Finance

What Happens When You Miss A Minimum Payment

Published: February 27, 2024

Discover the consequences of missing a minimum payment in the world of finance. Learn how it can affect your credit score and financial stability.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

**

Introduction

**

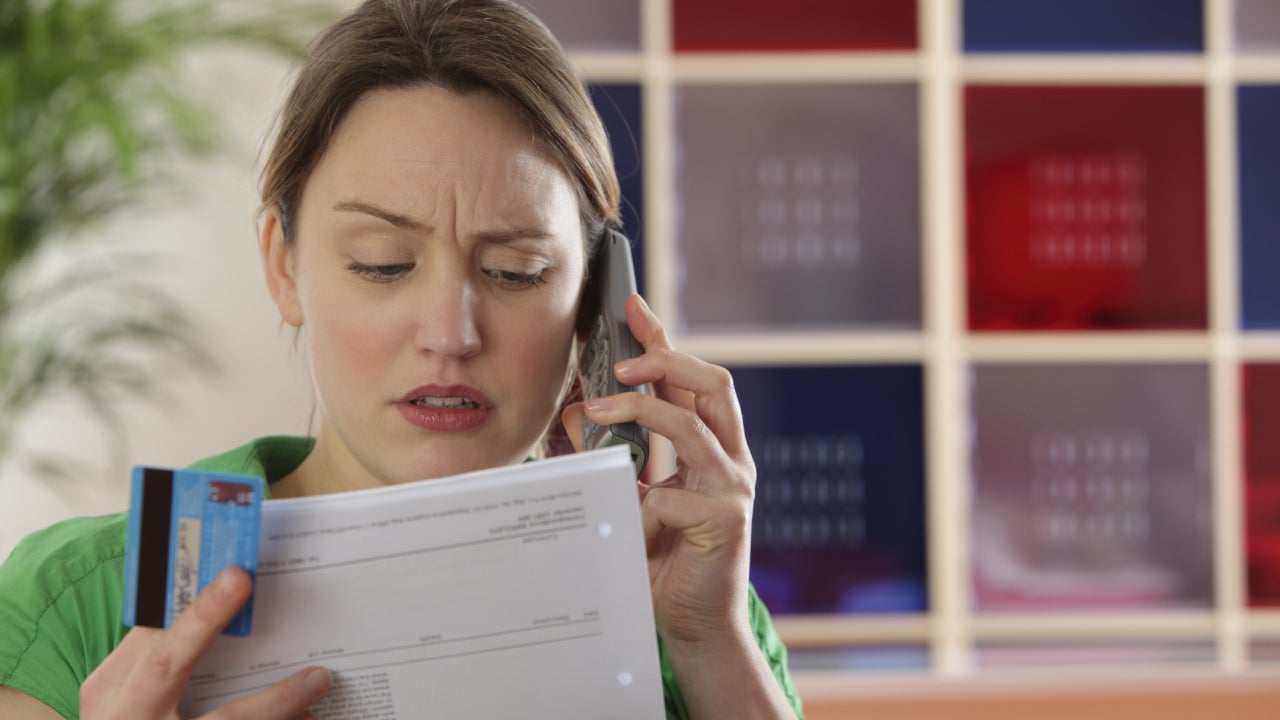

Welcome to the complex world of personal finance, where every decision can have a profound impact on your financial well-being. One such critical aspect is managing minimum payments on credit accounts. In this article, we will delve into the implications of missing a minimum payment, shedding light on the repercussions that can unfold when this obligation is not met.

At first glance, a minimum payment may seem like a routine task, just another item on your monthly financial checklist. However, the significance of this seemingly mundane requirement cannot be overstated. Whether it's a credit card, loan, or any other form of credit, failing to meet the minimum payment can trigger a cascade of adverse consequences that extend beyond the immediate financial realm.

By exploring the potential fallout of missing a minimum payment, we aim to equip you with the knowledge needed to navigate the intricacies of credit management. Understanding the implications of such a misstep is crucial for maintaining financial stability and safeguarding your creditworthiness.

In the following sections, we will dissect the concept of minimum payments, elucidate the ramifications of failing to meet this obligation, and offer insights into mitigating the fallout. By the end of this journey, you will emerge with a deeper understanding of the pivotal role that minimum payments play in the broader tapestry of personal finance. Let's embark on this exploration to unravel the intricacies of missed minimum payments and their far-reaching effects.

**

Understanding Minimum Payments

**

To comprehend the significance of minimum payments, it is essential to grasp their underlying purpose. When you borrow money through a credit card or a loan, the minimum payment represents the smallest amount you are required to repay each month to keep the account in good standing. This amount is typically calculated as a percentage of the total balance, subject to a minimum threshold.

While meeting the minimum payment may seem like a routine task, it serves as a crucial mechanism for lenders to ensure a steady inflow of funds and mitigate the risk of default. By adhering to this requirement, borrowers demonstrate their commitment to repaying the borrowed funds, thereby upholding the terms of the credit agreement.

However, it is important to recognize that making only the minimum payment can lead to long-term financial repercussions. This is primarily due to the accrual of interest on the remaining balance, potentially resulting in a protracted repayment period and increased interest costs. As such, while the minimum payment fulfills the immediate obligation, striving to pay more than the minimum can significantly reduce the overall interest burden and expedite the debt repayment process.

Moreover, understanding the components of the minimum payment is crucial. In addition to the interest accrued on the outstanding balance, the minimum payment encompasses a portion of the principal amount, ensuring a gradual reduction of the debt over time. By comprehending the composition of the minimum payment, borrowers can make informed decisions regarding their repayment strategy and strive to minimize the overall interest expenditure.

By gaining a comprehensive understanding of minimum payments, borrowers can navigate the intricacies of credit management with greater acumen. In the subsequent sections, we will explore the ramifications of missing a minimum payment, shedding light on the multifaceted implications that can ensue from this seemingly innocuous oversight.

**

Consequences of Missing a Minimum Payment

**

Missing a minimum payment on a credit account can trigger a cascade of adverse consequences that reverberate across various facets of your financial landscape. The repercussions of this oversight extend beyond the immediate financial implications, permeating into areas such as creditworthiness, cost escalation, and future borrowing opportunities.

One of the immediate consequences of missing a minimum payment is the incurring of late fees. Lenders typically impose a penalty for failing to meet the minimum payment deadline, resulting in additional financial strain. Moreover, the missed payment can lead to the activation of a penalty Annual Percentage Rate (APR), leading to a surge in the cost of carrying the outstanding balance. This escalation in interest charges can further compound the financial burden, amplifying the overall cost of the debt.

Furthermore, the impact on credit scores cannot be understated. Payment history constitutes a significant component of credit scoring models, and a missed minimum payment can tarnish your credit profile. This can diminish your credit score, potentially limiting your access to favorable credit terms in the future. The negative mark on your credit report resulting from a missed payment can endure for several years, exerting a lingering impact on your creditworthiness.

Additionally, missing a minimum payment can lead to strained relationships with creditors. It can erode the trust and confidence that lenders place in borrowers, potentially impeding future credit opportunities and jeopardizing existing credit relationships. This can manifest as reduced flexibility in negotiating credit terms and may hinder your ability to secure favorable financing options in the future.

By comprehending the far-reaching consequences of missing a minimum payment, borrowers can appreciate the gravity of this oversight and take proactive measures to mitigate its impact. In the subsequent sections, we will delve into the specific repercussions on credit scores, late fees, and future credit opportunities, offering insights into navigating the aftermath of a missed minimum payment.

**

Impact on Credit Score

**

The ramifications of missing a minimum payment extend deeply into the realm of credit scoring, wielding a profound influence on your credit profile. Payment history stands as a pivotal factor in credit scoring models, carrying significant weight in determining your creditworthiness. As such, a missed minimum payment can cast a shadow over your credit report, potentially tarnishing your credit score and impeding your financial prospects.

When a minimum payment is not made by the due date, the creditor may report the delinquency to the credit bureaus. This adverse mark on your credit report can significantly diminish your credit score, signaling to potential lenders that you may pose a heightened risk. Consequently, a lower credit score can curtail your access to favorable credit terms, impeding your ability to secure loans, credit cards, or other forms of financing at competitive interest rates.

Moreover, the impact of a missed payment on your credit score can endure for an extended duration. While the exact duration may vary, negative entries resulting from missed payments can linger on your credit report for up to seven years. During this period, the diminished credit score can impede your financial maneuverability, casting a shadow over your creditworthiness and hampering your ability to secure credit on favorable terms.

Furthermore, a lower credit score can reverberate beyond the realm of credit, affecting areas such as insurance premiums, rental applications, and even employment opportunities. Many insurers, landlords, and prospective employers assess credit scores as a measure of financial responsibility, and a diminished credit score stemming from missed payments can undermine your prospects in these domains.

By comprehending the enduring impact of missed payments on credit scores, borrowers can appreciate the gravity of this repercussion and take proactive measures to safeguard their creditworthiness. In the subsequent sections, we will delve into strategies for mitigating the impact of missed payments on credit scores, offering insights into navigating the aftermath of this adverse event.

**

Late Fees and Penalty APR

**

When a minimum payment is missed, one of the immediate consequences that borrowers encounter is the imposition of late fees by the creditor. These fees serve as a punitive measure for failing to meet the payment deadline, compounding the financial burden associated with the delinquency. The exact amount of late fees can vary among creditors, potentially escalating the overall cost of the missed payment.

Moreover, missing a minimum payment can trigger the activation of a penalty Annual Percentage Rate (APR) on the outstanding balance. The penalty APR represents an elevated interest rate that lenders may levy as a consequence of delinquency. This heightened APR can substantially increase the cost of carrying the outstanding balance, resulting in a surge in interest charges that exacerbates the financial strain stemming from the missed payment.

Furthermore, it is crucial to recognize that the imposition of late fees and penalty APR can perpetuate a cycle of financial strain, compounding the challenges associated with the missed payment. As the outstanding balance accrues additional interest at a heightened rate, the overall cost of the debt can escalate, potentially prolonging the repayment period and amplifying the financial burden on the borrower.

By comprehending the implications of late fees and penalty APR, borrowers can gain insight into the multifaceted repercussions of missing a minimum payment. In the subsequent sections, we will explore strategies for mitigating the impact of late fees and penalty APR, offering insights into navigating the aftermath of a missed minimum payment and alleviating the associated financial strain.

**

Repercussions on Future Credit

**

When a minimum payment is missed, the repercussions extend beyond the immediate financial penalties and can significantly impact future credit opportunities. The negative mark resulting from a missed payment can tarnish your credit report, potentially undermining your creditworthiness and impeding your ability to secure favorable credit terms in the future.

One notable repercussion is the potential restriction on access to credit. Lenders may perceive a history of missed payments as a red flag, leading to heightened scrutiny and potentially limiting your access to credit. Even if credit is extended, it may come with less favorable terms, such as higher interest rates or lower credit limits, reflecting the heightened risk associated with the tarnished payment history.

Moreover, the impact on future credit extends to existing credit relationships. Lenders may reevaluate the terms of your existing credit accounts, potentially imposing stricter conditions or reducing credit limits in response to the perceived risk stemming from missed payments. This can curtail your financial flexibility and impede your ability to effectively manage your credit obligations.

Furthermore, the repercussions of missed payments can endure for an extended duration. Negative entries on your credit report resulting from missed payments can linger for up to seven years, exerting a prolonged impact on your creditworthiness and influencing lenders’ perceptions of your financial responsibility. During this period, the tarnished payment history can impede your ability to secure credit on favorable terms, constraining your financial options.

By comprehending the enduring repercussions of missed payments on future credit, borrowers can appreciate the gravity of this repercussion and take proactive measures to mitigate its impact. In the subsequent sections, we will delve into strategies for navigating the aftermath of missed minimum payments and safeguarding future credit opportunities, offering insights into mitigating the long-term repercussions of this adverse event.

**

Options for Dealing with Missed Minimum Payments

**

When faced with a missed minimum payment, it is imperative to address the situation proactively to mitigate the repercussions and safeguard your financial well-being. Several options are available to navigate the aftermath of a missed payment and alleviate the associated financial strain.

One viable option is to communicate with the creditor and seek clemency for the missed payment. Many creditors offer hardship programs or forbearance options that can provide temporary relief for borrowers facing financial difficulties. By reaching out to the creditor and explaining the circumstances that led to the missed payment, you may be able to negotiate a modified payment plan or seek to waive the associated late fees, thereby alleviating the immediate financial burden.

Another avenue to consider is consolidating the debt through a balance transfer or debt consolidation loan. By consolidating multiple debts into a single account with a lower interest rate, you can streamline your repayment process and potentially reduce the overall interest burden. This can provide a structured approach to managing the outstanding balance and mitigate the financial strain stemming from the missed payment.

Moreover, it is crucial to reassess your budget and financial priorities to prevent future missed payments. By reevaluating your expenses, prioritizing debt repayment, and establishing a robust budgeting framework, you can fortify your financial resilience and mitigate the risk of future delinquencies. Implementing automated payments or setting up reminders for payment deadlines can also serve as effective safeguards against missed payments.

Seeking the guidance of a reputable credit counseling agency can also provide valuable insights and assistance in managing missed payments. Credit counselors can offer tailored advice, debt management plans, and financial education to help you navigate the aftermath of missed payments and regain financial stability.

By exploring these options and taking proactive measures to address missed minimum payments, borrowers can mitigate the repercussions and chart a course toward financial recovery. In the subsequent sections, we will delve into strategies for navigating the aftermath of missed minimum payments, offering insights into safeguarding your financial well-being and mitigating the impact of delinquencies on your credit profile.

**

Conclusion

**

The management of minimum payments on credit accounts holds profound implications for an individual’s financial well-being. A missed minimum payment can unleash a cascade of adverse consequences, permeating into areas such as credit scores, cost escalation, and future credit opportunities. Understanding the multifaceted repercussions of missed payments is pivotal for navigating the complexities of credit management and safeguarding one’s financial stability.

By comprehending the enduring impact of missed payments on credit scores, borrowers can appreciate the gravity of this repercussion and take proactive measures to safeguard their creditworthiness. The enduring repercussions on future credit underscore the importance of addressing missed payments proactively and implementing strategies to mitigate their impact.

Options such as communicating with creditors, exploring debt consolidation, reassessing financial priorities, and seeking guidance from credit counseling agencies can serve as valuable tools for navigating the aftermath of missed minimum payments. By embracing these options and taking proactive measures to address missed payments, borrowers can mitigate the repercussions and chart a course toward financial recovery.

As we conclude this exploration of missed minimum payments and their far-reaching effects, it is imperative to underscore the significance of proactive credit management. By cultivating financial resilience, fortifying budgeting frameworks, and seeking assistance when needed, individuals can mitigate the risk of missed payments and uphold their financial well-being.

Ultimately, the awareness and proactive management of minimum payments stand as pillars of financial prudence, empowering individuals to navigate the complexities of credit and safeguard their financial stability. By heeding the insights offered in this exploration, borrowers can fortify their financial resilience and chart a path toward a more secure financial future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance