Finance

How Much Is Gap Insurance Per Month?

Published: November 17, 2023

Discover how much gap insurance costs per month and get the financial coverage you need to protect you from potential car depreciation and loan/lease payoff.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to our guide on Gap Insurance!

When it comes to protecting your investment in a car, it’s essential to consider all the potential risks and liabilities. While standard auto insurance covers damages caused by accidents, theft, and natural disasters, it may not provide adequate coverage in certain situations. This is where Gap Insurance comes in.

Gap Insurance, also known as Guaranteed Asset Protection Insurance, is a type of auto insurance that covers the “gap” between the amount you owe on your car loan or lease and the actual cash value of the vehicle. In simple terms, it bridges the difference between what you owe and what your car is worth if it is declared a total loss.

Imagine this scenario: You buy a brand-new car for $30,000 and finance it with a loan. A few months later, unfortunately, you get into a severe accident, and your vehicle is deemed a total loss. While your traditional auto insurance may only reimburse you for the car’s current market value, Gap Insurance will cover the outstanding loan balance, ensuring you aren’t left with a financial burden.

Now that you understand the importance of Gap Insurance, let’s dive into the factors that affect the cost of this insurance coverage.

What is Gap Insurance?

Gap Insurance is a type of insurance coverage specifically designed to protect you from financial loss in the event that your car is deemed a total loss and the amount you owe on your loan or lease is higher than the actual cash value of the vehicle.

When you purchase a new car, its value starts to depreciate as soon as you drive it off the lot. In the event of an accident or theft, your standard auto insurance policy typically only covers the actual cash value of the car at the time of the incident. However, this amount may be significantly lower than what you owe on your loan or lease.

This is where Gap Insurance steps in. It covers the “gap” between what your car is worth and what you still owe, ensuring that you do not have to bear the financial burden of paying off a loan or lease for a vehicle you no longer have.

Gap Insurance typically covers the following scenarios:

- Accidents

- Theft

- Natural disasters

- Vandalism

- Fire

It’s important to note that Gap Insurance is not mandatory, and its necessity depends on your specific circumstances. If you purchased a new car with a small down payment or financed a significant portion of the vehicle’s value, Gap Insurance can provide you with peace of mind by protecting your financial investment.

In the next section, we will explore the factors that can affect the cost of Gap Insurance.

Factors Affecting Gap Insurance Cost

The cost of Gap Insurance can vary depending on several factors. Understanding these factors will help you determine how much you can expect to pay for this coverage. Here are some key factors that can affect the cost of Gap Insurance:

- Vehicle Type: The type of vehicle you own can impact the cost of Gap Insurance. Generally, more expensive vehicles will have higher Gap Insurance rates since the financial gap between the loan amount and the vehicle’s value is larger.

- Loan or Lease Terms: The terms of your loan or lease agreement can influence the cost of Gap Insurance. Longer loan terms and higher interest rates can increase the overall cost of the Gap Insurance coverage.

- Loan Amount: The total amount you financed or the remaining balance on your loan affects the Gap Insurance cost. The larger the loan amount, the higher the premium will be.

- Down Payment: The size of your down payment can also impact the cost of Gap Insurance. A larger down payment reduces the loan amount, decreasing the potential gap between the car’s value and the loan balance.

- Insurance Provider: Different insurance providers may offer Gap Insurance at varying rates. It’s always a good idea to compare quotes from multiple insurers to find the best rate for the coverage you need.

It’s important to keep in mind that the cost of Gap Insurance is typically a one-time payment or added as a percentage to your monthly auto insurance premium. However, it’s worth considering the overall cost of Gap Insurance over the term of your loan or lease. Some insurance providers may offer discounts or bundle Gap Insurance with other coverage options, potentially reducing the overall cost.

Now that we understand the factors that influence Gap Insurance cost, let’s explore the average cost of Gap Insurance per month.

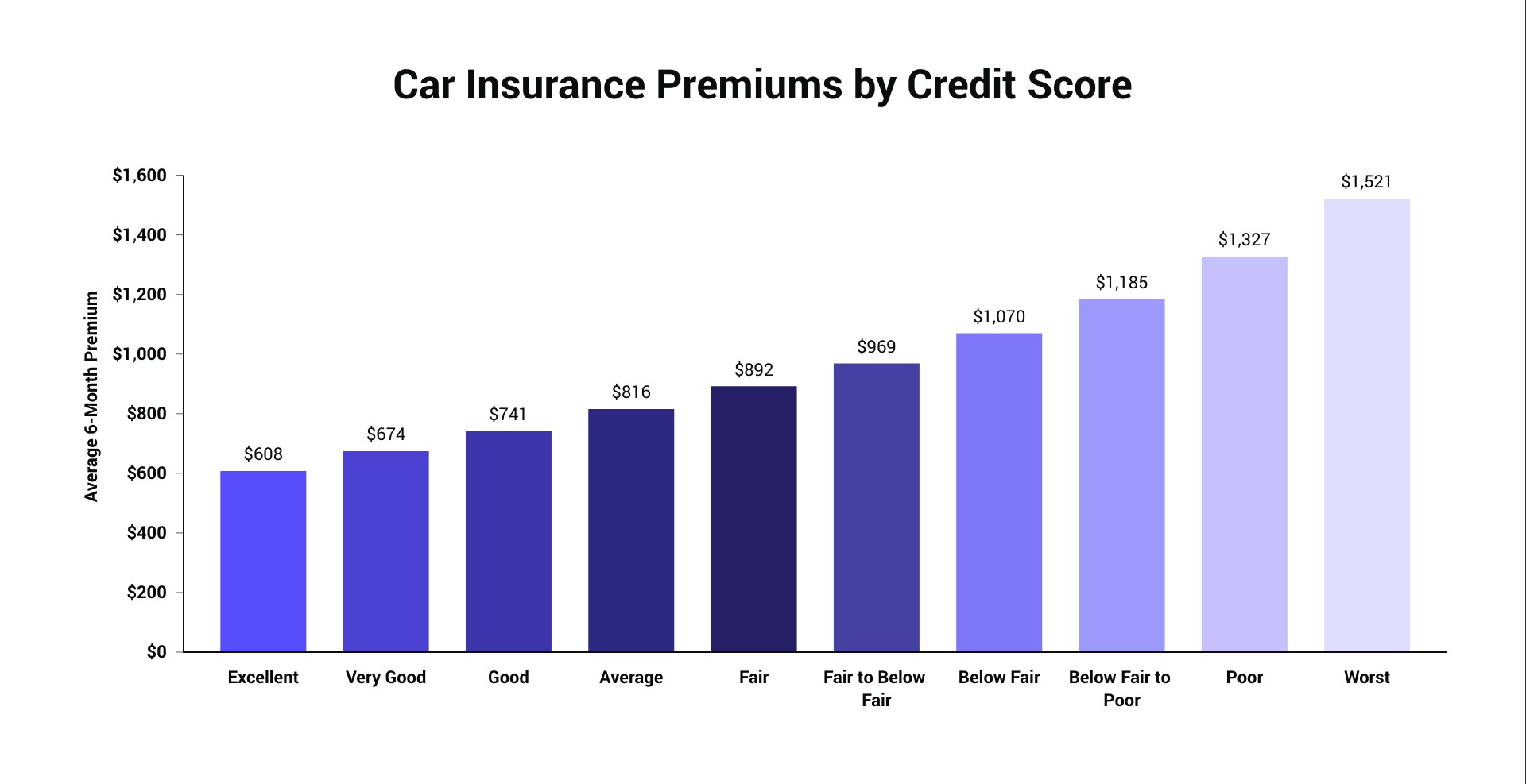

Average Cost of Gap Insurance Per Month

The cost of Gap Insurance can vary depending on factors such as the type of vehicle, loan or lease terms, and the insurance provider you choose. On average, Gap Insurance typically ranges from $20 to $40 per month. However, it’s important to note that these figures are estimates and can vary.

Several factors can influence the cost of Gap Insurance, including the value of your vehicle and the length and interest rate of your loan or lease. More expensive vehicles or vehicles with higher loan amounts will generally have higher Gap Insurance premiums. Additionally, longer loan terms and higher interest rates can also impact the cost of Gap Insurance.

Keep in mind that the cost of Gap Insurance may be paid as a one-time premium or added to your monthly auto insurance payments. Some insurance providers may even offer discounts or promotional offers, so it’s important to shop around and compare quotes to find the best rate for the coverage you need.

It’s essential to carefully consider your individual situation and finances when deciding whether to purchase Gap Insurance, as well as how much coverage you require. If you have a smaller down payment, a loan with a longer term, or a vehicle with a higher depreciation rate, Gap Insurance can provide valuable financial protection in the event of a total loss.

Now that we have explored the average cost of Gap Insurance per month, let’s discuss how to find the best Gap Insurance rates.

How to Find the Best Gap Insurance Rates

When seeking Gap Insurance, it’s essential to find the best rates available. Here are some steps you can take to find the most competitive Gap Insurance rates:

- Research and compare insurance providers: Start by researching reputable insurance providers that offer Gap Insurance. Look for companies that have good customer reviews, strong financial stability, and a reputation for providing reliable coverage. Take the time to compare quotes from multiple providers to ensure you’re getting the best rate.

- Consider bundling with your auto insurance: Check with your current auto insurance provider to see if they offer Gap Insurance as an add-on to your existing policy. Many insurers offer discounted rates for bundling different types of coverage, so it’s worth exploring this option to potentially save on premiums.

- Review policy terms and conditions: Carefully read and understand the terms and conditions of any Gap Insurance policy you are considering. Look for any restrictions, deductibles, or limitations that may affect your coverage or claims process.

- Explore dealership offerings: Some car dealerships offer Gap Insurance as part of their financing packages. While dealership Gap Insurance may be convenient, it’s important to compare their rates with other providers to ensure you’re getting the best deal.

- Ask about discounts: Inquire about any available discounts that could potentially lower your Gap Insurance premium. Insurance providers may offer discounts based on factors such as good credit history, multiple policies, or safe driving records.

By following these steps and conducting thorough research, you can increase your chances of finding the best Gap Insurance rates that suit your needs and budget.

Lastly, it’s important to note that Gap Insurance is not the only option available to protect yourself financially in the event of a total loss. Let’s explore some alternatives to Gap Insurance in the next section.

Alternatives to Gap Insurance

While Gap Insurance is a popular and effective option for protecting yourself from financial loss in the event of a total loss, there are alternatives worth considering. Here are a few alternatives to Gap Insurance:

- Loan/Lease Payoff Coverage: Some auto insurance providers offer loan/lease payoff coverage as part of their comprehensive or collision insurance. This coverage helps bridge the gap between the insurance payout and the remaining balance on your loan or lease if your car is totaled. It’s important to review your policy and determine if this coverage is included or can be added as an endorsement.

- New Car Replacement Insurance: This type of coverage ensures that if your recently purchased car is totaled, you receive enough money for a brand-new replacement rather than just the actual cash value. This can be particularly helpful for those who have a new vehicle with a higher loan balance and want to avoid the financial gap between the loan and the market value.

- Savings and Emergency Funds: Building an emergency fund or savings specifically for unexpected car-related expenses can help mitigate the financial impact of a total loss. By saving money over time, you can have a backup fund to cover the gap between the insurance payout and your loan or lease balance.

- Loan or Lease Gap Coverage: Some lenders or leasing companies offer their own Gap Insurance coverage. Before purchasing external Gap Insurance, check with your lender or leasing company to see if they provide this coverage. It may be offered at a lower cost or even included in your loan or lease agreement.

- Depreciation Shield: Some insurers offer Depreciation Shield coverage, which pays the difference between the market value of your car and the outstanding loan amount. This can be an alternative to Gap Insurance, particularly for those who have a lower loan balance and want coverage specifically for depreciation-related gaps.

It’s important to carefully evaluate these alternatives and compare them to Gap Insurance to determine which option suits your specific needs and financial situation. Consider factors such as the cost of the coverage, the remaining balance on your loan or lease, and the potential risks you want to protect against.

Ultimately, the goal is to protect yourself from the financial burden of a total loss, so choose the option that provides you with the most comprehensive coverage and peace of mind.

Now, let’s conclude our discussion on Gap Insurance.

Conclusion

Gap Insurance is an essential coverage option to consider when purchasing a new car or leasing a vehicle. It protects you from the potential financial loss of owing more on your loan or lease than the actual cash value of your vehicle in the event of a total loss. By bridging this gap, Gap Insurance provides peace of mind and helps to ensure you are not left with a hefty financial burden.

When determining the cost of Gap Insurance, factors such as the type of vehicle, loan or lease terms, and insurance provider all play a role. By understanding these factors, you can better estimate the monthly cost of Gap Insurance and find the most competitive rates available.

To find the best Gap Insurance rates, it’s important to research and compare insurance providers, consider bundling options with your existing auto insurance, and review all policy terms and conditions. By taking the time to explore your options and ask about potential discounts, you can secure the most affordable and comprehensive Gap Insurance coverage.

While Gap Insurance is a popular choice, it’s important to consider alternatives such as loan/lease payoff coverage, new car replacement insurance, savings and emergency funds, lender or leasing company Gap Insurance, or depreciation shield coverage. Each alternative provides its own unique benefits, so be sure to evaluate which option suits your situation best.

When it comes to protecting your investment in a car, Gap Insurance is a valuable tool for ensuring that you are financially protected in the event of a total loss. By considering the factors that affect the cost of Gap Insurance and exploring all available options, you can make an informed decision that provides you with the coverage you need at a price that fits your budget.

Remember, the key is to choose a coverage option that aligns with your specific needs and offers you the most comprehensive protection. Whether you opt for Gap Insurance or an alternative, taking the necessary steps to safeguard your financial well-being is always a smart choice.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance