Finance

What Is The Billing Cycle For Medicare?

Published: March 7, 2024

Learn about the Medicare billing cycle and how it impacts your finances. Understand the key aspects of Medicare billing to manage your expenses effectively.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Understanding the billing cycle for Medicare is crucial for individuals enrolled in this government health insurance program. Medicare, which primarily serves people aged 65 and older, as well as younger individuals with disabilities, consists of several parts, each with its own unique billing cycle. This article will delve into the intricacies of Medicare billing, shedding light on the billing cycles for Medicare Parts A, B, C, and D.

Navigating the complexities of Medicare billing can be daunting, but gaining insight into the billing cycles for each part can help beneficiaries better manage their healthcare expenses. By understanding when and how Medicare bills for its various services, individuals can make informed decisions about their healthcare needs and ensure timely payment of premiums and other costs associated with the program.

Medicare plays a pivotal role in providing essential healthcare coverage to millions of Americans, and comprehending its billing cycles is essential for both beneficiaries and healthcare providers. In the following sections, we will explore the billing cycles for each part of Medicare, shedding light on the timelines and processes involved in billing for Medicare Part A, Part B, Part C, and Part D. Understanding these billing cycles is key to maximizing the benefits of Medicare and ensuring seamless access to vital healthcare services.

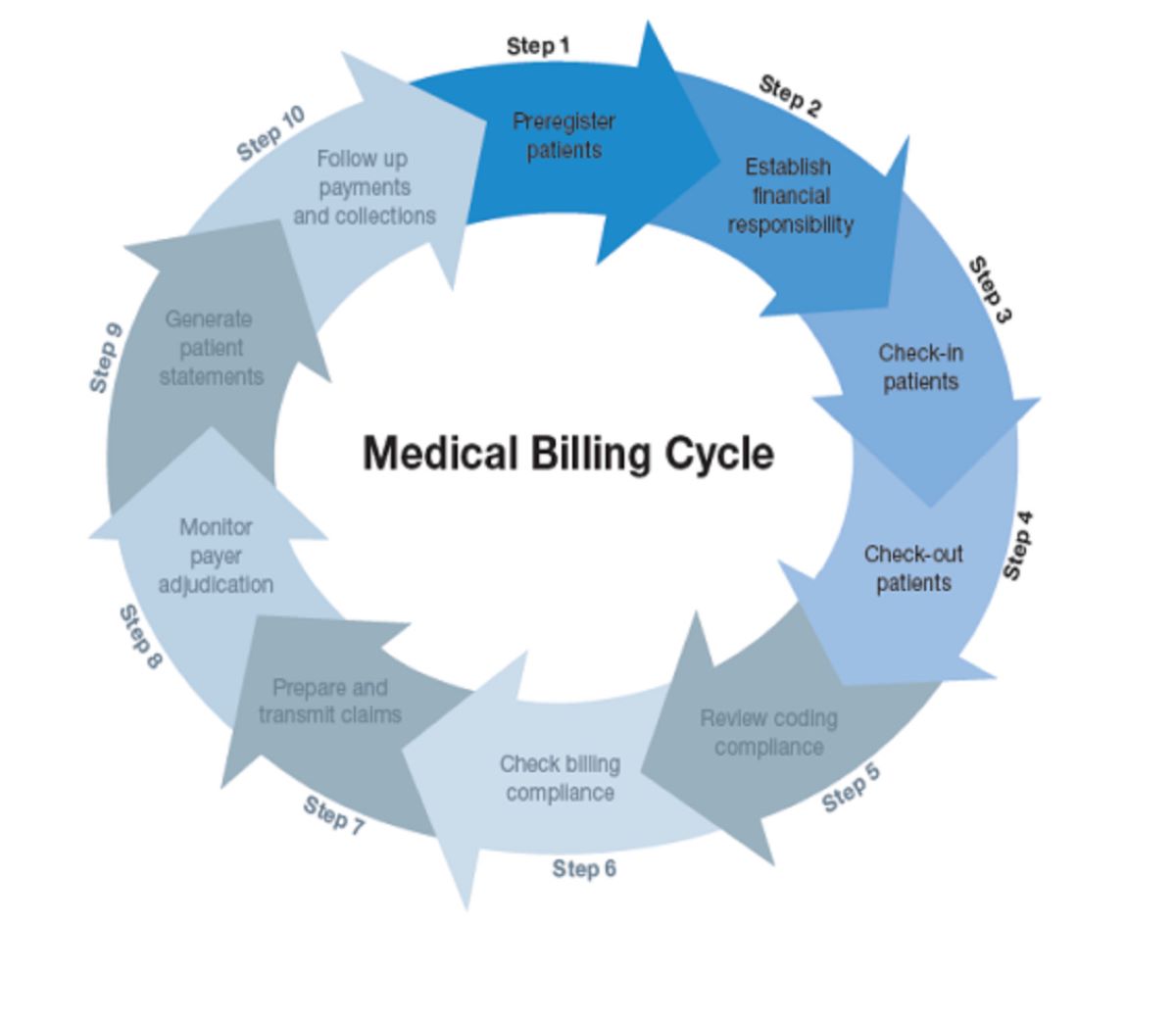

Understanding Medicare Billing

Medicare billing encompasses the process through which the program charges for the healthcare services it covers. This involves various aspects, including premiums, deductibles, copayments, and coinsurance. Understanding Medicare billing is essential for beneficiaries to comprehend their financial responsibilities and make informed decisions regarding their healthcare needs.

Medicare billing is structured into different parts, each with its own billing cycle and cost-sharing requirements. Medicare Part A primarily covers inpatient hospital care, skilled nursing facility care, hospice care, and some home health care services. Beneficiaries are generally eligible for premium-free Part A coverage if they or their spouse paid Medicare taxes while working. However, there are deductibles and coinsurance costs associated with Part A services, and the billing cycle for these expenses varies depending on the type of care received.

Medicare Part B, on the other hand, covers medically necessary services such as doctor’s visits, outpatient care, preventive services, and durable medical equipment. Beneficiaries are required to pay a monthly premium for Part B coverage, along with an annual deductible and coinsurance for the services received. The billing cycle for Medicare Part B involves monthly premium payments and potential out-of-pocket costs for covered services.

Medicare Part C, also known as Medicare Advantage, is offered through private insurance companies approved by Medicare. These plans provide the same coverage as Part A and Part B, and often include additional benefits such as prescription drug coverage, dental care, and vision services. The billing cycle for Medicare Part C involves premiums, deductibles, and cost-sharing arrangements determined by the specific Medicare Advantage plan selected by the beneficiary.

Lastly, Medicare Part D offers prescription drug coverage through private plans that are approved by Medicare. Beneficiaries enrolled in Part D plans pay a monthly premium and may be subject to annual deductibles, copayments, and coinsurance for their prescription medications. Understanding the billing cycle for Medicare Part D is crucial for beneficiaries to effectively manage their prescription drug expenses.

Overall, comprehending the nuances of Medicare billing is essential for beneficiaries to make informed decisions about their healthcare coverage and associated costs. By understanding the billing cycles for each part of Medicare and the financial obligations they entail, individuals can navigate the healthcare system with greater confidence and ensure timely payment for the services they receive.

Medicare Part A Billing Cycle

Medicare Part A, often referred to as hospital insurance, covers inpatient hospital care, skilled nursing facility care, hospice care, and some home health care services. Understanding the billing cycle for Medicare Part A is essential for beneficiaries to manage their financial responsibilities and make informed decisions about their healthcare needs.

For most beneficiaries, Medicare Part A is premium-free if they or their spouse paid Medicare taxes while working. However, there are cost-sharing requirements associated with Part A services, including deductibles and coinsurance. The billing cycle for Medicare Part A expenses varies depending on the type of care received.

For inpatient hospital care, beneficiaries may be subject to a deductible for each benefit period, which is based on the length of the hospital stay. The benefit period begins the day the patient is admitted to the hospital and ends when they have been out of the hospital or skilled nursing facility for 60 consecutive days. The billing cycle for the Part A hospital deductible resets with each new benefit period.

Similarly, for skilled nursing facility care, beneficiaries may be responsible for coinsurance costs after a certain number of days. The billing cycle for skilled nursing facility care under Medicare Part A involves potential out-of-pocket expenses once the initial coverage period is exhausted. Understanding these billing cycles is crucial for beneficiaries to anticipate and plan for their healthcare costs.

For hospice care and home health care services, Medicare Part A may cover a portion of the costs, with beneficiaries responsible for limited coinsurance for prescription drugs and respite care. The billing cycle for these services is determined by the frequency and duration of care received, with potential out-of-pocket costs for certain items and services.

Overall, understanding the billing cycle for Medicare Part A is essential for beneficiaries to navigate the cost-sharing requirements associated with inpatient hospital care, skilled nursing facility care, hospice care, and home health care services. By comprehending the timelines and processes involved in billing for Part A services, individuals can effectively manage their healthcare expenses and ensure timely payment for the care they receive.

Medicare Part B Billing Cycle

Medicare Part B, also known as medical insurance, covers medically necessary services such as doctor’s visits, outpatient care, preventive services, and durable medical equipment. Understanding the billing cycle for Medicare Part B is crucial for beneficiaries to comprehend their financial responsibilities and make informed decisions about their healthcare needs.

Beneficiaries enrolled in Medicare Part B are required to pay a monthly premium, along with an annual deductible and coinsurance for the services they receive. The billing cycle for Medicare Part B involves monthly premium payments and potential out-of-pocket costs for covered services.

The standard premium for Medicare Part B is set by the government and may be subject to income-related adjustments for higher-income beneficiaries. Premiums are typically deducted from Social Security, Railroad Retirement Board, or Civil Service Retirement payments. For individuals not receiving these benefits, alternative payment arrangements can be made.

In addition to the monthly premium, beneficiaries are responsible for an annual deductible, which is the amount they must pay for covered services before Medicare begins to pay its share. Once the deductible is met, beneficiaries typically pay 20% of the Medicare-approved amount for most doctor’s services, outpatient therapy, and durable medical equipment. The billing cycle for Medicare Part B coinsurance involves potential out-of-pocket costs for these services.

Understanding the billing cycle for Medicare Part B is essential for beneficiaries to anticipate and plan for their healthcare costs. By comprehending the timelines and processes involved in billing for Part B services, individuals can effectively manage their financial obligations and ensure timely payment for the medical services they receive.

Overall, Medicare Part B plays a critical role in providing essential medical coverage to beneficiaries, and understanding its billing cycle is key to navigating the cost-sharing requirements associated with doctor’s visits, outpatient care, preventive services, and durable medical equipment. By gaining insight into the billing cycle for Part B, beneficiaries can make informed decisions about their healthcare needs and ensure seamless access to vital medical services.

Medicare Part C Billing Cycle

Medicare Part C, also known as Medicare Advantage, is offered through private insurance companies approved by Medicare. These plans provide the same coverage as Part A and Part B, and often include additional benefits such as prescription drug coverage, dental care, and vision services. Understanding the billing cycle for Medicare Part C is crucial for beneficiaries to comprehend their financial responsibilities and make informed decisions about their healthcare needs.

The billing cycle for Medicare Part C involves premiums, deductibles, and cost-sharing arrangements determined by the specific Medicare Advantage plan selected by the beneficiary. Unlike traditional Medicare, where beneficiaries typically pay premiums for Part B coverage and may have supplemental coverage for out-of-pocket costs, Medicare Advantage plans often consolidate these expenses into a single premium.

Medicare Advantage plans may have different premium structures, including zero-premium plans that offer comprehensive coverage with no additional premium beyond the Part B premium. The billing cycle for Medicare Part C premiums varies based on the specific plan chosen by the beneficiary, with monthly payments required to maintain coverage.

In addition to premiums, Medicare Advantage plans may have annual deductibles and cost-sharing requirements for covered services. The billing cycle for Medicare Part C deductibles and cost-sharing involves potential out-of-pocket expenses for doctor’s visits, hospital stays, and other healthcare services, as determined by the plan’s benefits and network providers.

Understanding the billing cycle for Medicare Part C is essential for beneficiaries to navigate the cost-sharing requirements associated with Medicare Advantage plans and ensure timely payment for the healthcare services they receive. By comprehending the timelines and processes involved in billing for Part C services, individuals can effectively manage their financial obligations and make informed choices about their healthcare coverage.

Overall, Medicare Part C offers beneficiaries an alternative way to receive their Medicare benefits, and understanding its billing cycle is key to maximizing the advantages of Medicare Advantage plans. By gaining insight into the billing cycle for Part C, beneficiaries can make informed decisions about their healthcare needs and ensure seamless access to vital medical services and additional benefits offered through Medicare Advantage plans.

Medicare Part D Billing Cycle

Medicare Part D offers prescription drug coverage through private plans that are approved by Medicare. Beneficiaries enrolled in Part D plans pay a monthly premium and may be subject to annual deductibles, copayments, and coinsurance for their prescription medications. Understanding the billing cycle for Medicare Part D is crucial for beneficiaries to comprehend their financial responsibilities and make informed decisions about their prescription drug coverage.

The billing cycle for Medicare Part D involves monthly premium payments, annual deductibles, and cost-sharing arrangements for prescription medications. Part D plans are offered by private insurance companies and vary in terms of covered medications, formularies, and cost-sharing structures.

Beneficiaries have the option to choose from standalone Part D plans, which can be paired with Original Medicare, or Medicare Advantage plans that include prescription drug coverage. The billing cycle for Medicare Part D premiums varies based on the specific plan selected by the beneficiary, with monthly payments required to maintain prescription drug coverage.

In addition to premiums, Part D plans may have annual deductibles, which represent the initial out-of-pocket amount that beneficiaries must pay for their prescription drugs before the plan begins to provide coverage. The billing cycle for Medicare Part D deductibles involves potential out-of-pocket expenses for prescription medications, with the deductible amount varying among different Part D plans.

Once the deductible is met, beneficiaries typically pay a percentage of the cost of their medications in the form of copayments or coinsurance. The billing cycle for Medicare Part D copayments and coinsurance involves ongoing out-of-pocket costs for prescription drugs, with the specific amount determined by the plan’s formulary and the tier to which the medication belongs.

Understanding the billing cycle for Medicare Part D is essential for beneficiaries to effectively manage their prescription drug expenses and ensure timely payment for the medications they need. By comprehending the timelines and processes involved in billing for Part D services, individuals can make informed choices about their prescription drug coverage and navigate the cost-sharing requirements associated with Part D plans.

Overall, Medicare Part D plays a critical role in providing beneficiaries with access to affordable prescription medications, and understanding its billing cycle is key to maximizing the benefits of prescription drug coverage. By gaining insight into the billing cycle for Part D, beneficiaries can make informed decisions about their healthcare needs and ensure seamless access to vital prescription medications.

Conclusion

Understanding the billing cycles for Medicare Parts A, B, C, and D is essential for beneficiaries to navigate the complexities of the program and effectively manage their healthcare expenses. Each part of Medicare has its own unique billing cycle, cost-sharing requirements, and financial responsibilities, making it crucial for individuals to comprehend the timelines and processes involved in billing for the services they receive.

Medicare Part A, which primarily covers inpatient hospital care, skilled nursing facility care, hospice care, and some home health care services, involves specific billing cycles for deductibles and coinsurance associated with different types of care. Beneficiaries need to anticipate and plan for potential out-of-pocket expenses based on the billing cycle for Part A services.

Medicare Part B, which covers medically necessary services such as doctor’s visits, outpatient care, preventive services, and durable medical equipment, requires monthly premium payments and potential out-of-pocket costs for covered services. Understanding the billing cycle for Part B is crucial for beneficiaries to effectively manage their financial obligations and ensure timely payment for medical services.

Medicare Part C, also known as Medicare Advantage, offers beneficiaries an alternative way to receive their Medicare benefits, with billing cycles involving premiums, deductibles, and cost-sharing arrangements determined by the specific Medicare Advantage plan selected. Comprehending the billing cycle for Part C is essential for individuals to make informed choices about their healthcare coverage and additional benefits.

Medicare Part D, which provides prescription drug coverage through private plans, entails billing cycles for monthly premiums, annual deductibles, and ongoing cost-sharing for prescription medications. Beneficiaries need to understand the billing cycle for Part D to effectively manage their prescription drug expenses and ensure timely payment for their medications.

In conclusion, gaining insight into the billing cycles for Medicare Parts A, B, C, and D empowers beneficiaries to make informed decisions about their healthcare needs, anticipate and plan for out-of-pocket expenses, and ensure seamless access to vital medical services and prescription medications. By comprehending the nuances of Medicare billing, individuals can navigate the program with confidence and maximize the benefits available to them.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance