Finance

How To Report A 1031 Exchange On A Tax Return

Published: October 29, 2023

Learn how to report a 1031 exchange on your tax return and save on finance. Maximize your tax benefits with our step-by-step guide.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding the Basics of a 1031 Exchange

- Eligibility Requirements for Reporting a 1031 Exchange

- Determining the Value of the Exchanged Property

- Reporting the Gain or Loss from the 1031 Exchange

- Step-by-Step Guide to Reporting a 1031 Exchange on Your Tax Return

- Reporting the Exchange on Form 8824

- Filing Deadlines and Extensions for Reporting a 1031 Exchange

- Common Mistakes to Avoid When Reporting a 1031 Exchange

- Seeking Professional Assistance for Reporting a 1031 Exchange

- Conclusion

Introduction

A 1031 exchange, also known as a like-kind exchange, is a powerful tax strategy that allows real estate investors to defer capital gains taxes when selling investment properties and reinvesting the proceeds into other qualifying properties. This tax-deferral provision, outlined in Section 1031 of the Internal Revenue Code, provides investors with a unique opportunity to grow their real estate portfolio while deferring tax liabilities.

Understanding how to report a 1031 exchange on your tax return is crucial to ensure compliance with IRS regulations and maximize the tax benefits of this strategy. In this article, we will guide you through the process of reporting a 1031 exchange and provide helpful tips to avoid common mistakes.

Before diving into the intricacies of reporting a 1031 exchange, it is important to have a firm grasp of the basics. A 1031 exchange involves the exchange of one investment property for another, allowing investors to defer taxes on the capital gains realized from the sale of the relinquished property. However, it is important to note that personal residences, stocks, bonds, and partnership interests do not qualify for 1031 exchanges.

To be eligible for a 1031 exchange, the properties involved must be of like-kind, meaning they are similar in nature or character. For example, you can exchange a residential rental property for a commercial property or a vacant land for an office building. The IRS provides broad guidelines for determining like-kind properties, but it is always advisable to consult with a tax professional to ensure compliance.

When reporting a 1031 exchange on your tax return, you need to determine the value of the exchanged property. This is important because the capital gains taxes are deferred rather than eliminated, and the value of the replacement property will affect the basis and potential tax liability in the future.

Reporting the gain or loss from a 1031 exchange requires careful calculation and documentation. The tax implications will depend on factors such as the adjusted basis of the relinquished property, any cash or debt relief received, and the fair market value of the replacement property. Properly reporting these figures will help determine the taxable gain or loss and ensure accurate reporting on your tax return.

Now that we have covered the basics, we will provide you with a step-by-step guide on how to report a 1031 exchange on your tax return. Follow these instructions carefully to avoid any errors or omissions that may trigger an IRS audit or result in unnecessary tax liabilities.

Understanding the Basics of a 1031 Exchange

A 1031 exchange, also referred to as a like-kind exchange, is a tax-deferral strategy that allows real estate investors to sell an investment property and reinvest the proceeds into another qualifying property, while deferring the capital gains tax. This tax provision is outlined in Section 1031 of the Internal Revenue Code.

One key concept to understand is that a 1031 exchange involves the exchange of one investment property for another. The properties involved must be of like-kind, meaning they are similar in nature or character. For example, you can exchange a commercial building for a residential rental property, or a vacant land for an industrial property.

It’s important to note that a 1031 exchange does not eliminate the capital gains tax; it simply defers it to a future date. This allows real estate investors to preserve their capital and use it to acquire more valuable or income-producing properties. By reinvesting the proceeds into another property, investors can continue to build wealth and grow their real estate portfolio.

There are several benefits to utilizing a 1031 exchange. Firstly, it allows investors to defer the payment of capital gains tax, which can free up funds for additional property investments or other financial opportunities. Secondly, it provides the opportunity to consolidate or diversify property holdings without incurring immediate tax consequences. Lastly, it offers potential tax savings and increased cash flow by allowing investors to switch from a high-maintenance property to a more passive income-producing property.

It’s important to understand that not all properties are eligible for a 1031 exchange. Personal residences, stocks, bonds, and partnership interests do not qualify. However, most other types of real estate, such as commercial properties, rental properties, vacant land, and even leasehold interests, can be eligible for a 1031 exchange.

Additionally, there are specific rules and timelines that must be followed when conducting a 1031 exchange. The timeline starts when the relinquished property is sold, and the investor has 45 days to identify potential replacement properties. The investor then has 180 days from the sale of the relinquished property to acquire one or more replacement properties. It’s important to adhere to these deadlines to ensure the exchange qualifies for tax deferral.

In summary, a 1031 exchange is a powerful tax strategy that allows real estate investors to defer capital gains taxes when selling an investment property and reinvesting the proceeds into another qualifying property. This strategy can provide significant financial benefits and allow investors to continue building wealth in the real estate market. Understanding the basics of a 1031 exchange is crucial before proceeding with this tax-deferral strategy.

Eligibility Requirements for Reporting a 1031 Exchange

To qualify for tax-deferred treatment under a 1031 exchange, certain eligibility requirements must be met. Understanding these requirements is essential to ensure compliance with the Internal Revenue Service (IRS) regulations and maximize the benefits of this tax strategy.

First and foremost, the properties involved in the exchange must be held for investment or used in a trade or business. This means that personal residences, vacation homes, and properties primarily held for resale do not qualify for a 1031 exchange. The IRS considers properties that generate rental income or are actively used in a business operation as eligible for like-kind exchange treatment.

Furthermore, the properties involved in the exchange must be of like-kind. Like-kind refers to the nature or character of the properties, rather than their grade or quality. This means that a wide range of real estate properties can be eligible, such as residential rental properties, commercial buildings, vacant land, and even leasehold interests. However, exchanging real estate for other types of assets, such as stocks or bonds, does not qualify for a 1031 exchange.

It’s important to note that foreign real estate is not considered like-kind to U.S. real estate. Therefore, a 1031 exchange can only be conducted with properties located within the United States.

In addition to the like-kind requirement, there are strict timelines that must be followed when conducting a 1031 exchange. Within 45 days of selling the relinquished property, the taxpayer must identify one or more potential replacement properties. The identification must be made in writing and delivered to a qualified intermediary, who is responsible for facilitating the exchange process. The taxpayer can identify up to three potential replacement properties without regard to their fair market value, or they can identify more than three properties as long as the total fair market value does not exceed 200% of the relinquished property’s value. It’s crucial to meet this 45-day identification deadline to maintain eligibility for the tax-deferred treatment.

The second timeline requirement states that the taxpayer must acquire the replacement property within 180 days of selling the relinquished property. This 180-day period includes the initial 45-day identification period. It’s important to note that the replacement property must be received by the taxpayer before the end of the 180-day period, not just under contract or in the process of acquisition.

Lastly, it’s worth mentioning that there may be certain limitations or restrictions specific to individual states or local jurisdictions concerning 1031 exchanges. It’s essential to consult with a tax professional or qualified intermediary familiar with the laws in your area to ensure compliance with all applicable regulations.

In summary, to be eligible for reporting a 1031 exchange, properties must be held for investment or business use, and they must be of like-kind. Additionally, strict timelines must be adhered to, including the 45-day identification period and the 180-day replacement property acquisition period. Understanding these eligibility requirements is crucial to successfully navigate a 1031 exchange and fully benefit from its tax-deferral advantages.

Determining the Value of the Exchanged Property

When participating in a 1031 exchange, accurately determining the value of the exchanged property is crucial for proper reporting and tax calculations. The value of the exchanged property plays a significant role in determining the basis and potential tax liability of the replacement property. Let’s explore the key factors involved in determining the value of the exchanged property.

The value of the relinquished property, also known as the “sales price,” is generally based on the fair market value at the time of the exchange. Fair market value is the price that the property would sell for on the open market, assuming a willing buyer and seller. In most cases, this value is determined by a professional real estate appraiser, who assesses various factors such as comparable sales, location, condition, and market trends.

It’s important to note that the value of the exchanged property does not necessarily equate to the purchase price or the original cost of the property. This is because the adjusted basis of the relinquished property comes into play. The adjusted basis is the original cost plus any improvements made to the property, minus any depreciation claimed over the years. The adjusted basis is used to calculate the capital gain or loss on the sale of the property.

Another factor to consider when determining the value of the exchanged property is the amount of cash received or paid at the time of the exchange. If cash or non-like-kind property is received in addition to the replacement property, it is referred to as “boot.” Boot can result in taxable gain to the extent of the cash received or the fair market value of the non-like-kind property.

In addition, any mortgage or debt that is either assumed by the buyer of the relinquished property or transferred to the replacement property affects the overall value of the exchange. Any decrease in debt is considered “debt relief,” while any increase in debt is considered “debt replacement.” Debt relief can result in taxable gain, while debt replacement can increase the basis of the replacement property.

It is important to keep detailed documentation and records of all financial transactions and property values involved in the 1031 exchange. This includes copies of appraisals, HUD-1 settlement statements, loan documents, and any other relevant financial documentation. These records will be essential when reporting the exchange on your tax return and may be requested by the IRS in the event of an audit.

Ultimately, accurately determining the value of the exchanged property is crucial for ensuring compliance with IRS regulations and maximizing the tax benefits of a 1031 exchange. Consulting with a qualified intermediary or tax professional with expertise in 1031 exchanges can provide invaluable guidance and assistance in properly determining the value of the property and navigating the complexities of the exchange process.

Reporting the Gain or Loss from the 1031 Exchange

Reporting the gain or loss from a 1031 exchange is a critical step in accurately reflecting the financial impact of the transaction on your tax return. By properly reporting the gain or loss, you ensure compliance with IRS regulations and maximize the tax benefits of the exchange. Let’s explore the key considerations when reporting the gain or loss from a 1031 exchange.

The gain or loss from a 1031 exchange is determined by comparing the adjusted basis of the relinquished property with the fair market value of the replacement property. The adjusted basis includes the original purchase price of the property plus any improvements made, minus any depreciation claimed. The fair market value of the replacement property is typically based on an appraisal or other similar valuation method.

If the fair market value of the replacement property is greater than the adjusted basis of the relinquished property, there is a potential taxable gain. Conversely, if the fair market value is lower than the adjusted basis, there may be a loss. However, it’s important to note that the gain or loss is not recognized or realized at the time of the exchange since a 1031 exchange allows for tax deferral.

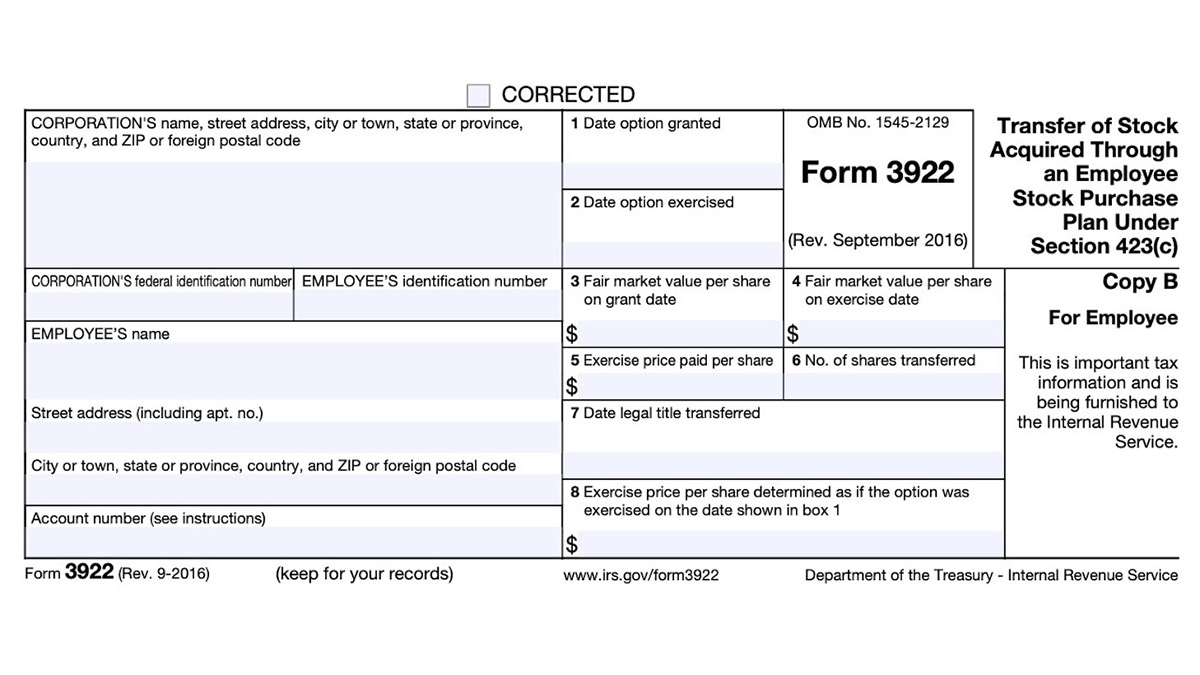

To report the gain or loss from the exchange, you will need to fill out Form 8824, Like-Kind Exchanges, and attach it to your tax return for the year in which the exchange took place. Form 8824 requires detailed information about the relinquished property, replacement property, and the financial aspects of the exchange.

On the form, you will report the adjusted basis of the relinquished property, the fair market value of the replacement property, and any cash or boot received or paid in the exchange. The form also requires you to calculate the realized gain or loss, which is the difference between the adjusted basis and the fair market value.

It’s important to note that any boot received or paid, such as cash or non-like-kind property, may be subject to capital gains taxes in the year of the exchange. This should be reported separately on your tax return as it is not eligible for tax deferral under Section 1031.

Reporting the gain or loss from a 1031 exchange accurately is crucial to avoid underreporting or overreporting your tax liability. It is recommended to consult with a tax professional or qualified intermediary with expertise in 1031 exchanges to ensure proper reporting and maximize the tax benefits of the exchange.

Remember that the purpose of a 1031 exchange is to defer the capital gains taxes, not eliminate them. Properly reporting the exchange on your tax return ensures compliance with IRS regulations and allows you to navigate the complexities of tax deferral while maximizing the benefits of this powerful tax strategy.

Step-by-Step Guide to Reporting a 1031 Exchange on Your Tax Return

Reporting a 1031 exchange on your tax return may seem daunting, but with a step-by-step guide, you can navigate the process with ease. Following these steps will help ensure accurate reporting and maximize the tax benefits of your exchange.

Step 1: Gather all necessary documentation: Collect all relevant documentation related to your 1031 exchange, including copies of the purchase and sale agreements, settlement statements, appraisals, and any other financial records.

Step 2: Complete Form 8824: Fill out Form 8824, Like-Kind Exchanges, which is used to report the exchange to the IRS. Provide detailed information about the relinquished property, including the adjusted basis and fair market value, as well as information about the replacement property.

Step 3: Calculate the realized gain or loss: Use the information from your documentation to determine the realized gain or loss from the exchange. This is the difference between the adjusted basis of the relinquished property and the fair market value of the replacement property.

Step 4: Report the gain or loss on your tax return: Transfer the information from Form 8824 to the appropriate sections of your tax return. Typically, this will be Schedule D for capital gains and losses, but consult your tax professional or the instructions for your specific tax form.

Step 5: Report any boot received or paid: If you received or paid any cash or non-like-kind property, report this separate from the 1031 exchange on your tax return. These transactions may be subject to capital gains taxes in the year of the exchange.

Step 6: Consult with a tax professional: It’s highly recommended to seek the guidance of a tax professional or qualified intermediary experienced in 1031 exchanges. They can review your documentation, provide advice on reporting, and ensure compliance with IRS guidelines.

Step 7: Retain records for future reference: Keep copies of all documentation related to the 1031 exchange for at least three years, as the IRS may request this information in the event of an audit. This includes the Form 8824, settlement statements, appraisals, and any other relevant financial records.

Following these steps will help you properly report your 1031 exchange on your tax return and maximize the tax benefits of this powerful tax-deferral strategy. Remember to consult with a tax professional to ensure accuracy and comply with all IRS regulations.

Reporting the Exchange on Form 8824

When participating in a 1031 exchange, it is essential to accurately report the exchange to the IRS. Form 8824, Like-Kind Exchanges, is the designated form for reporting a 1031 exchange. This form captures the necessary information about the relinquished property, the replacement property, and the financial aspects of the exchange. Let’s explore how to report the exchange on Form 8824.

Section 1: Begin by providing your personal information, including your name, social security number, and tax year for which the exchange took place.

Section 2: In this section, you will provide details about the relinquished property, such as the description, date acquired, and date sold. You’ll also include the adjusted basis, which is the original purchase price plus any improvements, minus depreciation claimed.

Section 3: Input the fair market value of the relinquished property and any liabilities assumed by the buyer, as well as any cash received or paid in the exchange, also known as “boot.”

Section 4: Here, you will identify the replacement property or properties. Include the description and date acquired, as well as the fair market value of each property and any liabilities transferred to the replacement property.

Section 5: Calculate the realized gain or loss by subtracting the adjusted basis of the relinquished property from the total fair market value of the replacement property.

Section 6: Determine the recognized gain or loss. If there is boot received, you may have a recognized gain to the extent of the boot received. If there is boot paid, you may have a recognized loss to the extent of the boot paid.

Section 7: Finally, summarize the gain or loss from the exchange and transfer this information to your tax return. Report the recognized gain or loss on the appropriate forms, such as Schedule D for capital gains and losses. Follow the specific instructions for your tax form to ensure proper reporting.

It’s crucial to accurately complete Form 8824 and attach it to your tax return for the year in which the 1031 exchange took place. Ensure that all information provided is correct and supported by appropriate documentation, such as purchase and sale agreements, appraisals, and settlement statements.

Remember to keep copies of Form 8824 and all supporting documentation for at least three years, as the IRS may request these records in case of an audit. Properly reported exchanges not only ensure compliance with IRS regulations but also maximize the tax benefits of participating in a 1031 exchange.

If you have any doubts or concerns about reporting the exchange on Form 8824, it is advisable to consult with a qualified tax professional or a knowledgeable intermediary. Their expertise will help ensure accurate reporting and compliance with IRS guidelines.

Filing Deadlines and Extensions for Reporting a 1031 Exchange

When it comes to reporting a 1031 exchange on your tax return, it’s important to be aware of the filing deadlines and the potential for extensions. Adhering to these deadlines ensures compliance with the Internal Revenue Service (IRS) regulations and avoids any penalties or interest charges. Let’s explore the important filing deadlines and the possibility of extensions for reporting a 1031 exchange.

Original Filing Deadline: The original due date for filing your tax return, including reporting the 1031 exchange, is typically April 15th of the year following the tax year in which the exchange occurred. However, if the original due date falls on a weekend or a holiday, the deadline is extended to the next business day.

Extensions: If you need additional time to gather the necessary information or seek professional advice, you can request an extension by filing Form 4868, Application for Automatic Extension of Time to File U.S. Individual Income Tax Return. This form grants an automatic extension of six months, moving the filing deadline to October 15th.

It’s important to note that an extension grants additional time to file your tax return but does not extend the deadline to pay any taxes owed. If you anticipate owing taxes from the 1031 exchange, it’s advisable to estimate the amount and make a payment by the original filing deadline to avoid potential penalties and interest charges.

Form 8824: Reporting the 1031 exchange on your tax return requires completing Form 8824, Like-Kind Exchanges. This form must be filed with your tax return by the applicable filing deadline, either the original deadline or the extended deadline if an extension was requested.

It’s important to gather all the necessary documentation and information related to the exchange well in advance of the filing deadline. This includes copies of purchase and sale agreements, settlement statements, appraisals, and any other financial records related to the exchange. Organizing your paperwork early on will help streamline the reporting process and ensure accuracy.

If you find that you cannot meet the filing deadline, it is imperative to request an extension using Form 4868 to avoid late-filing penalties. Failing to file a tax return or an extension request by the deadline could result in penalties and interest charges on any taxes owed.

While requesting an extension provides additional time to file your tax return, it is essential to remember that any taxes owed are still due by the original filing deadline. Promptly estimating and paying any taxes owed will help avoid potential penalties and interest charges.

Ultimately, being aware of the filing deadlines and the option for extensions provides flexibility and allows you to accurately report your 1031 exchange while maintaining compliance with IRS regulations.

If you have any concerns or questions regarding the deadlines or extensions for reporting a 1031 exchange, it’s advisable to consult with a tax professional or qualified intermediary who can provide guidance based on your specific circumstances.

Common Mistakes to Avoid When Reporting a 1031 Exchange

Reporting a 1031 exchange on your tax return can be a complex process, and it’s important to avoid common mistakes that could lead to errors or potential audits by the Internal Revenue Service (IRS). By being aware of these mistakes, you can ensure accurate reporting and maximize the tax benefits of your exchange. Let’s explore some common mistakes to avoid when reporting a 1031 exchange.

Incomplete or Inaccurate Documentation: One of the most common mistakes is failing to maintain or provide complete and accurate documentation related to the exchange. It’s crucial to keep copies of purchase and sale agreements, settlement statements, appraisals, and any other financial records. These documents are vital for properly reporting the exchange and may be requested by the IRS in case of an audit.

Missing Filing Deadlines: Failing to file Form 8824, Like-Kind Exchanges, by the appropriate deadline can result in penalties and interest charges. Stay updated on the filing deadlines and consider requesting an extension if needed. Be aware that while an extension grants additional time to file, it does not extend the deadline to pay any taxes owed. Paying estimated taxes by the original filing deadline can help avoid penalties and interest charges.

Failure to Identify Replacement Properties Correctly: When identifying potential replacement properties within the 45-day timeframe, it’s crucial to follow the IRS guidelines. Ensure that you properly identify the replacement properties in writing and deliver the identification to the qualified intermediary or other relevant parties involved. Failing to meet the identification requirements could jeopardize the eligibility of your 1031 exchange.

Inaccurate Reporting of Boot: Boot refers to cash or non-like-kind property received or paid as part of the exchange. Any boot received or paid must be reported separately on your tax return and may result in taxable gain or loss. It’s essential to accurately report boot transactions and consult with a tax professional to ensure compliance with IRS guidelines.

Not Consulting a Tax Professional: The intricacies of reporting a 1031 exchange can be challenging to navigate. Engaging the expertise of a tax professional or qualified intermediary can help you avoid common mistakes and ensure accurate reporting. They can provide guidance, review your documentation, and offer valuable advice tailored to your specific situation.

Failure to Understand the Rules and Guidelines: It’s crucial to have a solid understanding of the rules and guidelines associated with a 1031 exchange. Familiarize yourself with the requirements for like-kind properties, the timelines for identification and acquisition, and the specific reporting rules. This knowledge will help you comply with IRS regulations and maximize the tax benefits of your exchange.

Avoiding these common mistakes will help ensure accurate reporting and compliance with IRS regulations. Properly reporting your 1031 exchange not only mitigates the risk of audits and penalties but also allows you to fully benefit from the tax deferral advantages of this powerful tax strategy.

If you have any concerns or questions regarding the reporting of a 1031 exchange, it’s advisable to consult with a tax professional or qualified intermediary who can provide guidance tailored to your specific circumstances.

Seeking Professional Assistance for Reporting a 1031 Exchange

Reporting a 1031 exchange on your tax return can be a complex process, and seeking professional assistance can greatly benefit you in navigating the intricacies of this tax strategy. Consulting with a tax professional or qualified intermediary can provide valuable guidance and ensure accurate reporting. Here are some reasons why seeking professional assistance is beneficial when reporting a 1031 exchange.

Expertise and Knowledge: Tax professionals and qualified intermediaries have specialized knowledge and expertise in 1031 exchanges. They are well-versed in IRS regulations, reporting requirements, and the intricacies of the exchange process. Their in-depth understanding of the tax code enables them to provide accurate guidance and ensure compliance with the rules and guidelines.

Proper Documentation and Reporting: Professionals can assist you in gathering and organizing all the necessary documentation required for reporting the 1031 exchange. They can help you navigate complex paperwork, ensure accurate reporting of financial transactions, and provide guidance on properly completing Form 8824, Like-Kind Exchanges.

Tax Planning and Strategy: Professionals can assist you in maximizing the tax benefits of your exchange by developing appropriate tax planning strategies. They can help you evaluate potential replacement properties, assess tax implications, and strategize to minimize taxable gains. This can help you make informed decisions that align with your overall financial goals.

Compliance and Risk Mitigation: Properly reporting a 1031 exchange is crucial to comply with IRS regulations and mitigate the risk of audits or penalties. Professionals ensure that all reporting requirements are met, reducing the likelihood of errors or omissions on your tax return. They can also keep you informed about any changes in tax laws or regulations that may affect your exchange.

Guidance and Support: Professionals provide personalized guidance tailored to your specific situation. They can answer your questions, address your concerns, and offer support throughout the entire exchange process. Whether it’s determining the eligibility of properties, understanding the timelines, or assessing the tax implications, their expertise can give you peace of mind.

Audit Protection: In the event of an IRS audit, having professional assistance can be invaluable. They can serve as your advocate, helping to navigate the audit process and providing the necessary documentation and support to address any potential issues. Their expertise can help protect your interests and ensure a smoother audit experience.

Given the complexity and potential tax consequences involved in a 1031 exchange, seeking professional assistance is highly advisable. A qualified tax professional or qualified intermediary can guide you through the process, ensuring accurate reporting, compliance with IRS regulations, and maximizing the tax benefits of your exchange.

Remember to choose a reputable professional with experience in 1031 exchanges. Seek referrals, review their credentials, and consider their expertise in real estate transactions and tax law. By entrusting your 1031 exchange reporting to a professional, you can navigate the process with confidence and peace of mind.

Conclusion

Reporting a 1031 exchange on your tax return is a crucial step to ensure compliance with IRS regulations and maximize the tax benefits of this powerful tax-deferral strategy. By understanding the basics of a 1031 exchange, eligibility requirements, and the process of reporting the exchange, you can navigate the complexities with confidence.

Remember to accurately determine the value of the exchanged property by considering factors such as the adjusted basis, fair market value, and any cash or debt involved. Properly reporting the gain or loss from the exchange on Form 8824 ensures accurate reflection of the financial impact on your tax return.

Avoid common mistakes, such as incomplete or inaccurate documentation, missing filing deadlines, and improper identification of replacement properties. Seeking professional assistance from a tax professional or qualified intermediary can provide invaluable expertise, guidance, and support throughout the reporting process.

Always be mindful of the filing deadlines and the possibility of requesting extensions when needed. Adhering to these deadlines and accurately reporting the exchange not only ensures compliance with IRS regulations but also maximizes the tax benefits of your 1031 exchange.

A 1031 exchange can be a powerful tool for real estate investors to grow their portfolio while deferring capital gains taxes. By adhering to the reporting requirements, you can fully benefit from the tax deferral advantages and continue building wealth in the real estate market.

Remember, every individual’s tax situation is unique, and it is essential to consult with a tax professional or qualified intermediary to address your specific needs and circumstances. With their guidance, you can navigate the reporting process smoothly while optimizing the financial advantages of participating in a 1031 exchange.

In conclusion, reporting a 1031 exchange on your tax return requires attention to detail, accurate documentation, and proper reporting. By following the guidelines outlined in this article and seeking professional assistance when needed, you can confidently report your 1031 exchange and maximize the tax benefits while staying in compliance with IRS regulations.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance