Finance

What Does RCV Mean On An Insurance Claim

Published: November 13, 2023

Learn what RCV means on an insurance claim and how it relates to finance. Understand the importance of this term in the insurance industry and how it can impact your coverage.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding RCV and Insurance Claims

- Definition of RCV

- Importance of RCV in Insurance Claims

- Factors Affecting RCV Calculation

- RCV vs. ACV

- How RCV Impacts Insurance Claims

- Examples of RCV Calculation

- Common Issues and Challenges with RCV Claims

- Tips for Navigating RCV Claims Successfully

- Conclusion

Introduction

Welcome to the world of insurance claims! If you’ve recently experienced a loss or damage to your property and need to file an insurance claim, you may have come across the term “RCV.” But what does RCV mean in the context of insurance claims? Don’t worry, we’re here to demystify it for you.

RCV stands for “Replacement Cost Value” or “Reproduction Cost Value.” It is a crucial concept in the insurance industry as it determines the amount of money you will receive from your insurance company to repair or replace your damaged property. Understanding RCV is vital for ensuring you receive fair compensation for your losses.

In this article, we will dive into the definition of RCV and its importance in insurance claims. We’ll also discuss the factors that affect RCV calculations and explore the difference between RCV and ACV (Actual Cash Value). Additionally, we will provide examples of RCV calculations and highlight common issues and challenges that can arise during the RCV claims process. Finally, we’ll offer tips to help you navigate RCV claims successfully.

So, whether you’re a policyholder looking to better understand RCV or an insurance professional seeking insights into the intricacies of RCV claims, this article has got you covered. Let’s get started by exploring the fundamental meaning of RCV and its significance in the world of insurance.

Understanding RCV and Insurance Claims

Insurance claims can be complex and overwhelming, especially when it comes to determining the value of your damaged property. That’s where RCV comes into play. RCV is a key factor in insurance claims, as it determines the amount of money you will receive from your insurance company to repair or replace your damaged property.

When you file an insurance claim, the insurance company will typically assess the extent of the damage and calculate the cost to repair or replace the property. This is where RCV comes in. The RCV represents the cost to replace or reproduce the damaged property with a new item of similar kind and quality at current market prices.

For example, let’s say a fire damages your home. The insurance adjuster will evaluate the cost to rebuild your damaged home based on the current construction costs in your area. This includes labor, materials, and any associated expenses. The RCV is an essential component in determining the coverage limits of your insurance policy and the amount you will receive for your claim.

It’s important to note that RCV takes into account the full cost of replacing the damaged property, regardless of its age or depreciation. This is different from ACV (Actual Cash Value), which factors in depreciation and age of the property at the time of the loss. Typically, policies that provide RCV coverage will initially pay out the ACV and then reimburse the policyholder for the difference between the ACV and the RCV once repairs or replacements are complete.

The purpose of RCV is to ensure that policyholders are adequately compensated for their losses, allowing them to restore their property to its pre-loss condition. However, it’s important to understand that RCV may have certain limitations and exclusions depending on the specific terms and conditions of your insurance policy.

Now that we have defined RCV and its role in insurance claims, let’s delve into its significance and why it’s crucial for both policyholders and insurance companies.

Definition of RCV

RCV, or Replacement Cost Value, is a term used in the insurance industry to refer to the cost of replacing or reproducing damaged property with a comparable new item of similar kind and quality. It represents the current market value of the item at the time of the loss.

When determining the RCV, insurance companies consider various factors, such as the cost of labor, materials, and any associated expenses required to repair or replace the damaged property. In essence, RCV reflects the actual cost of fully restoring the property to its pre-loss condition.

It’s important to note that RCV does not take depreciation into account. Unlike Actual Cash Value (ACV), which factors in depreciation and the age of the damaged item, RCV focuses on the cost of replacing the property without considering any reduction in value due to wear and tear, age, or obsolescence.

For example, let’s say you have an insurance policy that covers the RCV of your computer equipment. If your computer is damaged or destroyed, the insurance company will assess the cost of purchasing a brand-new computer of equivalent specifications and quality, rather than reimbursing you for the depreciated value of your old computer.

It’s important to review your insurance policy to understand the specific terms and conditions relating to RCV coverage. Some policies may have limitations or exclusions that could impact the reimbursement amount for certain types of property or damages.

Now that we have a clear understanding of what RCV means, let’s explore why it holds such significance in the realm of insurance claims.

Importance of RCV in Insurance Claims

RCV, or Replacement Cost Value, plays a crucial role in insurance claims by ensuring that policyholders receive fair compensation for their losses. It is integral to accurately assessing the value of damaged property and determining the appropriate coverage limits of an insurance policy.

One of the key reasons RCV is important is that it allows policyholders to fully restore their damaged property to its pre-loss condition. By considering the current market value of replacement materials, labor costs, and associated expenses, RCV ensures that policyholders can afford to repair or replace their damaged property without incurring a significant financial burden.

Additionally, RCV provides a more accurate reflection of the overall value of the insured property. Unlike Actual Cash Value (ACV), which factors in depreciation and reduces the payout based on the age and wear and tear of the item, RCV reimburses policyholders based on the cost of replacing the damaged property with a new item of similar kind and quality. This ensures that policyholders are not penalized for the depreciation of their property over time.

Furthermore, RCV helps policyholders avoid underinsurance. Underinsurance occurs when the coverage limits of an insurance policy do not adequately reflect the true value of the insured property. In such cases, policyholders may not receive sufficient compensation to fully repair or replace their damaged property. RCV provides a more accurate assessment of the replacement costs, helping policyholders avoid the financial strain that may occur due to underinsurance.

On the other hand, RCV is also important for insurance companies as it allows them to accurately assess the potential extent of their liability and set appropriate premiums for policyholders. By considering the cost of replacement, insurance companies can ensure that they are providing adequate coverage and charging premiums that reflect the level of risk involved.

In summary, the importance of RCV in insurance claims cannot be overstated. It ensures that policyholders receive sufficient compensation to repair or replace their damaged property, avoids underinsurance, and allows insurance companies to accurately assess the potential liability. Now that we understand the significance of RCV, let’s explore the factors that can affect the calculation of RCV in insurance claims.

Factors Affecting RCV Calculation

Several factors come into play when calculating the Replacement Cost Value (RCV) in an insurance claim. Understanding these factors is essential for accurately assessing the cost of replacing or repairing the damaged property. Here are some key factors that can affect the RCV calculation:

- Materials and labor costs: The cost of materials, such as building materials, fixtures, and appliances, fluctuates over time due to market conditions and availability. Similarly, labor costs vary depending on factors such as location, expertise required, and current wage rates. These costs significantly impact the overall RCV calculation.

- Building codes and regulations: When repairing or replacing damaged property, it’s important to consider any changes in building codes or regulations that may require additional work or upgrades. Compliance with current codes and regulations can increase the cost of the project and, consequently, the RCV.

- Complexity of the project: The complexity of the repair or replacement project can affect the RCV calculation. Projects that involve intricate architectural designs, custom features, or specialized materials can significantly increase the cost of the overall project and, consequently, the RCV.

- Age and condition of the property: The age and condition of the damaged property are important factors to consider. Older properties may require extra attention and cost for restoration due to wear and tear or outdated features. The RCV calculation takes into account the cost of replacing or repairing the property in its current condition.

- Regional and local factors: Regional and local factors, such as geographical location, labor costs, and availability of materials, can impact the RCV calculation. The cost of living, construction rates, and market conditions can vary significantly from one region to another, leading to variations in RCV calculations.

It’s crucial to work with a qualified insurance adjuster or contractor who can assess these factors accurately and provide an appropriate RCV estimate. They will consider the specific details of the property and the scope of the repairs or replacements needed to calculate an accurate RCV.

Keep in mind that insurance policies may have specific provisions or endorsements that dictate how certain factors are considered in the RCV calculation. Always review your policy carefully to ensure you understand how these factors are addressed.

Understanding the various factors that influence the RCV calculation can help policyholders and insurance companies alike in accurately assessing the cost of repairing or replacing damaged property. Now that we’ve explored the factors affecting RCV, let’s differentiate between RCV and Actual Cash Value (ACV) in insurance claims.

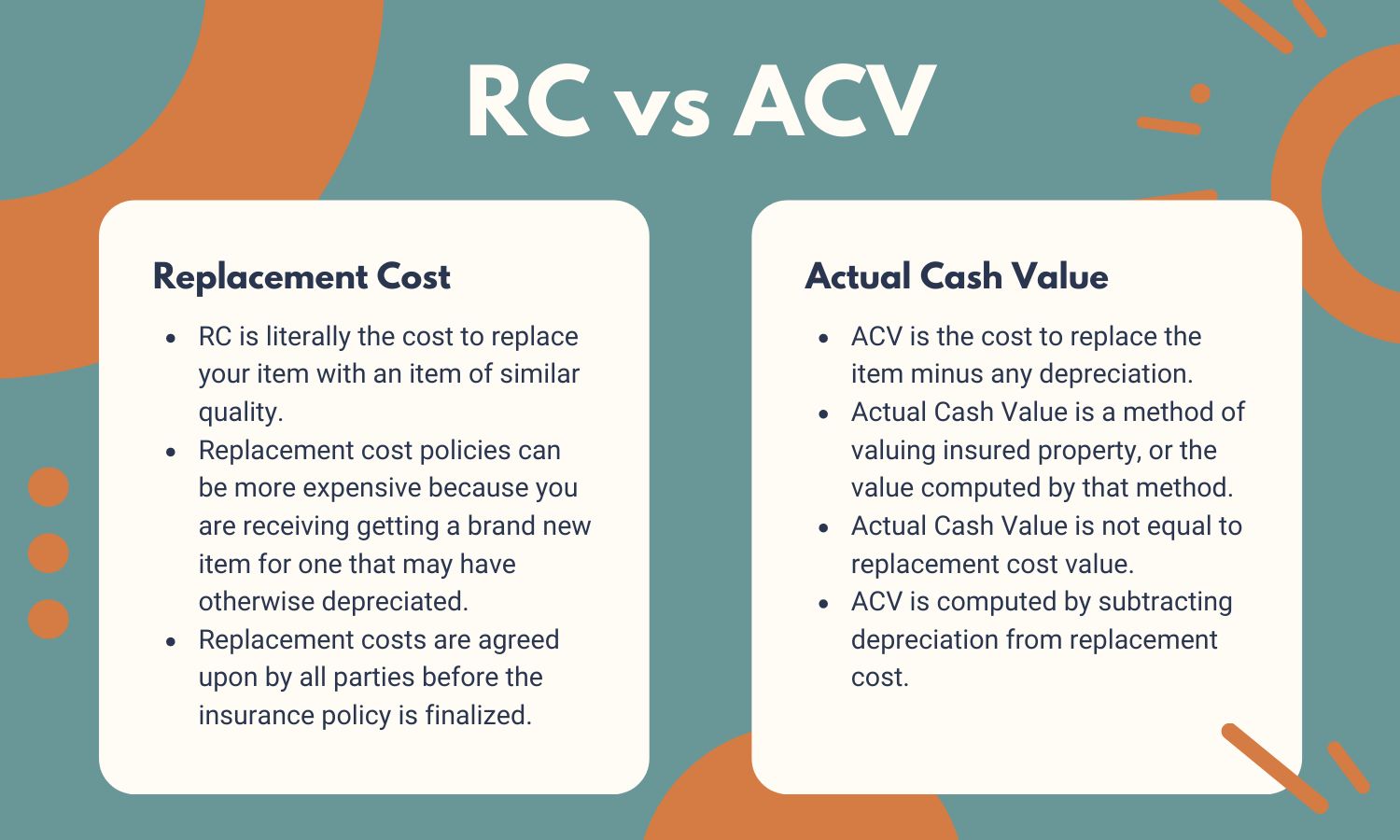

RCV vs. ACV

When it comes to insurance claims, understanding the difference between Replacement Cost Value (RCV) and Actual Cash Value (ACV) is crucial. These terms represent two different methods of calculating the value of damaged property and determining the amount of compensation policyholders will receive.

RCV, as we have discussed, represents the cost of replacing or reproducing the damaged property with a comparable new item of similar kind and quality. It does not factor in depreciation and focuses on the current market value of the replacement item at the time of the loss.

On the other hand, ACV, or Actual Cash Value, considers the depreciation and age of the damaged property at the time of the loss. It takes into account the original cost of the item, its useful life, and any wear and tear it has experienced over time. The ACV is calculated by subtracting the depreciation from the replacement cost value.

Let’s take an example to illustrate the difference between RCV and ACV. Say you have a five-year-old laptop that gets damaged beyond repair. The RCV of the laptop would be the cost of buying a brand-new laptop with similar specifications. However, the ACV would take into account the depreciation of the laptop over five years and provide compensation based on its current value.

It’s important to note that insurance policies can vary in their coverage terms and may offer either RCV or ACV for different types of property. Some policies may provide RCV coverage for certain items, such as the structure of a building, while offering ACV coverage for personal belongings. Reviewing your insurance policy can clarify which valuation method is used for different types of assets.

The choice between RCV and ACV coverage can impact the payout you receive in an insurance claim. RCV coverage typically offers a higher payout because it does not consider depreciation, allowing policyholders to replace or repair their damaged property with new items without incurring additional costs.

However, it’s important to note that some policies may initially pay out the ACV and then reimburse the policyholder for the difference between ACV and RCV once repairs or replacements are complete. Understanding the terms and provisions of your insurance policy is crucial to know what coverage you have and what to expect in a claim.

Now that we have clarified the distinction between RCV and ACV, let’s explore how RCV impacts insurance claims and the factors to consider when calculating the RCV in specific scenarios.

How RCV Impacts Insurance Claims

The Replacement Cost Value (RCV) is a vital factor that influences insurance claims and plays a significant role in determining the compensation policyholders receive for their losses. RCV impacts insurance claims in several ways:

Accurate compensation: RCV ensures that policyholders receive accurate compensation for their damaged property. By considering the current market value of materials, labor costs, and associated expenses, the insurance company can provide the funds necessary to repair or replace the damaged property without placing an excessive financial burden on the policyholder.

Full restoration of property: RCV allows for the full restoration of the damaged property to its pre-loss condition. Policyholders are reimbursed based on the cost of replacing or reproducing the property with a new item of similar kind and quality. This ensures that policyholders can genuinely restore their property and not settle for diminished value or compromised repairs.

Protection against underinsurance: RCV helps protect policyholders against underinsurance. Underinsurance occurs when the coverage limits of an insurance policy do not adequately reflect the true value of the insured property. RCV calculations ensure that policyholders receive sufficient compensation to fully repair or replace their damaged property, preventing financial strain and potential gaps in coverage.

Prioritizing quality: RCV encourages insurance companies and policyholders to prioritize quality when repairing or replacing damaged property. Since RCV focuses on the cost of replacing with similar kind and quality items, it incentivizes policyholders to seek reputable contractors and use higher-quality materials. This helps to maintain the value and integrity of the property in the long run.

Consideration of specific endorsements: Some insurance policies may have specific endorsements that impact RCV calculations in certain scenarios. For example, there might be additional coverage options for specialized equipment or collections that require specific considerations when determining the RCV. Reviewing your policy and understanding any applicable endorsements is crucial to ensure accurate compensation.

When filing an insurance claim, it’s important to provide accurate documentation and evidence to support the RCV calculation. This may include estimates from contractors, receipts for materials, and any other relevant information that substantiates the cost of repairing or replacing the damaged property.

It’s worth noting that insurance policies may have limitations or exclusions that impact the RCV calculation for specific types of property or damages. Familiarize yourself with the terms and provisions of your insurance policy to understand how RCV applies in different scenarios.

Now that we understand the impact of RCV in insurance claims, let’s explore some examples of how RCV is calculated for different types of property damage.

Examples of RCV Calculation

Calculation of the Replacement Cost Value (RCV) in insurance claims involves considering various factors such as labor costs, materials, and associated expenses. Let’s explore a few examples of how RCV can be calculated for different types of property damage:

Example 1: Home Structure

In the event of a fire damaging your home, the RCV calculation would involve assessing the cost of rebuilding the structure. This includes materials such as roofing, siding, flooring, and windows, as well as labor costs. The insurance adjuster would consider the square footage of the home, the complexity of the design, and regional construction rates to come up with an accurate RCV estimate.

Example 2: Personal Belongings

In the case of damage to personal belongings, such as furniture, electronics, or clothing, the RCV calculation would involve determining the cost of replacing each item. The insurance company may consider the brand, model, and current market prices of comparable items to arrive at the RCV. It’s important to provide accurate documentation, such as receipts or estimates from retailers, to support the RCV calculation for personal belongings.

Example 3: Automobile

For damage to a vehicle, the RCV calculation considers factors such as the make, model, year, and condition of the car. The insurance adjuster or appraiser will assess the cost of repairing the damage or replacing the vehicle with a similar one. They may also consider factors like mileage, accessories, and any applicable depreciation to determine the RCV.

Example 4: Specialty Items

Specialty items, such as artwork, antiques, or collectibles, require careful consideration when calculating the RCV. Insurance companies may request appraisals from qualified experts to determine the current market value and cost of replacing these items. Factors such as rarity, condition, and demand within the market are taken into account to arrive at an accurate RCV.

It’s important to remember that each insurance claim is unique, and the RCV calculation may vary depending on the specific circumstances and terms of your policy. Working with a qualified insurance adjuster or appraiser is crucial to ensure an accurate RCV calculation for your specific claim.

By understanding how RCV is calculated for different types of property damage, you can be better prepared to provide the necessary documentation and evidence to support your claim and ensure a fair and accurate reimbursement for your losses.

Now, let’s explore some common issues and challenges that policyholders may encounter when dealing with RCV claims.

Common Issues and Challenges with RCV Claims

While Replacement Cost Value (RCV) is an important concept in insurance claims, there can be various issues and challenges that policyholders may encounter during the claims process. It’s essential to be aware of these potential hurdles to navigate them effectively. Here are some common issues and challenges with RCV claims:

Policy Coverage Limits: One challenge is ensuring that the RCV of the damaged property falls within the coverage limits of your insurance policy. If the RCV exceeds the limits, you may face a coverage gap and be responsible for the additional costs out of pocket. Review your policy carefully and consider obtaining additional coverage if necessary.

Disagreements on RCV Calculation: There may be disagreements between policyholders and insurance companies regarding the RCV calculation. These disagreements can arise from differences in assessing the cost of materials, labor, or the choice of comparable replacements. It’s crucial to provide accurate documentation and evidence to support your RCV calculation and be prepared to negotiate with the insurance company if necessary.

Depreciation Disputes: In some cases, there may be disputes about the depreciation value applied to the damaged property. Insurance companies may try to reduce the RCV by applying higher depreciation rates than what is deemed fair. It’s important to understand the depreciation calculations and challenge any unjustified reductions by providing evidence of the property’s actual condition and value.

Scope of Repairs or Replacements: Determining the scope of repairs or replacements needed to restore the damaged property can be complex. Insurance adjusters may have different opinions on what is necessary to bring the property back to its pre-loss condition. It’s essential to document the damage thoroughly and consider obtaining multiple professional opinions to support your assessment of the required scope of work.

Delayed Claims Process: RCV claims can sometimes involve a more extended claims process due to the need for detailed assessments and calculations. This can cause delays in receiving the necessary funds for repairs or replacements. Staying in regular communication with the insurance company, providing requested documentation promptly, and following up on the progress of your claim can help expedite the process.

Insurance Policy Limitations and Exclusions: Insurance policies often have limitations and exclusions that may impact the RCV calculation. Certain types of property, damages resulting from specific perils, or policy endorsements may have specific provisions that affect the coverage. Review your policy carefully to understand any limitations or exclusions that could impact your RCV claim.

Inadequate Documentation: Insufficient or incomplete documentation can pose challenges during the RCV claims process. It’s crucial to thoroughly document the damage with photographs, gather receipts, estimates, and any other relevant information to support your claim. Detailed documentation will help substantiate the RCV calculation and enhance the likelihood of a fair and timely settlement.

By being aware of these common issues and challenges, you can be better prepared to navigate the RCV claims process. Working closely with your insurance company, providing accurate documentation, and seeking professional assistance when needed can help overcome these challenges and ensure a fair and satisfactory resolution to your RCV claim.

Now, let’s discuss some tips for successfully navigating RCV claims.

Tips for Navigating RCV Claims Successfully

Navigating Replacement Cost Value (RCV) claims can be a complex process. However, with careful planning and preparation, you can increase the likelihood of a successful and satisfactory outcome. Here are some tips to help you navigate RCV claims successfully:

1. Understand your policy: Familiarize yourself with the terms and conditions of your insurance policy, especially those related to RCV coverage. Know the coverage limits, limitations, and exclusions that may apply to your specific claim. This will help you understand your rights and what to expect during the claims process.

2. Document the damage: Thoroughly document the damage to your property with photographs or videos. This visual evidence will support your claim and provide a clear picture of the extent of the damage. Ensure that all relevant details are captured in the documentation.

3. Keep records: Maintain a comprehensive record of all communication, including emails, letters, and phone conversations with your insurance company, adjuster, and contractors. This documentation will serve as evidence of your interactions and any agreements made throughout the claims process.

4. Obtain multiple estimates: When seeking repair or replacement estimates, obtain multiple quotes from reputable contractors. This will help you understand the range of costs involved and ensure that you receive fair and competitive pricing. Be sure the estimates include the necessary scope of work to restore your property to its pre-loss condition.

5. Work with professionals: Engage with qualified professionals, such as public adjusters or contractors, who have experience in handling insurance claims. They can provide guidance, assess the damages, and assist with the RCV calculation. Their expertise can help ensure that you receive the appropriate compensation for your property loss.

6. Provide accurate documentation: Provide the insurance company with accurate and detailed documentation to support your RCV claim. This includes receipts, invoices, estimates, and any other relevant information that verifies the costs of repairing or replacing your damaged property.

7. Communicate with your insurance company: Keep lines of communication open with your insurance company throughout the claims process. Respond promptly to any requests for additional information or documentation. Regularly follow up on the status of your claim and maintain a record of all communication.

8. Consider professional reviews: If you encounter disputes or challenges during the claims process, consider seeking professional reviews or examinations. Independent appraisers or contractors can provide unbiased assessments of the damages and their associated costs, helping to resolve disagreements and ensure a fair resolution.

9. Be persistent: Insurance claims can sometimes be lengthy and require persistence. Be patient but persistent in pursuing your claim. Advocate for your rights and diligently follow up on the progress of your claim until a satisfactory resolution is reached.

10. Seek legal advice if necessary: If you encounter significant obstacles or disputes with your insurance company regarding your RCV claim, it may be advisable to seek legal advice. An attorney with experience in insurance claims can provide guidance and represent your interests to ensure a fair outcome.

By following these tips, you can navigate RCV claims more effectively and increase your chances of a successful outcome. Remember to stay organized, maintain thorough documentation, and seek professional assistance when needed to ensure a fair resolution to your insurance claim.

Now, let’s conclude our discussion on RCV claims.

Conclusion

Understanding the concept of Replacement Cost Value (RCV) and its importance in insurance claims is essential for policyholders and insurance professionals. RCV plays a significant role in accurately assessing the value of damaged property and determining the compensation policyholders receive to repair or replace their assets.

In this article, we explored the definition of RCV and its significance in insurance claims. We discussed how RCV ensures that policyholders receive fair compensation and are able to fully restore their damaged property. We also examined the factors that can affect the calculation of RCV, such as materials and labor costs, building codes, and the complexity of the project.

Additionally, we compared RCV to Actual Cash Value (ACV) and highlighted the differences between the two valuation methods. While RCV focuses on the cost of replacing property without factoring in depreciation, ACV takes into account the age and wear and tear of the damaged item.

We explored how RCV impacts insurance claims, including the accurate compensation it provides, the protection it offers against underinsurance, and the emphasis it places on quality restoration. We also discussed common issues and challenges that policyholders may face when dealing with RCV claims, such as policy limitations, disputes over calculations, and delays in the claims process.

To navigate RCV claims successfully, we provided several tips, including understanding your policy, documenting the damage, maintaining records of communication, obtaining multiple estimates, and working with professionals. We emphasized the importance of accurate documentation, effective communication with the insurance company, and persistence in pursuing a fair resolution for your claim.

In conclusion, RCV is a critical component of insurance claims, helping policyholders receive fair compensation and restore their damaged property. By understanding the intricacies of RCV, being prepared, and following the tips provided, policyholders can navigate the claims process with greater confidence and maximize their chances of achieving a satisfactory outcome.

Remember, each insurance claim is unique, and it is crucial to review your specific insurance policy and consult with professionals when necessary. By doing so, you can ensure that you are properly informed and equipped to handle RCV claims successfully.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance