Finance

Why Is My APR So High?

Published: March 3, 2024

Discover why your APR may be higher than expected and get expert finance tips to lower it. Understand the factors affecting your finance rates.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Understanding APR: Why Is My APR So High?

Introduction

When it comes to managing your finances, understanding the factors that contribute to the cost of borrowing is crucial. One of the key elements in this equation is the Annual Percentage Rate (APR), which plays a significant role in determining the total amount you’ll pay for borrowing funds. If you’ve ever found yourself wondering, “Why is my APR so high?” you’re not alone. Many individuals encounter this question as they navigate the world of credit cards, loans, and other financial products.

APR represents the annual cost of borrowing money, including both the interest rate and any additional fees associated with the loan. Whether you’re applying for a credit card, mortgage, auto loan, or personal loan, the APR directly impacts the overall expense of borrowing. It’s essential to comprehend the various factors influencing APR and how they can lead to higher or lower rates.

Throughout this article, we’ll delve into the intricacies of APR, shedding light on the reasons behind high APRs and providing insights into how you can potentially lower these rates. By gaining a deeper understanding of APR, you’ll be better equipped to make informed financial decisions and take proactive steps to manage your borrowing costs effectively.

Understanding APR

Annual Percentage Rate (APR) serves as a comprehensive metric for evaluating the cost of borrowing, encompassing not only the interest rate but also any additional fees and charges associated with the loan. Unlike the nominal interest rate, which solely reflects the interest percentage, the APR presents a more holistic view of the total borrowing expense. This figure is crucial for consumers as it enables them to compare the actual cost of different financial products, such as credit cards and loans, offered by various lenders.

When analyzing APR, it’s important to recognize that it includes not only the interest charged on the principal amount but also any origination fees, points, and other costs. By factoring in these additional expenses, the APR provides a more accurate representation of the total cost of borrowing. This transparency empowers consumers to make well-informed decisions, allowing them to assess the true affordability of a loan or credit card.

Furthermore, understanding the distinction between fixed and variable APR is crucial. While a fixed APR remains constant throughout the loan term, a variable APR is subject to fluctuations based on changes in an underlying benchmark, such as the prime rate. This variation can impact the total interest paid over time, highlighting the importance of carefully evaluating the terms and conditions associated with different APR structures.

By comprehending the intricacies of APR, borrowers can gain clarity regarding the actual cost of their loans and credit cards, enabling them to make prudent financial choices. In the subsequent sections, we’ll explore the factors that influence APR, the impact of credit scores on APR determination, and actionable tips for lowering APR to effectively manage borrowing costs.

Factors Affecting APR

Several key factors influence the determination of Annual Percentage Rates (APRs) across different financial products. Understanding these factors is essential for borrowers seeking to comprehend the rationale behind the APR assigned to their loans or credit cards. By gaining insight into these determinants, individuals can navigate the borrowing landscape more effectively and make informed decisions regarding their financial commitments.

1. Credit Risk: Lenders assess the credit risk associated with each borrower, considering factors such as credit score, payment history, and outstanding debt. Borrowers with lower credit scores or a history of delinquencies may be deemed riskier, resulting in higher APRs to offset the increased potential for default.

2. Economic Conditions: The prevailing economic environment can impact APRs, especially for variable-rate loans. Changes in the prime rate, inflation, and overall market conditions can influence the cost of borrowing, leading to fluctuations in APRs for variable-rate products.

3. Loan Term: The duration of the loan or credit card balance transfer period can impact the APR. Typically, longer loan terms may entail higher APRs, reflecting the extended period of risk for the lender.

4. Type of Loan: The nature of the loan, whether it’s a mortgage, auto loan, personal loan, or credit card, can significantly affect the APR. Secured loans, backed by collateral, often carry lower APRs compared to unsecured loans, which pose greater risk for lenders.

5. Lender’s Policies: Each lender may have distinct underwriting criteria and risk assessment methodologies, leading to variations in APRs across different financial institutions. Additionally, promotional offers and loyalty programs may influence the APR offered to borrowers.

By recognizing these influential factors, borrowers can gain a deeper understanding of the APR assigned to their financial products. In the subsequent sections, we’ll explore the impact of credit scores on APR determination and provide actionable tips for lowering APR to effectively manage borrowing costs.

Impact of Credit Score

One of the most influential factors affecting the Annual Percentage Rate (APR) assigned to loans and credit cards is the borrower’s credit score. Your credit score serves as a numerical representation of your creditworthiness, reflecting your history of managing credit and debt. Lenders rely on this score to assess the level of risk associated with extending credit to an individual, thereby influencing the APR offered.

Higher Credit Score: Individuals with excellent credit scores typically receive more favorable APRs. Lenders perceive these borrowers as lower risk due to their demonstrated history of responsible credit management. As a result, they are often eligible for lower APRs, translating to reduced borrowing costs over the loan term.

Lower Credit Score: Conversely, individuals with lower credit scores may encounter higher APRs. Lenders may view these borrowers as higher risk, leading to the imposition of elevated APRs to mitigate the potential for default. This can result in increased overall borrowing expenses for individuals with less favorable credit scores.

It’s important to note that the impact of credit scores on APR determination extends across various financial products, including mortgages, auto loans, personal loans, and credit cards. Additionally, the utilization of risk-based pricing allows lenders to tailor APRs based on individual credit profiles, emphasizing the significance of maintaining a healthy credit score.

Monitoring your credit score and taking proactive steps to improve it can significantly influence the APRs available to you. By consistently managing your finances, making timely payments, and minimizing outstanding debt, you can enhance your creditworthiness and potentially qualify for lower APRs, ultimately reducing the cost of borrowing.

As we delve deeper into the realm of APR, we’ll explore the comparison of different APRs across financial products and provide actionable tips for lowering APR to effectively manage borrowing costs.

Comparison of Different APRs

When navigating the landscape of financial products, it’s essential to compare the Annual Percentage Rates (APRs) offered by various lenders to make informed borrowing decisions. Whether you’re considering credit cards, mortgages, auto loans, or personal loans, understanding the nuances of APRs across different products is crucial for evaluating the total cost of borrowing.

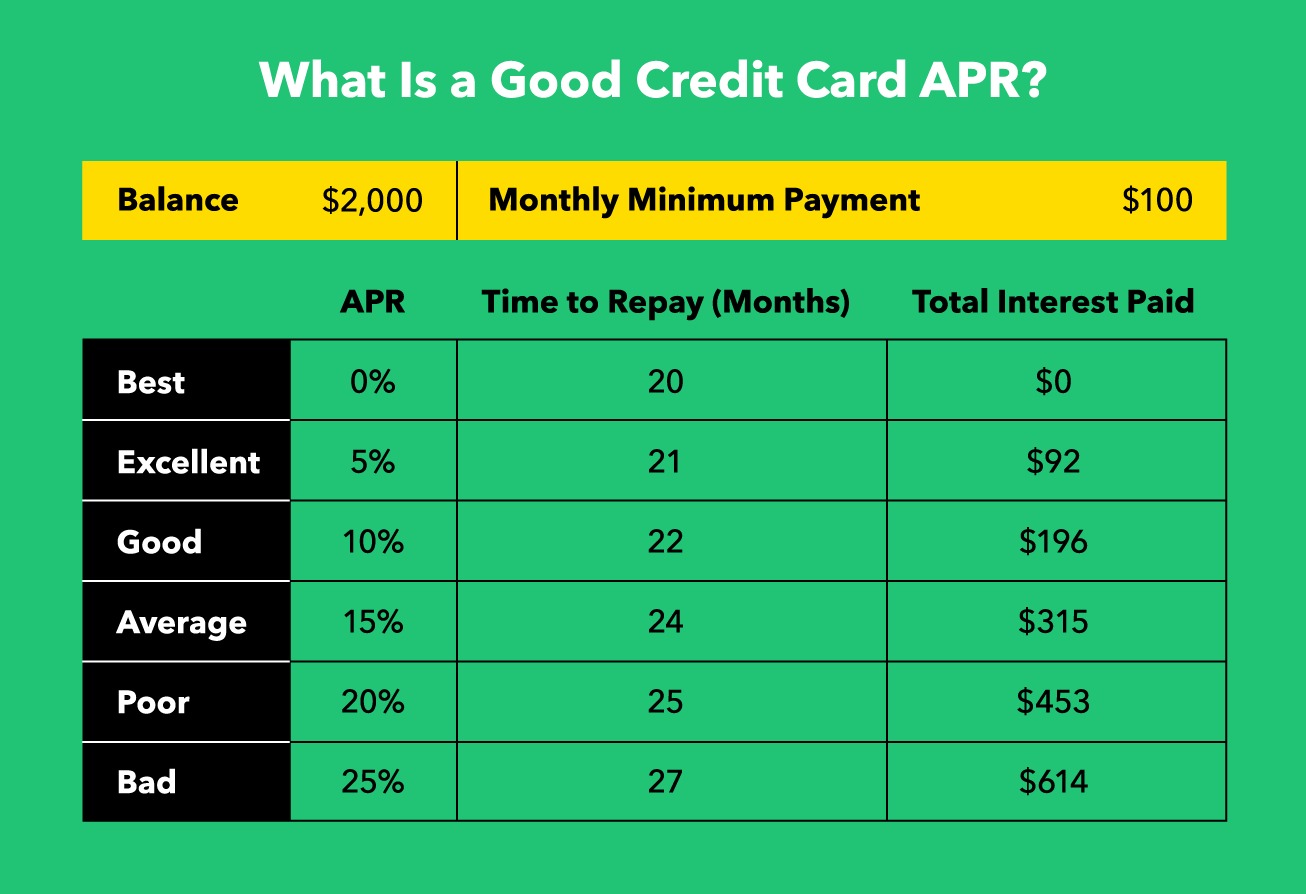

Credit Cards: Credit card APRs can vary widely, encompassing introductory rates, standard purchase APRs, balance transfer APRs, and cash advance APRs. Introductory rates may entice with low or 0% APRs for a limited period, while standard purchase APRs typically range from single to double digits based on the cardholder’s creditworthiness.

Mortgages: Mortgage APRs reflect the total cost of borrowing, incorporating the interest rate, points, and other fees. Fixed-rate mortgages offer stable APRs throughout the loan term, while adjustable-rate mortgages (ARMs) may feature lower initial APRs that adjust periodically based on market conditions.

Auto Loans: APRs for auto loans are influenced by factors such as the borrower’s credit score, the loan term, and the vehicle’s age. New car loans often feature lower APRs compared to used car loans, and borrowers with strong credit profiles may qualify for more competitive rates.

Personal Loans: APRs for personal loans can vary based on the lender, the loan amount, and the borrower’s creditworthiness. Secured personal loans, backed by collateral, may offer lower APRs, while unsecured personal loans typically carry higher APRs due to the absence of collateral.

By comparing the APRs across different financial products, borrowers can gain clarity regarding the total cost of borrowing and identify the most cost-effective options. It’s important to consider not only the APR but also any additional fees, repayment terms, and potential fluctuations in variable APRs when evaluating financial products.

In the following section, we’ll provide actionable tips for lowering APR, empowering borrowers to effectively manage their borrowing costs and optimize their financial wellness.

Tips for Lowering APR

Lowering the Annual Percentage Rate (APR) on your loans and credit cards can lead to substantial savings over time. By implementing strategic measures and leveraging your financial profile, you can potentially secure more favorable APRs, reducing the overall cost of borrowing. Here are actionable tips for lowering your APR:

- Enhance Your Credit Score: Improving your credit score can significantly impact the APRs available to you. Consistently managing your credit accounts, making timely payments, and minimizing credit utilization can enhance your creditworthiness, potentially qualifying you for lower APRs.

- Negotiate with Lenders: Engage with your current lenders to negotiate for lower APRs. Highlighting your positive payment history and creditworthiness may prompt lenders to reevaluate your APR, especially if you’ve received competing offers with more favorable rates.

- Consider Balance Transfer Offers: For credit card balances, explore balance transfer offers that provide introductory periods with low or 0% APRs. Transferring high-interest balances to these promotional offers can help you save on interest and expedite debt repayment.

- Explore Refinancing Options: For existing loans, such as mortgages and auto loans, consider refinancing to secure lower APRs. Changes in market conditions or improvements in your credit profile may make refinancing a viable strategy for reducing borrowing costs.

- Opt for Secured Loans: When feasible, opting for secured loans backed by collateral can lead to lower APRs. Lenders may offer more competitive rates for secured loans, leveraging the reduced risk associated with collateralized borrowing.

- Stay Informed About Promotional Rates: Keep abreast of promotional APR offers from financial institutions. These limited-time promotions can provide opportunities to access lower APRs, especially for credit cards and personal loans.

By proactively implementing these tips, you can potentially lower your APRs, effectively managing your borrowing costs and optimizing your financial well-being. It’s important to assess the feasibility and impact of each strategy based on your unique financial circumstances and goals.

As you navigate the realm of APR and borrowing, leveraging these tips can empower you to make informed financial decisions and maximize the value of your credit and loan products.

Conclusion

Understanding the intricacies of Annual Percentage Rates (APRs) is paramount for individuals navigating the realm of borrowing and credit. The APR serves as a comprehensive metric, encapsulating not only the interest rate but also additional fees and charges associated with loans and credit cards. By comprehending the factors influencing APR, borrowers can make informed decisions, effectively managing their borrowing costs and optimizing their financial well-being.

Factors such as credit risk, economic conditions, loan terms, loan types, and lender policies play pivotal roles in APR determination, underscoring the need for borrowers to assess the total cost of borrowing across different financial products. Furthermore, the impact of credit scores on APRs highlights the significance of maintaining a healthy credit profile to potentially secure more favorable borrowing terms.

Comparing APRs across credit cards, mortgages, auto loans, and personal loans enables individuals to identify cost-effective borrowing options, empowering them to make informed financial decisions. Additionally, implementing strategic measures such as enhancing credit scores, negotiating with lenders, and exploring promotional offers can potentially lead to lower APRs, resulting in substantial savings over time.

By leveraging these insights and actionable tips, borrowers can proactively manage their borrowing costs, mitigate financial stress, and work towards achieving their long-term financial goals. Ultimately, a comprehensive understanding of APR empowers individuals to make prudent borrowing decisions, optimize their financial resources, and pave the way for sustained financial wellness.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance