Home>Finance>Ending Inventory: Definition, Calculation, And Valuation Methods

Finance

Ending Inventory: Definition, Calculation, And Valuation Methods

Published: November 18, 2023

Learn about ending inventory in finance, including its definition, calculation methods, and valuation techniques.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Understanding Ending Inventory: Definition, Calculation, and Valuation Methods

Welcome to the world of inventory management! If you’re a business owner or an accounting professional, you know how crucial it is to manage your inventory effectively. One key aspect of inventory management is understanding and calculating your ending inventory. In this article, we will dive deep into the definition of ending inventory, how to calculate it, and the various valuation methods used. So let’s get started!

Key Takeaways:

- Ending inventory represents the value of the remaining unsold goods at the end of an accounting period.

- Calculate ending inventory by taking the total inventory at the beginning of the period, adding purchases, and subtracting the cost of goods sold.

What is Ending Inventory?

Ending inventory, also known as closing inventory, refers to the value of the goods or products that remain unsold at the end of an accounting period. It represents the stock that a company still holds and plans to sell in the future. This inventory value is an important figure for various financial ratios, such as the gross profit margin, and is crucial for accurate financial reporting.

To better understand ending inventory, let’s break down the calculation process and explore the various valuation methods used.

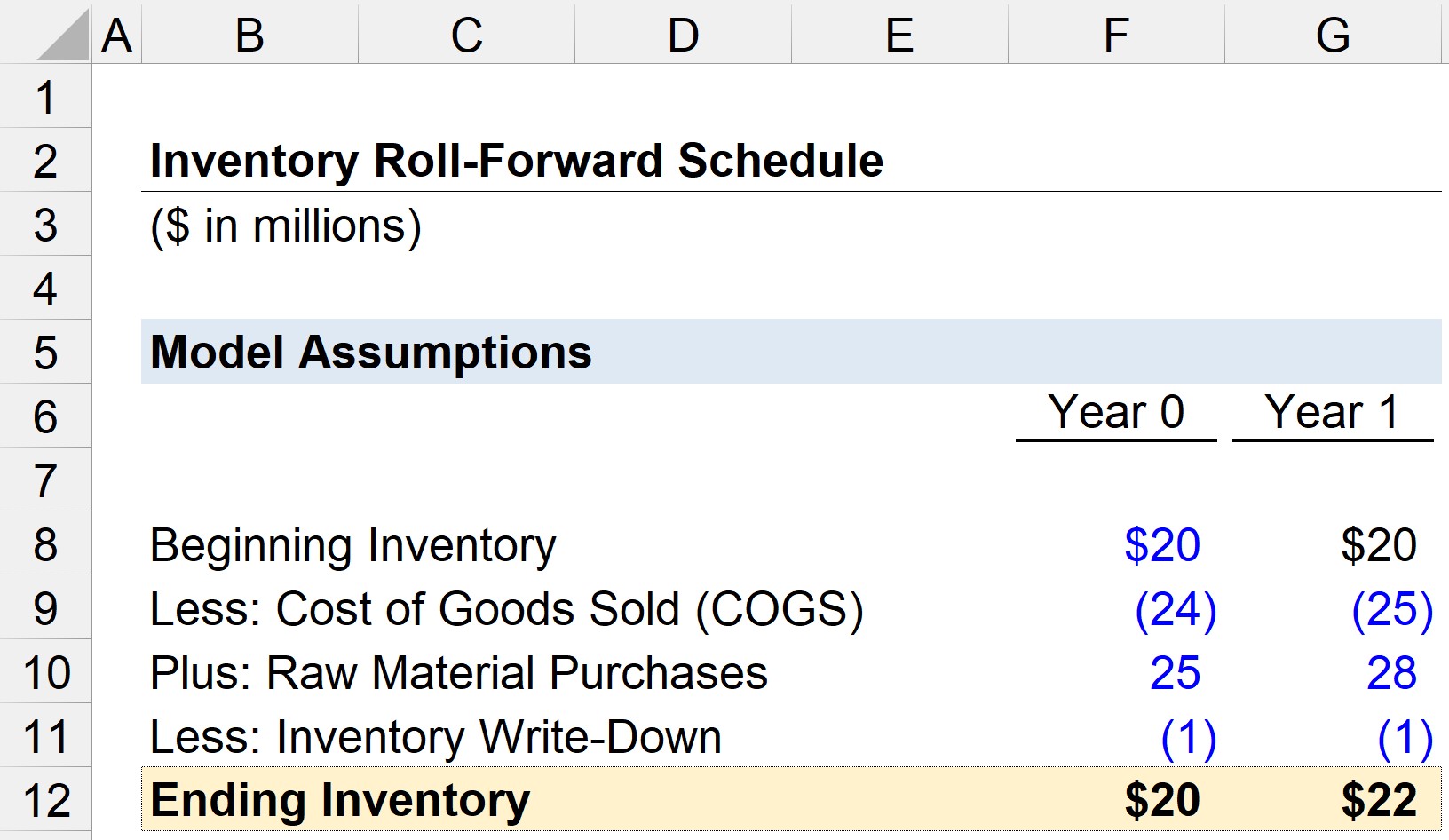

How to Calculate Ending Inventory

Calculating ending inventory involves a simple calculation that takes into account the value of the beginning inventory, purchases made during the period, and the cost of goods sold (COGS). Here’s the formula:

Ending Inventory = Beginning Inventory + Purchases – Cost of Goods Sold

Let’s break it down further:

- Beginning Inventory: This represents the value of the inventory at the start of the accounting period. It includes the cost of all the goods available for sale.

- Purchases: This refers to any additional inventory acquired during the accounting period. It includes the cost of goods purchased or manufactured.

- Cost of Goods Sold (COGS): This represents the cost of the goods that have been sold during the accounting period. It includes the direct cost of production or purchase, such as raw materials, labor, and overhead expenses.

By subtracting the COGS from the sum of the beginning inventory and purchases, we arrive at the ending inventory value. This figure represents the remaining value of the inventory that has not yet been sold.

Valuation Methods for Ending Inventory

When it comes to valuing ending inventory, there are several methods businesses can use. Let’s explore the three most common valuation methods:

- FIFO (First-In, First-Out): This method assumes that the first goods purchased or produced are the first to be sold. So, the cost of the oldest inventory is matched with the cost of goods sold, while the newest inventory is valued in the ending inventory. This method is generally used when inventory items are perishable or subject to price fluctuations.

- LIFO (Last-In, First-Out): In contrast to FIFO, the LIFO method assumes that the most recently purchased or produced goods are sold first. The cost of the newest inventory is matched with the cost of goods sold, while the oldest inventory is valued in the ending inventory. LIFO is commonly used when prices are rising because it helps in reducing taxable income since the older inventory is valued at lower, outdated prices.

- Weighted Average Cost: This method calculates the average cost of each item in the inventory. The cost of goods sold and ending inventory are calculated based on this weighted average cost. This method is useful when the cost of inventory is subject to frequent changes.

Each valuation method has its advantages and disadvantages, and businesses must choose the method that best suits their industry, financial goals, and inventory characteristics.

In Conclusion

Ending inventory is a vital component of inventory management, financial reporting, and decision-making for businesses. By understanding the definition, calculation, and valuation methods associated with ending inventory, business owners and accounting professionals can make informed decisions and better manage their inventory.

Remember, accurate calculation and valuation of ending inventory are crucial for maintaining healthy financial statements and achieving long-term business success. So, make sure to assess your inventory regularly, choose the right valuation method, and keep a close eye on your bottom line!

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance