Home>Finance>Inherent Risk: Definition, Examples, And 3 Types Of Audit Risks

Finance

Inherent Risk: Definition, Examples, And 3 Types Of Audit Risks

Published: December 9, 2023

Explore the definition of inherent risk in finance, along with real-life examples and the three main types of audit risks. Enhance your financial knowledge today.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Understanding Inherent Risk: Definition, Examples, and 3 Types of Audit Risks

If you work in the field of auditing or have a keen interest in financial risk management, you have likely come across the term “inherent risk.” But what exactly is inherent risk and why is it important? In this article, we will delve into the definition of inherent risk, provide examples of its presence in different industries, and explore three types of audit risks associated with it.

Key Takeaways:

- Inherent risk refers to the level of risk that exists in an organization’s financial statements before any control measures are implemented.

- Inherent risk can vary across different industries and organizations, with factors such as market conditions, regulatory requirements, and company policies influencing its magnitude.

What is Inherent Risk?

Inherent risk, in the context of auditing, is the level of risk that exists in an organization’s financial statements before any control measures are implemented. It represents the susceptibility of financial statements to material misstatements due to factors such as errors, fraud, or non-compliance with accounting standards.

It’s important to understand that inherent risk is an inherent characteristic of financial statements and exists regardless of the effectiveness of an organization’s internal controls. It is a concept that auditors consider when designing their audit procedures to ensure that they are addressing the highest areas of potential risk.

Now, let’s explore some examples of inherent risk in different industries to better illustrate its practical application.

Examples of Inherent Risk

Inherent risk can vary across industries and organizations due to several factors. Let’s look at a few examples to gain a better understanding:

- 1. Pharmaceuticals: The pharmaceutical industry involves extensive research and development activities, which often leads to complex financial reporting. In this industry, inherent risk might arise from factors such as the estimation of clinical trial costs, valuation of intangible assets, and compliance with stringent regulatory requirements.

- 2. Manufacturing: Inherent risk in the manufacturing industry might be related to areas such as inventory valuation, equipment obsolescence, and compliance with quality control standards.

- 3. Financial Services: In the financial services industry, inherent risk can stem from factors such as the complexity of financial instruments, compliance with anti-money laundering regulations, and the accuracy of financial disclosures.

These examples highlight how inherent risk can manifest differently in various industries, depending on the nature of their operations, market conditions, and regulatory frameworks.

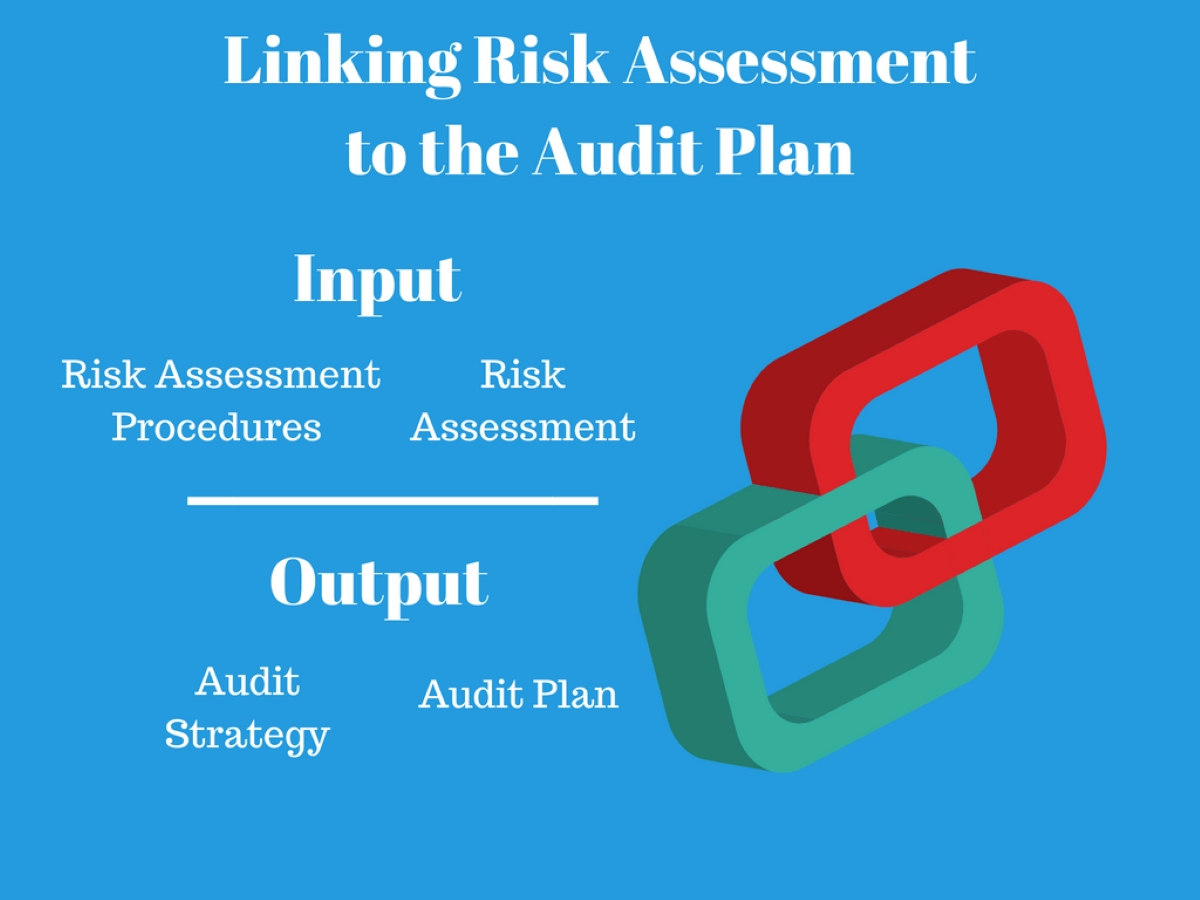

Types of Audit Risks Associated with Inherent Risk

When conducting an audit, auditors must consider three types of audit risks associated with inherent risk:

- Inherent risk: As mentioned earlier, inherent risk refers to the level of risk present in an organization’s financial statements before control measures are implemented. It represents the susceptibility to material misstatements.

- Control risk: Control risk refers to the risk that a material misstatement may not be prevented or detected and corrected by an organization’s internal controls. Auditors assess control risk to determine the extent to which they can rely on internal controls in their audit procedures.

- Detection risk: Detection risk represents the risk that auditors may not detect a material misstatement in the financial statements. Auditors consider detection risk when determining the nature, timing, and extent of their audit procedures.

By understanding these three types of audit risks associated with inherent risk, auditors can effectively plan their audit procedures, allocate resources, and prioritize their focus areas to mitigate the risks involved.

Conclusion

Inherent risk is an essential concept in auditing and financial risk management. It represents the level of risk present in an organization’s financial statements before any control measures are implemented. By understanding and assessing inherent risk, auditors can design their audit procedures to ensure that they address the highest areas of potential risk effectively.

Remember, inherent risk can vary across industries and organizations due to factors such as market conditions, regulatory requirements, and company policies. By considering the three types of audit risks associated with inherent risk – inherent risk, control risk, and detection risk – auditors can conduct thorough audits that provide valuable insights into an organization’s financial health and risk profile.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance