Home>Finance>What Is The Average Cost Of Car Insurance For A 21-Year-Old Male?

Finance

What Is The Average Cost Of Car Insurance For A 21-Year-Old Male?

Published: November 14, 2023

Looking for the average cost of car insurance for a 21-year-old male? Get insights on finance and find out what to expect for your insurance premiums.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Car insurance is a crucial aspect of responsible vehicle ownership. It provides financial protection in the event of accidents, theft, or damage to your car. However, the cost of car insurance can vary significantly depending on several factors, including your age, gender, driving record, and the type of car you drive. For 21-year-old males, finding affordable car insurance can often be a challenge.

Young drivers, especially males, are statistically more likely to be involved in accidents than older, more experienced drivers. Insurance companies take this into consideration when determining premiums, resulting in higher rates for this demographic. Understanding the average cost of car insurance for a 21-year-old male can help you plan and budget accordingly.

In this article, we will explore the various factors that affect car insurance rates and delve into the average cost of car insurance for 21-year-old males. Additionally, we will provide some valuable tips on how to lower your car insurance premiums without compromising on coverage.

Factors Affecting Car Insurance Rates

When it comes to determining car insurance rates for 21-year-old males, several key factors come into play. Insurance companies consider these factors to assess the level of risk associated with insuring an individual. Understanding these factors can help you comprehend why your car insurance premiums may be higher than expected:

- Age and Gender: Younger drivers, especially males, are statistically considered more prone to reckless driving and accidents, resulting in higher insurance rates compared to older, more experienced drivers. The lack of driving experience increases the perceived risk for insurance providers.

- Driving Record: A clean driving record with no tickets or accidents demonstrates responsible driving behavior and will likely result in lower insurance premiums. On the other hand, a history of speeding tickets or accidents may lead to higher rates due to the increased perceived risk.

- Type of Vehicle: The make and model of your car impact insurance rates. Generally, sports cars and luxury vehicles are more expensive to insure due to the higher cost of repairs and likelihood of theft.

- Location: Insurance rates can vary based on your location. If you live in an area with high crime rates or a high number of accidents, you may be charged higher premiums.

- Coverage and Deductibles: The extent of coverage you select and the deductible amount you choose will influence the cost of your insurance premiums. Higher coverage limits and lower deductibles typically result in higher premiums.

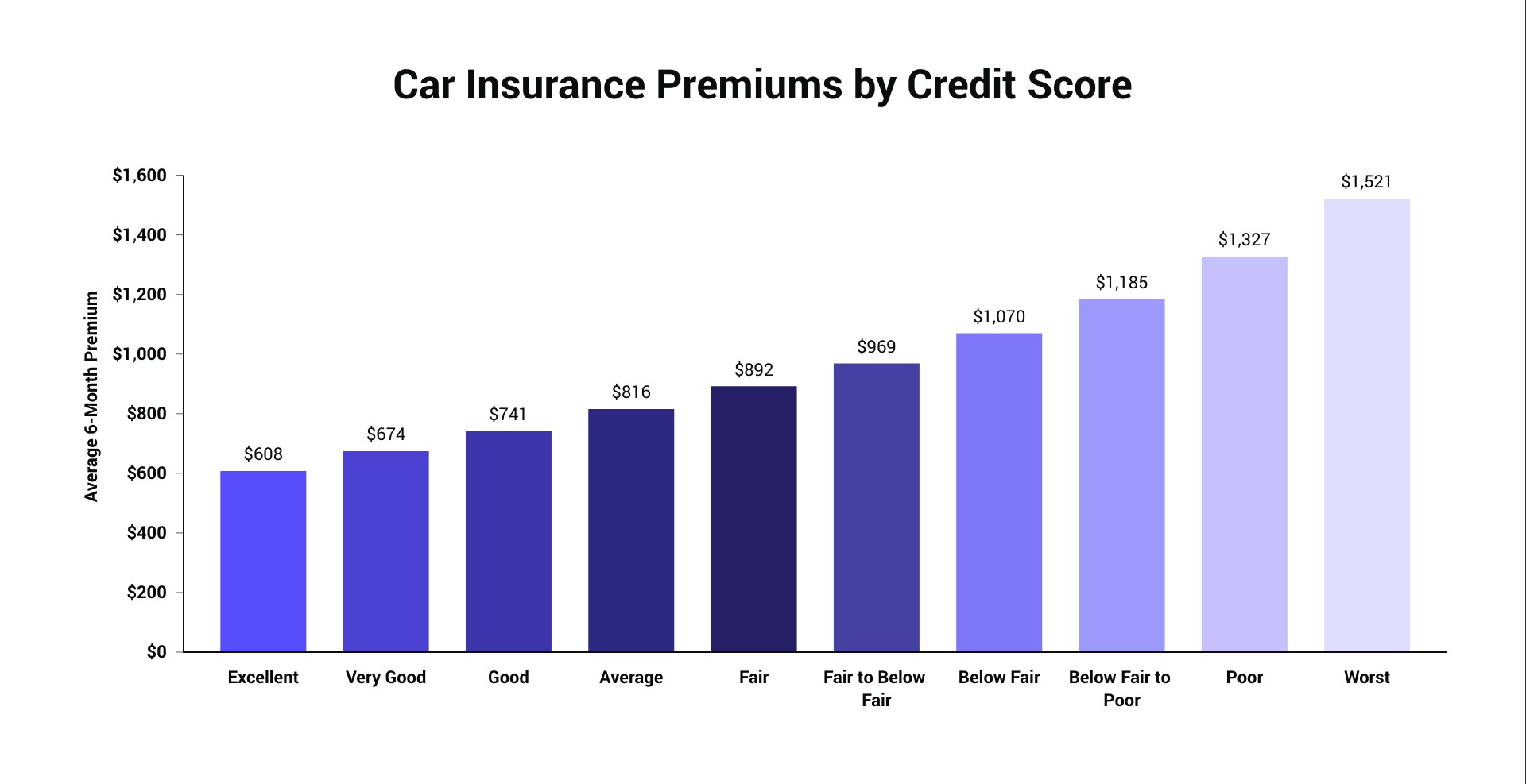

- Credit Score: In some states, insurance companies may consider your credit score as a factor when determining your car insurance rates. A lower credit score can lead to higher premiums.

- Claims History: If you have a history of filing insurance claims, especially for at-fault accidents, insurance companies may view you as a higher risk and increase your premiums.

It’s important to note that each insurance company may weigh these factors differently, so it’s worth shopping around and comparing quotes to find the best rates for your specific circumstances.

Average Cost of Car Insurance for 21-Year-Old Males

Due to the higher perceived risk associated with young and inexperienced drivers, 21-year-old males typically face higher car insurance premiums compared to older drivers. The exact cost can vary depending on various factors, but it is helpful to have a general understanding of the average cost of car insurance for this demographic.

On average, 21-year-old males can expect to pay anywhere between $2000 and $5000 per year for car insurance coverage. This estimate is based on national averages and may vary depending on individual circumstances and location. It is important to note that these figures are approximate and can fluctuate significantly based on the factors mentioned earlier.

The cost of car insurance for 21-year-old males is influenced by the higher likelihood of accidents and risky driving behavior associated with this age group. Insurance companies factor in this increased risk when determining premiums, making it essential for young male drivers to carefully consider their insurance options.

Moreover, the type of coverage and deductibles you choose will also impact the overall cost of your car insurance. If you opt for comprehensive coverage with lower deductibles, you can expect higher premiums. However, choosing higher deductibles may help lower your premiums, but it also means you would need to pay a larger out-of-pocket amount before insurance coverage kicks in.

Keep in mind that these average costs are just estimates, and the final rates will depend on the specific details of your driving history, location, and choice of insurance company. It’s always a good idea to compare quotes from multiple insurers to find the best coverage options at the most affordable rates.

Tips for Lowering Car Insurance Premiums

While car insurance premiums for 21-year-old males may be higher than average, there are several strategies you can employ to help reduce the cost of your car insurance. Here are some tips to consider:

- Shop around: Get quotes from multiple insurance providers to compare rates. Each company has its own pricing structures, so taking the time to shop around can help you find the best deal.

- Consider a higher deductible: Opting for a higher deductible can lower your premiums. Just be sure you can comfortably afford the deductible amount in the event of a claim.

- Take advantage of discounts: Many insurance companies offer discounts for various factors such as having a good academic record, completing a defensive driving course, or bundling your car insurance with other policies.

- Maintain a clean driving record: Avoiding traffic violations and accidents can help keep your insurance rates lower. Responsible driving behavior demonstrates to insurance companies that you are a low-risk driver.

- Consider a safer vehicle: Certain car models have better safety ratings and are less expensive to insure. Opting for a car with advanced safety features can potentially lower your premiums.

- Limit optional coverages: Assess your insurance policy and consider excluding optional coverages that may not be necessary for your situation. However, evaluate the potential impact on your overall coverage.

- Improve your credit score: In states where credit score is considered, maintaining a good credit score can help lower your car insurance premiums.

By implementing these tips, you can potentially lower your car insurance premiums and make it more affordable. However, it’s important to strike a balance between cost reduction and maintaining adequate coverage.

Remember, the cost of car insurance for 21-year-old males is influenced by multiple factors, and each insurance company may have its unique pricing structure. Be proactive in researching and exploring your options to find the best coverage at the most competitive rates.

Conclusion

Car insurance for 21-year-old males can be costly due to the higher perceived risk associated with this demographic. However, understanding the factors that affect insurance rates and knowing the average cost can help you make informed decisions and find ways to lower your premiums.

Factors such as age, gender, driving record, type of vehicle, location, and coverage options all play a significant role in determining car insurance rates. By being aware of these factors, you can take steps to minimize the impact they have on your premiums.

Shopping around for quotes, considering higher deductibles, taking advantage of available discounts, maintaining a clean driving record, and opting for safer vehicles are all viable strategies for reducing car insurance costs. Additionally, improving your credit score can be beneficial in states where it is a factor considered by insurance companies.

While it’s important to find affordable car insurance, remember that price should not be the sole determinant of your coverage. It’s crucial to strike a balance between cost and adequate protection to safeguard yourself and your vehicle financially.

Always consult with insurance professionals and thoroughly analyze the terms and conditions of policies before making a decision. By being proactive and making informed choices, you can secure the right car insurance coverage at a price that fits within your budget.

Remember, as you become a more experienced driver and reach different milestones in your life, your car insurance rates are likely to change. Continue to reassess your coverage and explore new opportunities for savings to ensure you always have the most cost-effective car insurance policy.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance