Finance

Why Does My 401K Fluctuate

Published: October 18, 2023

Learn why your 401K fluctuates and how it can impact your financial stability. Gain insights on managing your finances for a secure future.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding 401K Fluctuations

- Market Volatility and its Impact on 401K

- Economic Factors Influencing 401K Performance

- Investment Allocation and its Effect on 401K Fluctuations

- Employer Contributions and their Role in 401K Fluctuations

- Personal Contributions and their Impact on 401K Performance

- Monitoring and Adjusting Your 401K for Fluctuations

- Conclusion

Introduction

Welcome to the world of 401K investments! If you’re like many working individuals, you’ve probably heard of a 401K and may even have one set up through your employer. A 401K is a retirement savings plan that allows you to set aside a portion of your income and invest it for the future. It’s a great way to save for your golden years and secure your financial future.

However, if you’ve been tracking your 401K account, you may have noticed that its value doesn’t always stay constant. In fact, you might have experienced fluctuations in your 401K balance from time to time. This can be both exciting and nerve-wracking, especially if you don’t understand why it’s happening.

In this article, we will delve into the reasons behind these fluctuations and provide you with a deeper understanding of why your 401K balance goes up and down. By gaining this knowledge, you’ll be better equipped to navigate the ups and downs of the market and make informed decisions about your retirement savings.

So, if you’re ready to demystify the rollercoaster ride of your 401K account, let’s dive into the factors that contribute to its fluctuations.

Understanding 401K Fluctuations

Before we dive into the specifics of 401K fluctuations, let’s start by understanding the basic concept of a 401K. A 401K is a retirement savings account where you contribute a portion of your pre-tax income, which is then invested in a range of assets such as stocks, bonds, and mutual funds. The value of your 401K account is determined by the performance of these investments.

Now, let’s address the elephant in the room – why does your 401K balance fluctuate? The primary reason is that the value of the underlying investments in your account can increase or decrease over time. It’s important to note that market fluctuations are a normal part of investing. Just like any other investment, the value of the assets in your 401K account will fluctuate based on market conditions.

For example, during periods of economic prosperity and market growth, your investments may experience an upward trajectory, resulting in a higher 401K balance. Conversely, during economic downturns or market downturns, the value of your investments may decrease, leading to a lower 401K balance.

It’s also worth mentioning that the asset allocation within your 401K can contribute to fluctuations. If your portfolio is heavily invested in stocks, which have higher volatility compared to bonds or other more stable assets, you may experience more pronounced fluctuations in your 401K balance.

Another factor to consider is the impact of employer contributions and personal contributions. Employer contributions can boost your account balance, while personal contributions help to gradually grow your savings. Both of these factors can play a role in the fluctuations you observe in your 401K balance.

While it’s completely normal for your 401K balance to fluctuate, it’s important to not get too caught up in short-term variations. Remember, a 401K is a long-term investment. As long as you have a well-diversified portfolio and a solid investment strategy in place, you should be well-positioned to weather the ups and downs of the market and achieve your long-term retirement goals.

Now that we have a foundational understanding of why 401K balances fluctuate, let’s explore the specific factors that contribute to these fluctuations.

Market Volatility and its Impact on 401K

Market volatility refers to the rapid and significant price fluctuations in financial markets. It is influenced by various factors such as economic conditions, geopolitical events, and investor sentiment. Market volatility can have a significant impact on the performance of your 401K investments.

During periods of high market volatility, your 401K balance may experience fluctuations, both positive and negative. Sharp price movements in stocks, bonds, and other assets can directly impact the value of your investments. If the market is experiencing a downturn, your 401K balance may decrease. On the other hand, during periods of market growth, your 401K balance may increase.

It’s important to note that market volatility is a natural part of investing. The market can experience periods of extreme volatility, but it tends to correct itself over the long term. Trying to time the market and make investment decisions based on short-term fluctuations can be risky and may negatively impact your long-term returns.

One way to mitigate the impact of market volatility on your 401K is through diversification. By investing in a mix of different asset classes, such as stocks, bonds, and cash, you can spread the risk across your portfolio. This diversification helps to cushion the impact of market fluctuations and can potentially reduce the overall volatility of your 401K investments.

Additionally, it’s important to have a long-term perspective when it comes to your 401K. Market volatility can be unnerving, but it’s crucial to remember that your 401K is a long-term investment vehicle. Historically, the market has shown resilience and has delivered positive returns over the long term.

While it can be tempting to make knee-jerk reactions to market volatility, it’s generally best to stick to your long-term investment strategy and avoid making impulsive investment decisions. Attempting to time the market and make short-term moves can result in missed opportunities and may harm your overall investment performance.

In summary, market volatility is a common occurrence in financial markets and can have an impact on your 401K balance. By diversifying your investments and maintaining a long-term perspective, you can navigate market volatility and position yourself for long-term success in your retirement savings.

Economic Factors Influencing 401K Performance

The performance of your 401K is closely tied to the broader economic landscape. Various economic factors can impact the value and returns of your 401K investments. Understanding these factors can provide insights into the potential fluctuations in your 401K balance.

One important economic factor is interest rates. When interest rates are low, it can stimulate economic growth and benefit certain sectors of the market, such as housing and consumer spending. This can have a positive impact on the performance of your 401K investments, especially if you have exposure to those sectors. However, if interest rates rise, it can lead to a decrease in the value of certain assets, such as bonds. This can result in fluctuations in your 401K balance.

Another economic factor to consider is inflation. Inflation refers to the general increase in prices of goods and services over time. When inflation is low and stable, it is generally conducive to economic growth. However, if inflation spikes, it can erode the purchasing power of your retirement savings. This can potentially lead to a decrease in your 401K balance or lower returns on your investments.

Economic indicators, such as GDP growth, job market conditions, and consumer sentiment, can also impact the performance of your 401K. Positive economic indicators, such as robust economic growth and low unemployment rates, can drive up stock prices and contribute to the growth of your 401K balance. Conversely, negative economic indicators can result in market downturns and fluctuations in your 401K investments.

Global events and geopolitical factors can also influence the performance of your 401K. For example, political instability, trade tensions, or natural disasters can create uncertainty in the markets and lead to increased volatility. Keeping an eye on these external factors can help you understand why your 401K balance may be fluctuating.

While economic factors play a significant role in 401K performance, it’s worth emphasizing that long-term trends are more important than short-term fluctuations. Economic conditions can change over time, and attempting to time the market based on short-term economic factors can be challenging and risky.

Instead, focus on maintaining a well-diversified portfolio aligned with your long-term investment goals. By spreading your investments across different asset classes and sectors, you can reduce the impact of economic fluctuations on your 401K balance and position yourself for long-term success.

Stay informed about economic trends and consult with a financial advisor to ensure your investment strategy aligns with your risk tolerance and long-term financial goals.

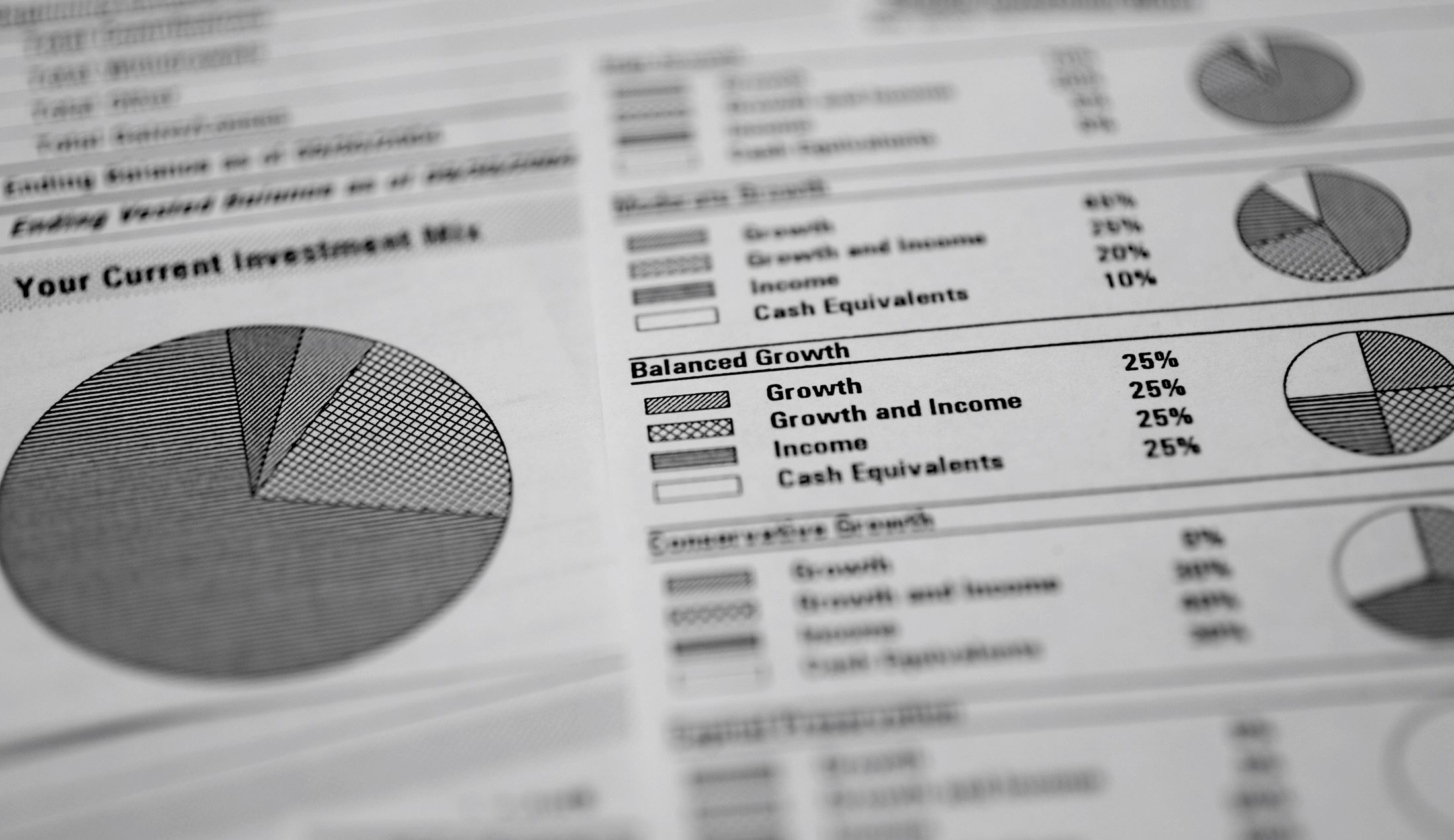

Investment Allocation and its Effect on 401K Fluctuations

One of the key factors that can contribute to fluctuations in your 401K balance is your investment allocation. Investment allocation refers to the distribution of your retirement savings across different asset classes, such as stocks, bonds, and cash. The specific allocation you choose can have a significant impact on the performance and volatility of your 401K investments.

If you have a higher allocation to stocks in your 401K, you may experience more pronounced fluctuations in your account balance. Stocks are generally considered more volatile than bonds or cash investments. While they offer the potential for higher returns, they also come with a higher level of risk. As a result, during periods of market volatility, the value of your stock investments may fluctuate more significantly.

On the other hand, if you have a higher allocation to bonds or cash, your 401K balance may be less susceptible to market fluctuations. Bonds are generally considered more stable than stocks and can act as a buffer during times of market volatility. Cash investments, such as money market funds, are typically the most stable but offer lower potential returns compared to stocks and bonds.

It’s important to note that the appropriate investment allocation for your 401K depends on several factors, including your risk tolerance, time horizon, and financial goals. If you have a longer time horizon until retirement and can tolerate higher levels of risk, a higher allocation to stocks may be appropriate. Conversely, if you have a shorter time horizon or a lower risk tolerance, a more conservative allocation with a higher proportion of bonds or cash may be suitable.

Regularly reviewing and rebalancing your investment allocation is essential to ensure it aligns with your goals and risk tolerance. Over time, as certain asset classes outperform or underperform others, your allocation may shift. Rebalancing involves selling or buying assets to realign your portfolio with your target allocation. This process helps to manage risk and maintain a consistent level of diversification.

By regularly rebalancing your 401K investments, you can mitigate the impact of fluctuations caused by a specific asset class’s performance. It allows you to buy assets that have experienced lower returns and sell assets that have performed well, thereby maintaining a disciplined approach to investing.

Ultimately, your investment allocation plays a significant role in determining the level of fluctuations in your 401K balance. By carefully considering your risk tolerance, time horizon, and periodically rebalancing your portfolio, you can better manage the volatility and position yourself for long-term growth.

Employer Contributions and their Role in 401K Fluctuations

Employer contributions play a crucial role in your 401K and can have an impact on its fluctuations. Many employers offer matching contributions, which means they will contribute a certain percentage of your salary to your 401K account based on the amount you contribute. The presence of employer contributions can help boost your 401K balance and potentially mitigate fluctuations caused by market volatility.

When your employer makes contributions to your 401K, it adds to the overall value of your account. This infusion of funds can help offset any fluctuations in your personal contributions or the performance of your investment portfolio. Employer contributions can provide a consistent source of growth, which can help smooth out the impact of market fluctuations on your 401K balance.

Additionally, employer contributions are typically made on a regular basis, such as with each paycheck. This regularity helps to provide a stable stream of funds into your 401K account, regardless of market conditions. It can act as a cushion during times of market downturns, helping to support the value of your account when investment performance may be impacted.

However, it’s important to note that employer contributions are subject to certain conditions, such as vesting schedules. Vesting refers to the period of time you must work for your employer before you are entitled to the full amount of their contributions. If you leave your job before you are fully vested, you may forfeit a portion of the employer contributions. Understanding the vesting schedule and requirements set by your employer is crucial to maximizing the benefits of employer contributions.

Employer contributions can vary depending on the company’s policies and the terms of your employment. Some employers may offer a dollar-for-dollar match, while others may have a cap or a different formula for determining their contributions. It’s important to be aware of your employer’s specific contribution guidelines, as this can impact the overall growth and fluctuations of your 401K balance.

In summary, employer contributions can play a significant role in your 401K and its fluctuations. The regularity and additional funds provided by employer contributions can help support the value of your account, especially during times of market volatility. Understanding the specifics of your employer’s contribution policy and vesting requirements is essential for maximizing the benefits of employer contributions.

Personal Contributions and their Impact on 401K Performance

Personal contributions are a key component of your 401K and can have a significant impact on its performance. Your personal contributions are the funds that you contribute to your 401K account from your own income. These contributions serve as the foundation for building your retirement savings and play a critical role in determining the growth and fluctuations of your 401K balance.

By making regular and consistent personal contributions, you are investing in your future and taking advantage of the power of compounding. Compounding allows your contributions to grow over time, as both the contributions and any investment returns earn additional returns. The more you contribute, the more your 401K balance can grow, assuming your investments perform well.

Your personal contributions also provide a measure of control over your 401K performance. By increasing your contributions, you can potentially accelerate the growth of your account and increase your retirement savings. Conversely, reducing or pausing your contributions may slow down the growth of your 401K balance.

During times of market volatility, personal contributions can help to offset the impact of fluctuations. By consistently contributing to your 401K, you continue to invest in the market, regardless of short-term market movements. This approach, known as dollar-cost averaging, helps to smooth out the impact of market fluctuations and can potentially lead to better long-term investment returns.

Moreover, personal contributions can help you take advantage of market downturns. When the market experiences a decline, stock prices may be lower, presenting potential buying opportunities. By continuing to contribute during these periods, you can purchase more shares at a lower cost. As the market recovers, these additional shares have the potential to grow in value and contribute to the overall growth of your 401K balance.

It’s important to note that personal contributions to your 401K are subject to contribution limits set by the Internal Revenue Service (IRS). These limits determine the maximum amount you can contribute to your 401K each year. It’s advisable to consult with a financial advisor or review IRS guidelines to ensure you are maximizing your personal contributions while staying within the legal limits.

In summary, personal contributions are a critical component of your 401K performance. They provide the foundation for building your retirement savings and have a direct impact on the growth and fluctuations of your 401K balance. By making regular and consistent contributions, you can take control of your financial future and position yourself for a comfortable retirement.

Monitoring and Adjusting Your 401K for Fluctuations

Monitoring and adjusting your 401K is an important aspect of managing its fluctuations and maximizing its performance. While it’s natural for your 401K balance to fluctuate over time, taking proactive steps to monitor and adjust your investments can help ensure you stay on track with your retirement goals.

The first step in effectively managing the fluctuations of your 401K is to regularly monitor its performance. This involves reviewing your account statements, tracking the performance of your investments, and keeping an eye on market trends. By staying informed, you can gauge how your 401K is performing and identify any significant fluctuations or trends in its value.

When monitoring your 401K, it’s important to keep a long-term perspective. Avoid making knee-jerk reactions to short-term fluctuations. Instead, focus on the overall trend and ensure that your investment strategy aligns with your long-term goals. Remember, a well-diversified and properly allocated portfolio is designed to weather market fluctuations and deliver returns over the long term.

Periodically assessing your investment allocation is another critical step in managing 401K fluctuations. Review your asset allocation and consider whether it still aligns with your risk tolerance and financial goals. If necessary, rebalance your portfolio to maintain a diversified mix of investments. This involves selling assets that have performed well and buying assets that have underperformed to bring your portfolio back in line with your desired allocation.

Rebalancing can help manage the fluctuations caused by one asset class’s performance while ensuring that your portfolio remains aligned with your risk preferences. Keep in mind that rebalancing should be done strategically and not in response to short-term market movements. Consider consulting with a financial advisor to determine the best approach for rebalancing your 401K.

Regularly reviewing your contributions is another aspect of managing 401K fluctuations. Assess if your personal contributions are sufficient and whether you can increase them to further bolster your retirement savings. Take advantage of any employer matching contributions available to you, as these can provide a valuable boost to your 401K balance.

Lastly, it’s important to stay informed and keep up with developments that could impact your 401K. This includes staying informed about changes in tax laws, market trends, and economic conditions. Consider consulting with a financial advisor who can provide guidance tailored to your specific circumstances and help you make informed decisions about your 401K.

In summary, monitoring and adjusting your 401K is a proactive way to manage its fluctuations and maximize its performance. Regularly monitor its performance, assess your investment allocation, review your contributions, and stay informed about market trends. By taking these steps, you can stay on track towards achieving your long-term retirement goals.

Conclusion

Fluctuations in your 401K balance are a natural part of investing, influenced by factors such as market volatility, economic conditions, investment allocation, and personal contributions. While these fluctuations may cause some concern, it’s important to maintain a long-term perspective and stay focused on your retirement goals.

Understanding the reasons behind 401K fluctuations can help you navigate the ups and downs of the market more effectively. Market volatility is a normal occurrence, and trying to time the market based on short-term fluctuations can be risky. Instead, focus on maintaining a well-diversified portfolio aligned with your risk tolerance and long-term objectives.

Economic factors, such as interest rates and inflation, can also impact 401K performance. By staying informed about economic indicators and remaining adaptable to market conditions, you can position your 401K for success.

Investment allocation plays a crucial role in determining the level of fluctuations in your 401K balance. Regularly reviewing and rebalancing your portfolio can help manage risk and ensure your investments align with your long-term goals.

Employer contributions provide stability and can help mitigate fluctuations in your 401K balance. Taking advantage of employer matches and understanding vesting schedules can maximize the benefits of employer contributions.

Personal contributions are a key component of your 401K and serve as the foundation for building your retirement savings. By making regular and consistent contributions, you can take control of your financial future and potentially offset the impact of market fluctuations.

Monitoring and adjusting your 401K is essential to managing fluctuations and maximizing performance. Regularly review your account, assess your investment allocation, and stay informed about market trends. By taking proactive steps, you can navigate the fluctuations and stay on track towards your retirement goals.

In conclusion, while 401K fluctuations can be unnerving at times, they are a natural part of the investing process. By understanding the factors that contribute to these fluctuations and taking a disciplined approach to managing your 401K, you can set yourself up for long-term success and a secure financial future in retirement.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance