Home>Finance>How To Remove Closed Accounts From Your Credit Report

Finance

How To Remove Closed Accounts From Your Credit Report

Published: October 20, 2023

Learn how to remove closed accounts from your credit report with our expert finance tips. Improve your credit score and financial health today!

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding Closed Accounts on Your Credit Report

- Why You Should Remove Closed Accounts

- How Closed Accounts Affect Your Credit Score

- Steps to Remove Closed Accounts from Your Credit Report

- Gather Necessary Documents and Information

- Review Your Credit Reports

- Dispute Any Errors or Inaccuracies

- Follow Up with Credit Bureaus

- Utilize a Credit Repair Service (Optional)

- Additional Tips for Removing Closed Accounts

- Conclusion

Introduction

Welcome to our comprehensive guide on how to remove closed accounts from your credit report. Your credit report plays a crucial role in your financial life, providing lenders with essential information about your creditworthiness. It includes details about your open and closed accounts, payment history, and credit utilization, among other factors.

Having closed accounts on your credit report can impact your credit score and may hinder your ability to secure future credit. That’s why it’s important to understand the process of removing closed accounts and take the necessary steps to ensure your credit report accurately reflects your current financial situation.

In this article, we will explain what closed accounts are, why you should remove them from your credit report, how they affect your credit score, and provide you with a step-by-step guide on how to remove them. Whether you’re planning to apply for a loan, mortgage, or credit card, improving your credit report by removing closed accounts can increase your chances of approval and help you secure better terms and interest rates.

Before we dive into the details, it’s important to note that removing closed accounts from your credit report may take time and effort. It involves reviewing your credit reports, disputing any errors, following up with credit bureaus, and potentially utilizing a credit repair service. However, the benefits of a clean credit report will be well worth the investment of time and energy.

Now, let’s begin by understanding what exactly closed accounts are and why they have an impact on your credit score.

Understanding Closed Accounts on Your Credit Report

Closed accounts refer to credit accounts that have been closed by either you or the lender. This could include credit cards, loans, or other lines of credit that you no longer use or have paid off. When you close an account, it means you have officially ended your relationship with the lender and no longer have access to the credit line associated with that account.

Even though these accounts are closed, they can still appear on your credit report for a certain period of time. This is because your credit report is a comprehensive record of your credit history, including both open and closed accounts. Closed accounts typically remain on your credit report for up to seven years from the date of activity.

It’s important to note that closed accounts can have an impact on your credit score. While positive closed accounts can demonstrate responsible credit management, negative closed accounts such as delinquent or charged-off accounts can have a detrimental effect on your creditworthiness.

Understanding the status of closed accounts on your credit report is crucial, as it allows you to assess the impact they may have on your overall credit profile. By knowing which closed accounts are affecting your credit score, you can take the necessary steps to remove any inaccuracies or negative information from your credit report.

In the following sections, we will delve deeper into why it’s important to remove closed accounts from your credit report and how they can affect your credit score. We will also provide you with the necessary steps to successfully remove closed accounts and improve your credit standing.

Why You Should Remove Closed Accounts

Removing closed accounts from your credit report is an essential step towards improving your credit score and overall financial health. Here are a few key reasons why you should consider removing closed accounts:

- Impact on credit utilization: Closed accounts still factor into your overall credit utilization ratio, which is a significant component of your credit score. If you have a high credit utilization ratio due to the presence of closed accounts with high balances, it can negatively impact your credit score. By removing these closed accounts, you can effectively lower your credit utilization ratio and potentially boost your credit score.

- Prevent negative information from affecting your credit: Closed accounts with negative payment history, such as late payments or defaults, can continue to impact your credit score. Removing these closed accounts can help eliminate any negative marks on your credit report and improve your overall credit profile.

- Accuracy of your credit report: Your credit report should accurately reflect your credit history and financial situation. Closed accounts that are incorrectly reported or contain errors can unfairly lower your credit score. By removing these inaccuracies, you can ensure that your credit report provides a true representation of your creditworthiness.

- Enhance your borrowing potential: Lenders often assess your credit report when considering your loan or credit card applications. By removing closed accounts from your credit report, you can present a cleaner credit history and increase your chances of being approved for credit at more favorable terms and interest rates.

- Financial peace of mind: Having a clear and accurate credit report can provide you with peace of mind and confidence in your financial standing. It allows you to have a better understanding of your creditworthiness and take control of your financial future.

By taking the necessary steps to remove closed accounts, you can proactively improve your credit score, demonstrate responsible credit management, and position yourself for better financial opportunities in the future. In the following sections, we will outline the step-by-step process of removing closed accounts from your credit report.

How Closed Accounts Affect Your Credit Score

Closed accounts can have both positive and negative impacts on your credit score. Understanding how these accounts influence your creditworthiness is crucial for managing your financial health. Here are a few key ways in which closed accounts can affect your credit score:

- Credit utilization ratio: Closed accounts still contribute to your overall credit utilization ratio, which is the amount of credit you are currently using compared to your total available credit. If you have a high credit utilization ratio due to the presence of closed accounts with balances, it can negatively impact your credit score. Lowering this ratio by removing closed accounts can help improve your credit score.

- Payment history: Closed accounts with negative payment history, such as missed payments or defaults, can significantly impact your credit score. Late payments or defaults on closed accounts can stay on your credit report for up to seven years and have a long-lasting effect on your creditworthiness. Removing these closed accounts can help eliminate the negative payment history and enhance your credit score.

- Length of credit history: Closed accounts that have a long and positive payment history can be beneficial for your credit score. They demonstrate your ability to manage credit responsibly over an extended period. Removing closed accounts with a positive payment history may shorten your overall credit history, which can slightly impact your credit score. However, the impact is generally minimal compared to the potential negative effects of closed accounts with negative payment history.

- Credit mix: Creditors and lenders prefer to see a diverse mix of credit types on your credit report, such as credit cards, loans, and mortgages. Closed accounts from different types of credit can contribute to a more favorable credit mix, which can positively influence your credit score. Removing closed accounts may impact your credit mix, but the impact is typically minimal compared to other factors.

- Overall credit health: Closed accounts can provide lenders with insights into your overall credit health. If you have many closed accounts with negative information, it may raise concerns about your ability to manage credit responsibly. Removing these closed accounts can help present a cleaner credit profile and improve your creditworthiness.

It’s important to note that the specific impact of closed accounts on your credit score will vary depending on your individual credit history and the other factors present in your credit report. However, in general, removing closed accounts with negative information and minimizing high credit utilization can have a positive impact on your credit score.

In the next section, we will provide you with a step-by-step guide on how to remove closed accounts from your credit report.

Steps to Remove Closed Accounts from Your Credit Report

If you have closed accounts on your credit report that you believe should be removed, follow these steps to successfully remove them:

- Gather Necessary Documents and Information: Start by collecting the necessary documents and information related to the closed accounts you want to remove. This may include account statements, payment records, and any correspondence with the lender.

- Review Your Credit Reports: Obtain copies of your credit reports from the three major credit bureaus: Equifax, Experian, and TransUnion. Carefully review each report to identify the closed accounts you wish to remove and check for any errors or inaccuracies.

- Dispute Any Errors or Inaccuracies: If you find errors or inaccuracies related to the closed accounts on your credit report, you have the right to dispute them. Send a written dispute letter to the credit bureau(s) that issued the report, clearly outlining the errors and providing any supporting documentation. The credit bureau will then investigate the dispute and make any necessary corrections.

- Follow Up with Credit Bureaus: After submitting your dispute letter, it’s important to follow up with the credit bureaus to ensure they are investigating your dispute within the required timeframe. Keep records of all communication, including dates and copies of any correspondence.

- Utilize a Credit Repair Service (Optional): If you find the process of removing closed accounts challenging or time-consuming, consider enlisting the help of a reputable credit repair service. These services specialize in handling credit report disputes and can assist you in navigating the process effectively.

It’s important to note that the process of removing closed accounts from your credit report may take time and patience. The credit bureaus are required to investigate disputes within 30 days, but the resolution can sometimes take longer.

Additionally, it’s important to maintain an ongoing focus on good credit habits, such as making payments on time and keeping credit utilization low. These actions can contribute to an overall positive credit profile and help offset any negative impact from closed accounts on your credit report.

By following these steps and staying diligent throughout the process, you can successfully remove closed accounts from your credit report and improve your credit standing.

In the next section, we will provide you with some additional tips to help you effectively remove closed accounts and maintain a healthy credit profile.

Gather Necessary Documents and Information

Before you begin the process of removing closed accounts from your credit report, it’s important to gather all the necessary documents and information. This will ensure that you have the necessary documentation to support your dispute and increase your chances of a successful removal. Here are the steps to gather the required documents:

- Collect Account Statements: Gather account statements for the closed accounts you wish to remove. These statements will provide detailed information about the account, including the account number, opening date, closing date, and any outstanding balances or payment history.

- Payment Records: Gather any payment records associated with the closed accounts, such as canceled checks, bank statements, or payment receipts. These records will provide evidence of your payment history and help support your dispute if there are any inaccuracies or errors on your credit report.

- Correspondence with Lender: If you have any correspondence with the lender regarding the closed accounts, such as letters or emails, make sure to keep them handy. These documents can be useful in clarifying any discrepancies and providing additional evidence to support your dispute.

- Personal Identification: Keep your personal identification documents handy, including your driver’s license, passport, or social security card. You may need to provide proof of your identity when submitting a dispute to the credit bureaus.

By gathering these documents and information ahead of time, you’ll be well-prepared to initiate the process of removing closed accounts from your credit report. Once you have everything in order, you can move on to the next step, which is reviewing your credit reports to identify any errors or inaccuracies.

Note that it’s important to keep copies of all the documents you collect. This will ensure that you have a record of your efforts to remove closed accounts and can provide evidence if needed in the future.

Now that you have gathered the necessary documents and information, we can proceed to the next section, which explores how to review your credit reports to identify any errors or inaccuracies.

Review Your Credit Reports

After gathering the necessary documents, the next step in removing closed accounts from your credit report is to review your credit reports. You will need to obtain copies of your credit reports from the three major credit bureaus: Equifax, Experian, and TransUnion. Reviewing your credit reports allows you to identify any errors or inaccuracies related to the closed accounts you wish to remove. Follow these steps to review your credit reports:

- Request Your Credit Reports: You can request a free copy of your credit reports once a year from each of the three credit bureaus through AnnualCreditReport.com. Alternatively, you can contact each credit bureau directly to obtain your reports.

- Thoroughly Examine Each Report: Carefully review each credit report to identify the closed accounts you want to remove. Pay close attention to the account details, including the account numbers, dates of closure, outstanding balances, and any negative remarks or inaccuracies associated with the accounts.

- Note Any Errors or Inaccuracies: If you come across any errors, such as incorrect balances, inaccurate payment history, or accounts that you did not close, make a note of them. These errors can affect your credit score and need to be addressed in the dispute process.

- Keep an Eye Out for Outdated Information: In some cases, closed accounts may remain on your credit report longer than necessary. Check the dates associated with the closed accounts, and if they exceed the permissible time limit (usually seven years), you can request their removal based on outdated information.

As you review your credit reports, it’s essential to pay attention to any discrepancies or incorrect information related to the closed accounts you want to remove. These errors can have a significant impact on your credit score and may need to be disputed with the credit bureaus.

By carefully reviewing your credit reports, you can pinpoint any inaccuracies and proceed to the next step, which involves disputing these errors with the credit bureaus. We will discuss this process in detail in the following section.

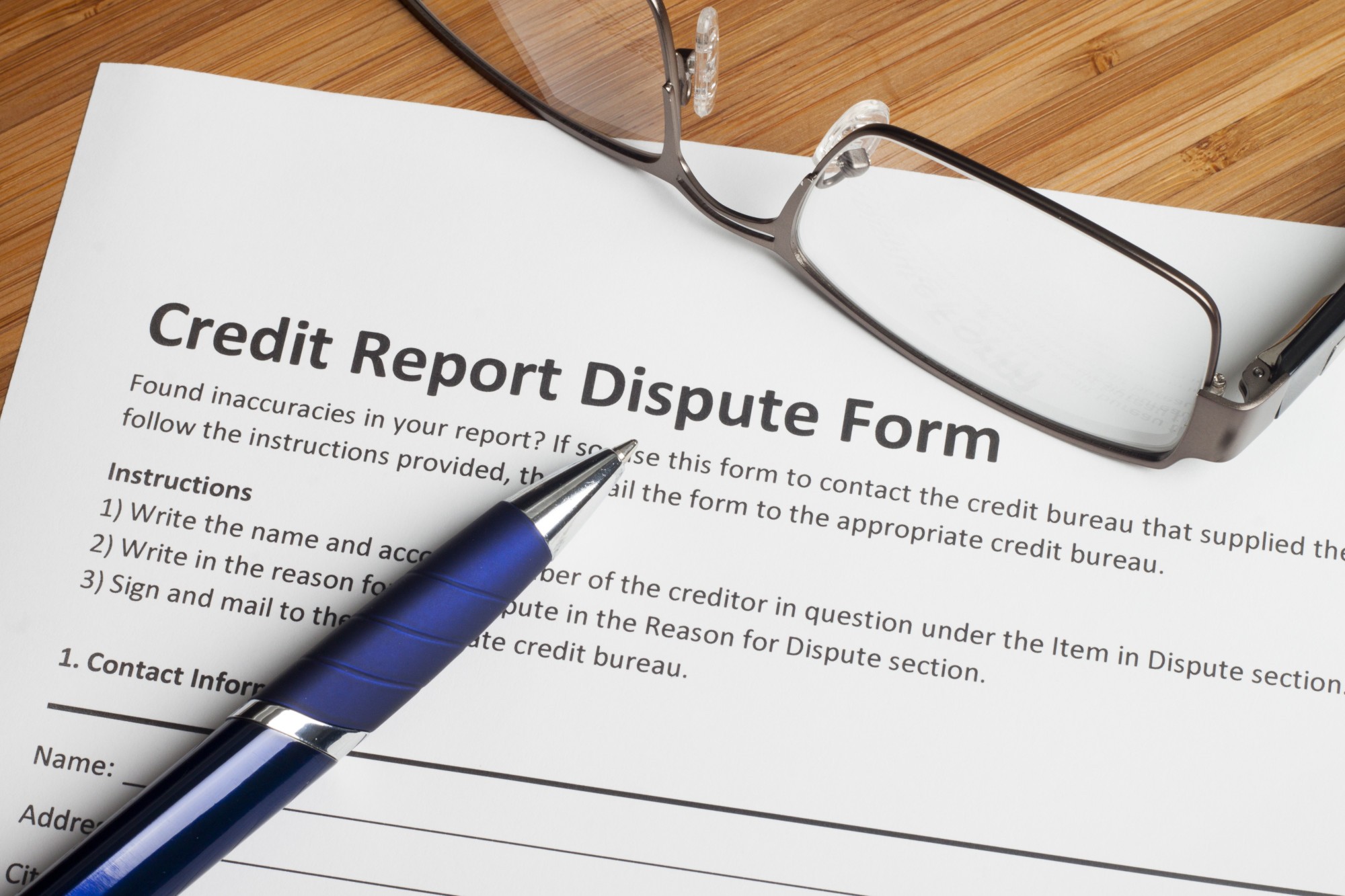

Dispute Any Errors or Inaccuracies

After reviewing your credit reports and identifying errors or inaccuracies related to the closed accounts you want to remove, the next step is to dispute these items with the credit bureaus. Disputing errors allows you to challenge and rectify any incorrect information on your credit report. Follow these steps to dispute errors or inaccuracies:

- Document the Errors: Make a list of the specific errors or inaccuracies you identified during your credit report review. Include details such as the account number, the nature of the error, and any supporting documentation you have gathered.

- Submit a Dispute: You can initiate a dispute by submitting a written dispute letter to the credit bureau(s) that issued the credit report with the errors. Include a clear explanation of the error and provide any supporting documentation you have. It’s crucial to be specific and concise in explaining the inaccuracies.

- Include Supporting Documentation: Attach copies of any documentation that supports your dispute, such as account statements, payment records, or correspondence with the lender. This documentation helps establish your case and proves that the reported information is incorrect.

- Send the Dispute Letter: Send your dispute letter via certified mail with a return receipt requested. This way, you will have proof that the credit bureau received the letter within the required timeframe. Keep a copy of the letter and the postal receipt for your records.

Remember to send a separate dispute letter to each credit bureau reporting the errors. Each credit bureau operates independently, and you must address the inaccuracies with each one individually.

Once the credit bureaus receive your dispute letter, they are responsible for investigating your claim within 30 days, as mandated by the Fair Credit Reporting Act (FCRA). During this investigation, the credit bureaus will reach out to the entity that reported the information (e.g., the lender) and request validation of the disputed items.

If the reported information is proven to be inaccurate or cannot be verified, the credit bureau must remove it from your credit report. They will then provide you with an updated copy of your credit report reflecting the changes. If the investigation does not resolve the dispute in your favor, you have the right to add a statement to the credit report with your version of the facts.

Disputing errors and inaccuracies is an essential step in removing closed accounts from your credit report. In the next section, we will discuss how to follow up with the credit bureaus to ensure the dispute process is progressing as expected.

Follow Up with Credit Bureaus

After submitting your dispute letter to the credit bureaus, it’s important to follow up to ensure that your dispute is being properly processed and investigated. Following up with the credit bureaus helps ensure that your efforts to remove closed accounts from your credit report are progressing as expected. Here are some steps to effectively follow up with the credit bureaus:

- Keep Documentation: Maintain a well-organized file with copies of all your correspondence with the credit bureaus, including your dispute letter and any supporting documentation. This documentation will be crucial in case you need to present evidence or refer back to previous communication.

- Follow the Timeline: The credit bureaus are required to investigate your dispute within 30 days of receiving your dispute letter. Keep track of the response deadline provided by each credit bureau and ensure that they are adhering to the timeline.

- Contact the Credit Bureaus: If the response deadline has passed or you have not received a satisfactory response from the credit bureaus, it’s important to reach out to them to inquire about the status of your dispute. Contact their customer service departments and reference your dispute case number to help facilitate communication.

- Escalate if Necessary: If your initial attempts to resolve the dispute are unsuccessful, you may need to escalate the matter. Consider sending a follow-up letter outlining your concerns and stating that you may seek legal recourse if the inaccuracies are not addressed promptly. Consult with a legal professional if you believe that further action is necessary.

It’s crucial to maintain open and regular communication with the credit bureaus during the dispute process. Stay proactive in ensuring that your dispute is receiving the attention it deserves and that your credit report is being updated accordingly.

Remember, the credit bureaus handle a large volume of disputes, and occasionally errors or delays may occur. However, by following up and advocating for the removal of closed accounts that are inaccurately reported, you increase your chances of success.

In the next section, we will discuss an optional step that you can consider if you find the process of removing closed accounts challenging or time-consuming: utilizing a credit repair service.

Utilize a Credit Repair Service (Optional)

If you find the process of removing closed accounts from your credit report overwhelming or time-consuming, you have the option to utilize a credit repair service. These services specialize in helping individuals navigate the credit dispute process and can provide expert assistance in removing inaccuracies from your credit report. Here are a few key points to consider when deciding whether to utilize a credit repair service:

- Expertise and Knowledge: Credit repair services have extensive knowledge of consumer rights, credit reporting laws, and the dispute process. They can efficiently handle the necessary paperwork, communicate with credit bureaus on your behalf, and provide guidance and support throughout the process.

- Time and Convenience: Disputing errors on your credit report can be time-consuming, requiring research, documentation, and regular communication with the credit bureaus. By utilizing a credit repair service, you can offload these tasks and save yourself time and effort.

- Experience and Success Rates: Credit repair services often have experience in dealing with a wide range of credit-related issues. They understand the common pitfalls and best approaches for resolving disputes, which can increase the likelihood of a successful outcome.

- Cost Considerations: It’s important to weigh the cost of using a credit repair service against the potential benefits. Credit repair services typically charge fees for their expertise and assistance. Evaluate your individual circumstances and the impact that the inaccuracies on your credit report may have on your financial goals.

When selecting a credit repair service, it’s crucial to do your research and choose a reputable and legitimate company. Look for established companies with positive customer reviews, transparent pricing, and a proven track record of success. Avoid companies that make lofty promises or charge excessive fees upfront.

Remember that utilizing a credit repair service is entirely optional. If you have the time, knowledge, and patience to navigate the dispute process on your own, you can successfully remove closed accounts from your credit report without outside assistance.

In the final section, we will provide you with additional tips to help you effectively remove closed accounts and maintain a healthy credit profile.

Additional Tips for Removing Closed Accounts

Removing closed accounts from your credit report can take time and effort, but with these additional tips, you can increase your chances of success and maintain a healthy credit profile:

- Stay organized: Keep a detailed record of all communications, including copies of letters, emails, and supporting documentation. This will help you track your progress and provide evidence if needed in the future.

- Be persistent: If your initial dispute is not successful, don’t give up. Continue to follow up with the credit bureaus and provide any additional information or documentation that may support your case.

- Maintain good credit habits: While removing closed accounts is important, focus on improving other aspects of your credit profile as well. Make all payments on time, keep credit utilization low, and manage your credit responsibly to build a positive credit history.

- Monitor your credit regularly: Regularly check your credit reports to ensure that the closed accounts have been removed and that there are no new errors or inaccuracies. You can request a free annual credit report from each of the three credit bureaus or utilize credit monitoring services.

- Consider professional advice: If you encounter challenges or feel overwhelmed during the process, don’t hesitate to seek advice from credit counseling agencies or consult with a financial professional. They can provide guidance tailored to your specific situation.

Removing closed accounts from your credit report is an important step towards maintaining a healthy credit profile and improving your overall financial well-being. By following these tips and staying persistent, you can successfully remove inaccurately reported closed accounts and positively impact your credit score.

Remember, the journey to a clean credit report may take time, but the benefits of an improved credit standing, better loan rates, and financial peace of mind make it well worth the effort.

Finally, always prioritize responsible financial management and credit habits to maintain a strong credit profile for years to come.

With the information and strategies provided in this guide, you are now well-equipped to take action and remove closed accounts from your credit report.

Conclusion

Removing closed accounts from your credit report is a crucial step towards improving your credit score and overall financial health. By understanding the impact of closed accounts, gathering necessary documents, reviewing your credit reports, disputing errors, and following up with the credit bureaus, you can successfully remove inaccurately reported closed accounts from your credit report.

While the process may require time, effort, and persistence, the benefits of a clean credit report are significant. Removing closed accounts can lower your credit utilization ratio, eliminate negative payment history, and enhance your borrowing potential. It can also provide you with financial peace of mind and improve your chances of securing credit at more favorable terms and interest rates.

Throughout the process, it’s important to stay organized, be persistent, and maintain good credit habits. Keep track of all correspondence and documentation, follow up with the credit bureaus, and regularly monitor your credit reports to ensure accuracy. Consider seeking professional advice when needed and utilize credit repair services if necessary.

Remember, removing closed accounts from your credit report is just one aspect of building and maintaining a healthy credit profile. Continue to practice responsible credit management, make timely payments, and diversify your credit mix to achieve long-term financial success.

By following the steps and tips outlined in this guide, you are well-equipped to take control of your credit report and improve your financial standing. So, take action today and start the journey towards a clean and accurate credit history.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance