Finance

How Aggressive Should My 401K Be

Published: October 18, 2023

Learn how to optimize your 401K investments and determine the right level of aggressiveness for maximum returns. Improve your financial planning with expert advice in finance.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding Risk and Reward in 401K Investments

- Determining Your Risk Tolerance

- Factors to Consider in Deciding How Aggressive to Be

- Conservative 401K Investment Strategies

- Moderately Aggressive 401K Investment Strategies

- Highly Aggressive 401K Investment Strategies

- Balancing Risk and Reward in Your 401K

- Conclusion

Introduction

When it comes to managing your 401K, one of the key decisions you need to make is how aggressive you want to be in your investments. Your level of aggressiveness will determine the potential risk and reward of your portfolio. But how do you determine the right balance?

In this article, we will dive into the factors that can help you decide how aggressive to be with your 401K investments. We will explore different investment strategies and risk levels, and provide insights that will assist you in making an informed decision.

It’s important to note that there is no one-size-fits-all answer to this question. Your optimal level of aggression will depend on various factors such as your financial goals, time horizon, risk tolerance, and overall investment strategy.

So, whether you’re a conservative investor looking for lower risk options, or a more daring investor seeking higher returns, this article will guide you through the decision-making process and help you determine the appropriate level of aggressiveness for your 401K investments.

Understanding Risk and Reward in 401K Investments

Before delving into the different levels of aggressiveness in 401K investments, let’s first understand the concept of risk and reward. In the world of investing, risk refers to the possibility of losing money or experiencing a decline in the value of your investments. On the other hand, reward refers to the potential for earning higher returns.

When it comes to 401K investments, there is a direct correlation between risk and reward. Generally, higher risk investments have the potential for higher returns, while lower risk investments are associated with lower potential returns. This means that the level of aggressiveness you choose for your 401K will ultimately determine the trade-off between risk and potential reward.

It’s important to note that risk and reward are not solely determined by the aggressiveness of your investments. Other factors, such as the performance of the market, economic conditions, and individual company performance, also play a significant role. However, the level of aggressiveness in your investment strategy will have a direct impact on the amount of risk you expose yourself to and the potential reward you can expect.

Conservative investment strategies typically focus on preserving capital and avoiding significant losses. These strategies may involve investing in more stable and low-risk assets, such as bonds or money market funds. While these investments provide lower potential returns, they also carry a lower risk.

On the other end of the spectrum, aggressive investment strategies aim for higher returns by taking on more risk. These strategies often involve investing in growth-oriented assets, such as stocks or equity funds. While they offer the potential for higher returns, they also come with a greater risk of volatility and potential losses.

The key to finding the right balance between risk and reward lies in understanding your risk tolerance and aligning it with your financial goals. By evaluating your comfort level with risk and considering your investment objectives, you can determine the appropriate level of aggressiveness for your 401K investments.

Determining Your Risk Tolerance

Understanding your risk tolerance is crucial when determining the appropriate level of aggressiveness for your 401K investments. Risk tolerance refers to your ability and willingness to withstand fluctuations in the value of your investments. It reflects your comfort level with taking on risk and the impact that potential losses may have on your financial well-being.

Assessing your risk tolerance involves considering various factors, including your investment goals, time horizon, financial situation, and personal preferences. Here are some key points to consider:

Investment Goals: Clearly define your investment goals. Are you saving for retirement, a down payment on a house, or a child’s education? The specific objectives you have will influence the level of risk you are willing to take on.

Time Horizon: Consider the length of time before you will need to access your funds. Longer time horizons generally allow for more aggressive investment strategies as they can better withstand short-term volatility.

Financial Situation: Evaluate your current financial situation and your ability to bear potential losses. Consider your income, expenses, debt levels, and emergency savings. A stable financial situation may provide you with more flexibility to tolerate higher-risk investments.

Personal Preferences: Reflect on your personal attitude towards risk. Are you comfortable with the ups and downs of the market, or do you prefer more stable investments? Understanding your own psychological response to risk is crucial.

Once you have considered these factors, you can determine your risk tolerance profile. Common risk tolerance categories include conservative, moderate, and aggressive. A conservative investor has a lower risk tolerance and prefers more stable investments, while an aggressive investor is comfortable with higher levels of risk and potential volatility.

It’s important to note that risk tolerance is subjective and can change over time. Factors such as market conditions, life events, and changes in personal circumstances can impact your risk tolerance. Regularly reassessing your risk tolerance is essential to ensure that your investment strategy aligns with your current financial situation and goals.

By having a clear understanding of your risk tolerance, you can better assess the appropriate level of aggressiveness for your 401K investments. Remember, it’s crucial to strike a balance between maximizing potential returns and managing risk to achieve your long-term financial objectives.

Factors to Consider in Deciding How Aggressive to Be

When determining how aggressive to be with your 401K investments, it’s important to consider various factors that can influence your decision-making process. Here are some key factors to keep in mind:

Financial Goals: Consider your financial goals and the timeframe in which you aim to achieve them. If you have long-term goals, such as retirement that is several decades away, you may have the flexibility to take on more aggressive investments. Short-term goals, on the other hand, may call for a more conservative approach to minimize potential losses.

Time Horizon: Evaluate your time horizon, which refers to the length of time you have until you need to access your funds. A longer time horizon allows for more fluctuations and potential recovery from market downturns. This may give you the opportunity to consider more aggressive investments with higher growth potential.

Risk Tolerance: Assess your risk tolerance, as it plays a significant role in determining the level of aggressiveness in your investments. If you feel comfortable with volatility and are willing to accept potential losses, you may opt for a more aggressive investment approach. If you prefer stability and a lower risk of loss, a conservative strategy may be more appropriate.

Investment Knowledge: Evaluate your level of investment knowledge and understanding. Aggressive investments often require a deeper understanding of the market and the ability to analyze risk factors. If you are confident in your investment knowledge and have the capacity to conduct thorough research, you may be inclined to pursue more aggressive options.

Diversification: Consider the level of diversification in your investment portfolio. Diversification helps spread the risk across different asset classes, reducing the impact of any single investment’s performance. If you have a well-diversified portfolio, you may be more comfortable taking on higher levels of risk in some areas, as the overall risk is mitigated.

Market Conditions: Take into account the current state of the market and economic conditions. Aggressive investments may perform well during bullish markets but can experience significant downturns during bearish periods. It’s vital to assess how market conditions align with your risk tolerance and financial goals.

Asset Allocation Strategy: Evaluate your asset allocation strategy, which refers to the distribution of your investments across different asset classes. A more aggressive allocation may involve a higher percentage of equity or growth-oriented investments, while a conservative allocation may lean towards fixed income or stable investments.

By considering these factors, you can make a more informed decision on how aggressive you want to be with your 401K investments. It’s crucial to find a balance between risk and potential reward that aligns with your financial goals, risk tolerance, and overall investment strategy. Regularly reassessing these factors as your circumstances change will help ensure your investment approach remains aligned with your objectives.

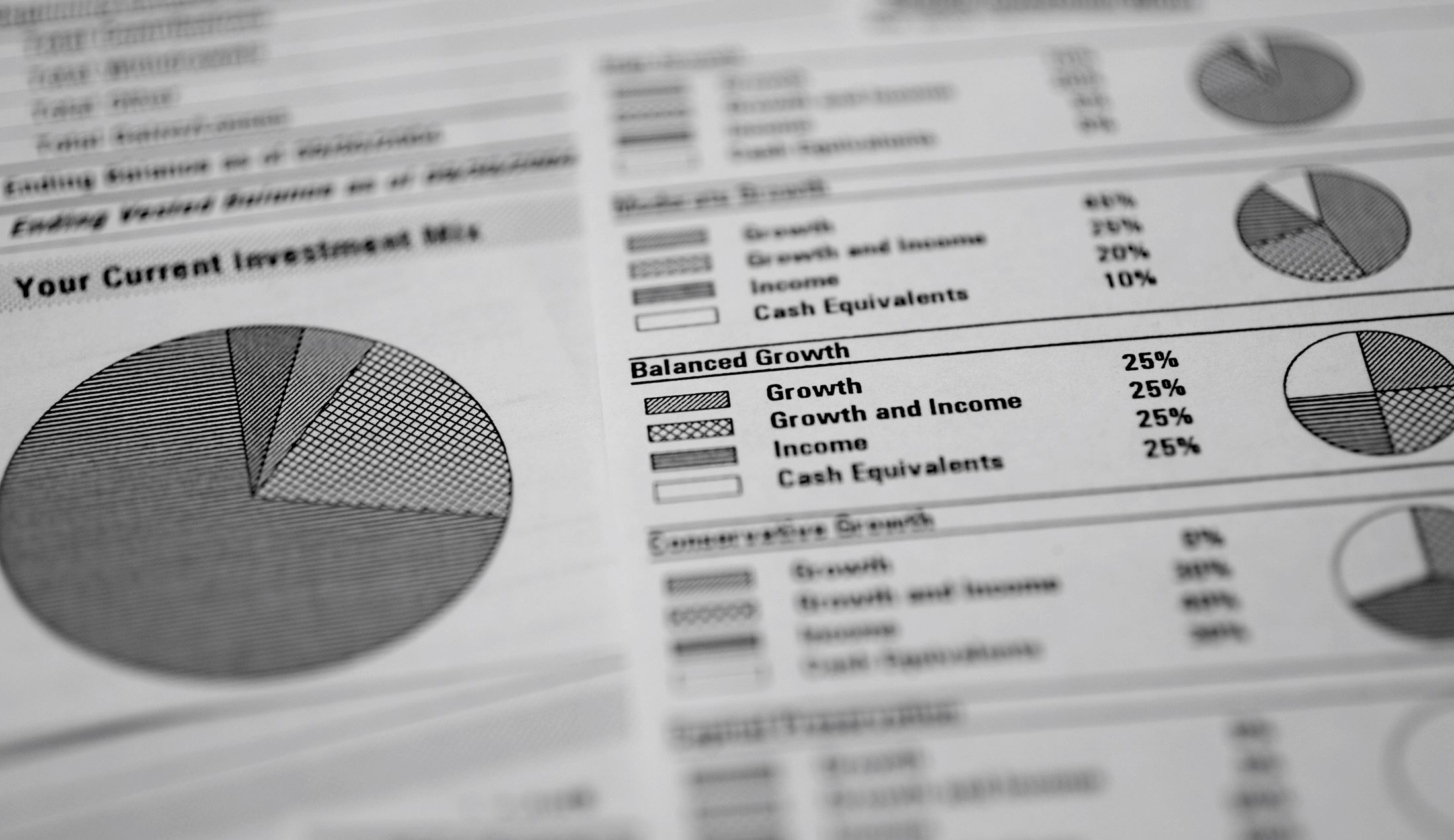

Conservative 401K Investment Strategies

For investors with a conservative risk tolerance, there are several strategies to consider when managing their 401K investments. These strategies aim to prioritize capital preservation and provide a stable and predictable return. Here are some conservative 401K investment strategies to explore:

Bond Funds: Investing in bond funds can be a conservative approach for 401K investors. Bond funds pool investors’ money to purchase a diversified portfolio of fixed-income securities, such as government bonds or corporate bonds. These investments typically provide regular interest payments and are less volatile compared to stocks, making them suitable for conservative investors seeking income and stability.

Target-Date Funds: Target-date funds are widely popular among conservative investors. These funds automatically adjust their asset allocation based on the investor’s projected retirement date. As retirement approaches, the fund gradually shifts from growth-oriented assets, such as stocks, to more stable investments like bonds. Target-date funds provide a hands-off approach for those who prefer a set-it-and-forget-it strategy aligned with their risk tolerance and retirement timeline.

Index Funds: Index funds are passively managed funds that aim to replicate the performance of a specific market index, such as the S&P 500. These funds provide broad market exposure at a low cost and are designed to match the returns of the overall market. Index funds offer diversification and are suitable for conservative investors who prefer a simple and low-risk investment approach.

Stable Value Funds: Stable value funds are a conservative option within 401K plans that focus on capital preservation and consistent returns. These funds primarily invest in fixed-income securities, such as government bonds and high-quality corporate bonds, with an emphasis on principal protection. Stable value funds offer steady returns and are ideal for risk-averse investors seeking minimal volatility.

Dividend-Paying Stocks: Another conservative strategy for 401K investors is to invest in dividend-paying stocks. Dividend stocks are shares of companies that distribute a portion of their profits to shareholders on a regular basis. These stocks often belong to established companies with a history of stable earnings and dividends. Investing in dividend-paying stocks can provide investors with regular income and potential capital appreciation, while still offering a conservative approach.

It’s important to note that conservative investment strategies may limit the potential for significant growth and higher returns. However, they provide stability and a lower risk of loss. Conservative investors prioritize the preservation of capital and are typically more concerned with avoiding substantial downturns in their portfolios.

Remember, while conservative strategies help protect your investments, it’s essential to regularly review and reassess your 401K portfolio to ensure it aligns with your long-term financial goals and risk tolerance.

Moderately Aggressive 401K Investment Strategies

For investors with a moderately aggressive risk tolerance, there are several strategies to consider when managing their 401K investments. These strategies aim to strike a balance between growth potential and risk management. Here are some moderately aggressive 401K investment strategies to explore:

Asset Allocation Funds: Asset allocation funds are diversified portfolios that automatically adjust the allocation of assets based on market conditions. These funds invest in a mix of stocks, bonds, and other asset classes to balance growth potential and risk. Asset allocation funds can be a suitable option for moderately aggressive investors looking for a diversified approach without the need for constant monitoring and rebalancing.

Equity Index Funds: Equity index funds are passively managed funds that aim to track the performance of a specific stock market index, such as the S&P 500. These funds provide exposure to a broad range of stocks and offer the potential for long-term growth. Equity index funds are suitable for investors seeking moderate growth potential while maintaining a lower level of risk compared to actively managed funds.

Growth Stock Funds: Growth stock funds invest in companies with a high potential for growth. These funds primarily focus on stocks of companies that are expected to experience above-average earnings growth. While they carry a higher level of risk compared to other investment options, growth stock funds can provide attractive returns for moderately aggressive investors with a longer time horizon.

Blue-Chip Stocks: Blue-chip stocks refer to shares of large, well-established companies with a history of stable earnings and dividends. These stocks are generally considered less risky than smaller, less established companies. Investing in blue-chip stocks can offer both income and potential capital appreciation, making them an appealing option for moderately aggressive investors seeking a balance between stability and growth.

REITs: Real Estate Investment Trusts (REITs) are investment vehicles that own and operate income-generating real estate properties. REITs can provide a way to diversify a 401K portfolio by adding exposure to the real estate sector. Moderate-risk investors may consider allocating a portion of their 401K to REITs to capture potential returns from the real estate market.

When employing moderately aggressive strategies, it’s crucial to monitor your investments regularly and stay informed about market conditions. Periodic rebalancing may be necessary to ensure that your portfolio maintains the desired risk profile and alignment with your financial goals.

Remember, moderately aggressive strategies involve a higher level of risk compared to conservative approaches. It’s important to assess your risk tolerance, time horizon, and financial goals before implementing these strategies to ensure they align with your investment objectives.

Highly Aggressive 401K Investment Strategies

For investors with a highly aggressive risk tolerance, there are several strategies to consider when managing their 401K investments. These strategies prioritize growth potential over capital preservation and involve higher levels of risk. Here are some highly aggressive 401K investment strategies to explore:

Small-Cap Growth Stocks: Small-cap growth stocks are shares of smaller companies that have the potential for rapid growth. These companies are often in the early stages of development and can be more volatile than larger, established companies. Investing in small-cap growth stocks can offer the potential for significant returns, but it comes with higher risks due to the inherent volatility of these stocks.

Sector-specific Funds: Sector-specific funds focus on a particular industry or sector, such as technology, healthcare, or energy. These funds provide exposure to companies within a specific sector, allowing investors to concentrate their investments based on their beliefs and research. Investing in sector-specific funds can offer the potential for higher returns but carries more significant risks as the fund’s performance is closely tied to the performance of a specific industry.

International and Emerging Market Funds: International and emerging market funds invest in companies based outside of the domestic market, offering exposure to global economic growth. Investing in international and emerging market funds can provide diversification and the potential for higher returns, but it comes with increased risks due to currency fluctuations, political instability, and differing market regulations.

Individual Stocks: Highly aggressive investors may choose to invest in individual stocks, handpicking specific companies they believe will outperform the market. This strategy requires a high level of research, analysis, and monitoring of individual companies. While individual stock investing can offer substantial returns, it is also associated with a higher level of risk and requires careful consideration and due diligence.

Leveraged Funds: Leveraged funds aim to amplify the returns of an underlying index or asset class through the use of financial derivatives and borrowing. These funds can magnify gains during favorable market conditions but also increase losses during downturns. Highly aggressive investors may consider leveraging their investments to potentially achieve higher returns, but it’s important to note that leverage also increases the risk of significant losses.

Highly aggressive strategies involve a higher level of risk and volatility. These strategies are suitable for investors who have a long-term horizon and the ability to withstand significant fluctuations in portfolio value. It’s crucial to regularly monitor and review highly aggressive investments to ensure they remain aligned with your risk tolerance and long-term financial goals.

Although highly aggressive strategies carry potential for high returns, they are not suitable for everyone. It’s important to carefully assess your risk tolerance, financial goals, and investment knowledge before implementing highly aggressive 401K investment strategies.

Balancing Risk and Reward in Your 401K

One of the most important aspects of managing your 401K is finding the right balance between risk and reward. Balancing these two factors is essential for optimizing your investment returns while ensuring you can handle potential downturns. Here are some strategies to help you find the right balance in your 401K:

Diversification: Diversifying your portfolio is key to reducing risk. Allocate your investments across a mix of asset classes, such as stocks, bonds, and cash equivalents. Diversification helps mitigate the impact of any single investment’s performance and allows you to take advantage of different market conditions. Regularly review and rebalance your 401K portfolio to ensure it remains diversified in line with your risk tolerance and investment goals.

Asset Allocation: Determining the appropriate allocation of assets in your portfolio is crucial. Generally, younger investors with a longer time horizon can afford to take on more aggressive investments as they have more time to potentially recover from any short-term losses. On the other hand, investors nearing retirement may opt for a more conservative allocation to protect their savings. Consider your risk tolerance, time horizon, and financial goals when determining your asset allocation strategy.

Regular Monitoring: Regularly monitor your 401K investments to assess performance and make adjustments as needed. Stay informed about market trends, economic conditions, and any changes that may impact your investment strategy. It’s also essential to periodically review your risk tolerance and ensure that your investments align with your comfort level.

Consider Professional Advice: If you find it challenging to strike the right balance between risk and reward in your 401K, consider seeking professional advice from a financial advisor. They can help you assess your risk tolerance, evaluate your investment goals, and develop a customized investment strategy that aligns with your needs.

Stay Disciplined: Emotions can influence investment decisions, leading to irrational behavior such as buying high during market peaks or selling low during downturns. It’s crucial to stay disciplined and avoid making impulsive decisions based on short-term market fluctuations. Maintain a long-term perspective and stick to your investment plan.

Review Your Plan’s Investment Options: Familiarize yourself with the investment options available in your 401K plan. Understand the investment objectives, risk levels, and performance history of each option. This knowledge will allow you to make informed decisions and select investments that align with your risk tolerance and financial goals.

Remember, finding the right balance between risk and reward is a highly individualized process. It requires considering your risk tolerance, investment horizon, and financial goals. Regularly reassess and adjust your investment strategy as your circumstances change to ensure that your 401K portfolio remains balanced and aligned with your long-term objectives.

Conclusion

Deciding how aggressive to be with your 401K investments is a key consideration for maximizing returns while managing risk. Understanding your risk tolerance, financial goals, and time horizon is essential in determining the appropriate level of aggressiveness for your portfolio.

Conservative strategies focus on capital preservation and stability, with options such as bond funds, target-date funds, and stable value funds. Moderately aggressive strategies strike a balance between growth potential and risk, incorporating asset allocation funds, equity index funds, and dividend-paying stocks. Highly aggressive strategies prioritize growth potential and involve strategies like small-cap growth stocks, sector-specific funds, and individual stocks.

Regardless of your risk tolerance, it’s important to diversify your portfolio, regularly review your investments, and align your asset allocation strategy with your financial goals. Balancing risk and reward in your 401K requires ongoing monitoring, periodic adjustments, and staying disciplined in your investment decisions.

Remember, your risk tolerance and investment strategy may evolve over time. Life events, economic conditions, and market trends can impact your decision-making process. Regularly reassess your risk tolerance and investment strategy to ensure that your 401K aligns with your changing circumstances and long-term objectives.

In conclusion, finding the right balance between risk and reward in your 401K is a personal journey. Take the time to evaluate your risk tolerance, financial goals, and time horizon. Seek professional advice when needed, and stay disciplined in your investment approach. By striking the right balance, you can optimize your 401K portfolio and work toward achieving your long-term financial aspirations.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance