Finance

What Is Credit Spread

Published: January 13, 2024

Learn about credit spread in finance and how it affects your financial decisions. Understand the concept and make informed choices.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to the world of finance, where terms like credit spread play a crucial role in understanding and assessing investment opportunities. Whether you’re an experienced investor or just starting to dip your toes into the world of finance, understanding credit spreads is essential for making informed decisions.

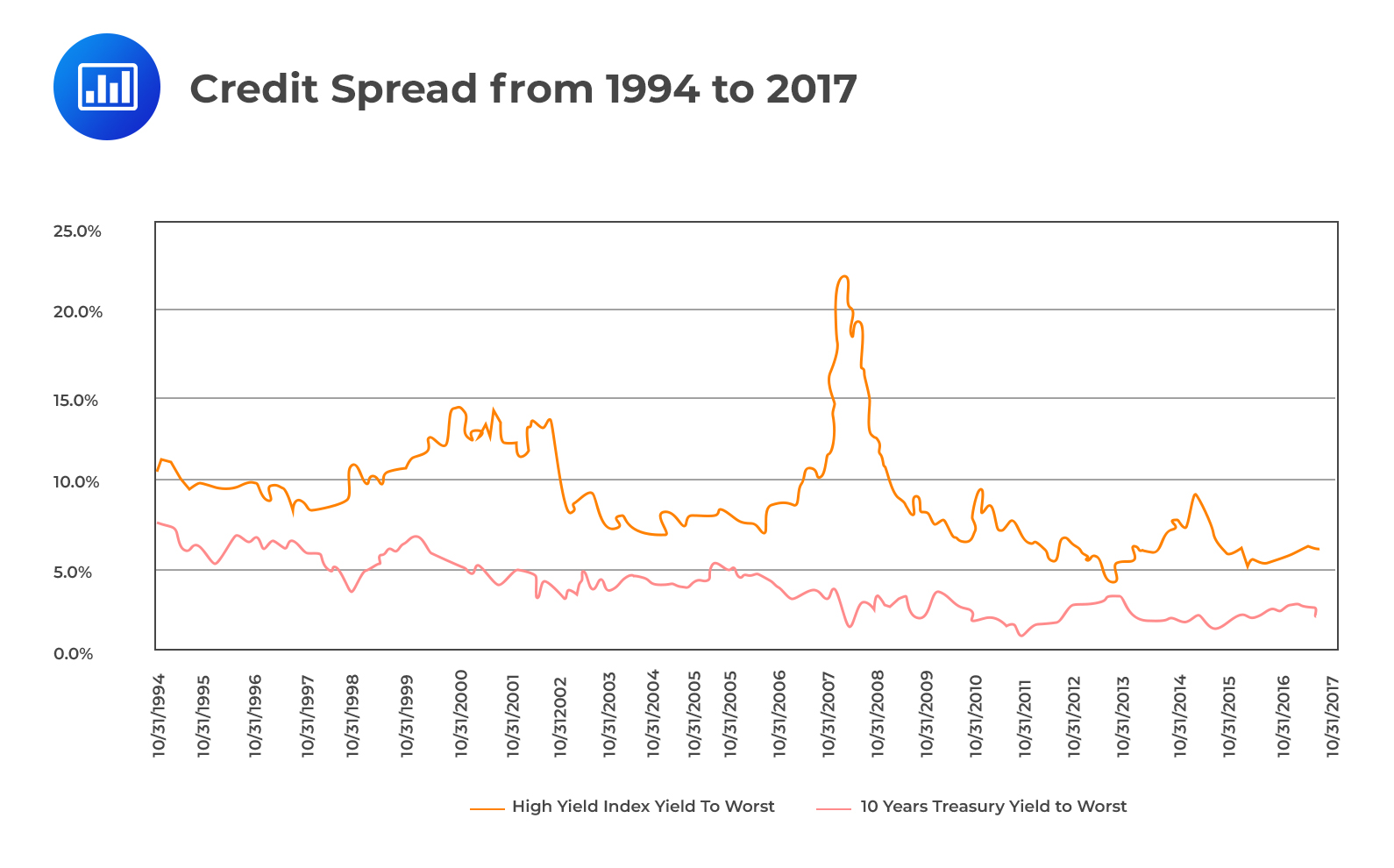

A credit spread is a term commonly used in the world of fixed income securities and options trading. It refers to the difference in interest rates or yields between two financial instruments with similar maturities but varying degrees of credit quality. In simple terms, it represents the compensation investors receive for taking on additional credit risk.

The calculation of the credit spread involves comparing the yield of a specific bond or security with a benchmark yield, typically a government bond with an equivalent maturity. The credit spread reflects the market’s perception of the issuer’s creditworthiness and the risk of default.

As an investor, understanding credit spreads is crucial because it provides insight into the risk-reward profile of an investment. A wider credit spread indicates greater perceived risk and higher potential returns, while a narrower credit spread suggests lower perceived risk and lower potential returns.

There are various factors that influence credit spreads. Market conditions, economic indicators, credit rating changes, and investor sentiment all play a role in determining the attractiveness of a particular credit spread. Being aware of these factors can help investors better navigate the bond market and identify opportunities for potential gains.

Credit spreads are of great importance to both issuers and investors. For issuers, understanding credit spreads can help determine the interest rate they offer to attract investors and raise funds. A narrower credit spread allows issuers to borrow at a lower cost, while a wider credit spread may indicate higher borrowing costs due to perceived credit risk.

For investors, credit spreads serve as an essential tool for assessing the riskiness and potential return of a fixed income investment. It helps investors compare bonds with similar maturities but differing credit qualities and make informed investment decisions based on their risk appetite and return expectations.

There are different types of credit spreads, including yield spreads, option-adjusted spreads, and spread duration. Each type provides investors with a different perspective on the credit risk associated with a specific investment. Understanding these different types of credit spreads can help investors evaluate investment alternatives and select the most suitable options for their portfolios.

In the next sections, we will delve deeper into the calculation of credit spreads, the factors that affect them, the importance of credit spreads, different types of credit spreads, trading strategies using credit spreads, and the risks associated with them. By the end of this article, you will have a comprehensive understanding of credit spreads and be equipped to make informed investment decisions in the realm of fixed income securities and options trading.

Definition of Credit Spread

A credit spread, in the world of finance, refers to the difference in interest rates or yields between two financial instruments with similar maturities but varying degrees of credit quality. It is a measure of the compensation that investors receive for taking on additional credit risk.

To understand credit spreads better, let’s break down the components. The first component is the benchmark yield, typically a government bond with an equivalent maturity. This is considered to have almost no credit risk since governments are generally viewed as reliable borrowers.

The second component is the yield of the bond or security being evaluated. This yield incorporates the perceived credit risk of the issuer. The credit spread is calculated by subtracting the benchmark yield from the yield of the bond or security under analysis.

For example, let’s say that a 10-year government bond is currently yielding 2% and a corporate bond with a similar maturity is yielding 4%. The credit spread in this case would be 2%, as it represents the additional yield that investors demand for taking on the credit risk associated with the corporate bond.

Credit spreads are often expressed in basis points (bps), where one basis point is equal to 0.01%. So, a credit spread of 200 bps is equivalent to 2%.

A wider credit spread indicates a higher perceived credit risk and suggests that investors will demand higher compensation for holding the bond or security. On the other hand, a narrower credit spread signifies a lower perceived credit risk, indicating that investors are willing to accept lower compensation for taking on the bond’s credit risk.

Credit spreads can vary widely depending on the creditworthiness of the issuer. High-quality issuers, such as governments or highly rated corporations, typically have narrower credit spreads since investors perceive them to have lower default risk. In contrast, lower-rated issuers or those with a history of financial instability will have wider credit spreads to compensate investors for the heightened credit risk.

Credit spreads are crucial in fixed income securities and options trading because they provide valuable insights into the risk-return profile of an investment. By analyzing credit spreads, investors and analysts can assess the attractiveness of a bond or security, compare different investment options, and make informed investment decisions based on their risk appetite and return expectations.

Calculation of Credit Spread

Calculating a credit spread involves comparing the yield or interest rate of a specific bond or security with a benchmark yield. The benchmark yield is typically a government bond with an equivalent maturity, which is considered to have minimal credit risk.

The credit spread is obtained by subtracting the benchmark yield from the yield of the bond or security being evaluated. The resulting figure represents the additional compensation that investors demand for taking on the credit risk associated with the bond or security.

Let’s illustrate the calculation process with an example. Suppose we have a corporate bond with a yield of 5% and a 10-year government bond with a yield of 2%. To determine the credit spread, we subtract the government bond yield from the corporate bond yield:

Credit Spread = Corporate Bond Yield – Government Bond Yield

Credit Spread = 5% – 2%

Credit Spread = 3%

In this example, the credit spread is 3%. This means that investors are demanding an additional 3% yield for bearing the credit risk associated with the corporate bond compared to the risk-free government bond.

Credit spreads are often expressed in basis points (bps), where one basis point is equal to 0.01%. The credit spread in our example of 3% would then be equivalent to 300 basis points.

It is essential to note that credit spreads can vary depending on the credit quality of the issuer, the overall market conditions, and investor sentiment. Higher credit spreads indicate higher credit risk and potentially higher returns, while narrower spreads suggest lower credit risk and lower potential returns.

Furthermore, it is important to keep in mind that credit spreads can fluctuate over time as market conditions and investor perceptions change. They can widen during periods of economic uncertainty or when the creditworthiness of the issuer deteriorates. Conversely, credit spreads can narrow when economic conditions improve or when investor confidence in the issuer increases.

Calculating credit spreads allows investors to evaluate the risk-reward profile of fixed income securities and make informed investment decisions. By analyzing credit spreads, investors can compare different bonds or securities, assess the creditworthiness of issuers, and identify opportunities for potential gains.

Factors Affecting Credit Spread

Credit spreads are influenced by a variety of factors that impact the perceived creditworthiness of an issuer and the demand for their bonds or securities. Understanding these factors is crucial for investors and analysts to assess credit risk and make informed investment decisions. Here are some key factors that can influence credit spreads:

1. Credit Rating: The credit rating of an issuer assigned by rating agencies, such as Moody’s, Standard & Poor’s, and Fitch, is a significant factor in determining credit spreads. Higher-rated issuers with strong creditworthiness tend to have narrower credit spreads, reflecting lower perceived default risk. Conversely, issuers with lower credit ratings or negative credit events may experience wider spreads, as investors demand higher compensation for taking on higher credit risk.

2. Economic Conditions: The overall economic environment plays a vital role in shaping credit spreads. During periods of economic growth and stability, credit spreads tend to narrow as default risks decrease and investor confidence rises. Conversely, economic downturns or recessions can lead to wider credit spreads due to increased default risks and investor concerns about the financial health of issuers.

3. Market Sentiment: Investor sentiment and market perception can impact credit spreads. Positive market sentiment and optimism can lead to narrower spreads as investors are more willing to accept lower compensation for taking on credit risk. Conversely, negative market sentiment and fear can widen credit spreads as investors become more risk-averse and demand higher returns for bearing credit risk.

4. Liquidity: The liquidity of the bond or security being evaluated also influences credit spreads. Bonds or securities that are more liquid and actively traded tend to have narrower spreads due to increased market confidence and ease of buying or selling. Less liquid bonds may experience wider spreads as investors may demand higher compensation for the potential difficulties in trading these securities.

5. Interest Rates: Changes in interest rates can impact credit spreads. When interest rates rise, credit spreads may widen as investors may demand higher returns to compensate for the opportunity cost of holding bonds or securities with credit risk. Conversely, when interest rates decline, credit spreads may narrow as investors seek higher yields in riskier assets.

6. Industry or Sector Factors: Credit spreads can also be influenced by industry-specific or sector-specific factors. Certain industries or sectors may be more prone to credit risk due to factors such as regulatory changes, technological disruptions, or market dynamics. Investors may demand higher compensation for investing in bonds or securities within these riskier sectors, leading to wider spreads.

7. Company-Specific Factors: Issuer-specific factors such as financial health, management quality, business performance, and specific events like mergers, acquisitions, or legal proceedings can impact credit spreads. Positive developments or strong financial performance may narrow spreads, while negative events or weak financial indicators can widen spreads.

It is important to note that these factors do not operate in isolation but interact with each other. For example, adverse economic conditions may impact an issuer’s credit rating, leading to wider credit spreads. Likewise, a positive development in a specific industry may lead to narrower spreads for issuers within that sector.

By considering these factors, investors and analysts can assess credit risk more effectively and make informed investment decisions based on their risk appetite and investment objectives. Monitoring changes in these factors allows investors to stay updated on evolving credit conditions and adjust their investment strategies accordingly.

Importance of Credit Spreads

Credit spreads play a vital role in the world of finance and investments. They provide valuable insights into the risk and return dynamics of fixed income securities and help investors make informed decisions. Here are some key reasons why credit spreads are important:

1. Risk Assessment: Credit spreads serve as a crucial tool for assessing credit risk. By analyzing the credit spread of a bond or security, investors can gauge the market’s perception of the issuer’s creditworthiness. Wider spreads indicate higher credit risk, while narrower spreads suggest lower credit risk. This information allows investors to evaluate the risk associated with a particular investment and adjust their portfolio accordingly.

2. Yield Comparison: Credit spreads enable investors to compare the yield or return of different fixed income securities. By considering the credit spreads of bonds with similar maturities but varying credit qualities, investors can evaluate the additional compensation they would receive for taking on credit risk. This allows for a more accurate assessment of the risk-return profile of investment alternatives and helps investors identify opportunities for potential gains.

3. Investment Decisions: Credit spreads assist investors in making informed investment decisions. By considering the credit quality of an issuer and the corresponding credit spread, investors can determine whether a bond or security offers an adequate return given the associated credit risk. This information is especially valuable for risk-conscious investors who seek to balance risk and return, aligning their investment choices with their financial goals and risk appetite.

4. Portfolio Diversification: Credit spreads facilitate portfolio diversification. By investing in bonds or securities with different credit qualities, investors can spread their risk across a range of issuers and industries. Credit spreads help investors identify investment opportunities in different sectors or credit segments, allowing for a more diversified portfolio that can potentially reduce overall risk and enhance returns.

5. Bond Pricing: Credit spreads play a significant role in the pricing of bonds. When analyzing the value of a bond, investors consider the credit spread in conjunction with other factors such as interest rates and the bond’s maturity. A wider credit spread typically results in a lower bond price, as investors demand higher compensation for the perceived credit risk. Conversely, a narrower credit spread generally leads to a higher bond price due to the lower perceived credit risk.

6. Market Sentiment Indicator: Credit spreads can serve as an indicator of market sentiment. Narrowing credit spreads often signal improving market conditions and increased investor confidence, while widening spreads may suggest deteriorating sentiment and rising concerns over credit risk. Monitoring changes in credit spreads can provide valuable insights into market trends, helping investors stay attuned to evolving market conditions and adjust their investment strategies accordingly.

Overall, credit spreads provide essential information for investors to assess credit risk, compare investment alternatives, and make informed decisions. By understanding credit spreads and their implications, investors can navigate the fixed income market more effectively and align their portfolios with their financial goals and risk tolerance.

Types of Credit Spreads

Credit spreads come in various forms, each providing a unique perspective on credit risk and aiding investors in their decision-making process. Here are the main types of credit spreads:

1. Yield Spreads: Yield spreads represent the difference in yields between two securities with similar maturities but varying degrees of credit quality. They are commonly used to compare the yields of corporate bonds or other fixed income securities with those of government bonds or risk-free benchmarks. Yield spreads help investors understand the additional compensation demanded by the market for bearing credit risk.

2. Option-Adjusted Spreads (OAS): Option-adjusted spreads take into account embedded options, such as call or put provisions, within bonds or securities. These spreads reflect the additional yield that investors require to compensate for the uncertainty associated with potential changes in interest rates or other factors that may impact the value of the embedded options. OAS provides a more accurate measure of credit risk by adjusting for the impact of these options on bond pricing.

3. Z-Spreads: Z-spreads measure the spread over the risk-free rate that compensates investors for the credit risk and any other risks associated with a bond or security. Unlike yield spreads, which compare the yields of two different securities, the Z-spread is added to each cash flow of a bond’s yield curve until the present value of all the cash flows equals the bond’s market price. Z-spreads help investors assess the overall compensation that they can expect for investing in a particular bond.

4. Option Cost Spreads: Option cost spreads are used in the analysis of structured credit products, such as mortgage-backed securities or collateralized debt obligations (CDOs). These spreads represent the additional yield demanded by investors to compensate for the embedded options within these securities, such as prepayment or default risk. Option cost spreads help investors assess the risk-reward profile of these complex financial instruments.

5. Spread Duration: Spread duration measures the sensitivity of a bond or security’s price to changes in credit spreads. It provides an estimate of the potential price impact resulting from changes in credit risk. Spread duration helps investors evaluate the risk associated with changes in credit spreads and make decisions based on their risk appetite and investment horizon.

Each type of credit spread offers valuable insights into the credit risk and compensation associated with different bonds or securities. Investors can choose the most suitable type(s) of credit spread based on their investment objectives, risk tolerance, and the specific characteristics of the securities they are analyzing. By analyzing these spreads, investors can gain a comprehensive understanding of the risk-reward profiles of different fixed income instruments and make informed investment decisions.

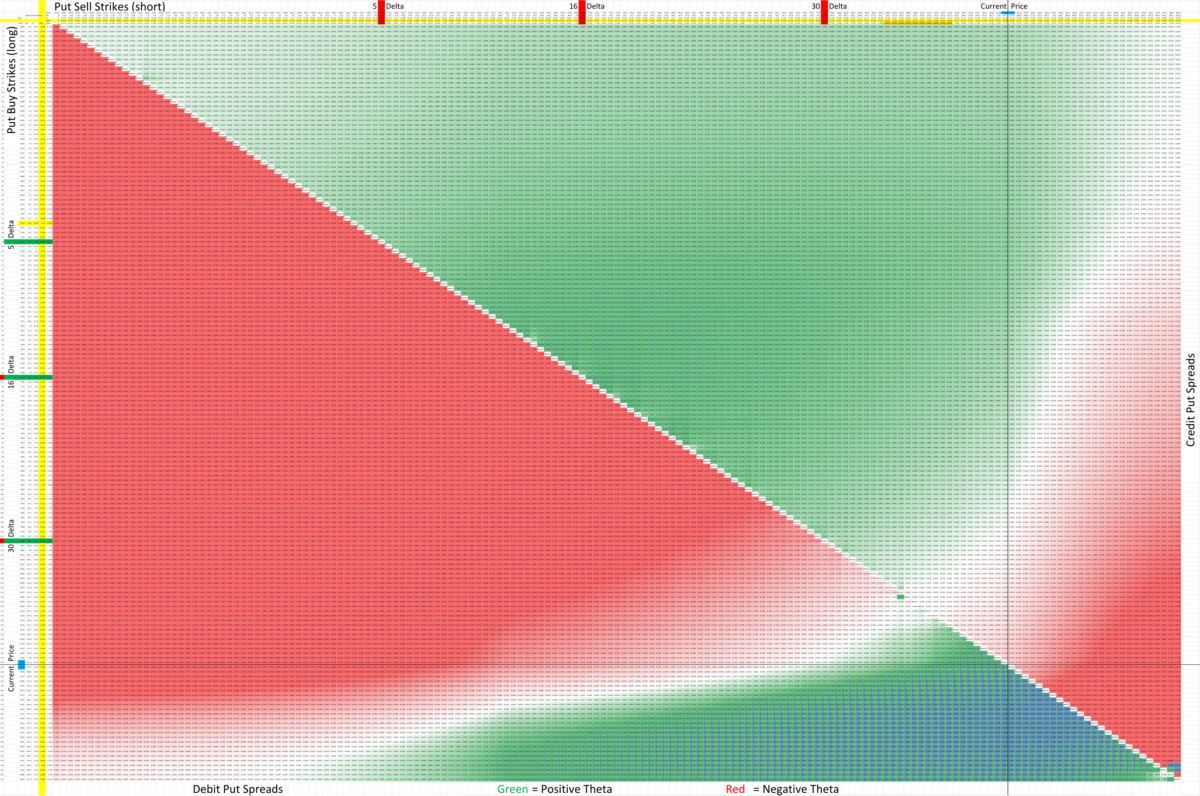

Trading Strategies Using Credit Spreads

Credit spreads can be utilized in various trading strategies to take advantage of perceived opportunities and manage risk. These strategies aim to profit from changes in credit spreads or to generate income by selling credit protection. Here are a few common trading strategies using credit spreads:

1. Bullish Credit Spread: This strategy is implemented when an investor expects the credit spread to narrow. It involves buying a lower-yielding bond or security while simultaneously selling a higher-yielding bond or security with the same maturity. The investor profits if the credit spread narrows, as the higher-yielding security’s price decreases more than the lower-yielding security, resulting in a net gain.

2. Bearish Credit Spread: In contrast to a bullish credit spread, a bearish credit spread is employed when an investor anticipates the credit spread to widen. It entails selling a lower-yielding bond or security and simultaneously buying a higher-yielding bond or security with the same maturity. If the credit spread widens, the higher-yielding security’s price decreases less than the lower-yielding security, resulting in a net gain.

3. Credit Spread Option Strategies: Option strategies using credit spreads involve positions in credit options to profit from changes in credit spreads. For example, a credit put spread strategy consists of selling a put option on a bond or security with a higher perceived credit risk and simultaneously buying a put option on a bond or security with lower perceived credit risk. The investor profits if the credit spread narrows or if the options expire worthless, resulting in a gain from the premium received.

4. Spread Trading: Spread trading involves simultaneously buying and selling different bonds or securities with similar characteristics but diverging credit spreads. The objective is to capture the price differential between the two securities as the credit spreads converge. Traders can take advantage of temporary market inefficiencies or mispricings to generate a profit from the convergence of credit spreads.

5. Income Generation: Selling credit spreads can be a strategy to generate income. By selling credit default swaps, credit options, or spreads, investors receive a premium in exchange for agreeing to bear the credit risk of a particular issuer. If the credit event does not occur, and the issuer does not default, the investor keeps the premium as income. This strategy can be useful for investors seeking additional yield and who have a favorable outlook on the creditworthiness of the underlying issuer.

It’s important to note that trading strategies using credit spreads involve risks, including the potential for losses if the credit spreads move in an unexpected direction. As with any trading strategy, thorough research, risk management, and understanding of market dynamics are essential. Investors should review their risk tolerance and consult with financial professionals before implementing credit spread trading strategies.

By utilizing these strategies effectively, investors can potentially capitalize on changing credit spreads and generate profits or income in the fixed income market.

Risks Associated with Credit Spreads

While credit spreads can present opportunities for investors, it is essential to understand and evaluate the risks involved. Here are some key risks associated with credit spreads:

1. Credit Risk: The primary risk associated with credit spreads is credit risk. Credit risk refers to the possibility that the issuer of a bond or security may default on its debt obligations or experience a credit event, such as a bankruptcy. When investing in bonds or securities with wider credit spreads, there is a higher chance of default, which can result in significant losses for investors.

2. Market Volatility: Credit spreads can be influenced by market volatility. Increased market volatility can lead to wider credit spreads as investors demand higher compensation for bearing the uncertainty and perceived risk. Sudden shifts in investor sentiment, economic conditions, or geopolitical events can trigger significant changes in credit spreads, potentially impacting the value of investments.

3. Liquidity Risk: Liquidity risk arises when there is insufficient demand for buying or selling a specific bond or security at a reasonable price. If an investor holds a bond with a wider credit spread that has low liquidity, it may be challenging to sell the asset quickly or at a fair price. This illiquidity can result in transaction costs, delays, or even the inability to exit the position, potentially leading to losses.

4. Interest Rate Risk: Changes in interest rates can affect credit spreads. When interest rates rise, credit spreads may widen as investors require additional compensation for the opportunity cost of holding riskier bonds or securities. Conversely, when interest rates decline, credit spreads may narrow as investors move towards higher-yielding assets. Interest rate movements can impact the value of bonds or securities with credit spreads and potentially result in capital losses.

5. Systemic Risk: Systemic risk refers to the risk of a widespread disruption or breakdown in the financial system. Credit spreads can be influenced by systemic factors such as financial crises, market panics, or regulatory changes. Systemic risks can cause a sharp increase in credit spreads, impacting the value of investments and potentially leading to significant losses.

6. Downgrade Risk: Credit spreads are influenced by credit ratings assigned by rating agencies. A downgrade in the credit rating of an issuer can result in wider credit spreads for their bonds or securities. Negative news or events surrounding the issuer, such as deteriorating financial health or adverse business conditions, can trigger a downgrade. Downgrade risk can lead to a decrease in the value of investments and potential losses for investors.

7. Event Risk: Event risk refers to the risk associated with specific events that can impact the creditworthiness of an issuer. Events such as mergers, acquisitions, regulatory changes, or legal proceedings can lead to changes in credit spreads. Investors need to monitor these events and assess their potential impact on the credit risk and value of their investments.

It is crucial for investors to carefully assess and manage these risks when investing in bonds or securities with credit spreads. Diversification, thorough research, monitoring credit ratings, and staying informed about market conditions are essential risk management strategies. Consulting with financial professionals or advisors can also provide valuable insights and guidance in navigating the risks associated with credit spreads.

By understanding these risks, investors can make informed decisions and potentially mitigate the potential negative effects associated with credit spreads.

Conclusion

Credit spreads are a fundamental concept in the world of finance, providing valuable information about credit risk and investment opportunities. Understanding credit spreads is essential for investors and analysts looking to assess the risk-return profiles of fixed income securities and make informed investment decisions.

In this article, we explored the definition of credit spreads and their calculation process. We discussed the factors that influence credit spreads, including credit ratings, economic conditions, market sentiment, and more. We highlighted the importance of credit spreads in assessing risk, comparing investments, and diversifying portfolios.

We also explored the different types of credit spreads, including yield spreads, option-adjusted spreads, and spread duration, each offering unique insights into credit risk and investment analysis. Additionally, we discussed various trading strategies that utilize credit spreads, including bullish and bearish spreads, option strategies, spread trading, and income generation strategies.

However, it is crucial to acknowledge the risks associated with credit spreads. Credit risk, market volatility, liquidity risk, and other factors can impact the value of investments and potentially lead to losses. Understanding and managing these risks is integral in implementing sound investment strategies.

In conclusion, credit spreads are a valuable tool for investors in evaluating risk and return in the fixed income market. By analyzing credit spreads, investors can make informed investment decisions, navigate market changes, and potentially capitalize on opportunities. It is important to conduct thorough research, regularly monitor credit conditions, and seek professional advice to effectively utilize credit spreads and manage associated risks.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance