Home>Finance>Covered Interest Rate Parity: Definition, Calculation, And Example

Finance

Covered Interest Rate Parity: Definition, Calculation, And Example

Published: November 4, 2023

Learn about covered interest rate parity in finance, including its definition, calculation, and example. Understand how this concept impacts financial markets.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Covered Interest Rate Parity: Definition, Calculation, and Example

As part of our Finance category, we are diving into the concept of Covered Interest Rate Parity (CIRP). In this blog post, we will provide a clear definition of CIRP, explain how to calculate it, and provide a practical example to help you better understand its application. By the end of this article, you will have a solid foundation in CIRP and be able to apply it to real-world financial scenarios.

Key Takeaways:

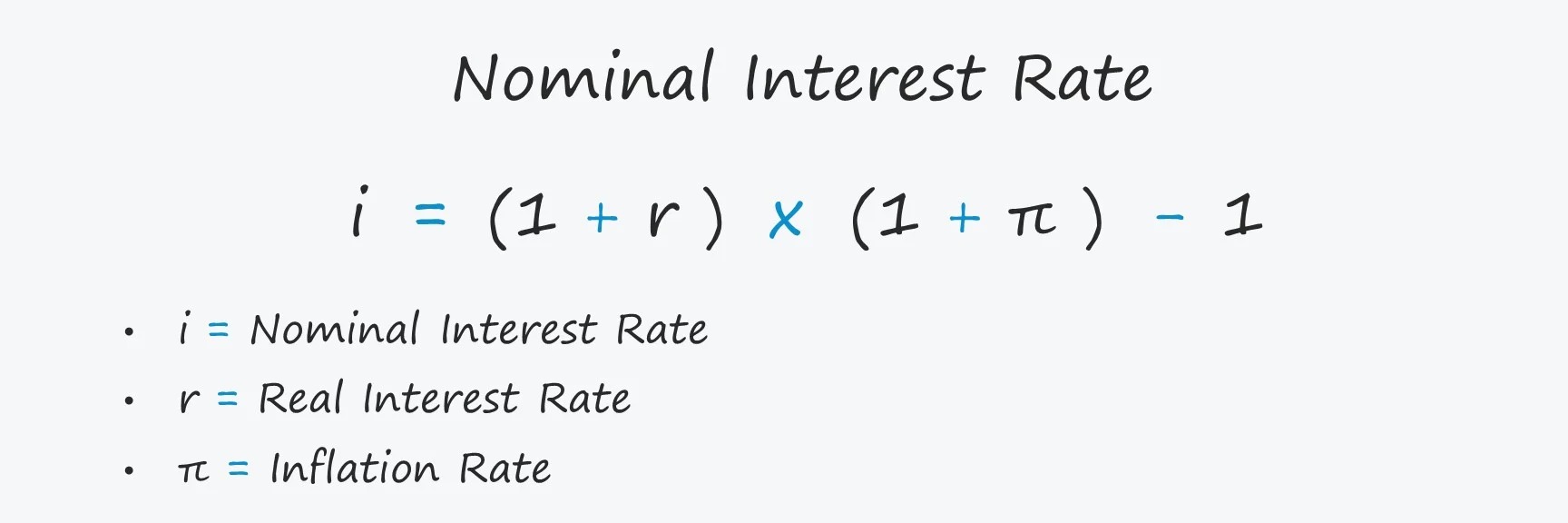

- Covered Interest Rate Parity (CIRP) is an economic principle that establishes a relationship between interest rates and exchange rates.

- CIRP states that the difference in interest rates between two countries should equal the difference in the forward exchange rate and the spot exchange rate.

What is Covered Interest Rate Parity (CIRP)?

Covered Interest Rate Parity (CIRP) is a fundamental principle in international finance that establishes a relationship between interest rates and exchange rates in a global market. It is based on the concept of arbitrage, which assumes that market participants will take advantage of any discrepancies in pricing to make risk-free profits.

Essentially, CIRP states that the difference in interest rates between two countries should equal the difference in the forward exchange rate and the spot exchange rate. In simple terms, it suggests that the interest rate differential between two countries should be offset by the expected change in the exchange rate over a given period.

How to Calculate Covered Interest Rate Parity?

- Identify the interest rates of two countries involved in the transaction: the domestic country (where you reside) and the foreign country (where the investment is made).

- Find the spot exchange rate, which is the current exchange rate between the two currencies.

- Determine the forward exchange rate, which is the exchange rate agreed upon for a future date.

- Calculate the interest rate differential by subtracting the domestic interest rate from the foreign interest rate.

- Calculate the expected change in the exchange rate by multiplying the interest rate differential by the length of the investment period.

- Finally, compare the expected change in the exchange rate to the difference between the forward and spot exchange rates. If they are not equal, there may be an arbitrage opportunity.

Example of Covered Interest Rate Parity

Let’s consider an example to illustrate how Covered Interest Rate Parity works:

Assume you’re an investor in the US, and you have $10,000 that you want to invest in a fixed deposit for one year. In this example:

- The US interest rate is 2%.

- The interest rate in the foreign country (where you want to invest) is 4%.

- The current spot exchange rate is 1 USD = 1.25 Foreign Currency.

- The forward exchange rate for one year is set at 1 USD = 1.27 Foreign Currency.

Let’s calculate the Covered Interest Rate Parity:

- Interest rate differential = 4% (Foreign interest rate) – 2% (Domestic interest rate) = 2%.

- Expected change in the exchange rate = 2% (Interest rate differential) * 1 year = 2%.

- Difference between forward and spot exchange rates = 1.27 (Forward rate) – 1.25 (Spot rate) = 0.02.

Since the expected change in the exchange rate (2%) is equal to the difference between the forward and spot exchange rates (0.02), there is no arbitrage opportunity according to Covered Interest Rate Parity.

Understanding Covered Interest Rate Parity is crucial in international finance as it helps investors evaluate potential gains or losses from investments in different countries. By applying this concept, investors can make informed decisions and assess the risks associated with currency fluctuations.

In conclusion, Covered Interest Rate Parity (CIRP) provides a framework for understanding the relationship between interest rates and exchange rates. By calculating the interest rate differential and comparing it to the expected change in the exchange rate, investors can identify opportunities for potential arbitrage. Utilizing CIRP can contribute to more informed decision-making in international investments and enhance overall financial strategies.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: Chelsea • Finance

By: • Finance

By: • Finance