Finance

How To Create A Blockchain Smart Contract

Published: October 23, 2023

Learn how to create a finance-focused blockchain smart contract and streamline your financial transactions with our step-by-step guide.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Overview of Blockchain Technology

- Understanding Smart Contracts

- Benefits of Implementing Smart Contracts on the Blockchain

- Key Components of a Blockchain Smart Contract

- Step-by-step Guide to Creating a Blockchain Smart Contract

- Testing and Deploying a Blockchain Smart Contract

- Best Practices for Developing Blockchain Smart Contracts

- Common Challenges and Solutions in Blockchain Smart Contract Development

- Conclusion

Introduction

Welcome to the world of blockchain smart contracts! Blockchain technology has revolutionized various industries, offering transparency, security, and efficiency like never before. Among the many benefits that blockchain brings, the ability to execute smart contracts stands out as a game-changer.

In this article, we will delve into the fascinating realm of blockchain smart contracts, exploring their functionality, advantages, and the process of creating them. Whether you are a developer in the financial sector or simply an enthusiast looking to understand this powerful technology, this article will provide you with the insights you need.

Blockchain technology, which gained prominence with the rise of cryptocurrencies, is essentially a decentralized and distributed ledger that records transactions across multiple computers. This decentralized nature eliminates the need for intermediaries and enhances transparency and security. Smart contracts, on the other hand, are self-executing contracts with predefined conditions written into the code. Once these conditions are met, the contract is automatically enforced without the need for any human intervention.

Imagine a scenario where you want to buy a property. Instead of relying on multiple intermediaries such as lawyers and banks, a blockchain smart contract can automate the entire process. The contract would execute the transfer of ownership and release funds once the agreed-upon conditions, such as payment and documentation, are met. This eliminates the risk of fraud and human error, streamlining the transaction.

Implementing smart contracts on the blockchain offers numerous benefits. One of the key advantages is the removal of intermediaries, which reduces costs and improves efficiency. Transactions can be executed faster, eliminating delays associated with manual processes. Additionally, the decentralized nature of the blockchain ensures transparency and immutability, making it nearly impossible to manipulate or tamper with contract records.

In the following sections, we will explore the key components of a blockchain smart contract, the step-by-step process of creating one, best practices for smart contract development, and common challenges that developers may encounter. So let’s dive in and unlock the power of blockchain smart contracts!

Overview of Blockchain Technology

Before delving deeper into blockchain smart contracts, let’s take a moment to understand the fundamental concepts of blockchain technology itself. Originally introduced as the underlying technology for the groundbreaking cryptocurrency Bitcoin, blockchain has since evolved into a versatile and powerful tool with applications across various industries.

At its core, a blockchain is a decentralized and distributed ledger that records data across multiple computers, known as nodes. Each node in the network maintains a copy of the entire blockchain, ensuring transparency and security. Unlike traditional centralized systems where data is stored on a single server or controlled by a central authority, a blockchain is maintained by a network consensus.

Blockchain operates on the principle of cryptographic hashes, which are unique identifiers generated by complex mathematical algorithms. Each block in the chain contains a hash of the previous block, creating an immutable and transparent link between them. This structure ensures the integrity of the data and prevents it from being tampered with.

One of the key features of blockchain technology is its decentralized nature. Traditional systems rely on intermediaries such as banks, governments, and third-party service providers to validate and record transactions. In contrast, blockchain enables peer-to-peer transactions, eliminating the need for intermediaries and reducing associated costs and delays.

Another crucial aspect of blockchain technology is its security. The decentralized nature of the network, combined with cryptographic algorithms, ensures that data stored on the blockchain is highly secure. Because each transaction is recorded and linked to the previous one, the entire history of transactions is transparent and virtually tamper-proof.

Blockchain technology has the potential to revolutionize industries beyond finance. It can be used for supply chain management, healthcare records, voting systems, intellectual property protection, and much more. By eliminating the need for trust in a centralized authority, blockchain fosters trust among participants in a transparent and immutable way.

As blockchain technology continues to evolve, it is important to note that there are different types of blockchains. Public blockchains, like Bitcoin and Ethereum, are open to anyone and allow anyone to participate in the network. Private blockchains, on the other hand, are restricted to a specific group of participants and often used by enterprises for internal purposes.

In the next section, we will focus specifically on smart contracts – one of the most exciting and transformative applications of blockchain technology.

Understanding Smart Contracts

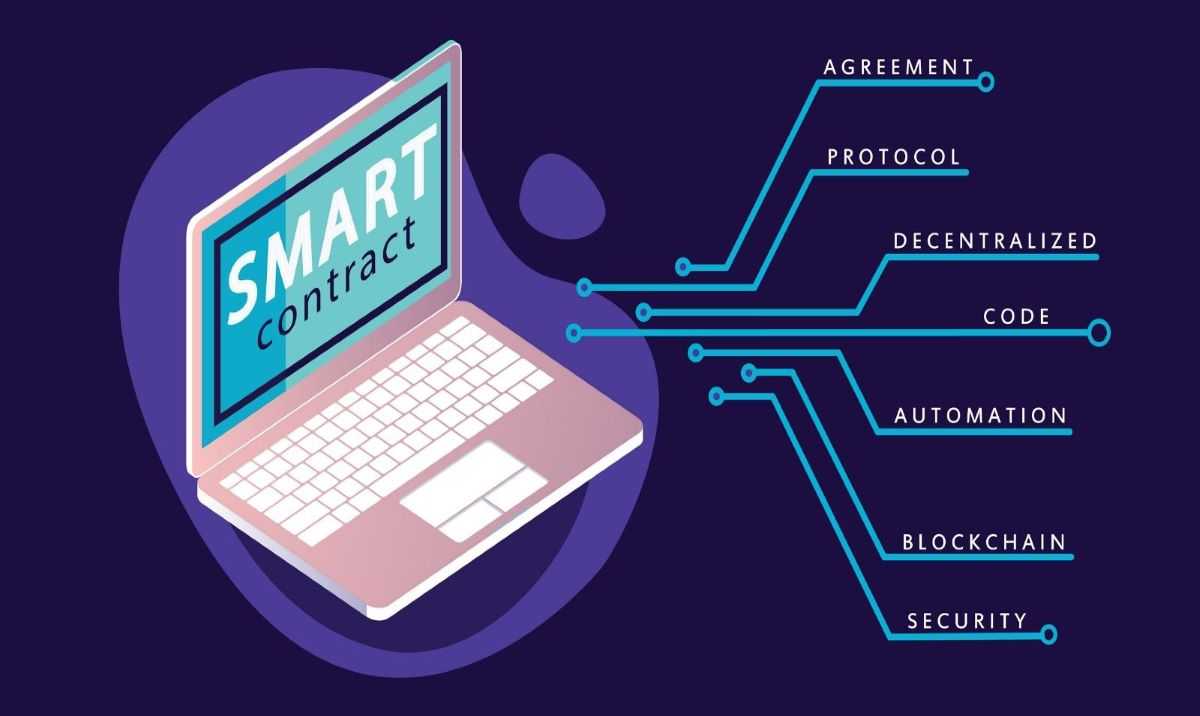

Smart contracts are self-executing contracts with predefined conditions written into the code. They run on blockchain technology, enabling the automation and enforcement of contractual agreements without the need for intermediaries or third parties. Smart contracts operate on the principle of “if-then” statements, meaning that if a certain condition is met, a specific action is automatically executed.

Unlike traditional contracts that are written in natural language and require human interpretation, smart contracts are code-based and operate on a set of predetermined rules. These rules are built into the smart contract’s code, ensuring that the contract’s conditions and actions are executed exactly as programmed.

Smart contracts have various components, including the contract’s terms and conditions, the participating parties, and the specific actions to be performed once the conditions are met. These contracts are typically stored on a blockchain, making them transparent, immutable, and tamper-proof.

Smart contracts can facilitate a wide range of transactions and agreements, such as financial transfers, real estate transactions, supply chain management, and even voting systems. The decentralized and transparent nature of blockchain ensures that all parties can verify the terms of the contract and its execution, reducing the risk of fraud or misinterpretation.

For example, let’s consider a real estate transaction. With a smart contract, the buyer and seller can define the conditions of the sale, including the purchase price and the required documentation. Once the agreed-upon conditions are met (e.g., the payment is made and the documents are verified), the smart contract automatically transfers the ownership of the property, eliminating the need for intermediaries such as lawyers or escrow agents.

Smart contracts bring numerous benefits to the table. They eliminate the need for trust in a centralized authority, reduce costs by removing intermediaries, and streamline transactions by automating processes. Additionally, smart contracts eliminate the possibility of human error or malicious interference.

It is important to note that smart contracts are not infallible and must be carefully coded and audited. Bugs or vulnerabilities in the code can lead to unintended consequences or exploits. Therefore, proper development, testing, and security practices are crucial when implementing smart contracts on the blockchain.

In the next section, we will dive deeper into the benefits of implementing smart contracts on the blockchain and explore how they can transform various industries.

Benefits of Implementing Smart Contracts on the Blockchain

Implementing smart contracts on the blockchain brings numerous benefits to various industries. Let’s explore some of the key advantages:

- Automation: Smart contracts allow for the automation of contractual agreements. Once the predetermined conditions are met, the smart contract automatically executes the agreed-upon actions, saving time and reducing the need for manual intervention.

- Efficiency: By removing intermediaries and streamlining processes, smart contracts increase efficiency. Transactions can be executed faster and with fewer errors, resulting in cost savings and improved productivity.

- Transparency: Blockchain technology provides transparency by maintaining a public ledger of all transactions. Smart contracts, stored on the blockchain, allow all parties involved to verify the terms and conditions of the contract, reducing the risk of fraud or misinterpretation.

- Security: The decentralized nature of blockchain and the cryptographic algorithms used ensure that smart contracts are secure. Once a transaction is recorded on the blockchain, it becomes nearly impossible to manipulate or tamper with, providing a high level of data integrity and security.

- Cost Savings: Smart contracts eliminate the need for intermediaries, such as lawyers or escrow agents, thereby reducing associated costs. By automating processes and eliminating unnecessary paperwork, smart contracts can significantly reduce transaction costs across various industries.

- Speed: The automation provided by smart contracts eliminates the need for manual processing, resulting in faster transaction execution. This is particularly beneficial in time-sensitive industries, such as supply chain management or financial services.

- Accuracy: Smart contracts operate based on predefined rules and conditions. By removing manual intervention, the chances of human errors and omissions are minimized, ensuring accurate and consistent execution of the contract.

- Immutable Records: Once a smart contract is executed and recorded on the blockchain, it becomes a permanent and unchangeable record. This immutability ensures the integrity of the transaction history and provides an auditable trail of events.

The benefits of implementing smart contracts on the blockchain extend across various sectors, including finance, supply chain management, insurance, healthcare, and more. By leveraging the power of blockchain technology and smart contracts, organizations can achieve greater efficiency, reduce costs, and enhance the trust and security of their operations.

In the next section, we will delve into the key components required to create a blockchain smart contract and explore the step-by-step process involved.

Key Components of a Blockchain Smart Contract

A blockchain smart contract consists of several key components that are crucial for its proper implementation and execution. Understanding these components is essential for creating effective and efficient smart contracts. Let’s explore the key components:

- Terms and Conditions: The terms and conditions define the rules and obligations that both parties agree to when entering into a smart contract. These conditions are typically written in code and can range from simple to complex, depending on the nature of the contract.

- Participants: A smart contract involves multiple participants, typically represented by their unique digital identities. Each participant has a specific role and set of permissions within the smart contract.

- Assets and Values: Smart contracts often involve the transfer of digital or physical assets, such as cryptocurrencies, documents, or property titles. The contract must define the assets being transferred and their associated values.

- Trigger Events: Smart contracts are executed based on specific trigger events. These events can be predefined conditions that need to be met, such as a payment being made, a deadline passing, or an external data feed providing a specific input.

- Actions and Functions: Smart contracts include a series of actions and functions that are executed when the trigger events occur. These actions can involve the transfer of assets, updating of records, or executing specific calculations or operations.

- Validation and Consensus: In a decentralized blockchain network, the validation and consensus mechanism ensure that the smart contract’s execution is agreed upon by all participating nodes. This prevents unauthorized or fraudulent transactions.

- Digital Signatures: Each participant in the smart contract uses their digital signature to authorize and validate their actions within the contract. These signatures provide cryptographic proof of identity and ensure the integrity and authenticity of the contract.

- Error Handling: Smart contracts need to include error handling mechanisms to handle exceptional situations or unexpected events. Proper error handling ensures that the contract can gracefully handle issues and prevent unintended consequences.

- Security Measures: To ensure the security of a smart contract, it is essential to include appropriate security measures. This includes secure coding practices, vulnerability testing, and mechanisms to prevent unauthorized access or tampering of the contract’s code or data.

Each of these components plays a crucial role in the successful execution of a blockchain smart contract. By carefully defining and incorporating these components into the contract’s code, developers can create robust and reliable smart contracts that automate and enforce agreements in a secure and efficient manner.

In the next section, we will dive into a step-by-step guide on how to create a blockchain smart contract.

Step-by-step Guide to Creating a Blockchain Smart Contract

Creating a blockchain smart contract involves several steps, from defining the contract’s terms and conditions to deploying it on a blockchain network. Let’s walk through a step-by-step guide on how to create a blockchain smart contract:

- Identify the Use Case: Start by clearly identifying the specific use case for your smart contract. Determine what problem it aims to solve and how it can streamline processes or improve efficiency within a particular industry or domain.

- Define the Terms and Conditions: Outline and define the terms and conditions of the smart contract. Specify the actions, trigger events, and conditions that will determine how the contract executes and what it delivers.

- Choose the Blockchain Platform: Select a suitable blockchain platform that supports the execution of smart contracts. Ethereum is one of the most popular choices as it provides a robust and widely adopted platform for creating and deploying smart contracts.

- Write the Smart Contract Code: Depending on the chosen blockchain platform, you will need to write the smart contract code in a programming language supported by that platform. For Ethereum, the programming language is Solidity, while other platforms might use languages such as Chaincode or WebAssembly.

- Define the Data Structures and Functions: Define the necessary data structures and functions within the smart contract code. This includes variables, data types, and the operations or actions that the contract will perform when triggered.

- Test the Smart Contract: Thoroughly test the smart contract code to ensure it functions as intended. Conduct both unit tests and integration tests to verify the contract’s behavior in different scenarios and edge cases.

- Compile the Smart Contract: Compile the smart contract code into a bytecode format that can be executed on the blockchain platform. This is typically done using a compiler or tool provided by the platform.

- Deploy the Smart Contract: Deploy the compiled smart contract onto the chosen blockchain network. This involves creating a transaction that includes the bytecode and deploying it to the network using a wallet or a development tool.

- Interact with the Smart Contract: Once deployed, you can interact with the smart contract by invoking its functions or triggering its events. This can be done using a web interface, a command-line tool, or through custom applications that interact with the blockchain.

- Maintain and Update the Contract: Smart contracts may require updates or maintenance over time. It is important to monitor the contract’s performance, address any issues that arise, and apply updates to improve its functionality or security.

Remember, creating a blockchain smart contract requires careful planning, coding, and testing. It is essential to have a solid understanding of the chosen blockchain platform and the programming language used for smart contract development. Following best practices and security measures will help ensure the reliability and integrity of your smart contract.

In the next section, we will explore the process of testing and deploying a blockchain smart contract.

Testing and Deploying a Blockchain Smart Contract

Testing and deploying a blockchain smart contract is a critical step in the development process. Thorough testing helps ensure that the contract functions as intended and meets the specified requirements. Once the contract has been thoroughly tested, it can be deployed on the chosen blockchain network to make it accessible to users. Let’s explore the process of testing and deploying a blockchain smart contract:

Testing the Smart Contract

Testing a smart contract involves evaluating its functionality, performance, and security. Here are some key steps in testing a smart contract:

- Unit Testing: Perform unit tests to verify the behavior of individual functions or components within the smart contract code. This helps identify and fix any bugs or errors at an early stage.

- Integration Testing: Conduct integration tests to assess how different components of the smart contract interact with each other and with external systems or dependencies.

- Functional Testing: Test the contract’s functionality against predefined test cases to ensure that it behaves correctly in different scenarios. This includes testing contract deployment, invoking functions, and handling different conditions.

- Performance Testing: Evaluate the performance of the smart contract by simulating various levels of load and stress. This helps identify any bottlenecks or scalability issues that may arise in real-world usage.

- Security Audits: Conduct security audits to identify vulnerabilities or potential exploits in the contract code. This involves reviewing the code for common security pitfalls, such as reentrancy attacks, unauthorized access, or integer overflows.

- Gas Optimization: Gas is a measure of computational effort in the Ethereum blockchain. Optimize the smart contract’s code to minimize the gas consumption, as higher gas costs can impact the contract’s efficiency and transaction costs.

Deploying the Smart Contract

Once the smart contract has passed all necessary tests, it can be deployed on the blockchain network. Here’s a general process for deploying a smart contract:

- Select the Deployment Environment: Choose the appropriate deployment environment for your smart contract. This can be a public blockchain network like Ethereum, a private blockchain network, or a test network for development purposes.

- Prepare the Deployment Transaction: Create a transaction that includes the compiled bytecode of the smart contract. This transaction is used to deploy the contract onto the blockchain network.

- Set Deployment Parameters: Specify any required input or configuration parameters for the deployment, such as constructor arguments or initial values for contract variables.

- Submit the Deployment Transaction: Sign and submit the deployment transaction to the blockchain network. This typically requires a wallet or a development tool that allows interaction with the network.

- Wait for Confirmation: After submitting the deployment transaction, wait for a sufficient number of confirmations to ensure that the contract is successfully deployed and recognized by the network.

- Interact with the Deployed Contract: Once deployed, the smart contract can be interacted with by invoking its functions or triggering events. Users or other smart contracts can interact with it according to the specified terms and conditions.

Testing and deploying a blockchain smart contract are crucial steps to ensure its functionality, security, and usability. Thorough testing mitigates potential risks and helps deliver a reliable and robust contract. By following best practices, developers can confidently deploy their smart contracts and enable real-world usage on the blockchain network.

In the next section, we will discuss best practices for developing blockchain smart contracts.

Best Practices for Developing Blockchain Smart Contracts

Developing blockchain smart contracts requires careful planning, coding, and implementation to ensure their effectiveness, security, and reliability. Here are some best practices to consider when developing blockchain smart contracts:

- Clearly Define the Objectives: Clearly define the objectives and requirements of the smart contract before starting the development process. This includes identifying the problem it aims to solve and the desired outcomes.

- Thoroughly Design the Contract: Carefully design the contract’s architecture, taking into account all the necessary components, functions, and business logic. Follow standard design patterns to ensure an organized and maintainable codebase.

- Emphasize Security: Security should be a top priority when developing smart contracts. Follow best security practices, such as input validation, using secure coding techniques, and conducting thorough security audits to identify and fix vulnerabilities.

- Keep Contracts Simple: Keep the smart contract logic as simple as possible. Avoid unnecessary complexity and intricate dependencies, as this can increase the chances of bugs and vulnerabilities.

- Comment and Document Code: Provide clear and comprehensive comments and documentation for the smart contract code. This helps other developers understand the contract’s functionality and makes it easier to maintain and update in the future.

- Test Rigorously: Thoroughly test the smart contract code using a combination of unit tests, integration tests, and functional tests. Test for different scenarios and edge cases to ensure the contract behaves as expected and handles exceptional conditions properly.

- Consider Gas Optimization: Optimize the contract’s code to minimize gas consumption on blockchain platforms. Gas optimization helps reduce transaction costs and improves the overall efficiency of the contract’s execution.

- Use Libraries and Standards: Leverage existing libraries and standard protocols when developing smart contracts. This helps reduce development time, ensures compatibility, and minimizes the chances of errors.

- Update and Maintain Contracts: Stay proactive in maintaining and updating the smart contracts. Monitor the contract’s performance, address any issues promptly, and implement updates to improve functionality, security, and efficiency.

- Follow Industry and Platform Guidelines: Stay up to date with the latest industry practices and guidelines for smart contract development. Familiarize yourself with the specific standards and guidelines of the blockchain platform you are working with.

By following these best practices, you can develop robust and secure blockchain smart contracts that fulfill their intended purposes. Remember that developing smart contracts requires constant learning and adaptation to stay abreast of evolving technologies and best practices.

In the next section, we will discuss common challenges faced during the development of blockchain smart contracts and potential solutions to overcome them.

Common Challenges and Solutions in Blockchain Smart Contract Development

Developing blockchain smart contracts comes with its own set of challenges. From coding errors to security vulnerabilities, it’s important to be aware of the common pitfalls and have strategies in place to overcome them. Here are some common challenges in blockchain smart contract development and potential solutions to address them:

- Security Vulnerabilities: Smart contracts can be susceptible to security vulnerabilities if not properly coded and audited. Common vulnerabilities include reentrancy attacks, integer overflows, and unauthorized access. To mitigate these risks, follow secure coding practices, conduct thorough security audits, and leverage existing security tools and frameworks.

- Complexity: Smart contracts can become complex, especially when dealing with intricate business logic and real-world scenarios. To mitigate complexity, follow best practices for code organization and maintainability. Break down the contract’s logic into smaller, manageable functions and use design patterns to modularize the code.

- Gas Optimization: Gas optimization is crucial to reduce transaction costs and improve the overall efficiency of smart contracts. To address gas optimization challenges, refactor the code to minimize redundant computations, reduce storage usage, and optimize loops and data structures. Additionally, consider using libraries or methodologies specifically designed for gas efficiency.

- Interoperability: Ensuring interoperability between different blockchain platforms is a challenge when developing smart contracts. To address this, follow industry standards and use compatible protocols and libraries. Consider using cross-chain bridges or interoperability solutions that facilitate communication and data exchange between different blockchain networks.

- Scalability: Scalability is a common challenge in blockchain, particularly when executing complex smart contracts on large networks. To address scalability issues, use mechanisms like off-chain computations, state channels, or layer-two solutions to reduce the computational burden on the main blockchain network.

- Legal and Regulatory Compliance: Smart contracts need to comply with legal and regulatory requirements, which can vary across jurisdictions. Ensure that your smart contract adheres to the relevant legal frameworks by involving legal experts during the development process. Consider implementing features like self-executing dispute resolution mechanisms to ensure compliance and address potential legal conflicts.

- Testing Rigor: Testing smart contracts thoroughly is essential to identify and fix bugs before deployment. To improve testing rigor, develop comprehensive test cases that cover various scenarios, including edge cases and exceptional conditions. Embrace automated testing frameworks and adopt a test-driven development approach to ensure consistent and reliable contract behavior.

- Upgradability and Maintenance: Smart contracts may require updates or maintenance over time to accommodate changing requirements or fix bugs. Design contracts with upgradability in mind, using mechanisms like proxy contracts or modular architecture. Implement version control and follow a disciplined approach to contract upgrades to ensure smooth transition and backward compatibility.

By being aware of these common challenges and proactively implementing solutions, you can mitigate risks and develop robust and reliable blockchain smart contracts. It’s important to continuously learn and adapt as the blockchain technology landscape evolves and new challenges emerge.

In the next section, we will conclude our exploration of blockchain smart contracts.

Conclusion

Blockchain smart contracts have emerged as a powerful technology with the potential to revolutionize multiple industries. By automating contractual agreements and eliminating the need for intermediaries, smart contracts offer transparency, efficiency, and security like never before. Through this article, we have explored the key components of smart contracts, the benefits they bring to the table, and the step-by-step process of creating and deploying them.

Understanding the fundamentals of blockchain technology and the concept of smart contracts is essential in harnessing their potential. The transparency and immutability of blockchain technology ensure the integrity of smart contract transactions, reducing risks and increasing trust among parties involved.

However, developing blockchain smart contracts is not without its challenges. Security vulnerabilities, complexity, gas optimization, and interoperability are some of the common hurdles to overcome. By following best practices, conducting thorough testing, and addressing these challenges head-on, developers can create robust and secure smart contracts.

The adoption of smart contracts is growing across industries, enabling faster, more secure, and cost-effective transactional processes. From financial services and supply chain management to healthcare and voting systems, smart contracts have the potential to enhance efficiency, reduce costs, and improve trust in various sectors.

As blockchain technology continues to evolve, it is essential to stay updated with the latest advancements, industry standards, and regulatory frameworks. Continuous learning and adaptation will ensure that blockchain smart contracts remain effective, secure, and aligned with the needs of businesses and users.

In conclusion, blockchain smart contracts are transforming the way we establish and enforce agreements. By leveraging the power of blockchain technology, we can unlock vast opportunities for automation, transparency, and trust. As the adoption and innovation in this field continue, smart contracts are poised to reshape industries, creating a more connected and efficient digital economy.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance