Finance

What Is Trade Receivables In Accounting

Published: October 9, 2023

Learn about trade receivables in accounting and its importance in finance. Understand how they contribute to a company's cash flow and overall financial health.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- What Are Trade Receivables?

- Importance of Trade Receivables in Accounting

- Recognition and Measurement of Trade Receivables

- Accounting Treatment for Trade Receivables

- Valuation and Presentation of Trade Receivables

- Impairment of Trade Receivables

- Managing and Controlling Trade Receivables

- Key Metrics for Analyzing Trade Receivables

- Conclusion

What Are Trade Receivables?

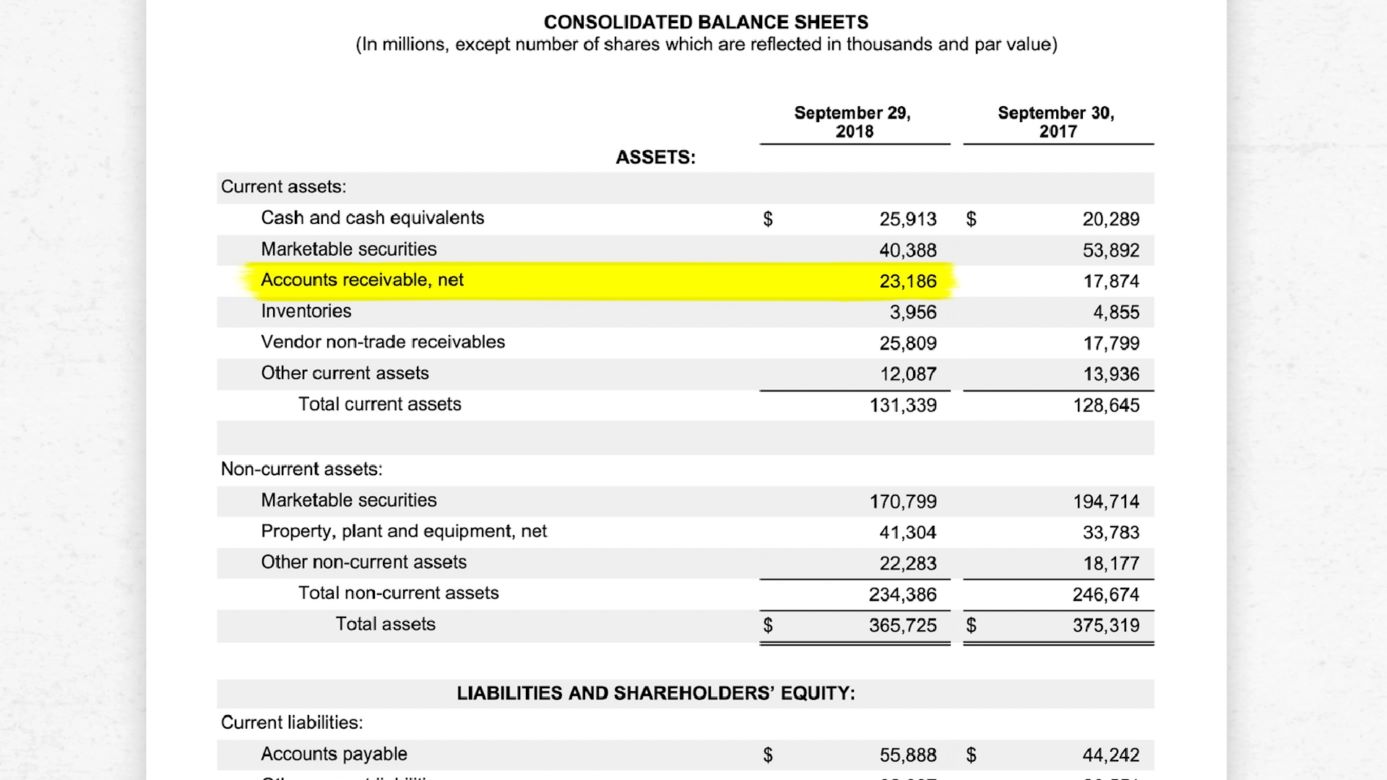

Trade receivables, also known as accounts receivable, are a key component of a company’s working capital. They represent the amounts owed to a business by its customers for the sale of goods or services on credit.

When a company sells its products or services on credit, it creates an account receivable. Essentially, trade receivables are the outstanding invoices that a company expects to collect from its customers within a certain period of time, typically within 30, 60, or 90 days. These receivables are considered as short-term assets on the company’s balance sheet.

Trade receivables are a vital aspect of a company’s cash flow and profitability. They reflect the company’s sales revenue that is yet to be collected in cash. For many businesses, trade receivables can make up a significant portion of their total assets and can have a substantial impact on their financial performance.

Companies across various industries, such as manufacturing, retail, and services, frequently use trade receivables to boost sales and attract customers who may not have the means to pay upfront. By offering credit terms, businesses can encourage customers to make purchases and pay at a later date, thereby facilitating sales and promoting growth.

It is important to note that trade receivables come with a certain level of risk. Not all customers may fulfill their payment obligations, resulting in bad debts or non-payment. This risk highlights the importance of effective credit management and assessing the creditworthiness of customers before extending credit.

Overall, trade receivables play a crucial role in a company’s financial operations by balancing the need to stimulate sales with the management of credit risk.

Importance of Trade Receivables in Accounting

Trade receivables hold significant importance in accounting as they provide insight into a company’s financial health, cash flow, and overall profitability. Understanding the importance of trade receivables can help businesses make informed decisions and effectively manage their credit policies. Here are some key reasons why trade receivables are crucial in accounting:

- Revenue Recognition: Trade receivables are a representation of revenue earned by a company but not yet received in cash. Recognizing trade receivables allows businesses to record sales and revenue in their financial statements accurately. This is essential for stakeholders, such as investors and lenders, to assess the company’s financial performance.

- Cash Flow Management: Trade receivables directly impact a company’s cash inflows. Monitoring and managing the collection of trade receivables is essential for maintaining healthy cash flow. Efficient collection processes ensure that the company has sufficient funds to meet its financial obligations and invest in growth opportunities.

- Working Capital Management: Trade receivables are a component of working capital, which represents the funds required for day-to-day operations. A well-managed trade receivables balance is crucial for optimizing working capital and ensuring the smooth functioning of the business. It allows for the timely payment of suppliers, employees, and other operational expenses.

- Assessment of Credit Risk: Analyzing trade receivables provides insights into the creditworthiness of customers and the potential risk of non-payment or bad debts. By monitoring the aging of receivables and implementing effective credit control measures, businesses can minimize credit risk and avoid significant financial losses.

- Financial Analysis: Trade receivables play a vital role in financial analysis, helping stakeholders evaluate a company’s liquidity, profitability, and overall financial stability. Ratios such as the days sales outstanding (DSO) and the accounts receivable turnover ratio provide valuable insights into the company’s collection efficiency and the effectiveness of credit policies.

- Decision Making: Trade receivables data supports decision-making processes. It helps businesses determine credit limits, set payment terms, identify customers with overdue payments, and negotiate favorable payment terms with suppliers based on their own collections.

Overall, trade receivables provide essential information for effective financial management, enabling businesses to maintain liquidity, manage credit risk, and make informed strategic decisions. Accurate accounting and diligent monitoring of trade receivables are vital for the financial success and sustainability of any organization.

Recognition and Measurement of Trade Receivables

Recognition and measurement of trade receivables involve determining when and how to record these assets on a company’s financial statements. Proper recognition and accurate measurement are essential for presenting a realistic and reliable financial position. Here are the key aspects of the recognition and measurement process:

Recognition: Trade receivables are recognized when there is a legally enforceable right to payment from the customer for goods delivered or services rendered. This typically occurs at the time of the sale or delivery of goods. The transaction is recorded by debiting the accounts receivable and crediting the sales revenue account.

Measurement: Trade receivables are initially measured at their fair value, which is usually the invoiced amount. The fair value represents the consideration the company expects to receive in exchange for the goods or services provided. It includes any applicable trade discounts or rebates.

Subsequent Measurement: After initial recognition, trade receivables are typically measured at amortized cost using the effective interest rate method. This involves recognizing interest income or expense over the expected payment period, taking into account the stated interest rate and any relevant changes to the customer’s credit risk.

Provision for Doubtful Debt: In cases where there is reasonable doubt about the collectability of a trade receivable, a provision for doubtful debts is established. This provision represents an estimate of the potential losses due to non-payment or bad debts. The amount is recognized as an expense, reducing the carrying value of the receivables and reflecting the anticipated losses.

Estimation of Bad Debts: Estimating the allowance for doubtful debts requires careful consideration of factors such as historical collection patterns, customer creditworthiness, economic conditions, and industry trends. Regular assessment and adjustments are necessary to ensure the adequacy of the provision.

Disclosure: Adequate disclosure is essential to provide users of financial statements with a clear understanding of a company’s trade receivables. This includes information about the significant accounting policies, credit terms, maturity profiles, and any concentrations of credit risk.

It’s important for companies to adhere to recognized accounting standards, such as Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS), to ensure consistency and comparability in the recognition and measurement of trade receivables. By following these guidelines, companies can provide accurate and transparent financial information to their stakeholders.

Accounting Treatment for Trade Receivables

The accounting treatment for trade receivables involves the proper recording, valuation, and subsequent measurement of these assets as part of a company’s financial statements. The following outlines the key aspects of the accounting treatment for trade receivables:

Initial Recognition: Trade receivables are initially recorded at their fair value upon the sale of goods or the provision of services on credit. This is typically done by debiting the accounts receivable and crediting the corresponding revenue account, such as Sales or Services Revenue.

Valuation: Following initial recognition, trade receivables are measured at their amortized cost, which represents the present value of the expected cash flows. The carrying value of the receivables is reduced by any applicable allowance for doubtful debts or provision for bad debts.

Allowance for Doubtful Debts: A provision for doubtful debts, also known as an allowance for doubtful debts, is established to account for the potential non-payment or bad debts associated with trade receivables. This provision is estimated based on historical collection patterns, customer creditworthiness, economic conditions, and other relevant factors.

Subsequent Measurement: Trade receivables are typically measured at amortized cost using the effective interest rate method. This involves recognizing interest income over the expected payment period, taking into account any changes in the customer’s credit risk or payment terms.

Bad Debt Write-offs: When it becomes evident that a trade receivable is uncollectible, it is written off as a bad debt. This involves debiting the provision for doubtful debts and crediting the specific trade receivable account. The write-off reduces the carrying value of the receivables and reflects the actual loss incurred by the company.

Disclosures: Adequate disclosure is essential to provide users of financial statements with relevant information about trade receivables. This includes the accounting policies followed, the amount of provision for doubtful debts, aging analysis of receivables, and any concentration of credit risk.

It is important for companies to adhere to applicable accounting standards, such as Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS), to ensure consistent and transparent accounting for trade receivables. By following these guidelines, companies can accurately report their financial position and provide users with reliable information about their trade receivables.

Valuation and Presentation of Trade Receivables

The valuation and presentation of trade receivables in a company’s financial statements are essential for providing a clear and accurate picture of the receivables’ value and their impact on the company’s financial position. Here are the key considerations for the valuation and presentation of trade receivables:

Carrying Value: Trade receivables are typically carried at their net realizable value, which represents the estimated amount the company expects to collect from customers after accounting for any provisions for doubtful debts.

Provision for Doubtful Debts: A provision for doubtful debts is established to account for the potential non-payment or bad debts associated with trade receivables. The provision is an estimate based on historical collection patterns, customer creditworthiness, economic conditions, and other relevant factors. The provision is subtracted from the gross trade receivables to arrive at the net carrying value.

Allowance Method: The allowance method is commonly used to value trade receivables. Under this method, a specific provision is set aside based on an estimate of the expected losses from bad debts. The provision is deducted from the gross receivables on the balance sheet to arrive at the net receivables.

Recovery of Previously Written-off Receivables: If a previously written-off trade receivable is collected after being recognized as bad debt, the recovery is recorded as a reduction in the provision for doubtful debts and as an increase in cash or receivables. The recovery amount is presented separately in the financial statements to highlight the impact on the company’s financial position.

Presentation in the Financial Statements: Trade receivables are typically presented as a separate line item on the balance sheet, under current assets. They are categorically disclosed to provide users of financial statements with transparency regarding the company’s outstanding receivables and their significance in the company’s operations.

Disclosures: It is important to provide sufficient disclosures in the financial statements regarding trade receivables. This includes information about the accounting policies applied, the aging analysis of trade receivables (i.e., how long they have been outstanding), the provision for doubtful debts, and any concentration of credit risk.

Accurate valuation and transparent presentation of trade receivables provide stakeholders with valuable insights into the financial health, credit risk, and liquidity position of a company. Following appropriate accounting standards and guidelines ensures consistency and comparability in the valuation and presentation of trade receivables across different companies and industries.

Impairment of Trade Receivables

The impairment of trade receivables refers to the recognition and accounting treatment of potential losses that may arise from the non-payment or default of customers. It is crucial for companies to assess and recognize impairment to accurately reflect the value of the receivables on their financial statements. Here are the key aspects of the impairment of trade receivables:

Impairment Assessment: Companies need to regularly assess their trade receivables for potential impairment. This involves evaluating individual receivables or groups of receivables to determine if there are any objective indicators of impairment, such as financial difficulties of customers or delays in payment.

Recognizing Impairment: If there is evidence of impairment, companies need to recognize an allowance for impairment losses to reduce the carrying amount of the trade receivables. The allowance is based on the estimated difference between the carrying value of the receivables and the present value of expected future cash flows.

Estimating Impairment Loss: Estimating the amount of impairment loss requires careful consideration of factors such as historical collection data, industry trends, economic conditions, and customer creditworthiness. Companies may use various methods, including the specific identification method, the provision matrix method, or statistical models, to estimate impairment losses.

Reversal of Impairment: If, in a subsequent period, the conditions that led to the impairment have improved, companies may reverse the impairment loss. However, the reversal is limited to the amount that would not have been recognized originally as an expense if no impairment had been recognized. This reversal is recorded as a reduction in the allowance for impairment losses.

Disclosure: Transparent disclosure is vital to provide users of financial statements with relevant information about the impairment of trade receivables. This includes disclosing the accounting policies applied, the methods used to estimate impairment, the amount of allowance for impairment losses, and any changes in the estimation process.

The impairment of trade receivables reflects the potential credit risks and uncertainties associated with collecting payments from customers. By appropriately assessing, recognizing, and disclosing impairment losses, companies can provide stakeholders with a more accurate picture of the financial impact of trade receivables on their operations and overall financial position.

Managing and Controlling Trade Receivables

Effectively managing and controlling trade receivables is essential for maintaining a healthy cash flow, minimizing credit risk, and optimizing the overall financial performance of a company. By implementing sound strategies and practices, businesses can ensure timely collection of payments and mitigate the impact of bad debts. Here are key considerations for managing and controlling trade receivables:

Credit Assessment: Conducting a thorough credit assessment of customers is crucial before extending credit. This involves evaluating their credit history, financial stability, and payment patterns to determine their creditworthiness. Implementing credit limits and terms based on the assessment helps minimize the risk of non-payment.

Credit Terms and Policies: Clearly defining credit terms and policies is important to set expectations with customers. This includes specifying payment due dates, late payment penalties, and any discounts or incentives for early payment. Effective communication of these terms and policies helps prevent overdue receivables.

Invoice Accuracy and Timeliness: Accurate and timely invoicing is essential to ensure prompt payment. Invoices should be detailed, transparent, and free from errors. Implementing efficient invoice generation and delivery processes helps streamline the payment collection cycle.

Monitoring Aging of Receivables: Regularly monitoring the aging of receivables helps identify overdue accounts and take appropriate actions. Utilizing an aging analysis report enables businesses to prioritize collection efforts and allocate resources accordingly for addressing delinquent accounts.

Collections and Follow-up: Establishing a systematic approach to collections and follow-up is crucial for maintaining good customer relationships while ensuring timely payments. Implementing proactive communication, providing payment reminders, and actively engaging with customers can help expedite the collection process.

Receivables Analysis: Regularly analyzing receivables and related metrics provides insights into the overall cash flow and credit management effectiveness. Key metrics to monitor include Days Sales Outstanding (DSO), Receivables Turnover Ratio, and Aging Bucket Analysis. This information helps identify trends, potential issues, and areas for improvement.

Credit Insurance or Factoring: Businesses may opt for credit insurance or engage in receivables factoring to mitigate credit risk. Credit insurance protects against non-payment, while factoring involves selling receivables to a third-party at a discount in exchange for immediate cash. These options can provide additional financial security and improve liquidity.

Effective Dispute Resolution: Resolving customer disputes in a timely and fair manner is essential for maintaining good customer relationships and preventing payment delays. Implementing a structured process to address and resolve customer issues can help minimize the impact on receivables collection.

Continuous Improvement: Regularly reviewing and refining credit policies, collection strategies, and internal processes is important for continuous improvement in managing trade receivables. Identifying areas for enhancement, embracing technology-driven solutions, and staying updated with industry best practices help optimize receivables management.

By implementing effective strategies for managing and controlling trade receivables, businesses can improve cash flow, reduce credit risk, and enhance overall financial performance. Adopting proactive approaches, leveraging technology, and maintaining strong customer relationships contribute to successful receivables management and long-term business sustainability.

Key Metrics for Analyzing Trade Receivables

Analyzing trade receivables through key metrics provides valuable insights into the efficiency, effectiveness, and financial health of a company’s credit and collection processes. These metrics help businesses monitor and evaluate the performance of their trade receivables and identify areas for improvement. Here are some key metrics for analyzing trade receivables:

Days Sales Outstanding (DSO): DSO is a widely used metric that measures the average number of days it takes for a company to collect payment from its customers after a sale is made. It helps assess the efficiency of a company’s credit and collection policies. A lower DSO indicates faster collection and better management of receivables.

Receivables Turnover Ratio: The receivables turnover ratio measures how many times, on average, a company collects its average accounts receivable balance during a given period. It indicates the efficiency of receivables management and the ability to convert credit sales into cash. A higher turnover ratio signifies faster collection and more effective credit policies.

Aging Bucket Analysis: Aging analysis categorizes trade receivables based on the length of time they have been outstanding, typically into different timeframes like 0-30 days, 31-60 days, 61-90 days, and over 90 days. This analysis provides a snapshot of the age composition of receivables and helps identify potential collection issues or trends.

Bad Debt Ratio: The bad debt ratio measures the percentage of total sales revenue that is not expected to be collected due to non-payment or defaults. It highlights the credit risk and the effectiveness of credit underwriting and collection efforts. A higher bad debt ratio indicates a higher risk of non-payment and potential financial losses.

Collection Effectiveness Index (CEI): The CEI measures the effectiveness of a company’s collection efforts in terms of the percentage of outstanding receivables collected during a given period. It compares the amount of cash collected to the total outstanding receivables and helps assess the efficiency of the collection process. A higher CEI indicates more effective collection efforts.

Credit Quality Ratio: The credit quality ratio assesses the creditworthiness and risk associated with a company’s customer base. It classifies customers into different credit quality categories based on their credit scores, payment history, and financial stability. This analysis aids in managing credit risk and establishing appropriate credit limits for customers.

Average Collection Period: The average collection period calculates the average number of days it takes for a company to collect payment from its customers based on the total trade receivables and credit sales. It helps evaluate the effectiveness of credit policies and the efficiency of collections. A shorter average collection period indicates faster payment collection.

Write-off Percentage: The write-off percentage measures the portion of trade receivables that is deemed uncollectible and ultimately written off as bad debt. It provides insights into the effectiveness of credit assessment, collection efforts, and the accuracy of estimating provisions for doubtful debts. A higher write-off percentage may indicate inadequate credit management.

By analyzing these key metrics and monitoring them regularly, businesses can gain valuable insights into their receivables management performance. These metrics help identify areas for improvement, enhance cash flow, minimize credit risk, and maximize the profitability and financial stability of a company.

Conclusion

Trade receivables are a vital component of a company’s financial operations, representing the amounts owed by customers for goods or services provided on credit. Proper management, valuation, and control of trade receivables are essential for maintaining a healthy cash flow, optimizing working capital, and minimizing credit risk. By implementing effective strategies and monitoring key metrics, businesses can improve their financial performance and ensure timely collection of payments.

Recognizing and measuring trade receivables accurately is crucial to provide transparent and reliable financial information. This involves assessing creditworthiness, establishing appropriate credit limits, and implementing sound credit policies. Additionally, timely and accurate invoicing, efficient collection efforts, and proactive follow-up on overdue accounts contribute to the successful management of trade receivables.

Analyzing trade receivables through key metrics such as DSO, receivables turnover ratio, and aging bucket analysis provides insights into the efficiency, effectiveness, and financial health of receivables management. These metrics help identify areas for improvement, optimize credit and collection processes, and mitigate credit risk.

Furthermore, the measurement and presentation of trade receivables, including the provision for doubtful debts, are important for accurately reflecting their value on the balance sheet. Proper disclosure of accounting policies and the impact of credit risk ensures transparent reporting, enabling stakeholders to make informed decisions about a company’s financial position.

In conclusion, effective management and control of trade receivables are crucial for maintaining a healthy cash flow, optimizing working capital, and minimizing credit risk. By implementing sound credit policies, monitoring key metrics, and accurately valuing and presenting trade receivables, businesses can enhance their financial performance, strengthen customer relationships, and ensure long-term success.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: Chelsea • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance