required licenses or permits that your business needs to operate legally. These documents can vary depending on the industry and the location of your business.

- Professional Certifications: If your business requires specific professional certifications or qualifications, lenders may request proof of these credentials.

- Contracts and Agreements: Lenders may request copies of any key contracts or agreements that are central to your business operations, such as lease agreements, customer contracts, or partnership agreements.

- Insurance Policies: Lenders may ask for documentation of your business insurance policies, such as liability insurance or property insurance.

- Compliance Certificates: Certain industries have specific regulatory requirements. Lenders may require compliance certificates or documentation that demonstrates your business’s adherence to these regulations.

Providing these legal and regulatory documents is essential to demonstrate that your business is operating lawfully and minimizing potential risks. It establishes your credibility as a responsible business owner who maintains compliance with legal and industry standards.

Before applying for a business loan, it’s crucial to review the specific legal and regulatory requirements of your industry and location. This way, you can ensure that you have all the necessary documents ready and up to date.

Working with legal counsel or industry experts can be beneficial in ensuring that you have the proper licenses, permits, and certifications required for your business. They can also assist in reviewing your contracts, agreements, and insurance policies to ensure they meet the lender’s requirements.

Remember, the lender’s objective in requesting these documents is to minimize their risk and ensure that your business operates legally and responsibly. By providing the necessary legal and regulatory documents, you demonstrate your commitment to compliance and increase your credibility as a borrower.

With the discussion of the common documents required for a business loan now complete, it’s important to remember that these are general requirements and may vary depending on the lender and the type of loan. To ensure a smoother loan application process, carefully review the lender’s guidelines and ask for clarification if you have any questions or concerns about the required documents.

Now that you have a comprehensive understanding of the documents typically required for a business loan, you can confidently prepare your loan application and improve your chances of securing the financing you need to fuel your business’s growth and success.

Good luck with your loan application!

Conclusion

Applying for a business loan requires careful planning and preparation. Understanding the common documents required by lenders can streamline the loan application process and increase your chances of securing the financing you need. Throughout this article, we have explored the key documents typically requested when applying for a business loan.

Personal identification documents such as driver’s licenses and passports establish your identity and authorization to represent the business. Business entity documents, such as articles of incorporation or partnership agreements, illustrate the legal structure and ownership of your business.

Financial statements provide lenders with insights into your business’s financial health, including its assets, liabilities, income, and expenses. Tax returns demonstrate your tax compliance and financial performance over a specified period. A well-prepared business plan showcases your understanding of your industry, market analysis, and strategies for success.

For secured loans, collateral documents prove the ownership and value of assets pledged as security. Legal and regulatory documents ensure your business is compliant with relevant laws, regulations, and industry requirements.

By submitting these documents, you demonstrate transparency, credibility, and financial stability to the lender. It’s crucial to ensure that all documents are accurate, up to date, and well-organized to present a professional loan application.

Remember that the specific documents required may vary depending on the lender and the type of loan. Always review the lender’s guidelines and ask for clarification if needed.

Preparing all the required documents ahead of time will save you valuable time during the loan application process and increase the likelihood of a successful loan approval. Collaborating with professionals, such as accountants or legal advisors, can further streamline the process and address any potential gaps or concerns.

Securing a business loan can provide the necessary financial resources to fuel your business’s growth, invest in new initiatives, or overcome temporary cash flow challenges. With a thorough understanding of the documents required and proper preparation, you can confidently approach lenders and optimize your chances of obtaining the financing you need.

Best of luck in your business loan application journey!

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance