Home>Finance>What Information Do You Need To Get Car Insurance?

Finance

What Information Do You Need To Get Car Insurance?

Published: November 19, 2023

Looking for car insurance? Find out what information you need to provide to get a quote today. Get the coverage you need to protect your vehicle and your finances.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Car insurance is an essential component of responsible car ownership. It not only provides financial protection in case of an accident or theft but is often required by law in many countries. When purchasing car insurance, there is certain information that you will need to provide to insurance providers to obtain a quote and secure coverage. This information is crucial in determining the appropriate premiums, coverage limits, and deductibles.

Understanding what information you need to gather beforehand can help streamline the process and ensure you receive accurate quotes tailored to your specific needs. In this article, we will discuss the key pieces of information that you will typically need when getting car insurance.

It’s worth noting that specific requirements may vary depending on the insurance provider and the country or state you reside in. However, the following sections provide a general overview of the personal and vehicle details, driving history, insurance history, and desired coverage information that insurers typically require.

By having this information readily available, you can save time and ensure a smoother insurance application process.

Personal Information

When applying for car insurance, you will need to provide personal information to the insurance provider. This information helps insurers assess your risk profile and determine the appropriate premiums for your policy. Here are the key personal details typically required:

- Name: Provide your full legal name as it appears on your identification documents.

- Date of Birth: Insurance providers use your date of birth to verify your age, as it can impact your risk level.

- Address: Your current residential address is essential for determining factors such as crime rates and accident statistics in your area, which can influence your premiums.

- Phone Number and Email Address: Insurers need to be able to contact you regarding your policy, claims, and other important updates.

- Occupation: Certain occupations may be associated with different risk levels, and insurers may consider this when determining your premiums.

- Marital Status: Some insurance companies take into account marital status when calculating premiums, as statistics show that married individuals tend to have lower accident rates.

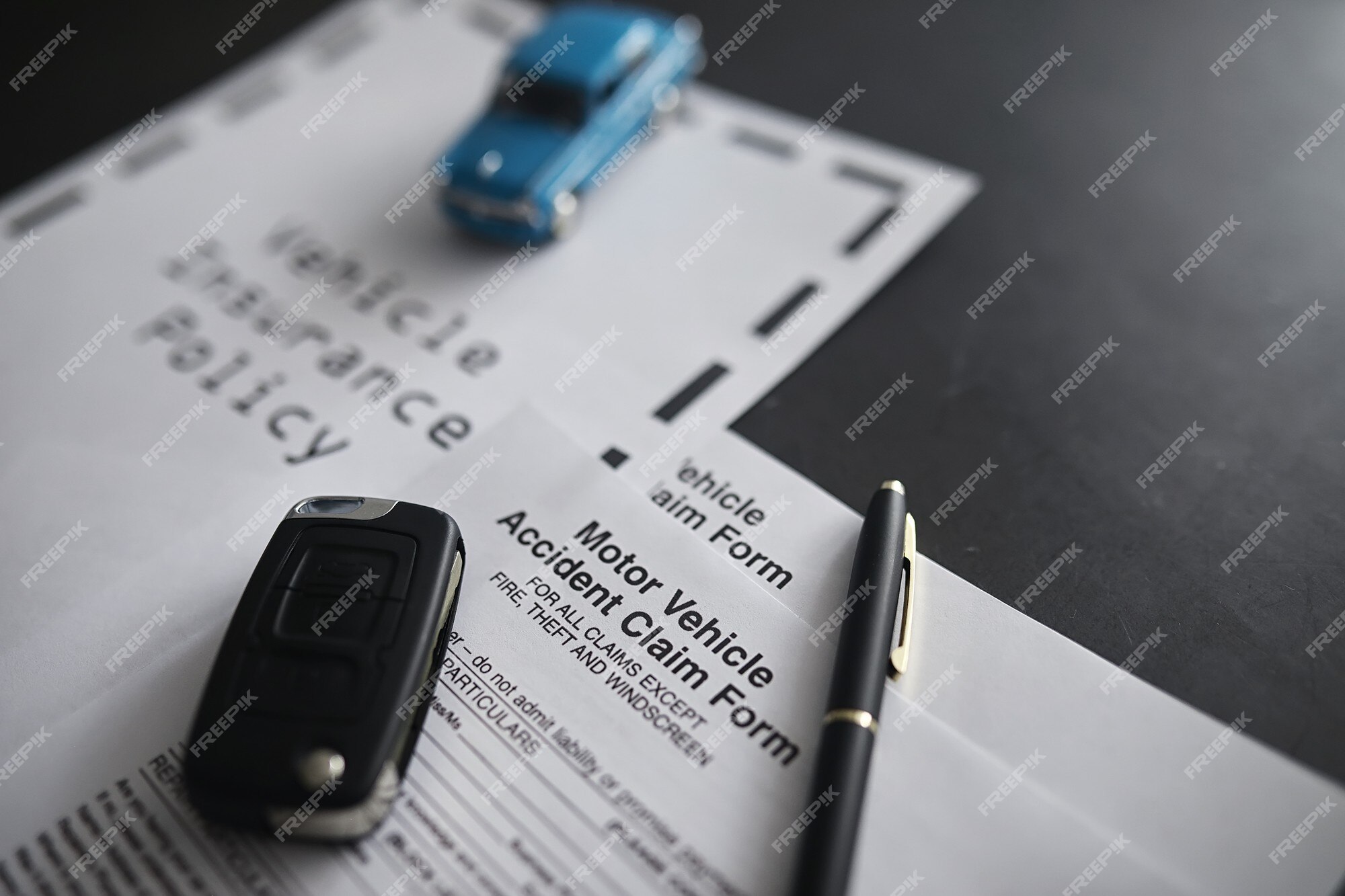

- Driver’s License Information: You will need to provide your driver’s license number, issue date, and expiration date. Insurers use this information to verify your driving history.

It’s important to provide accurate personal information to avoid any potential issues in the future. Any inaccuracies or omissions in your information could result in voiding your policy or difficulties in filing claims.

Remember, your personal information should be protected and handled securely by insurance providers. Ensure that you are sharing your information with reputable and trusted companies.

Vehicle Details

When obtaining car insurance, providing accurate and detailed information about your vehicle is crucial. Insurance companies consider various factors related to your vehicle to determine premiums and coverage options. Here are the key details you will need to provide:

- Make and Model: The make and model of your vehicle help insurers assess its value, safety features, and repair costs.

- Year: The manufacturing year of your vehicle provides insurers with important information regarding its age and depreciation.

- VIN Number: The Vehicle Identification Number (VIN) is a unique identification code for your vehicle. It helps insurers verify the vehicle’s history, such as accident records and previous insurance claims.

- Usage: You will need to specify how you primarily use your vehicle, such as for commuting, pleasure, or business purposes. This information can impact your premiums.

- Mileage: Insurers may ask for the estimated annual mileage of your vehicle, as higher mileage can increase the risk of accidents and potential claims.

- Modifications: If you have made any modifications to your vehicle, such as installing custom parts or adding performance enhancements, it’s important to disclose this information as it may affect your coverage and premiums.

- Ownership: You will need to specify if you own the vehicle outright or if it is leased or financed. This information can impact the coverage options available to you.

Providing accurate vehicle details ensures that you receive an accurate quote and appropriate coverage for your specific car. Any inaccuracies or omissions can potentially result in coverage gaps or claim denials in the event of an accident or incident.

Additionally, keep in mind that insurance premiums can vary based on the type of vehicle you own. Sports cars, luxury vehicles, and SUVs may have higher premiums due to their higher value, increased risk of theft, or higher repair costs.

Driving History

Your driving history plays a significant role in determining your car insurance premiums. Insurance providers assess your past driving behavior as an indicator of your risk level. When obtaining car insurance, you will need to provide details about your driving history, including:

- License Details: Insurance companies typically ask for your driver’s license number, issue date, and any license restrictions or endorsements.

- Accidents and Claims: You will be required to disclose any previous accidents or claims you have made. This includes at-fault accidents, comprehensive claims, and any traffic violations that resulted in fines or points on your driving record.

- Traffic Violations: Insurance providers may ask about any traffic violations or citations you have received, such as speeding tickets, DUI/DWI convictions, or reckless driving.

- Driver Training Courses: Some insurers offer discounts for completing driver training courses or defensive driving courses. You may need to provide proof of completion to qualify for these discounts.

Being transparent about your driving history is vital, as any discrepancies or false information can have serious consequences. Insurance companies have access to driving records and can verify the accuracy of the information you provide.

Remember, having a clean driving history with no accidents or violations can lead to lower insurance premiums. On the other hand, a history of accidents or traffic violations may result in higher premiums due to the perceived higher risk.

It’s important to note that each insurance provider has its own criteria and rules regarding how they assess driving history. Some companies may overlook certain minor violations or accidents, while others may consider them more heavily in determining your premiums.

Always be honest about your driving history and ensure you provide accurate information to avoid any issues when filing claims or renewing your policy in the future.

Insurance History

Your insurance history provides valuable insights to insurance providers about your past coverage and claims experience. When applying for car insurance, you will typically be asked to provide information about your previous insurance policies, including:

- Current Insurance Policy: If you already have car insurance, you will need to provide details of your current policy, including the insurance company, coverage limits, and expiration date.

- Prior Insurance Coverage: You may also need to disclose information about previous insurance policies you had in the past, even if they are no longer active. This includes the insurance company name, coverage details, and any gaps in coverage.

- Claims History: Insurance providers typically ask about any claims you have made in the past few years. This includes at-fault accidents, comprehensive claims, and claims related to theft, vandalism, or natural disasters.

- Loss Ratio: Insurance companies may inquire about your loss ratio, which is the ratio of claims paid out by the insurance company in relation to the premiums paid. This information helps insurers evaluate your risk profile.

- Cancelled or Non-Renewed Policies: You will need to disclose if you have ever had a car insurance policy cancelled or non-renewed by an insurance company. This information may impact your eligibility for coverage or premiums.

Insurance companies use this information to assess your risk level and determine premiums. Any gaps in coverage or a history of frequent claims may lead to higher premiums or limitations on coverage options.

Additionally, if you have had continuous car insurance coverage with no lapses, you may be eligible for certain discounts or lower premium rates. Insurance providers often reward responsible individuals who have maintained consistent coverage.

It’s important to provide accurate and complete information about your insurance history to ensure a smooth application process and to avoid any issues when filing claims in the future.

Desired Coverage

When obtaining car insurance, it’s important to understand the different types of coverage available and select the appropriate level of coverage based on your needs and preferences. Here are the key points to consider when determining your desired coverage:

- Liability Coverage: Liability coverage is a basic requirement in most jurisdictions. It covers bodily injury and property damage to others in the event you are at fault in an accident.

- Collision Coverage: Collision coverage helps pay for repairs or replacement of your vehicle if it is damaged in a collision with another vehicle or object.

- Comprehensive Coverage: Comprehensive coverage protects your vehicle against non-collision incidents such as theft, vandalism, natural disasters, and falling objects.

- Uninsured/Underinsured Motorist Coverage: This coverage provides protection if you are involved in an accident with a driver who doesn’t have insurance or does not have enough coverage to fully compensate you for damages.

- Medical Payments Coverage: Medical payments coverage, also known as personal injury protection, covers medical expenses for you and your passengers in the event of an accident, regardless of who is at fault.

- Rental Car Coverage: If you rely on a rental car while your vehicle is being repaired after an accident or event, rental car coverage can help cover the cost of the rental.

- Additional Coverage Options: Depending on your needs, you may consider additional coverage options such as roadside assistance, gap coverage, or new car replacement coverage.

Consider your budget, the value of your vehicle, and your personal circumstances when selecting coverage options. It’s important to strike a balance between adequate coverage and affordability.

Working with an experienced insurance agent can help you understand your options and select the right coverage for your needs. They can also provide guidance on coverage limits and deductibles based on your risk tolerance.

Remember that insurance requirements and options may vary by country, state, and insurance provider. It’s important to familiarize yourself with the specific requirements and regulations in your area.

Additional Information

In addition to the core details mentioned above, there are a few additional pieces of information that insurance providers may ask for when obtaining car insurance. While these details may not directly impact your premiums, they can help insurers assess your eligibility for certain discounts or additional coverage options. Some common additional information includes:

- Annual Mileage: Insurance companies may ask for your estimated annual mileage to assess your vehicle usage and determine risk factors associated with higher mileage.

- Anti-Theft Devices: If your vehicle is equipped with security features such as alarm systems, tracking devices, or immobilizers, providing this information can result in potential discounts on your premiums.

- Garaging Address: If your vehicle is primarily stored at a different address than your residential address, insurers may ask for the specific location where your car is garaged.

- Primary Driver: Insurance providers will want to know who the primary driver of the vehicle will be. This information helps insurers assess risk based on the individual’s driving history and habits.

- Membership Affiliations: Some insurance companies offer discounts to individuals who are members of certain organizations or associations. You may be asked if you belong to any such groups.

- Payment Preferences: Insurance providers usually ask for your preferred payment method, whether it’s through monthly installments, annual payments, or electronic funds transfer.

It’s important to provide accurate and up-to-date information when supplying these additional details. Any inconsistencies or omissions may impact your eligibility for discounts or additional coverage options.

Beyond the required information, it’s also essential to communicate any specific concerns or needs to your insurance provider. If you have unique circumstances, such as a high-risk occupation or a history of auto insurance claims, make sure to discuss these factors with your insurer to ensure your policy adequately addresses your situation.

Remember, the more transparent and comprehensive you are in providing information, the more accurate and tailored your car insurance coverage will be.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance