Finance

What Does Credit Spread Mean

Modified: January 15, 2024

Learn the definition of credit spread in finance and how it impacts your financial decisions. Understand the concept of credit spread and its significance in the world of finance.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to our comprehensive guide on credit spreads. Whether you are new to the world of finance or have some experience in the industry, understanding credit spreads is vital for making informed investment decisions. In this article, we will explore the concept of credit spreads, their significance, and the various factors that affect them.

A credit spread is a financial metric used to assess the creditworthiness of a borrower. It represents the difference in yields between two debt instruments with similar maturities but different credit ratings. Typically, the higher the credit spread, the higher the perceived risk of default by the borrower.

Credit spreads play a crucial role in fixed income investing. They provide insight into market sentiment regarding credit risk and act as a valuable tool for investors to evaluate the potential return and risk associated with an investment. By analyzing credit spreads, investors can make more informed decisions about the bonds they choose to invest in.

Understanding credit spreads requires an understanding of the components that make them up. These components include the risk-free rate, issuer-specific factors, and market conditions. By assessing these factors, investors can gain a better understanding of the creditworthiness of a borrower and the potential for default.

There are several methods used to measure credit spreads, including option-adjusted spreads, yield spreads, and spread duration. Each method has its own advantages and disadvantages, and the choice of measurement will depend on the investor’s specific goals and needs.

Analyzing credit spreads is crucial for investors and financial institutions alike. By monitoring credit spreads, investors can identify potential investment opportunities or risks and adjust their portfolios accordingly. Financial institutions, such as banks, use credit spreads to assess the credit quality of their borrowers, determine lending rates, and manage risk.

In the following sections of this article, we will delve deeper into the components of credit spreads, the factors that influence them, and the various types of credit spreads that exist. We will also discuss the risks associated with credit spreads and highlight some common credit spread strategies.

Join us as we explore the fascinating world of credit spreads and gain valuable insights into the realm of fixed income investing.

Definition of Credit Spread

Credit spread refers to the difference in yield between two debt instruments of similar maturities but with different credit ratings. It is a measure of the market’s perception of the creditworthiness and default risk of a borrower or issuer. The credit spread reflects the compensation demanded by investors for taking on additional risk associated with a lower credit rating.

When an investor purchases a fixed income security, such as a bond or a loan, they expect to receive regular interest payments and the return of their principal at maturity. However, there is always a risk that the issuer may default on their obligations, leading to a loss for the investor. Credit spreads help to quantify this default risk by comparing the yield of a riskier security to that of a risk-free instrument with the same maturity.

Typically, a higher credit spread indicates a higher perceived risk of default by the borrower, while a lower credit spread suggests a lower perceived risk. This is because investors demand higher returns as compensation for taking on increased credit risk. Therefore, a higher credit spread translates to a higher yield on the riskier security to attract investors.

For example, let’s consider two bonds with the same maturity of 10 years. Bond A has a credit rating of AAA, indicating a low default risk, while Bond B has a credit rating of BB, indicating a higher default risk. The yield on Bond A might be 3%, while the yield on Bond B might be 6%. In this case, the credit spread between the two bonds would be 3%, reflecting the additional yield investors require for taking on the increased default risk of Bond B.

Credit spreads are an essential measure in the fixed income market and play a crucial role in investment decision-making. By analyzing credit spreads, investors can assess the relative credit risk of different investments, compare the compensation offered by various debt instruments, and identify opportunities for potential returns.

Components of Credit Spread

The credit spread of a debt instrument is influenced by various factors, each contributing to the overall perceived creditworthiness and risk associated with the borrower or issuer. Understanding the components of a credit spread is essential for assessing the relative credit risk of different investments. Here are some of the key components:

- Risk-Free Rate: The risk-free rate serves as a benchmark for measuring the additional compensation demanded by investors for taking on credit risk. It represents the theoretical return on an investment with no credit risk. Generally, the risk-free rate is derived from government bonds or other debt instruments with minimal default risk.

- Issuer Credit Rating: The credit rating of the issuer is a significant determinant of the credit spread. Credit rating agencies assess the creditworthiness of issuers and assign ratings that reflect their ability to fulfill their financial obligations. Higher-rated issuers with stronger credit profiles typically have lower credit spreads compared to lower-rated issuers with higher credit risk.

- Market Conditions: Market conditions, such as supply and demand dynamics, investor sentiment, economic indicators, and overall market volatility, can impact credit spreads. In times of economic uncertainty or market stress, credit spreads tend to widen as investors demand higher compensation for taking on additional risk. Conversely, during periods of economic stability and investor confidence, credit spreads may narrow.

- Liquidity: The liquidity of a debt instrument can influence its credit spread. Less liquid securities may attract higher credit spreads due to the increased difficulty of selling the security in the market. Investors require a higher compensation for holding illiquid securities as they face greater challenges in exiting their positions if needed.

- Term Structure: The time to maturity of a debt instrument also affects its credit spread. Generally, longer-maturity securities have higher credit spreads compared to shorter-maturity securities. This is because longer-term investments expose investors to more uncertainties and potential risks over an extended period.

These are just a few of the key components that contribute to the determination of credit spreads. It is important to analyze and consider each of these factors when evaluating the creditworthiness and risk associated with a particular investment.

Factors Affecting Credit Spread

Credit spreads are influenced by a range of factors that impact the perceived credit risk and the compensation demanded by investors. Understanding these factors helps investors assess the prevailing market conditions and make informed investment decisions. Here are some key factors that affect credit spreads:

- Economic Conditions: The overall state of the economy plays a significant role in determining credit spreads. During periods of economic expansion and growth, credit spreads tend to narrow as investors have higher confidence in the ability of issuers to meet their financial obligations. Conversely, during economic downturns or recessions, credit spreads widen as investors demand higher compensation for the increased risk of default.

- Interest Rates: Changes in interest rates impact credit spreads. When interest rates rise, credit spreads typically widen as investors demand higher returns to compensate for the increased cost of borrowing and potential default risk. Conversely, when interest rates decline, credit spreads tend to narrow as borrowing costs decrease and investors seek higher-yielding investments.

- Industry and Sector Factors: Credit spreads can vary across different industries and sectors. Factors such as regulatory changes, technological advancements, competition, and market dynamics within specific industries can impact the perceived credit risk of issuers and, therefore, their credit spreads.

- Issuer-Specific Factors: The financial health and creditworthiness of individual issuers significantly influence credit spreads. Factors such as revenue growth, profitability, leverage, management quality, and debt repayment capacity impact the perceived credit risk. Higher-quality issuers with strong financial profiles typically have lower credit spreads compared to issuers with weaker credit profiles.

- Market Sentiment: Investor sentiment and market perceptions can affect credit spreads. Positive market sentiment, driven by factors such as favorable economic indicators, strong corporate earnings, or increased risk appetite, can lead to narrower credit spreads. Conversely, negative sentiment, influenced by factors such as geopolitical risks, economic uncertainties, or financial market volatility, can cause credit spreads to widen as investors demand higher compensation for risk.

- Supply and Demand Dynamics: The supply and demand of debt securities in the market can impact credit spreads. Increased demand for a specific issuer’s debt securities, either due to strong market demand or limited supply, can result in narrower credit spreads. On the other hand, increased supply or reduced demand can lead to wider credit spreads as investors demand higher compensation for the increased risk.

It is important to note that the relative importance and impact of these factors on credit spreads may vary depending on the specific market conditions and individual investment circumstances. Monitoring and analyzing these factors can provide valuable insights into the credit market and assist investors in identifying opportunities and managing risks when making investment decisions.

Measurement of Credit Spread

The measurement of credit spreads is crucial for understanding and analyzing the credit risk associated with different debt instruments. There are various methods used to measure credit spreads, each providing unique insights into the relative creditworthiness and compensation offered by different securities. Here are some common approaches to measuring credit spreads:

- Option-Adjusted Spread (OAS): OAS is a widely used method for measuring credit spreads, especially in the bond market. It takes into account the embedded optionality of certain bonds, such as callable or convertible bonds, by adjusting for the potential changes in cash flows due to the exercise of these options. OAS provides a more accurate measure of the credit spread by factoring in the option risk.

- Yield Spread: Yield spread measures the difference in yield between a risky security and a comparable risk-free security with the same maturity. It represents the amount of additional yield investors demand for assuming the credit risk associated with the security. Yield spreads are commonly used to compare the relative credit risk of different bonds and assess the compensation offered by each.

- Spread Duration: Spread duration measures the sensitivity of a bond’s price to changes in credit spreads. It reflects the expected change in the bond’s price for a one basis point (0.01%) change in spread. Spread duration helps investors gauge the potential impact of credit spread movements on the value of their fixed income investments.

- Z-Spread: Z-spread, also known as the zero-volatility spread, measures the credit spread over the risk-free yield curve. It represents the constant spread added to the risk-free yield curve to make the present value of a bond’s cash flows equal to its market price. Z-spread is commonly used in the analysis of mortgage-backed securities and other structured products.

- Relative Value Spread: Relative value spread compares the credit spread of a bond or security to a benchmark, such as a comparable security from the same issuer or a benchmark index. It helps investors identify bonds or securities that may be overvalued or undervalued relative to their peers, considering their credit risk and compensation.

Each of these methods has its own advantages and limitations, and the choice of measurement depends on the specific requirements and goals of the investor. It is important to note that credit spread measurements are dynamic and can change over time due to market conditions, investor sentiment, and issuer-specific factors. Regular monitoring and analysis of credit spreads are essential for staying updated on the evolving credit market and making well-informed investment decisions.

Importance of Credit Spread Analysis

Credit spread analysis is a crucial component of fixed income investing and plays a significant role in assessing the creditworthiness and risk associated with debt instruments. Understanding the importance of credit spread analysis is essential for investors seeking to make informed investment decisions. Here are some reasons why credit spread analysis is important:

- Evaluating Credit Risk: Credit spread analysis provides insights into the credit risk associated with a particular investment. By comparing the credit spreads of different securities, investors can assess the relative creditworthiness of issuers and identify potential risks. A wider credit spread indicates a higher perceived default risk, while a narrower credit spread suggests a lower perceived risk.

- Assessing Relative Value: Credit spreads can help investors identify relative value opportunities in the fixed income market. By comparing the credit spreads of similar securities, investors can determine which securities offer higher returns for a given level of credit risk. This analysis enables investors to make more informed decisions about the potential returns and risks of different investment options.

- Monitoring Market Sentiment: Credit spreads can be a reflection of market sentiment and investor confidence. Wider credit spreads may indicate a more cautious market environment with higher perceived risks, while narrower credit spreads may indicate a more optimistic market sentiment. Monitoring changes in credit spreads can provide insights into market dynamics and help investors gauge market sentiment.

- Identifying Investment Opportunities: Credit spread analysis can help investors identify attractive investment opportunities. By analyzing credit spreads, investors can pinpoint securities that offer higher yields relative to their credit risk. This allows investors to potentially enhance their returns by selecting investments with favorable risk-reward profiles.

- Managing Portfolio Risk: Credit spread analysis is essential for managing portfolio risk in fixed income investments. By diversifying investments across different credit spreads, investors can mitigate risk by spreading exposure to different levels of credit risk. Understanding credit spreads allows investors to construct well-balanced portfolios that align with their risk tolerance and investment objectives.

- Negotiating Interest Rates: Credit spreads can also be relevant for borrowers. By understanding the credit spreads associated with their own debt instruments, borrowers can negotiate more favorable interest rates based on their creditworthiness. A strong credit profile and narrower credit spreads can help borrowers secure loans at lower interest rates, reducing their cost of borrowing.

Overall, credit spread analysis is vital for assessing credit risk, identifying investment opportunities, managing portfolio risk, and making well-informed investment decisions in the fixed income market. Continuously monitoring and analyzing credit spreads allow investors to stay informed about the prevailing market conditions and adapt their investment strategies accordingly.

Types of Credit Spreads

Credit spreads can take different forms based on the specific criteria used to assess the creditworthiness and risk associated with a debt instrument. Understanding the different types of credit spreads is important for investors to effectively evaluate and compare different investment options. Here are some common types of credit spreads:

- Corporate Credit Spreads: Corporate credit spreads compare the yield of corporate bonds to risk-free government bonds of the same maturity. These spreads reflect the additional compensation demanded by investors for taking on the credit risk associated with corporate issuers. Widening corporate credit spreads indicate increased perceived risk in the corporate bond market, while narrowing spreads may suggest improved market conditions and investor confidence.

- Municipal Credit Spreads: Municipal credit spreads compare the yield of municipal bonds, issued by state or local governments, to comparable risk-free government bonds. These spreads reflect the difference in credit risk between municipalities. Municipal credit spreads can vary based on factors such as the financial health of the issuing municipality, its revenue sources, and its ability to repay debt obligations. Higher-quality municipalities typically have narrower credit spreads compared to riskier municipalities.

- Emerging Market Credit Spreads: Emerging market credit spreads compare the yield of debt instruments issued by governments or corporations in emerging economies to comparable developed market bonds. These spreads reflect the additional compensation demanded by investors for the potentially higher political, economic, and currency risks associated with investing in emerging markets. Widening emerging market credit spreads typically indicate increased uncertainty and perceived risk in these markets.

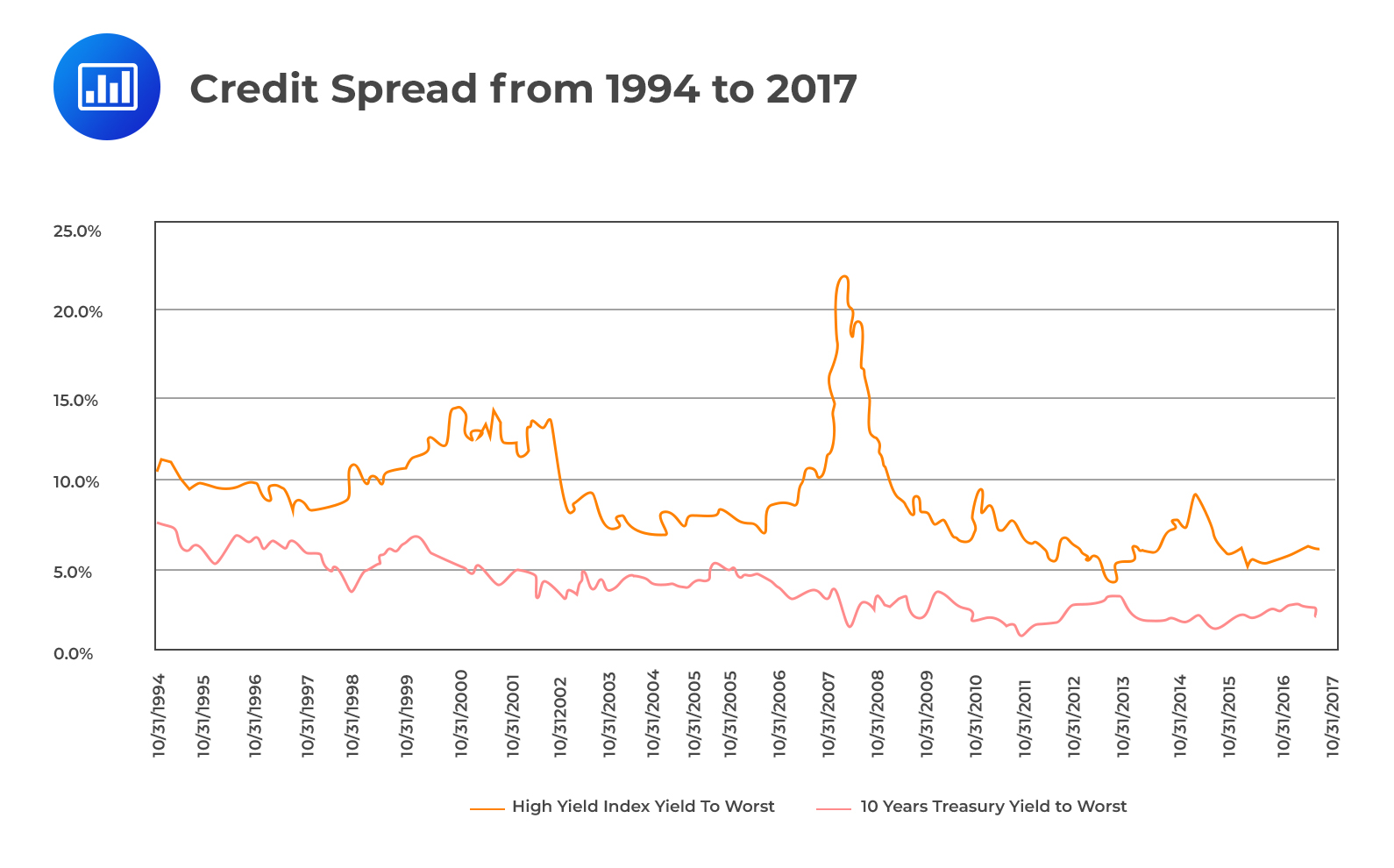

- High-Yield Credit Spreads: High-yield credit spreads, also known as junk bond spreads, compare the yield of high-yield or speculative-grade bonds to risk-free government bonds. These spreads reflect the higher credit risk associated with issuers that have lower credit ratings. High-yield credit spreads tend to be wider than investment-grade credit spreads due to the higher default risk associated with lower-rated issuers. Widening high-yield credit spreads may indicate deteriorating credit conditions, while narrowing spreads may signal improving investor sentiment.

- Investment-Grade Credit Spreads: Investment-grade credit spreads compare the yield of bonds with investment-grade credit ratings to risk-free government bonds. These spreads represent the compensation demanded by investors for assuming the credit risk associated with investment-grade issuers. Investment-grade credit spreads tend to be narrower than high-yield credit spreads due to the lower default risk associated with higher-rated issuers. Narrowing investment-grade credit spreads may indicate improving credit conditions, while widening spreads may suggest increasing market concerns.

It is important to note that credit spreads can vary depending on market conditions, investor sentiment, and the specific credit risk associated with issuers or sectors. By analyzing and comparing these different types of credit spreads, investors can gain insights into the relative credit risk and compensation offered by different debt instruments, helping them make informed investment choices.

Risks Associated with Credit Spreads

Credit spreads are not without their risks, and understanding these risks is crucial for investors when evaluating fixed income investments. Here are some of the key risks associated with credit spreads:

- Default Risk: One of the primary risks associated with credit spreads is default risk. Default risk refers to the possibility that the issuer of a debt instrument may fail to meet its financial obligations and default on its debt payments. When investing in securities with wider credit spreads, investors are exposed to a higher risk of default, which can result in significant losses.

- Market Risk: Credit spreads are influenced by market conditions, and changes in market sentiment and economic factors can impact credit spreads. Market risk refers to the potential for credit spreads to widen or narrow due to changes in market dynamics. Investors may face losses if credit spreads widen unexpectedly or if market conditions change unfavorably.

- Liquidity Risk: Liquidity risk is another factor to consider when investing in credit spreads. Less liquid securities, such as bonds issued by smaller companies or in emerging markets, may have wider credit spreads. In times of market stress or limited buyer interest, selling these securities at fair prices can be challenging, leading to potential losses or limited exit opportunities.

- Interest Rate Risk: Credit spreads can be influenced by changes in interest rates. If interest rates rise, credit spreads may widen as investors demand higher compensation for assuming credit risk. This, in turn, can result in lower bond prices and potential capital losses for investors. It is essential to consider the potential impact of interest rate movements on credit spreads when making investment decisions.

- Reinvestment Risk: Reinvestment risk refers to the risk of receiving lower returns when reinvesting cash flows from a bond or other fixed income security into new securities. If credit spreads narrow over time, the reinvestment of cash flows at lower spreads can lead to reduced income and potentially lower overall returns for investors.

- Issuer-Specific Risk: Credit spreads can be influenced by the credit risk associated with specific issuers or sectors. Investing in securities with wider credit spreads may expose investors to higher credit risk due to factors such as deteriorating financial conditions, regulatory changes, or industry-specific challenges. Understanding issuer-specific risks is important when evaluating credit spreads.

It’s crucial for investors to carefully assess these risks and conduct thorough due diligence when investing in credit spreads. Diversifying investments, staying informed about market conditions, and monitoring the credit quality of issuers can help mitigate these risks and enhance the potential for positive returns in fixed income investments.

Credit Spread Strategies

Credit spreads present various opportunities for investors to implement strategies that seek to generate returns through the analysis and management of credit risk. These strategies can be useful in different market conditions and help investors achieve specific investment objectives. Here are some common credit spread strategies:

- Buy and Hold: The buy and hold strategy involves purchasing bonds or other debt instruments with credit spreads that are attractive relative to their perceived credit risk and holding them until maturity. This strategy capitalizes on the potential for narrowing credit spreads over time, leading to capital gains for the investor.

- Relative Value Trading: Relative value trading involves identifying mispriced credit spreads among similar securities and taking advantage of the price differences. Investors look for securities with wider credit spreads compared to their fundamental credit risk, anticipating that the spreads will narrow, allowing them to capture the price appreciation and generate returns.

- Credit Spread Option Strategies: Options can be used to implement credit spread strategies. For example, an investor can sell credit spread options, such as credit default swaps (CDS), to receive premiums from buyers who seek protection against credit events. This strategy generates income for the seller while assuming the risk of a credit event occurring.

- Credit Spread Duration Management: Credit spread duration management involves actively managing the duration of a bond portfolio to take advantage of changes in credit spreads. Investors may adjust the weighted average duration of their portfolio by buying or selling bonds with different maturities or changing the allocation between investment-grade and high-yield bonds.

- Quality Selection: Quality selection strategy involves actively assessing and selecting securities based on their credit quality and associated spreads. Investors seek securities with narrower credit spreads relative to their credit rating, indicating potential mispricing or undervaluation. By focusing on high-quality issuers with strong credit profiles, investors aim to minimize default risk and potentially generate stable returns.

- Issuer Diversification: Diversification is an important strategy when investing in credit spreads. By spreading investments across different issuers, sectors, and regions, investors reduce the impact of defaults by any single issuer. Diversification can help manage the risk associated with credit spreads and enhance the overall risk-adjusted returns of the portfolio.

It’s important to note that credit spread strategies involve inherent risks and may require thorough research, analysis, and monitoring. Each strategy has its own advantages and considerations, and the suitability of a particular strategy will depend on an investor’s risk tolerance, investment goals, and market outlook. It is advisable to consult with a financial advisor or investment professional before implementing any credit spread strategy.

Conclusion

Credit spreads play a significant role in fixed income investing, providing valuable insights into the credit risk associated with debt instruments. Understanding credit spreads and their analysis is crucial for investors seeking to make informed investment decisions and manage their portfolios effectively. By assessing credit spreads, investors can evaluate the relative creditworthiness of issuers, identify attractive investment opportunities, and manage the risks associated with credit risk exposure.

This comprehensive guide has covered the fundamentals of credit spreads, including their definition, components, measurement methods, and various types. We explored the factors that influence credit spreads and discussed the importance of credit spread analysis in evaluating credit risk, assessing relative value, and monitoring market conditions. Additionally, we highlighted some common credit spread strategies that investors can utilize to capitalize on credit risk opportunities.

It is crucial to remember that credit spreads are not without risks. Investors should be aware of potential default risk, market risk, liquidity risk, and other factors that can impact credit spreads. Proper risk management and due diligence are essential when investing in credit spreads.

In conclusion, credit spread analysis provides investors with a valuable tool to evaluate the creditworthiness of issuers, assess market conditions, and make informed investment decisions. By understanding credit spreads and employing effective strategies, investors can navigate the fixed income market and potentially achieve their investment goals while managing risk effectively.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance