Finance

What Is Insurance In Black Jack?

Modified: February 21, 2024

Learn how insurance works in blackjack and its impact on your finances. Discover the role of insurance in this popular card game and make informed financial decisions.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to the world of blackjack, where the thrill of the game and the potential for big wins keep players coming back for more. But amidst the excitement, there’s one term that often gets tossed around: insurance. If you’re new to the game or just looking to understand this concept better, you’ve come to the right place.

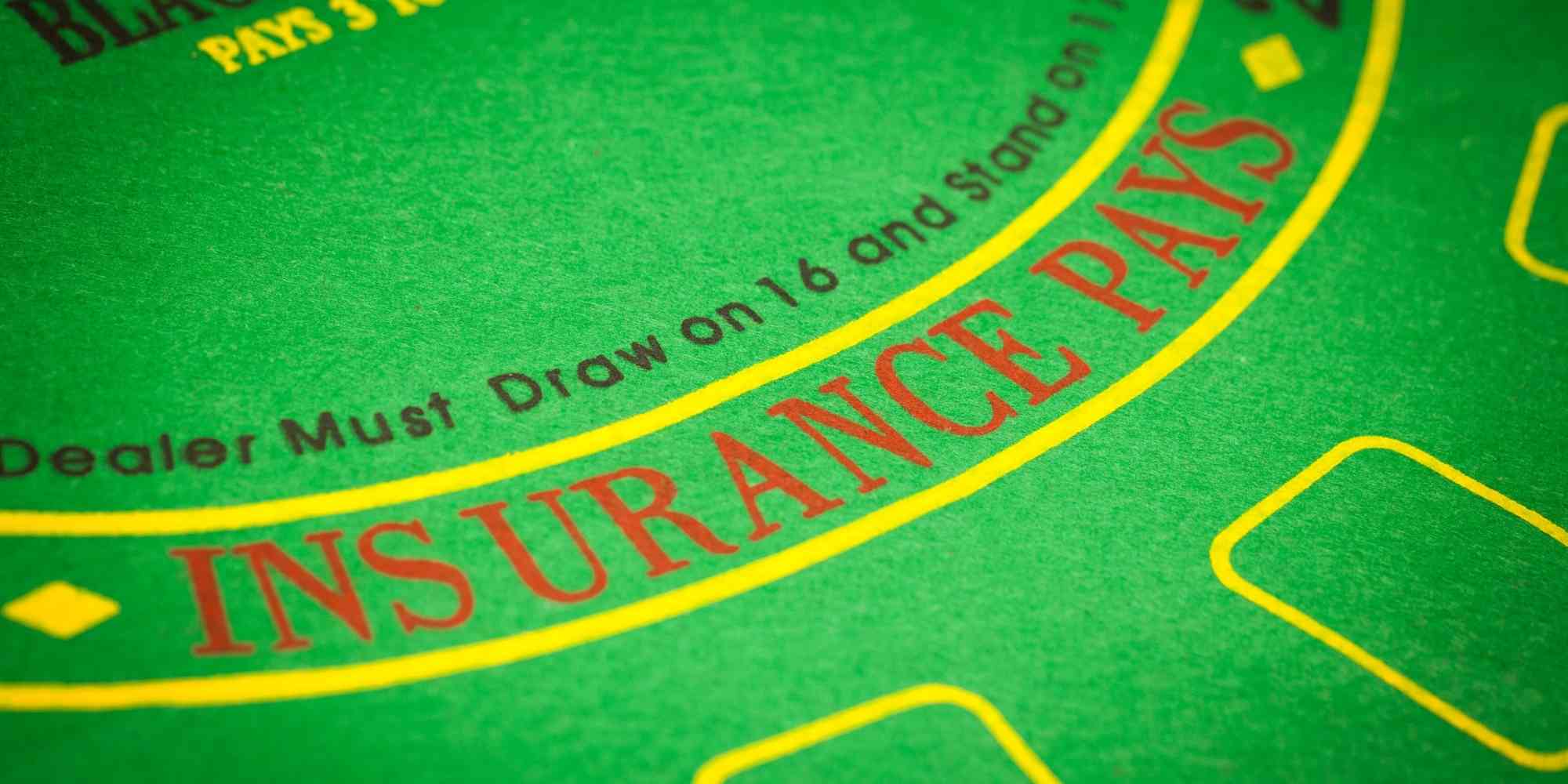

In simple terms, insurance in blackjack is a side bet that players have the option to take when the dealer’s upcard is an Ace. It’s a way for players to protect themselves against the possibility that the dealer has a blackjack, which pays out at 3:2 odds. While insurance may seem like a tempting offer, it’s important to understand how it works and its implications before deciding whether to take it or not.

In this article, we’ll explore the concept of insurance in blackjack in depth, discussing how it works, its pros and cons, common misconceptions, and tips for making informed decisions about whether to take insurance or not. Whether you’re a seasoned player or a blackjack novice, gaining a clear understanding of this aspect of the game can help you navigate the tables with confidence.

So, let’s dive into the world of insurance in blackjack and unravel its secrets. Strap in and get ready to level up your knowledge as we explore this intriguing aspect of the game.

What is Insurance?

Before delving into the specifics of insurance in blackjack, let’s start by understanding what insurance means in a general sense. In various contexts, insurance is a way to protect against potential financial losses or liabilities. It provides a safety net, ensuring that individuals or businesses are financially protected if certain events occur.

In the case of blackjack, insurance operates on a similar principle. When the dealer’s upcard is an Ace, players have the option to take insurance as a side bet. The purpose of this bet is to protect against the possibility that the dealer has a blackjack, also known as a natural. To take insurance, players must place an additional bet equal to half of their original wager.

If the dealer indeed has a blackjack, the insurance bet pays out at 2:1 odds, effectively mitigating the player’s losses from the original wager. However, if the dealer does not have a blackjack, the insurance bet is lost, and the game proceeds as usual.

It’s important to note that insurance is an independent bet separate from the player’s main hand. Regardless of whether the player’s hand wins or loses, the outcome of the insurance bet is determined solely by the dealer’s upcard.

While the idea of protecting oneself against the dealer’s potential blackjack may seem appealing, it’s crucial to understand the mechanics and implications of taking insurance before making a decision. In the next section, we’ll explore how insurance works in blackjack and what factors players should consider when deciding whether or not to take it.

How Does Insurance Work in Blackjack?

Once the dealer’s upcard is revealed to be an Ace, players are given the option to take insurance. To do so, they must place an additional bet equal to half of their original wager. This insurance bet is then placed in a separate area of the blackjack table.

If the dealer does indeed have a blackjack (a total of 21 on their initial two cards), the insurance bet pays out at 2:1 odds. This means that if a player has a $10 original wager and takes insurance, they would need to place an additional $5 as the insurance bet. If the dealer has a blackjack, the player would receive $10 as a payout for the insurance bet, effectively canceling out the loss on their original $10 wager.

However, if the dealer does not have a blackjack, the insurance bet is lost, and the player’s original wager is still in play. If the player’s hand wins against the dealer’s non-blackjack hand, they are paid out at the usual 1:1 odds. If the player’s hand loses to the dealer’s non-blackjack hand, the original wager is collected by the dealer.

It’s important to remember that insurance is an optional side bet that players can choose to take or decline. Some players might opt to take insurance every time they are offered, hoping to protect themselves against potential losses. However, others might choose to never take insurance, deeming it a less favorable bet in the long run.

The decision to take insurance should be based on a strategic understanding of the odds and probabilities involved. In the next section, we’ll explore the pros and cons of taking insurance in blackjack to help players make informed decisions at the tables.

The Pros and Cons of Taking Insurance

When it comes to taking insurance in blackjack, there are both advantages and disadvantages that players should consider before making a decision. Let’s explore the pros and cons of taking insurance:

The Pros:

- Protection against Dealer Blackjack: Taking insurance can provide a safeguard against the possibility of the dealer having a blackjack. If the dealer does have a blackjack, the insurance bet pays out at 2:1 odds, effectively canceling out the loss on the player’s original wager.

- Perceived Security: For some players, taking insurance offers a sense of security and peace of mind, knowing that they have mitigated potential losses in case the dealer does have a blackjack.

The Cons:

- Negative Expected Value: From a strategic standpoint, the insurance bet has a negative expected value. Over time, taking insurance will result in a loss of money in the long run. This is because the 2:1 payout does not compensate for the likelihood of the dealer not having a blackjack.

- Increased House Edge: By taking insurance, players effectively increase the house edge in the game. Since the insurance bet is statistically unfavorable, choosing to take it regularly will erode potential profits.

- Complicates Strategy: Taking insurance introduces an additional decision point in the game, potentially distracting players from optimal blackjack strategy. Getting caught up in the insurance bet can lead to a deviation from basic strategy and a decrease in overall profitability.

Considering these pros and cons, it’s clear that the decision to take insurance in blackjack is not a simple one. It ultimately depends on the player’s risk tolerance, their understanding of the game’s probabilities, and their overall blackjack strategy. In the following section, we’ll address some common misconceptions about insurance in blackjack.

Common Misconceptions about Insurance in Blackjack

Insurance in blackjack is often surrounded by misconceptions and misunderstandings. Let’s address some of the most common misconceptions:

Misconception 1: Insurance Protects Against Losses on the Player’s Hand

One of the misconceptions about insurance is that it protects the player’s hand from losses. In reality, insurance is a separate bet that only covers the possibility of the dealer having a blackjack. It has no impact on the outcome of the player’s hand.

Misconception 2: Taking Insurance is Always a Good Idea

Some players believe that taking insurance is a safe and profitable move, regardless of the circumstances. However, as mentioned earlier, the insurance bet has a negative expected value in the long run. So, while it may offer short-term protection, consistently taking insurance will erode potential profits.

Misconception 3: Insurance Increases Chances of Winning

Another misconception is that taking insurance increases the player’s chances of winning. In reality, insurance has no impact on the player’s hand. The odds of winning or losing on the player’s hand remain the same, regardless of whether insurance is taken or not.

Misconception 4: Insurance is a Form of Card Counting

Some players mistakenly associate insurance with card counting, a strategy used to gain an advantage over the casino. However, card counting and taking insurance are unrelated. Card counting involves keeping track of the high and low-value cards remaining in the deck, while insurance is a separate side bet option.

Understanding these common misconceptions can help players make more informed decisions at the blackjack table. It’s essential to base your choices on a clear understanding of the mechanics and probabilities involved rather than relying on myths and misunderstandings.

Tips for Making Informed Decisions about Insurance

When it comes to deciding whether to take insurance in blackjack, it’s crucial to approach the decision with a strategic mindset. Here are some tips to help you make informed decisions:

1. Understand the Odds:

Take the time to familiarize yourself with the probabilities involved in taking insurance. Understand that the insurance bet has a negative expected value in the long run, meaning it will result in a loss over time. Knowing the odds can help you make a more informed decision based on logic rather than emotions.

2. Stick to a Strategy:

Develop and adhere to a solid blackjack strategy. Focus on playing basic strategy and making decisions based on the value of your hand and the dealer’s upcard. Deviating from a sound strategy to chase insurance bets can lead to suboptimal outcomes.

3. Consider Your Bankroll:

Assess your bankroll and consider how much you’re willing to risk on insurance bets. If taking insurance fits within your overall budget and risk tolerance, it can be an occasional option. However, be mindful of the potential negative impact on your bankroll over time.

4. Pay Attention to Blackjack Variations:

Note that some variations of blackjack do not offer insurance as an option. If you find yourself playing a variation without the insurance bet, adjust your strategy accordingly and focus on playing your hand rather than worrying about insurance.

5. Practice and Learn:

Improve your blackjack skills through practice and study. The more you familiarize yourself with the game, its strategies, and probabilities, the better equipped you’ll be to make educated decisions at the table.

By following these tips, you can approach the decision of whether to take insurance in blackjack with a clear understanding and a strategic mindset. Remember that ultimately, it’s your choice whether to take insurance or not, and making an informed decision is key to maximizing your chances of success in the game.

Conclusion

Insurance in blackjack is a concept that can be both enticing and misunderstood. While it may offer a sense of protection against the dealer’s potential blackjack, it’s important to approach the decision to take insurance with a clear understanding of the odds and probabilities involved.

Throughout this article, we’ve explored the fundamentals of insurance in blackjack, how it works, and its pros and cons. We’ve debunked common misconceptions and provided tips for making informed decisions at the tables.

Ultimately, whether to take insurance or not is a personal choice that should align with your own blackjack strategy and risk tolerance. It’s essential to consider the negative expected value of the insurance bet and the potential impact on your overall profitability in the long run.

Remember to focus on playing basic blackjack strategy, understanding the odds, and managing your bankroll effectively. By doing so, you can make well-informed decisions that optimize your chances of success in the game.

So, the next time you encounter the option of insurance in blackjack, weigh the pros and cons, trust your knowledge of the game, and make a decision that aligns with your goals and strategies. Stay confident, keep refining your skills, and may luck be on your side as you navigate the thrilling world of blackjack.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance