Home>Finance>Cash Flow From Operating Activities (CFO) Defined, With Formulas

Finance

Cash Flow From Operating Activities (CFO) Defined, With Formulas

Published: October 24, 2023

Learn about cash flow from operating activities (CFO) in finance and how to calculate it with formulas. Enhance your understanding of financial management.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Cash Flow From Operating Activities (CFO) Defined, With Formulas

When it comes to managing your personal or business finances, understanding cash flow is crucial. Cash flow represents the movement of money in and out of your accounts over a specific period. One key aspect of cash flow is Cash Flow From Operating Activities (CFO). In this blog post, we will define CFO and provide you with the essential formulas to calculate it.

Key Takeaways:

- Cash Flow From Operating Activities (CFO) measures the cash generated or used by a company’s core business operations.

- CFO reflects the ability of a company to generate cash flow from its day-to-day activities.

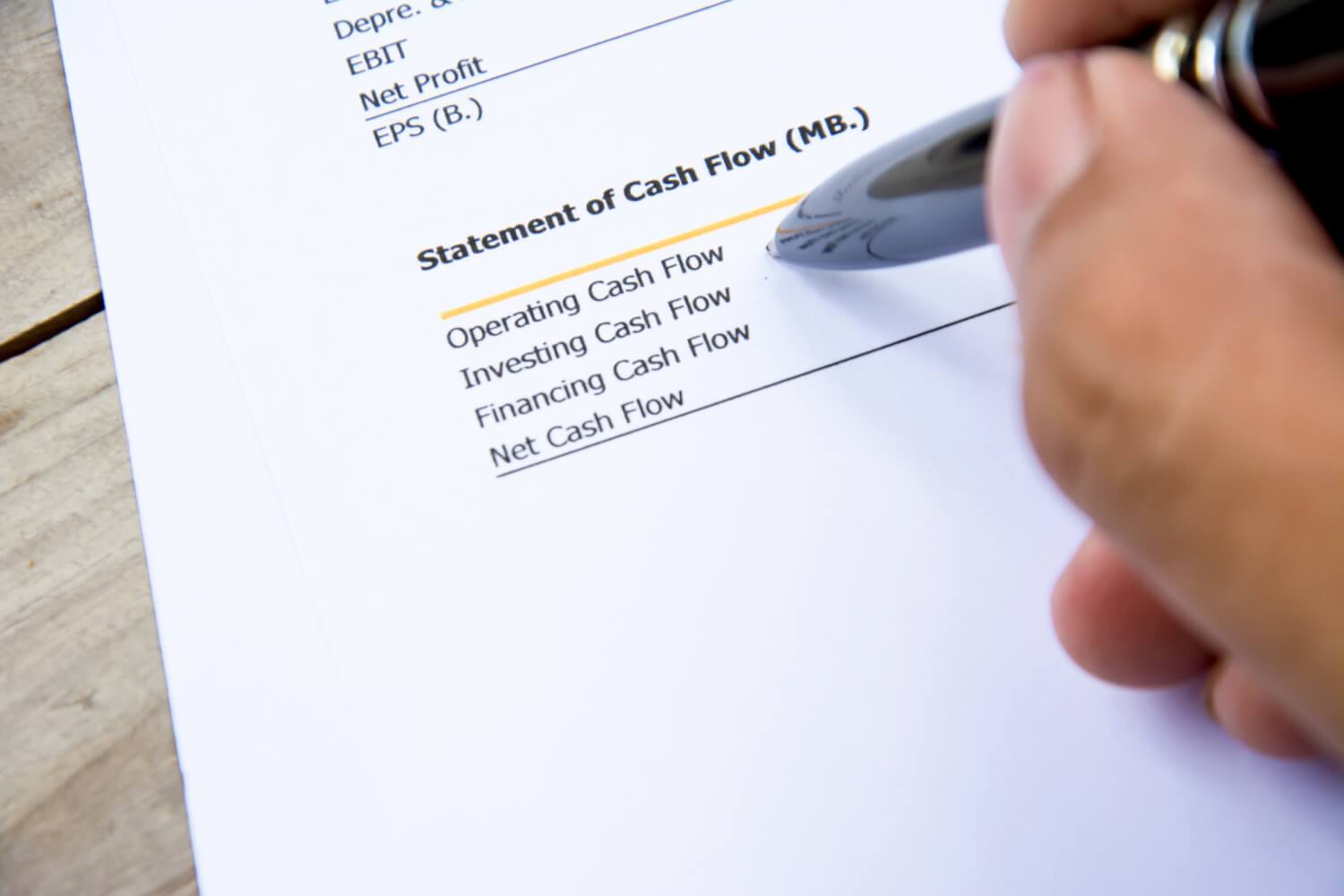

So, what exactly is Cash Flow From Operating Activities (CFO)? CFO is a vital metric that shows the amount of cash generated or used by a company’s core business operations, such as sales, production, and delivery of goods or services. It provides insights into the company’s ability to generate cash from its day-to-day activities, excluding other sources like financing or investing activities.

Calculating CFO involves evaluating different components of a company’s financial statements, such as the income statement and balance sheet. Here are two common formulas to determine CFO:

- Indirect Method: This method starts with net income and adjusts for non-cash expenses like depreciation and changes in working capital. The formula looks like this:

- Direct Method: The direct method focuses on individual cash inflows and outflows from operating activities. It analyzes line items in the income statement and changes in assets and liabilities. The formula is:

CFO = Net Income + Depreciation and Amortization + Changes in Working Capital

CFO = Cash Inflows – Cash Outflows

Understanding CFO is essential for evaluating a company’s financial health and making informed decisions. A positive CFO indicates that a company is generating enough cash from its core operations to cover expenses, invest in growth, pay dividends, and reduce debt. Conversely, a negative CFO may signify difficulties in generating sufficient cash flow, potentially leading to financial challenges.

In summary, Cash Flow From Operating Activities (CFO) provides insights into a company’s ability to generate cash internally from its core operations. Calculating CFO involves utilizing formulas like the indirect or direct method. By understanding CFO, you can better assess a company’s financial stability and make informed decisions about investments or managing personal finances.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance