Finance

When Will A Credit Card Company Sue You

Published: October 26, 2023

Learn when a credit card company may take legal action against you and how to avoid being sued. Get expert advice on finance and debt management.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding Credit Card Debt

- Steps Credit Card Companies Take Before Considering a Lawsuit

- Factors that Can Lead to Credit Card Companies Suing You

- Signs that a Credit Card Lawsuit Is Imminent

- What to Do If You Are Sued by a Credit Card Company

- Defending Against a Credit Card Lawsuit

- Potential Consequences of Losing a Credit Card Lawsuit

- How to Avoid Getting Sued by a Credit Card Company

- Conclusion

Introduction

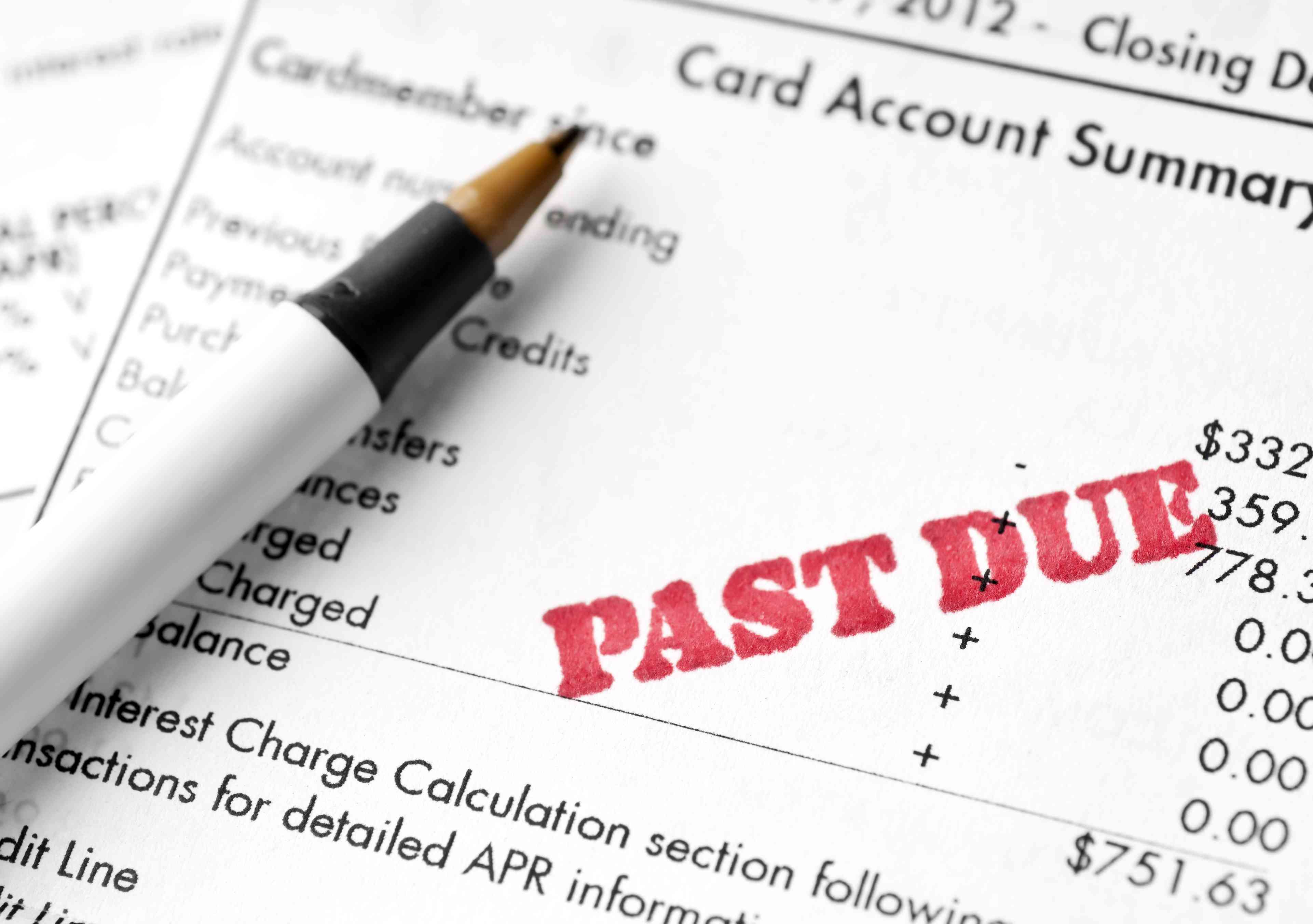

Credit cards have become an integral part of our financial lives, offering convenience and flexibility in managing expenses. However, sometimes life circumstances can make it difficult to keep up with credit card payments, leading to mounting debt. In such situations, credit card companies may take legal action to recover the outstanding balances.

Understanding the process of when a credit card company may sue you is crucial for anyone facing financial difficulties or struggling with credit card debt. By knowing the steps leading up to a potential lawsuit and how to navigate the situation, you can better protect yourself and manage your financial obligations.

In this article, we will delve into the factors that can lead to credit card companies considering legal action, signs indicating a potential lawsuit, and the steps you can take to defend yourself if you are sued. Additionally, we will discuss the consequences of losing a credit card lawsuit and provide tips on how to avoid getting sued in the first place.

It is essential to remember that every situation is unique, and this article serves as a general guide. If you are facing legal action or need specific advice regarding your credit card debt, it is recommended to consult with a qualified legal professional.

Understanding Credit Card Debt

Credit card debt refers to the amount of money you owe to your credit card issuer for the purchases you have made using your credit card. It is a form of revolving debt, meaning that as you make payments toward your debt, the available credit limit on your card is replenished, allowing you to make further purchases.

When you use your credit card, you are essentially borrowing money from the credit card company. If you fail to make the required minimum payment or go over your credit limit, you may incur penalties and interest charges, which can rapidly increase your debt. It is essential to understand the terms and conditions of your credit card agreement, including interest rates, late fees, and any additional charges.

Credit card debt can become overwhelming if not managed effectively. Excessive debt can result in financial stress, damaged credit scores, and potential legal action from credit card companies. It is crucial to keep track of your credit card balances, make timely payments, and avoid excessive spending to prevent falling into a cycle of debt.

If you find yourself struggling with credit card debt, there are several options available to help you regain financial control. You can work towards creating a budget, cutting unnecessary expenses, and increasing your income to free up funds for debt repayment. Additionally, debt consolidation or seeking professional advice from credit counseling services can provide strategies to manage and reduce your credit card debt effectively.

Understanding the implications of credit card debt and taking proactive steps to manage it is key to financial stability. By prioritizing debt repayment and adopting responsible spending habits, you can avoid the negative consequences associated with excessive credit card debt, including potential legal action from credit card companies.

Steps Credit Card Companies Take Before Considering a Lawsuit

Before a credit card company decides to take legal action against a debtor, they typically follow a series of steps in an attempt to collect the outstanding debt. These steps may vary among credit card companies, but the general process typically includes the following:

- Notification: When a credit card payment is missed or overdue, the credit card company will typically notify the cardholder of the missed payment through phone calls, emails, or written notices. This notification serves as a reminder and encourages the cardholder to rectify the situation by making the payment.

- Collection Efforts: If the initial notification does not prompt the cardholder to make the payment, the credit card company may escalate their collection efforts. This can include contacting the cardholder more frequently, utilizing collection agencies, or employing in-house collection agents to negotiate payment arrangements or settlements.

- Charge-Off: If the account remains delinquent for a significant period, typically around six months, the credit card company may consider charging off the debt. Charge-off is a formal accounting procedure where the company declares the debt as unlikely to be collected. However, this does not absolve the cardholder of the debt, and collection attempts may continue.

- Assignment to Collections: At this stage, the credit card company may decide to assign the debt to a third-party collections agency. The collections agency will then attempt to collect the debt on behalf of the credit card company. The collections agency may engage in aggressive collection activities, such as frequent phone calls and letters, in an effort to secure payment.

- Legal Action: If the efforts made by the credit card company and collections agency fail to recover the debt, the credit card company may decide to pursue legal action. This typically involves filing a lawsuit against the cardholder to obtain a judgment, which allows them to collect the debt through various means, such as wage garnishment or property liens.

It is important to note that the steps outlined above are general guidelines, and the specific actions taken by credit card companies may vary. Additionally, the timelines for each step can vary depending on various factors, such as state laws and the credit card company’s policies.

Understanding the steps credit card companies take before considering a lawsuit can help you anticipate their actions and explore alternative solutions beforehand. It is crucial to stay proactive and communicate with your credit card company or collections agency to find a resolution that works for both parties and avoids the need for legal intervention.

Factors that Can Lead to Credit Card Companies Suing You

Credit card companies typically resort to legal action as a last resort to collect outstanding debts from cardholders. While each case is unique, several factors can increase the likelihood of a credit card company deciding to sue you:

- Delinquency: Consistently missing credit card payments or falling behind on your payments can increase the chances of facing legal action. When you fail to meet your financial obligations, credit card companies may view this as a breach of the credit card agreement and may pursue legal remedies to recoup the owed debt.

- Large Debt Balances: Having significant outstanding debt balances can make you a target for legal action. Credit card companies are more likely to initiate lawsuits if the owed amount is substantial, as it poses a higher risk of non-repayment.

- Repeated Non-Payment: If you have a history of non-payment, credit card companies may be more inclined to sue to protect their interests. If previous collection attempts have been unsuccessful, they may see legal action as the only viable option to recover the debt.

- Absence of Communication: Lack of communication with your credit card company can escalate the situation towards a lawsuit. Ignoring notices, calls, or attempts to negotiate repayment arrangements can give credit card companies the impression that you are avoiding your financial obligations.

- Expired Statute of Limitations: Each jurisdiction has a statute of limitations that limits the period during which creditors can file a lawsuit to collect the debt. However, it is important to note that acknowledging the debt or making partial payments can reset the statute of limitations clock in some jurisdictions.

- Fraudulent Activity: Engaging in fraudulent activities, such as using a credit card with no intention to repay or providing false information during the application process, can increase the likelihood of facing legal consequences. Credit card companies take fraud seriously and may pursue legal action to protect their interests and deter fraudulent behavior.

- High Credit Card Utilization: Maxing out your credit card limits or consistently utilizing a high percentage of your available credit can indicate financial instability. Credit card companies may view this as a risk factor and may be more inclined to take legal action to mitigate potential losses.

While these factors can increase the likelihood of credit card companies suing you, it does not guarantee that legal action will be taken. Each situation is evaluated on a case-by-case basis. It is essential to stay proactive, communicate with your credit card company, and explore alternative options for debt resolution to avoid the need for a lawsuit.

Signs that a Credit Card Lawsuit Is Imminent

Facing a credit card lawsuit can be a stressful and overwhelming experience. It is important to recognize the warning signs that indicate a potential lawsuit might be imminent, so that you can take appropriate action to protect your rights and finances. Here are some common signs to watch out for:

- Increased Collection Efforts: If you notice a significant increase in collection calls, letters, or emails from your credit card company or a third-party collections agency, it may be a sign that legal action is being considered. Credit card companies may intensify their collection efforts as a precursor to filing a lawsuit.

- Service by Process Server: Being served with a summons or legal documents by a process server is a clear indication that you are being sued by your credit card company. These documents will outline the details of the lawsuit, including the amount being claimed and instructions on how to respond.

- Notice of Legal Action: You may receive a notice directly from the credit card company indicating their intention to pursue legal action if the debt remains unpaid. This notice may outline the steps they intend to take and provide you with a specified period to resolve the matter before legal action is initiated.

- Court-Related Correspondence: Receiving correspondence from a court or a law firm representing the credit card company is a strong indication that a lawsuit has been filed against you. This can include letters notifying you of a court date or a judgment entered against you.

- Bank Account or Wage Garnishment: In more severe cases, after a judgment has been obtained, credit card companies may seek to enforce the judgment by garnishing your bank accounts or wages. If you notice sudden deductions from your bank account or receive notice of wage garnishment, it is a clear sign that legal action has been taken.

- Legal Representation: If you receive communication from an attorney representing the credit card company, it is likely that a lawsuit has been filed or is imminent. Legal representation indicates that the situation has escalated, and it may be necessary for you to also seek legal advice.

Remember, the signs mentioned above should not be relied on as absolute indicators of a credit card lawsuit, as each case may have unique circumstances. If you notice any of these signs, it is crucial to seek legal advice promptly. An attorney specializing in debt collection and consumer protection can provide guidance and help you navigate the legal process effectively.

What to Do If You Are Sued by a Credit Card Company

Being sued by a credit card company can be a daunting experience, but it’s important to remember that you have rights and options to protect yourself. If you find yourself in this situation, here are some steps you can take:

- Read and Respond: Carefully read through the summons and complaint documents served to you. Take note of the deadline to respond, which is typically a specific number of days from the date of service. Ignoring the lawsuit can result in a default judgment, so it’s crucial to respond within the given timeframe.

- Consult an Attorney: Consider seeking legal advice from an attorney who specializes in debt collection and consumer protection laws. They can help you understand your rights, assess your situation, and guide you through the legal process. An attorney can also provide representation and negotiate on your behalf.

- Gather Documentation: Collect and organize any relevant documents related to the debt and the credit card account. This may include credit card statements, payment records, correspondence, and any evidence that can support your defense or challenge the validity of the debt.

- File a Response: Prepare and file a response to the lawsuit within the given timeframe. This response should address each allegation made in the complaint. It is essential to follow the proper legal format and include any defenses or counterclaims you may have. Working with an attorney can ensure your response is accurate and properly presented.

- Explore Settlement Options: If appropriate, you can explore the possibility of negotiating a settlement with the credit card company or their legal representatives. This may involve working out a payment plan or reaching a mutually acceptable agreement to resolve the debt without going to trial. Having legal representation can be beneficial during settlement negotiations.

- Prepare for Trial: If the lawsuit proceeds to trial, it is crucial to be prepared. Work closely with your attorney to gather evidence, identify witnesses, and build a strong defense. Attend all required court hearings and comply with any pre-trial procedures outlined by the court.

- Know your Rights: Familiarize yourself with your rights as a debtor. This includes understanding applicable state and federal laws regarding debt collection, statutes of limitations, and potential defenses you may have. Understanding your rights can help you navigate the legal process more effectively.

Remember, each situation is unique, and the best course of action will depend on your specific circumstances. Consulting with a knowledgeable attorney is crucial to ensure you have proper guidance and representation throughout the lawsuit process.

Defending Against a Credit Card Lawsuit

When faced with a credit card lawsuit, it is important to mount a strong defense to protect your rights and financial well-being. Here are some strategies to consider when defending against a credit card lawsuit:

- Hire an Attorney: Seek the assistance of an experienced attorney who specializes in debt collection. They can help assess your case, navigate the legal process, and develop a strong defense strategy tailored to your specific situation.

- Challenge the Creditor’s Standing: Request that the creditor prove their legal standing to sue you. This may involve demanding evidence that they are the rightful owner of the debt and have the legal authority to collect it. Challenging their standing can often lead to a dismissal or negotiation of the case.

- Dispute the Debt: Contest the debt by requesting verification and validation of the alleged amount owed. The creditor must provide evidence that the debt is accurate and properly documented. If they fail to do so, it may weaken their case against you.

- Statute of Limitations: Research and determine if the debt falls within the statute of limitations in your jurisdiction. If the debt is time-barred, meaning the creditor has exceeded the legal timeframe to pursue legal action, you may be able to have the case dismissed.

- Prove Lack of Documentation: Request that the creditor provides complete and accurate documentation to support their claims. This may include original signed contracts, account statements, and transaction history. If they are unable to provide these documents, it may undermine their case against you.

- Settlement Negotiation: Explore the possibility of negotiating a settlement with the creditor. If they are unable to provide sufficient evidence or have other weaknesses in their case, they may be more inclined to negotiate a resolution rather than proceed with a risky trial.

- Counterclaims: If you have a valid reason to do so, consider filing counterclaims against the creditor. Counterclaims assert that the creditor has violated consumer protection laws or engaged in unfair debt collection practices. This can strengthen your position and potentially lead to a more favorable outcome.

- Engage in Mediation or Alternative Dispute Resolution: Depending on the jurisdiction and the specific court, you may have the option to engage in mediation or alternative dispute resolution methods. These processes can provide an opportunity to reach a mutually acceptable settlement without the need for a trial.

Always consult with a qualified attorney to determine the best defense strategy for your specific case. They will offer valuable guidance, ensure your rights are protected, and fight for a favorable resolution on your behalf.

Potential Consequences of Losing a Credit Card Lawsuit

Losing a credit card lawsuit can have significant consequences for your financial situation and creditworthiness. It is crucial to understand the potential implications of an unfavorable outcome. Here are some common consequences that may arise:

- Judgment against You: If you lose a credit card lawsuit, a judgment will be entered against you. This means that the court has determined that you are legally obligated to repay the debt owed to the credit card company.

- Financial Penalties: The court may impose financial penalties, such as the repayment of the outstanding debt, interest, and legal fees incurred by the credit card company. These additional expenses can significantly increase the amount you owe.

- Wage Garnishment: After obtaining a judgment, the credit card company may seek a wage garnishment order to collect the debt. This means that a portion of your income will be deducted directly from your paycheck, making it challenging to manage your finances effectively.

- Bank Account Levy: If the credit card company is granted a judgment, they may have the right to seize funds from your bank accounts to satisfy the debt. This can lead to financial hardship and make it difficult to cover other necessary expenses.

- Damage to Credit Score: Losing a credit card lawsuit can damage your credit score significantly. The judgment and subsequent negative information will be reported to credit bureaus, making it harder for you to obtain credit in the future and potentially raising interest rates on existing debts.

- Difficulty Obtaining Loans or Credit: A negative judgment on your credit report can make it challenging to secure future loans or credit, including mortgages, car loans, or even credit cards. Lenders and financial institutions may perceive you as a higher credit risk due to the judgment against you.

- Property Liens: In some cases, a credit card company may seek to place a lien on your property as a means of ensuring repayment of the debt. This can affect your ability to sell or refinance the property until the debt is satisfied.

- Continued Collection Efforts: Even after a judgment is obtained, the collection efforts may continue. The credit card company may use various methods, such as additional collection calls, letters, or hiring collection agencies to recover the debt owed.

It is important to act promptly if you are facing a credit card lawsuit to have the best chance of avoiding these consequences. Seeking legal advice, exploring settlement options, and mounting a strong defense can help mitigate the potential negative impact on your financial well-being.

How to Avoid Getting Sued by a Credit Card Company

Avoiding a credit card lawsuit should be a priority for anyone facing financial difficulties or struggling with credit card debt. While each situation is unique, there are several proactive steps you can take to minimize the risk of being sued by a credit card company:

- Create a Budget and Stick to It: Develop a realistic budget that accounts for all your income and expenses. This will help you manage your finances effectively and ensure that you have enough funds to meet your credit card payments.

- Make Timely Payments: Always make your credit card payments on time, even if it means paying the minimum amount due. Late or missed payments can lead to penalties, increased interest rates, and ultimately, a potential lawsuit.

- Communicate with Your Credit Card Company: If you are facing financial difficulties that prevent you from making your credit card payments, contact your credit card company as soon as possible. They may be willing to work with you by offering temporary payment arrangements or adjusting your payment schedule.

- Seek Credit Counseling: Consider enrolling in a credit counseling program to gain financial education and guidance. Credit counselors can help you create a realistic debt repayment plan and negotiate with your creditors on your behalf.

- Monitor Your Credit Card Balances: Regularly review your credit card balances to ensure that you are not overspending or approaching your credit limit. Keeping your credit card utilization low can help prevent financial strain and reduce the risk of potential legal action.

- Be Wary of Predatory Lenders: Be cautious when dealing with lenders that offer high-interest loans or credit cards targeting individuals with poor credit. Such loans often come with unfavorable terms and conditions that can lead to mounting debt and potential lawsuits.

- Know Your Rights: Educate yourself on consumer protection laws and your rights as a borrower. Understanding the Fair Debt Collection Practices Act (FDCPA) and other relevant legislation can help you identify any violations and protect yourself from abusive debt collection practices.

- Consider Debt Consolidation: If you have multiple credit card debts, debt consolidation may be a viable option. Consolidating your debt into a single loan with a lower interest rate can make it more manageable and reduce the likelihood of falling behind on payments.

- Seek Legal Advice: If you are unable to resolve your credit card debt issues on your own, consult with a qualified attorney who specializes in debt collection and consumer protection. They can provide personalized advice and represent your interests if legal action becomes unavoidable.

By following these steps, you can take proactive measures to avoid getting sued by a credit card company and work towards regaining financial stability. Remember that early intervention and open communication are key to resolving credit card debt issues and preventing legal consequences.

Conclusion

Dealing with credit card debt and the potential for lawsuits can be overwhelming, but being informed and taking proactive steps can help you navigate these challenges. Understanding the factors that can lead to a credit card company suing you, as well as the signs that indicate a lawsuit may be imminent, is crucial in taking appropriate action to protect yourself.

If you find yourself sued by a credit card company, it is important to respond promptly, seek legal advice, and explore all available options for defense. Working with an experienced attorney can provide the expertise needed to build a strong defense, challenge the creditor’s claims, and potentially negotiate a favorable resolution.

Avoiding a credit card lawsuit altogether is ideal. By managing your finances responsibly, making timely payments, and communicating with your credit card company, you can minimize the risk of legal action. Seeking credit counseling, monitoring your credit card balances, and understanding your rights as a borrower can further empower you to avoid falling into excessive credit card debt.

Remember, each situation is unique, and the information in this article serves as a general guide. It is essential to seek personalized advice from professionals and legal experts to address your specific circumstances effectively. By being proactive, informed, and seeking appropriate assistance, you can navigate the challenges of credit card debt and potential lawsuits, and work towards achieving financial stability and peace of mind.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance