Finance

Why Am I Losing Money On My 401K

Published: October 17, 2023

Discover the reasons behind your 401K losses and gain control over your finances. Unlock expert financial advice and maximize your retirement investments with ease.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Investing in a 401(k) can be a smart way to save for retirement. With its tax advantages and potential for employer match, it’s no wonder that millions of Americans contribute to their 401(k) accounts each year. However, despite the benefits, some individuals may find themselves perplexed by the sight of their 401(k) balance dwindling. If you find yourself in this situation, you may be wondering why you are losing money on your 401(k) and what steps you can take to rectify the situation.

First and foremost, it’s important to understand that investing in the stock market involves some degree of risk. The value of your 401(k) can fluctuate based on market performance, which means that it’s natural to experience periods of gains and losses. However, if you consistently see a downward trend in your account balance, there may be underlying factors contributing to the erosion of your investment.

In this article, we will explore various reasons why you may be losing money on your 401(k). We will delve into topics such as understanding the basics of a 401(k), evaluating investment choices, assessing fees and expenses, analyzing market performance, evaluating contribution amounts, monitoring and adjusting investment strategies, considering tax implications, and seeking professional advice. By examining these factors, you will gain insights into how to make informed decisions to protect and potentially grow your retirement savings.

Understanding the Basics of a 401(k)

Before delving into the reasons why your 401(k) may be losing value, it’s essential to have a solid understanding of the basics of this retirement savings account. A 401(k) is a type of employer-sponsored retirement plan that allows employees to contribute a portion of their paycheck on a pre-tax basis. These contributions, along with any employer match, are invested in a selection of funds or investment options, usually including stocks, bonds, and mutual funds.

One key advantage of a 401(k) is the potential for tax savings. By contributing to a 401(k), you can reduce your taxable income for the year, as the contributions are deducted from your paycheck before taxes are calculated. This can result in substantial savings, particularly if you’re in a higher tax bracket.

Another benefit of a 401(k) is the potential for employer matching contributions. Many employers offer a matching program, where they will contribute a certain percentage of your salary to your 401(k) account. This is essentially free money that can significantly boost your retirement savings over time.

However, it’s important to note that 401(k) accounts are subject to certain limitations and restrictions. For example, there are annual contribution limits imposed by the IRS, which may change from year to year. It’s crucial to be aware of these limits and ensure that you’re maximizing your contributions without exceeding the allowed thresholds.

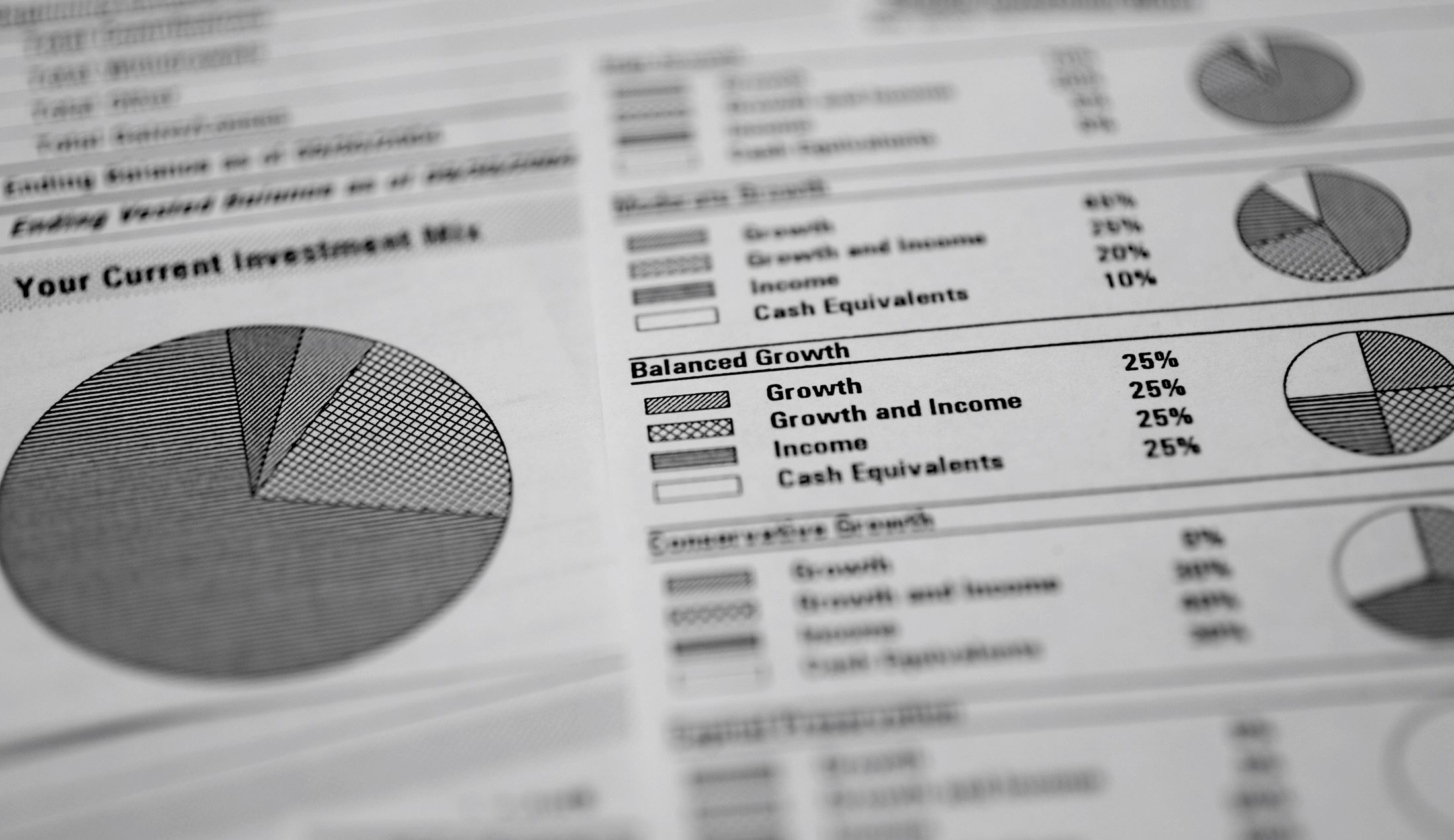

Additionally, 401(k) accounts typically come with a variety of investment options. These options can vary depending on the plan provider, but commonly include a mix of stocks, bonds, and mutual funds. It’s essential to understand the risk and return characteristics of each investment option and choose a diversified portfolio that aligns with your risk tolerance and investment goals.

By familiarizing yourself with the basics of how a 401(k) works, you’ll be better equipped to navigate the potential reasons behind its loss in value. In the next section, we will explore how the choice of investment options can impact the performance of your 401(k) account.

Evaluating Investment Choices

When it comes to your 401(k), the investment choices you make can have a significant impact on the growth and performance of your account. It’s crucial to evaluate these investment options carefully and choose ones that align with your risk tolerance and long-term financial goals.

One common reason for losing money on a 401(k) is investing too heavily in high-risk assets without considering the potential downside. While high-risk investments can offer the potential for high returns, they also come with a greater risk of significant losses. If your portfolio is heavily concentrated in volatile stocks or speculative investments, it’s essential to review your allocation and consider diversifying your holdings.

Diversification is a strategy that involves spreading your investments across different asset classes and sectors. By diversifying, you can mitigate the impact of any single investment’s downturn on your overall portfolio. For example, instead of solely investing in technology stocks, consider allocating funds to other sectors like healthcare or consumer goods to reduce your exposure to market-specific risks.

Another factor to consider when evaluating investment choices is the expense ratio of the funds within your 401(k) plan. The expense ratio represents the annual fee charged by the fund to cover administrative and management costs. High expense ratios can eat into your overall returns and erode the performance of your 401(k) over time. Be sure to review the expense ratios of the funds available in your plan and choose options with lower fees, such as passively managed index funds.

Additionally, it’s essential to keep in mind the time horizon for your retirement savings. Generally, as you approach retirement, it’s advisable to shift your investment strategy towards lower-risk assets to preserve capital. This is known as a target date fund, which automatically adjusts the asset allocation based on your expected retirement date. Review your investment choices and consider if they align with your desired time frame for retirement.

Evaluating your investment choices in your 401(k) should be an ongoing process. Regularly review your portfolio and make adjustments as necessary to ensure that your investments align with your risk tolerance, time horizon, and financial goals. By choosing a diversified and balanced investment strategy, you can minimize the risk of losing money on your 401(k) and potentially enhance the growth of your retirement savings.

Assessing Fees and Expenses

When managing your 401(k) investments, it’s crucial to be aware of the fees and expenses associated with your account. These costs can have a significant impact on the performance of your retirement savings over time. Understanding and assessing the fees and expenses can help you optimize your returns and prevent unnecessary losses.

One common fee associated with 401(k) accounts is the administrative fee. This fee covers the costs of managing and maintaining the plan, such as record-keeping, customer support, and legal compliance. It’s important to review the administrative fees charged by your plan provider to ensure that they are reasonable and in line with industry standards. If the administrative fees are too high, they can eat into your investment returns and result in a lower accumulation of wealth over time.

Another fee to consider is the expense ratio of the funds within your 401(k) plan, as mentioned in the previous section. The expense ratio represents the annual fee charged by each fund to cover its operating expenses. Funds with higher expense ratios can significantly impact your overall returns. It’s essential to evaluate the expense ratios of the funds available in your plan and choose options with lower fees, such as index funds or passively managed funds.

Some 401(k) plans may also charge individual service fees for specific transactions, such as taking out a loan or making a hardship withdrawal. These fees can vary depending on the plan provider and the type of transaction. Be sure to review the fee schedule of your 401(k) plan and understand the costs associated with any potential transactions you may consider.

Additionally, it’s important to be aware of any hidden or undisclosed fees that may be associated with your 401(k) plan. These fees can include revenue sharing, 12b-1 fees, or broker-sold fund fees. While these fees may not be immediately apparent, they can still impact the growth of your retirement savings. Take the time to review your plan’s fee disclosure document or consult with your plan administrator to gain clarity on any potential hidden fees.

By carefully assessing the fees and expenses associated with your 401(k) account, you can make informed decisions to optimize your investment returns. Consider comparing the fees of different investment options within your plan and explore the possibility of rolling over your 401(k) into an IRA, where you may have access to a wider range of investment choices with potentially lower fees. Remember, every dollar saved on fees is a dollar that can contribute to the growth of your retirement savings.

Analyzing Market Performance

Market performance has a significant impact on the value of your 401(k) account. Fluctuations in the stock market can cause your investments to increase or decrease in value. Therefore, analyzing market performance is a critical step in understanding why you might be losing money on your 401(k).

It’s important to remember that the stock market is inherently volatile, and short-term fluctuations are a normal part of investing. However, if your 401(k) consistently underperforms the market over an extended period, it may be worth investigating the reasons behind this lagging performance.

Several factors can contribute to poor market performance. First, the overall economic conditions can have an impact on the stock market. Economic downturns or recessions can lead to a decline in stock prices and lower returns. It’s important to keep an eye on the broader economic indicators, such as GDP growth, employment rates, and inflation, to gauge the potential impact on your 401(k) investments.

Another factor to consider is the performance of specific industries or sectors within the market. Certain sectors may experience turbulence due to changing consumer preferences, technological advancements, or regulatory changes. If your portfolio is heavily concentrated in underperforming sectors, it may be worthwhile to reassess your allocation and consider diversifying your investments across different industries.

Additionally, the performance of individual companies can also impact your 401(k) returns. A company’s financial health, management decisions, and market competition can influence its stock price and, subsequently, the value of your investments. It’s important to monitor the performance and financial reports of the companies you are invested in to assess their potential impact on your portfolio.

Timing is another crucial factor when it comes to market performance. Attempting to time the market and make investment decisions based on short-term market trends can be challenging and often leads to poor results. Instead, a long-term investment approach based on your financial goals and risk tolerance can help navigate market fluctuations more effectively.

Regularly reviewing the market performance and its impact on your 401(k) investments is essential. It’s vital to maintain a balanced and diversified portfolio, stay informed about market trends, and make adjustments as necessary to mitigate potential losses and maximize long-term gains.

Evaluating Contribution Amounts

The amount you contribute to your 401(k) plays a crucial role in the growth and performance of your retirement savings. Evaluating your contribution amounts is essential to ensure that you are on track to meet your long-term financial goals.

One common reason for a decrease in 401(k) value is not contributing enough to the account. If you contribute below the maximum allowed amount or only make minimal contributions, your savings may not grow as quickly as you’d like. It’s important to assess your current contribution level and determine if you can afford to increase it. Even incremental increases in your contributions over time can significantly impact the growth of your retirement savings through the power of compounding.

On the other hand, contributing too much to your 401(k) may also have implications, especially if it results in financial strain or prevents you from addressing other important financial needs. It’s important to strike a balance between saving for retirement and meeting your current financial obligations. Consider speaking with a financial advisor to determine an appropriate contribution amount that aligns with your overall financial circumstances.

Another factor to consider in evaluating contribution amounts is the employer match program. Many employers offer a matching contribution up to a certain percentage of your salary. Failure to contribute at least enough to receive the maximum employer match is essentially leaving free money on the table. Take advantage of the employer match program by contributing at least the amount required to maximize this benefit.

Additionally, it’s important to evaluate your contribution amounts in light of your desired retirement lifestyle and timeline. Consider your retirement goals, estimated expenses, and desired income level during retirement. This can help you gauge if your current contribution amounts are sufficient to meet your objectives. If necessary, make adjustments by increasing your contributions to ensure that you are on track to reach your retirement goals.

Lastly, it’s worth noting that circumstances may change over time, including income level, family size, and financial obligations. Regularly reassessing your contribution amounts can help ensure that your retirement savings align with your evolving financial needs and goals.

By carefully evaluating your contribution amounts and making adjustments as necessary, you can proactively take steps to maximize the growth of your 401(k) and increase your likelihood of achieving a financially secure retirement.

Monitoring and Adjusting Investment Strategies

One key aspect of managing your 401(k) is monitoring and adjusting your investment strategies as needed. The investment landscape is dynamic and ever-changing, and it’s crucial to regularly review and adapt your approach to optimize your returns and mitigate potential losses.

First and foremost, it’s essential to monitor the performance of your investment portfolio. Review the performance of individual funds or asset classes within your 401(k) and assess their contribution to your overall returns. Identify any underperforming investments and consider whether it may be appropriate to reallocate funds to better-performing options.

Regularly reviewing your asset allocation is another critical step in monitoring your investment strategy. Asset allocation refers to the distribution of your investments across different asset classes, such as stocks, bonds, and cash. Over time, market fluctuations can lead to imbalances in your desired asset allocation. Rebalancing your portfolio periodically can help maintain the desired risk and return profile. Consider rebalancing at least once or twice a year or when there are significant market shifts.

In addition to monitoring performance and asset allocation, it’s crucial to stay informed about market trends and developments. Keep up with financial news, industry reports, and expert analysis to gain insights into potential investment opportunities or risks. Stay updated on economic indicators, such as interest rates, inflation, and geopolitical events, which can impact the market and your investment portfolio.

When significant changes occur in your personal life or financial situation, it’s important to reassess your investment strategy. Life events such as marriage, having children, changing jobs, or nearing retirement can warrant adjustments to your risk tolerance, time horizon, and goals. Consider consulting with a financial advisor to ensure that your investment strategy aligns with your evolving needs and objectives.

Lastly, it’s important to be mindful of your emotions and avoid making impulsive decisions based on short-term market fluctuations. Avoid the temptation to buy or sell investments solely based on market volatility. Stick to your long-term investment plan and make adjustments based on data and analysis rather than emotional reactions.

By actively monitoring and adjusting your investment strategies within your 401(k), you can proactively respond to market changes, optimize your returns, and position yourself for long-term success in building and preserving your retirement savings.

Considering Tax Implications

When it comes to managing your 401(k), it’s essential to consider the tax implications associated with your contributions, withdrawals, and overall retirement savings strategy. Understanding and strategically navigating the tax aspects can help you maximize your retirement savings and minimize your tax burden.

Contributions to a traditional 401(k) are made on a pre-tax basis, meaning that the amount you contribute is deducted from your taxable income for the year. This provides an immediate tax advantage as it reduces your overall tax liability. The funds within your 401(k) grow tax-deferred, meaning you won’t pay taxes on any investment gains or distributions until you withdraw the funds during retirement.

However, it’s important to note that when you make withdrawals from a traditional 401(k), they are subject to ordinary income tax. The tax rate you pay on withdrawals will depend on your income level at the time of retirement. It’s crucial to consider your future tax bracket when planning your retirement income strategy and withdrawal schedule.

For individuals looking to potentially reduce their tax burden in retirement, it may be beneficial to consider contributing to a Roth 401(k), if available. Roth 401(k) contributions are made on an after-tax basis, meaning you don’t receive an immediate tax deduction. However, the funds within a Roth 401(k) grow tax-free, and qualified withdrawals in retirement are tax-free as well. By strategically balancing contributions to both traditional and Roth 401(k) accounts, you can create a tax-diversified retirement income strategy.

Another tax consideration is required minimum distributions (RMDs). Once you reach the age of 72, the IRS mandates that you begin taking minimum withdrawals from your traditional 401(k). The amount you must withdraw each year is calculated based on your account balance and life expectancy. Failing to take RMDs or withdrawing less than the required amount can result in hefty penalties. It’s essential to plan for RMDs and consider their impact on your overall tax situation.

In addition to contributions and withdrawals, it’s important to be aware of the potential tax consequences of loans or early withdrawals from your 401(k). While your plan may allow for loans, taking out a 401(k) loan can have tax implications if you fail to repay the loan according to the terms. Additionally, early withdrawals from a 401(k) before the age of 59 ½ are generally subject to income tax and an additional 10% early withdrawal penalty.

It’s highly recommended to consult with a tax advisor or financial planner who can help you navigate the tax implications of your 401(k) and develop a retirement income strategy that aligns with your financial goals and minimizes your tax liability.

By carefully considering the tax implications of your 401(k) contributions, withdrawals, loans, and overall retirement strategy, you can optimize your savings and ensure a more tax-efficient retirement income.

Seeking Professional Advice

Managing a 401(k) and making sound investment decisions can be complex and overwhelming, especially for individuals without extensive knowledge in finance and retirement planning. Seeking professional advice from financial advisors or retirement specialists can provide valuable guidance and expertise to help you navigate the intricacies of your 401(k) and optimize your retirement savings strategy.

A financial advisor can provide personalized guidance tailored to your specific needs and financial goals. They can assess your current financial situation, evaluate your risk tolerance, and help you develop a comprehensive retirement plan. With their expertise, they can provide insights into asset allocation strategies, investment selection, and portfolio diversification to help maximize your returns while minimizing risk.

Furthermore, a financial advisor can help you evaluate your contribution amounts and help determine if you’re on track to meet your retirement goals. They can assess the impact of potential life events or changes in financial circumstances on your retirement savings strategy and make appropriate adjustments accordingly.

In addition to financial advisors, your 401(k) plan provider may offer resources or tools to help you make informed investment decisions. Many plans provide access to online platforms or robo-advisors that offer automated investment advice based on your risk profile and goals.

It’s essential to research and choose a reputable and qualified financial advisor or retirement specialist. Consider their credentials, experience, and track record before engaging their services. Look for professionals who are certified financial planners (CFP®) or have other relevant designations, indicating their expertise and commitment to fiduciary responsibility.

When working with a financial advisor, ensure that you have a clear understanding of their fees, compensation structure, and any potential conflicts of interest. Transparency and open communication are essential for a successful advisor-client relationship.

While seeking professional advice comes at a cost, the potential benefits can outweigh the fees involved. A trusted advisor can provide you with peace of mind, knowing that your 401(k) is being managed in alignment with your long-term goals, and that you have expert guidance on hand to navigate any challenges or market uncertainties that may arise.

Ultimately, seeking professional advice can empower you to make informed decisions, optimize your 401(k) contributions and investment strategies, and increase the chances of achieving a financially secure retirement.

Conclusion

Managing a 401(k) and ensuring its growth and long-term success requires careful attention to various factors. By considering the basics of a 401(k), evaluating investment choices, assessing fees and expenses, analyzing market performance, evaluating contribution amounts, monitoring and adjusting investment strategies, considering tax implications, and seeking professional advice, you can navigate the complexities of retirement planning and increase the likelihood of achieving your financial goals.

While experiencing a loss in your 401(k) balance can be disheartening, it’s important to remember that investing involves risks, and short-term fluctuations are part of the journey. However, by understanding the reasons behind any losses and taking appropriate actions, you can minimize the impact and potentially allow your account to recover and grow.

Regularly assessing your investment choices, diversifying your portfolio, and monitoring market performance will enable you to make informed decisions and adjust your strategy as needed. Additionally, evaluating contribution amounts, taking advantage of employer matches, and considering tax implications will help you maximize your savings potential and minimize your tax obligations.

While you can certainly manage your 401(k) on your own, seeking professional advice from certified financial planners or retirement specialists can provide valuable insights and guidance. They can support you in developing a tailored retirement plan, optimizing your investments, and navigating any challenges that may arise along the way.

Remember, your 401(k) is a long-term investment vehicle designed to provide financial security in retirement. By being proactive, informed, and strategic with your approach, you can position yourself for a fulfilling and financially secure future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance