Finance

How Does Self Credit Work

Published: January 8, 2024

Learn how self credit works and obtain financial freedom. Understand the ins and outs of managing your finances and securing a stable future with self credit.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- What is Self Credit?

- Understanding the Concept of Self Credit

- How Self Credit Differs from Traditional Credit

- The Process of Building Self Credit

- Factors that Influence Self Credit Scores

- Benefits of Self Credit for Individuals

- Potential Challenges of Self Credit

- Tips for Effectively Managing Self Credit

- Frequently Asked Questions about Self Credit

- Conclusion

What is Self Credit?

Self credit, also known as self-lending or self-financing, is a unique approach to credit-building that empowers individuals to establish and improve their credit scores without relying on traditional financial institutions. It offers an alternative solution for those who may have limited or no credit history, enabling them to build their creditworthiness and gain access to better financial opportunities.

In traditional credit systems, individuals typically need to apply for credit cards, loans, or other types of credit products from banks or lenders in order to establish credit history. However, this can be challenging for individuals who have little to no credit history, as they are often deemed as high-risk borrowers and face difficulty in obtaining credit.

Self credit works by utilizing a process commonly known as credit builder loans. Instead of relying on credit cards or loans from traditional lenders, individuals make monthly payments into a savings account or a certificate of deposit (CD). These payments are reported to the credit bureaus, and over time, they help establish a positive credit history.

The funds deposited into the savings account or CD act as collateral for the credit builder loan. After a predetermined period (usually six to twelve months), the individual receives the funds they deposited, along with any accumulated interest. This process not only helps to establish credit but also enables individuals to save money for future financial needs.

It is important to note that self credit is not the same as secured credit cards or secured loans, where individuals are required to put down a deposit in order to access credit. Self credit allows individuals to build their credit without the risk of overspending or incurring unnecessary debt.

Overall, self credit offers a unique and innovative approach to building credit. It provides individuals with an opportunity to establish a positive credit history, which can open doors to better interest rates, lower insurance premiums, and increased financial security.

Understanding the Concept of Self Credit

Self credit is a concept that empowers individuals to take control of their creditworthiness and financial future. It allows individuals to build credit without relying on traditional financial institutions or credit products. By understanding the concept of self credit, individuals can make informed decisions about their financial well-being and take proactive steps toward a stronger credit profile.

At its core, self credit is based on the principle of responsible financial behavior. It encourages individuals to save money while simultaneously building credit. Unlike traditional credit-building methods, self credit focuses on a savings-centric approach where individuals make regular payments into a dedicated account. These payments are reported to credit bureaus, gradually building a positive credit history.

The concept of self credit is rooted in the belief that financial responsibility should be accessible to everyone, regardless of their credit history or financial standing. It aims to break down barriers and provide individuals with a pathway to establish credit on their own terms.

One key aspect of self credit is the credit builder loan. This loan operates differently from other loans as the borrower does not receive the loan proceeds upfront. Instead, the borrower makes regular payments into a savings account or CD, which serves as collateral. As the borrower consistently makes payments, the credit builder loan reports positive payment history to the credit bureaus, strengthening their credit profile over time.

In addition to building credit, self credit also encourages individuals to develop healthy savings habits. By making regular payments into a designated account, individuals are simultaneously saving money while working towards a stronger credit score. This savings-centric approach not only helps individuals build credit, but it also sets them up for future financial success.

Furthermore, self credit allows individuals to have more control over their credit journey. Instead of relying on traditional credit products or lenders, individuals have the power to dictate their credit-building progress. This sense of ownership and empowerment can lead to greater financial confidence and long-term financial stability.

Overall, understanding the concept of self credit is essential for individuals looking to establish or improve their credit. By recognizing the opportunities and benefits it provides, individuals can make informed decisions about their financial future and take proactive steps towards achieving a healthier credit profile.

How Self Credit Differs from Traditional Credit

Self credit differs from traditional credit in several key ways, offering individuals a unique and alternative approach to building their creditworthiness. By understanding the differences between self credit and traditional credit, individuals can choose the method that best suits their financial goals and needs.

1. Access to credit: Traditional credit typically requires individuals to have an established credit history or meet certain criteria to qualify for credit products such as credit cards or loans. Self credit, on the other hand, allows individuals with limited or no credit history to build credit by making regular payments into a savings account or CD.

2. Collateral and risk: Traditional credit products often require collateral, such as a car or property, to secure the loan. This means that failure to repay the loan can result in the loss of the collateral. In self credit, individuals use their own savings as collateral for the credit builder loan, reducing the risk associated with traditional credit.

3. Building credit history: Traditional credit relies on borrowing and repaying debts, such as credit card balances or loan installments, to build credit history. Self credit, on the other hand, focuses on establishing a positive credit history through regular payments into a savings account. These payments are reported to credit bureaus, helping individuals build credit over time.

4. Control and flexibility: Traditional credit products are often offered by banks and lenders, giving them control over the terms and conditions of the credit. With self credit, individuals have more control over their credit-building journey. They can choose the amount of their regular payments and have a say in how their credit builder loan is structured.

5. Credit utilization: Traditional credit revolves around credit utilization, which refers to the amount of available credit a person uses. In self credit, there is no credit utilization factor since individuals are not using borrowed funds. Instead, the focus is on responsible savings and building a positive payment history.

6. Financial education: Self credit often provides individuals with access to financial education resources to help them understand credit management, budgeting, and saving. Traditional credit products may or may not include such educational components, leaving individuals to seek out financial knowledge on their own.

It’s important to note that while self credit offers individuals an alternative approach to building credit, it may not suit everyone’s financial needs and goals. It’s essential for individuals to research and evaluate both self credit and traditional credit options to determine the best path for their unique circumstances.

The Process of Building Self Credit

Building self credit involves a systematic process that individuals can follow to establish and improve their creditworthiness. By understanding the steps involved, individuals can effectively navigate the process and achieve their credit-building goals.

1. Research and Choose a Self-Credit Provider: Start by researching different self-credit providers and credit unions that offer credit builder loans. Compare their offerings, fees, and terms to find the one that aligns with your needs and financial goals.

2. Apply for a Credit Builder Loan: Once you have selected a self-credit provider, submit an application for a credit builder loan. The application process is usually straightforward and requires basic personal information.

3. Deposit Funds into a Savings Account or CD: Upon approval, you will be required to deposit funds into a savings account or CD as collateral for the credit builder loan. The amount you deposit will determine the limit of your credit builder loan.

4. Make Regular and On-Time Payments: The next step is to make regular monthly payments toward the credit builder loan. These payments should be made on time and in the agreed-upon amount.

5. Credit Reporting: The self-credit provider will report your payment history to the major credit bureaus—Equifax, Experian, and TransUnion. This helps to establish a positive credit history and improve your credit score over time.

6. Monitor Your Progress: Regularly monitor your credit reports and scores to keep track of your credit-building progress. This will also help you identify any errors or discrepancies that need to be addressed.

7. Complete the Loan Term: After successfully making all the monthly payments, you will complete the loan term. At this point, you will receive the funds you deposited, along with any interest earned during the process.

8. Continue Building Credit: Building self-credit is an ongoing process. Even after completing a credit builder loan, it’s important to continue practicing good credit habits, such as making payments on time and keeping your credit utilization low.

By following these steps and maintaining responsible credit behavior, individuals can build a positive credit history and improve their credit scores over time. It’s important to be patient and consistent throughout the process, as credit-building is a gradual journey that requires dedication and financial discipline.

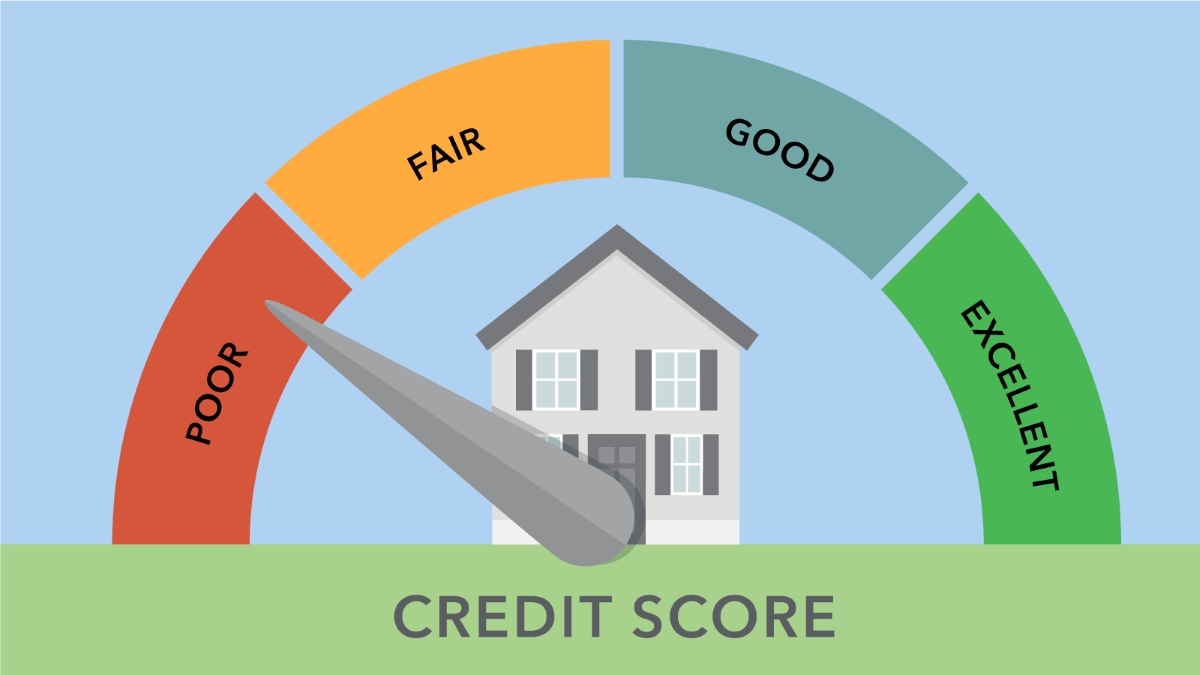

Factors that Influence Self Credit Scores

Similar to traditional credit scores, self credit scores are influenced by various factors that reflect an individual’s creditworthiness. These factors play a key role in determining a person’s self credit score and can impact their ability to access favorable financial opportunities. By understanding these factors, individuals can make informed decisions to improve their self credit scores.

1. Payment History: One of the most significant factors in calculating self credit scores is an individual’s payment history. Consistently making on-time payments toward the credit builder loan is crucial in establishing a positive credit history and improving the self credit score. Late payments or defaulting on payments can have a detrimental effect on the self credit score.

2. Credit Utilization: While self credit does not involve traditional credit products, credit utilization still plays a role in credit scoring. Credit utilization refers to the percentage of available credit being used. Even though individuals are using their own funds in a credit builder loan, maintaining a low utilization rate shows responsible financial management and can positively impact the self credit score.

3. Length of Credit History: The length of credit history is another important factor in determining self credit scores. The longer an individual maintains a positive credit history, the better their self credit score will be. This factor highlights the importance of building credit early and maintaining good credit habits over time.

4. Credit Mix: Having a diverse range of credit types can positively impact self credit scores. While self credit primarily focuses on credit builder loans, having a mix of other credit accounts, such as credit cards or installment loans, can demonstrate responsible credit management and improve the overall self credit score.

5. Financial Stability: Self credit scoring also takes into account an individual’s overall financial stability. Factors such as income, employment history, and debt-to-income ratio can influence the self credit score. Demonstrating a stable financial situation can contribute to a higher self credit score.

6. Credit Inquiries: The number of credit inquiries made by an individual can impact their self credit score. While self credit does not require credit checks or inquiries like traditional credit applications, it’s still important to be mindful of other credit inquiries that could affect the score.

7. Credit Education and Financial Literacy: Some self-credit providers may consider an individual’s credit education and financial literacy when assessing their creditworthiness. Participating in financial education programs, attending credit counseling, or demonstrating knowledge of credit management may positively impact the self credit score.

It’s important to note that the weight and importance of each factor may vary depending on the self-credit provider and their specific scoring model. However, by focusing on maintaining a positive payment history, keeping credit utilization low, and practicing responsible financial habits, individuals can increase their self credit scores and improve their overall creditworthiness.

Benefits of Self Credit for Individuals

Self credit offers numerous benefits for individuals who are looking to establish or improve their creditworthiness. By taking advantage of this alternative credit-building method, individuals can unlock a range of advantages that can positively impact their financial lives. Here are some key benefits of self credit:

1. Access to Credit: Self credit provides individuals with an opportunity to access credit even if they have limited or no credit history. By building a positive credit history through regular payments into a credit builder loan, individuals can demonstrate their creditworthiness and increase their chances of obtaining credit in the future.

2. Improved Credit Scores: Self credit can help individuals improve their credit scores over time. By responsibly managing a credit builder loan and making on-time payments, individuals can establish a positive payment history, lower their credit utilization ratio, and demonstrate financial responsibility—factors that can boost their credit scores.

3. Financial Stability: Building self credit goes hand in hand with developing financial stability. By making regular payments into a credit builder loan, individuals develop a habit of setting aside funds each month. This can lead to enhanced financial discipline, budgeting skills, and an increased sense of control over personal finances.

4. Lower Interest Rates: Having a good credit score can result in lower interest rates on future loans or credit products. By building self credit, individuals can increase their chances of qualifying for loans with favorable terms and conditions, saving them money in interest payments over time.

5. Expanded Financial Opportunities: Self credit opens up a range of financial opportunities that may otherwise be limited for individuals with poor or no credit history. With an established credit profile, individuals can access a variety of financial products, such as credit cards, personal loans, or even mortgages, providing them with more options to meet their financial needs.

6. Enhanced Renting Capabilities: Many landlords and property management companies perform credit checks on potential tenants. By building self credit, individuals can increase their chances of passing these checks and securing desirable rental properties.

7. Financial Confidence: Building self credit can instill a sense of financial confidence. By taking charge of their credit journey, individuals gain a deeper understanding of credit management, saving strategies, and responsible financial behavior. This increased knowledge and confidence can have a positive impact on other areas of their financial lives.

8. Future Investment Opportunities: As individuals continue to build their self credit and improve their credit scores, they may gain access to investment opportunities that require a strong credit profile. This can include real estate investments, business loans, or other ventures that can help individuals grow their wealth over time.

In summary, self credit offers individuals a path towards building credit, improving credit scores, and unlocking a range of financial benefits. By taking advantage of this alternative credit-building method, individuals can lay the foundation for a stronger financial future and seize opportunities that may have otherwise been out of reach.

Potential Challenges of Self Credit

While self credit can be a beneficial way to build credit, it is important to be aware of some potential challenges that individuals may face during the process. By understanding these challenges, individuals can be better prepared and develop strategies to overcome them. Here are some common challenges of self credit:

1. Limited Credit Building Opportunities: Unlike traditional credit, which offers a wide range of credit products and opportunities to build credit, self credit primarily revolves around credit builder loans. This limited option for credit building may require individuals to explore additional avenues to diversify their credit profile.

2. Long-Term Commitment: Building credit takes time and patience. The process of self credit typically involves committing to a credit builder loan for several months or years. It’s essential to be prepared for the long-term commitment required to see improvements in credit scores and establish a positive credit history.

3. Financial Discipline: Self credit requires individuals to consistently make payments toward the credit builder loan. This calls for financial discipline and budgeting skills to ensure timely payments each month. Without strong financial discipline, individuals may struggle to maintain regular payments, which can hinder their progress in building self credit.

4. Limited Credit Impact: While self credit can help establish a positive credit history, its impact on credit scores may be more limited compared to traditional credit products. Credit scores take into account various factors, and solely relying on self credit may not have as significant an impact as a diverse credit mix.

5. Limited Credit Limit: With self credit, the credit limit is usually determined by the amount individuals deposit as collateral. This limitation may result in a lower credit limit compared to what could be obtained with traditional credit products. This can present a challenge when individuals need access to a higher credit limit for certain financial needs.

6. Lack of Credit Rewards and Benefits: Unlike certain credit cards or loan products, self credit may not offer the same rewards, cashback, or benefits as traditional credit options. Individuals may miss out on the perks and incentives that come with certain credit products.

7. Potential Cost: Some self-credit providers may charge fees or interest on credit builder loans. It’s important to carefully review the terms and costs associated with the self-credit program to ensure it aligns with your financial goals and is cost-effective in the long run.

8. Limited Recognition: While self credit can help establish a positive credit history, not all lenders or creditors may recognize self credit scores or give them the same weight as traditional credit scores. This can present challenges when individuals need to demonstrate their creditworthiness to certain institutions or lenders.

Despite these challenges, self credit remains a viable option for individuals looking to build or improve their credit. By being aware of these potential obstacles and taking proactive steps to address them, individuals can effectively navigate the self credit journey and achieve their credit-building goals.

Tips for Effectively Managing Self Credit

Managing self credit requires discipline and a strategic approach to ensure individuals can maximize the benefits and achieve their credit-building goals. By following these tips, individuals can effectively manage their self credit and improve their creditworthiness:

1. Make Payments on Time: Consistently make your monthly payments on time. Late payments can have a negative impact on your credit score, so it’s crucial to prioritize timely payment of your credit builder loan.

2. Budget and Plan: Create a budget that includes your credit builder loan payments. This will help you allocate funds appropriately, ensuring that you have enough money set aside each month to make your payments on time.

3. Avoid Overcommitting: Be realistic about the amount you can comfortably afford as monthly payments. Avoid overcommitting yourself and jeopardizing your ability to make consistent payments.

4. Monitor Your Credit: Regularly check your credit reports to ensure that your credit builder loan payments are being reported accurately. This will also help you identify any errors or discrepancies that need to be addressed.

5. Consider Credit Mix: While self credit primarily focuses on credit builder loans, it’s beneficial to have a mix of credit types. Consider opening a secured credit card or taking out small installment loans to diversify your credit profile, if you can manage them responsibly.

6. Monitor Your Credit Utilization: Although self credit does not involve traditional credit cards, it’s still important to keep an eye on your credit utilization. Aim to keep your utilization low to demonstrate responsible credit management.

7. Build Emergency Savings: In addition to making payments toward your credit builder loan, strive to build an emergency savings fund. This will give you a financial safety net and help you avoid relying on credit in case of unexpected expenses.

8. Stay Informed: Educate yourself on credit management and financial literacy. Be proactive in expanding your knowledge and understanding of credit, saving strategies, and responsible financial practices.

9. Patience and Persistence: Building self credit takes time, so remain patient and persistent. Continue making payments and practicing responsible financial habits. Over time, you will see the positive impact on your credit profile.

10. Seek Professional Advice: If you have questions or need guidance, consider consulting with a credit counselor or financial advisor. They can provide personalized advice to help you effectively manage your self credit and achieve your financial goals.

By following these tips, individuals can effectively manage their self credit and build a strong credit history. It’s important to remember that responsible financial behavior and consistency are key in maximizing the benefits of self credit and improving overall creditworthiness.

Frequently Asked Questions about Self Credit

Here are some commonly asked questions about self credit, along with their answers to help individuals gain a deeper understanding of this credit-building method:

1. What is self credit?

Self credit, also known as self-lending or self-financing, is a credit-building technique that allows individuals to build credit without relying on traditional financial institutions. It involves making regular payments into a credit builder loan, which helps establish a positive credit history and improve credit scores over time.

2. How does self credit work?

With self credit, individuals deposit funds into a savings account or certificate of deposit (CD) as collateral for a credit builder loan. They make monthly payments toward the loan, and these payments are reported to credit bureaus. Over time, as individuals demonstrate responsible payment behavior, their credit scores improve.

3. Can self credit help establish credit if I have no credit history?

Yes, self credit can be an effective way to establish credit, especially for individuals with limited or no credit history. By making regular payments into a credit builder loan, individuals can establish a positive credit history and demonstrate their creditworthiness to lenders.

4. How long does it take to build credit with self credit?

Building credit with self credit is a gradual process and can take several months or even years to see significant improvements in credit scores. Consistency in making on-time payments and practicing responsible financial habits will contribute to a faster credit-building journey.

5. Does self credit require a credit check?

No, self credit does not typically involve a credit check. It focuses on an individual’s ability to make regular payments into a credit builder loan, rather than relying on a traditional credit check to determine creditworthiness.

6. Can self credit help improve my credit score?

Yes, self credit can help improve credit scores over time. By establishing a positive payment history and demonstrating responsible financial behavior, individuals can see their credit scores increase, opening up access to more favorable financial opportunities.

7. Are there any fees involved in self credit?

Some self-credit providers may charge fees for the credit builder loan. It’s important to review the terms and conditions of the self-credit program to understand any associated fees or costs.

8. Can I use self credit to qualify for other types of credit?

Yes, building self credit can enhance your creditworthiness and increase your chances of qualifying for other types of credit, such as credit cards, personal loans, or mortgages. Lenders may view a positive credit history established through self credit as a positive factor when assessing creditworthiness.

9. Can I use self credit to repair my credit?

Yes, self credit can be a useful tool in credit repair. By making consistent payments and practicing responsible financial behavior, individuals can improve their credit scores and repair past credit issues over time.

10. Can I monitor my self credit score?

While there may not be a specific self credit score, individuals can monitor their overall credit score using free credit monitoring services or by accessing their credit reports regularly. This will help individuals track their credit-building progress and identify any areas that need improvement.

These frequently asked questions provide a basic understanding of self credit and its benefits. However, it’s important to research and consult with self-credit providers or financial advisors for specific details relating to individual circumstances.

Conclusion

Self credit offers individuals a unique and empowering path to establish and improve their creditworthiness. By utilizing credit builder loans and making regular payments into savings accounts or CDs, individuals can build a positive credit history and improve their credit scores over time.

While self credit differs from traditional credit in several ways, it presents numerous benefits for individuals looking to gain access to credit, improve their financial stability, and unlock financial opportunities. Self credit provides an alternative for those with limited or no credit history, offering a pathway to establish credit on their own terms.

Effective management of self credit requires discipline, financial literacy, and responsible financial behavior. By making payments on time, diversifying credit types, monitoring credit utilization, and practicing budgeting and saving strategies, individuals can maximize the benefits of self credit and strengthen their financial well-being.

It is important to note that self credit is not a quick fix and building credit takes time and patience. Consistency in making payments and practicing responsible financial habits is key to achieving long-term credit-building goals.

While self credit presents great opportunities, it does come with potential challenges. Limited credit-building options, long-term commitment, and the need for financial discipline can pose obstacles along the way. However, by being aware of these challenges and following effective strategies, individuals can overcome them and achieve their goals.

In conclusion, self credit is a viable option for individuals seeking to establish or improve their credit. By taking control of their credit journey and utilizing the tools and techniques of self credit, individuals can pave the way for a stronger financial future, increased creditworthiness, and enhanced financial opportunities.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance