Home>Finance>Uncovered Interest Rate Parity (UIP): Definition And Calculation

Finance

Uncovered Interest Rate Parity (UIP): Definition And Calculation

Published: February 12, 2024

Discover the concept of Uncovered Interest Rate Parity (UIP) in finance, including its definition and calculation methods. Enhance your understanding of global currency markets and interest rate differentials.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Uncovered Interest Rate Parity (UIP): Definition and Calculation

Welcome to our “Finance” category where we delve into various concepts and strategies to help you strengthen your understanding of the financial world. In this blog post, we will explore an important concept called Uncovered Interest Rate Parity (UIP). We’ll define UIP, explain its calculation, and discuss its significance in the world of finance. So, let’s dive right in!

Key Takeaways:

- Uncovered Interest Rate Parity (UIP) compares the expected returns on two different currencies in order to determine potential fluctuations in exchange rates.

- The UIP formula states that the difference in interest rates between two countries should be equal to the expected change in the exchange rate.

Understanding Uncovered Interest Rate Parity (UIP)

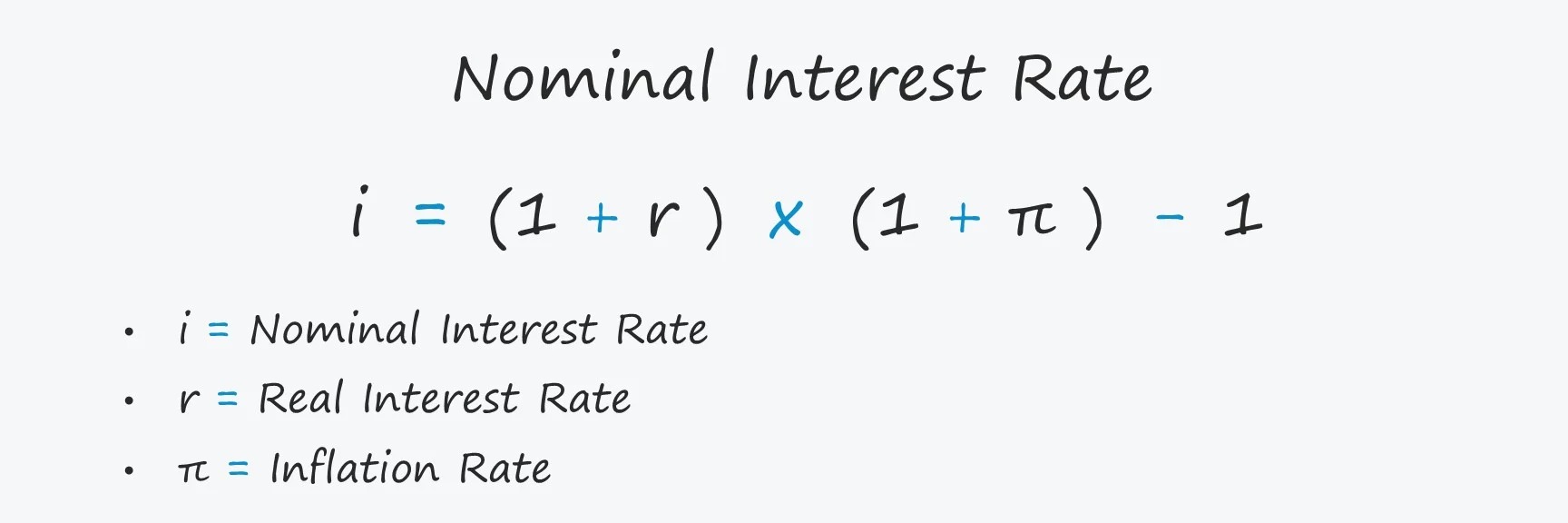

Uncovered Interest Rate Parity is a theory that links interest rates, inflation rates, and exchange rates. It suggests that the difference in interest rates between two countries should be equal to the expected change in the exchange rate. In other words, the theory assumes that investors are risk-neutral and base their investment decisions solely on expected returns.

The calculation for Uncovered Interest Rate Parity involves comparing the expected returns on two different currencies. Here’s a step-by-step breakdown:

- Identify the interest rates on two currencies: Start by determining the interest rates offered by two countries. Let’s consider an example with Country A and Country B.

- Calculate the interest rate differential: Subtract the interest rate of Country A from the interest rate of Country B. This gives you the interest rate differential.

- Factor in the expected change in the exchange rate: Multiply the interest rate differential by the expected change in the exchange rate between the two currencies.

- Compare the expected returns: If the calculated value matches the expected returns on the currencies, the uncovered interest rate parity holds true.

Significance of Uncovered Interest Rate Parity (UIP)

Uncovered Interest Rate Parity is an important tool for investors and traders in the forex market. Here’s why it’s significant:

- Forecasting exchange rate movements: By using UIP, investors can make predictions about potential fluctuations in exchange rates. This knowledge can guide investment decisions and hedging strategies.

- Evaluating interest rate differentials: UIP helps assess whether an interest rate differential is accurately priced into exchange rates. If the market deviates from the UIP expectations, there may be opportunities for profit through arbitrage.

- Studying macroeconomic factors: By examining the UIP deviations, economists can gain insights into various macroeconomic factors that affect currency valuations, such as inflation rates and monetary policy.

In conclusion, Uncovered Interest Rate Parity is a concept that allows investors and economists to analyze the relationship between interest rates and exchange rates. By understanding and applying UIP, one can gain valuable insights into the potential movements of currencies in the global marketplace. So, go ahead and explore the world of UIP, as it may unlock new opportunities for financial success!

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance