Finance

How Do Debt Consolidation Companies Make Money

Published: March 6, 2024

Learn how debt consolidation companies generate revenue and make money in the finance industry. Understand the financial mechanisms behind their profitability.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Debt consolidation is a financial strategy that has gained prominence as individuals seek to manage their debts more effectively. It involves combining multiple debts into a single, more manageable payment. This approach can provide relief from the burden of juggling various payments, interest rates, and due dates. Debt consolidation companies play a pivotal role in facilitating this process, offering services designed to simplify debt repayment for their clients.

In this article, we will delve into the world of debt consolidation and explore the mechanisms through which debt consolidation companies generate revenue. By understanding the financial dynamics at play, individuals can make informed decisions when considering debt consolidation as a potential solution for their financial challenges. Let's embark on a journey to unravel the intricacies of debt consolidation and the financial landscape within which these companies operate.

Debt consolidation is a multifaceted concept that encompasses various financial aspects, and a comprehensive understanding of its mechanisms is crucial for anyone navigating the realm of personal finance. Whether you are a consumer seeking to alleviate the burden of multiple debts or an individual interested in the inner workings of the financial industry, this exploration of debt consolidation and the revenue models of debt consolidation companies will provide valuable insights into this dynamic field.

Understanding Debt Consolidation

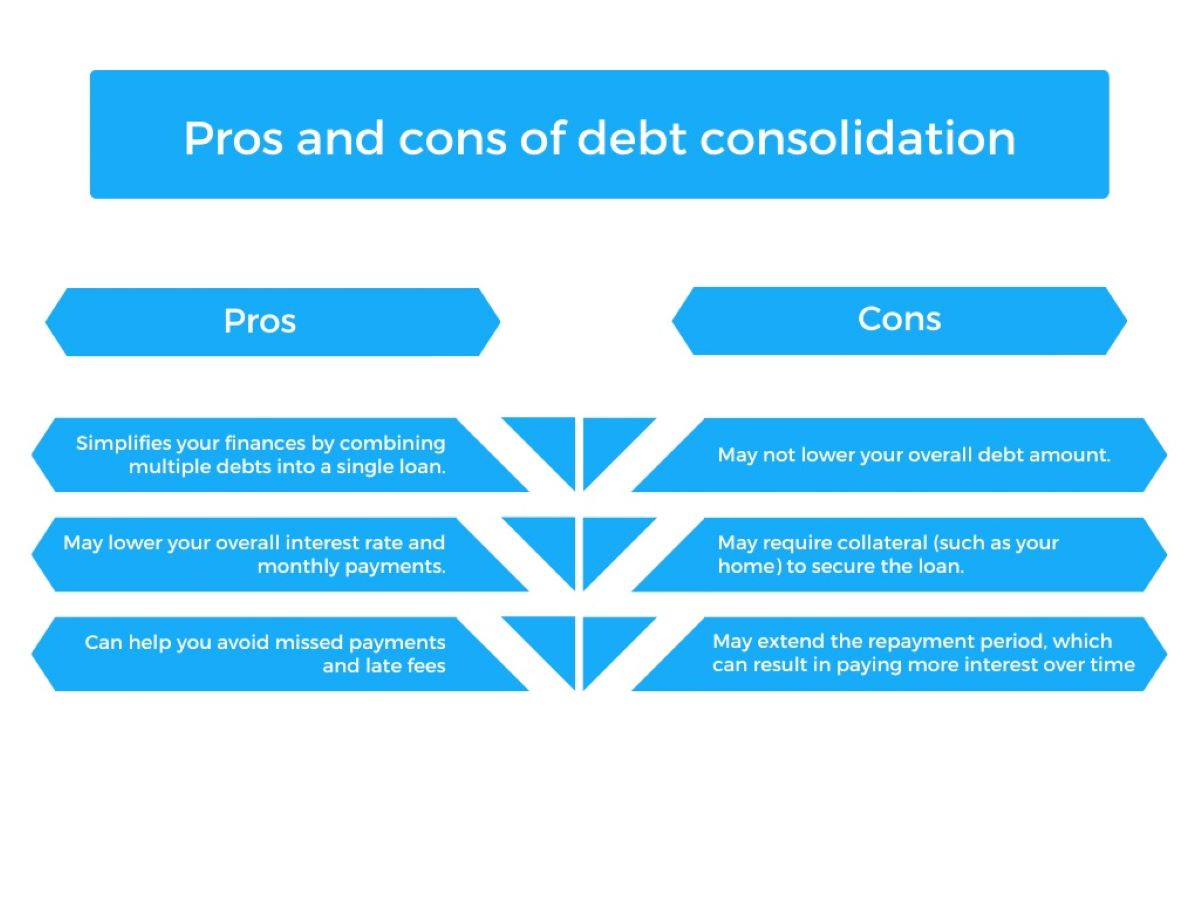

Debt consolidation involves merging multiple debts, such as credit card balances, personal loans, or medical bills, into a single, more manageable loan or payment plan. This approach aims to streamline the debt repayment process by combining various outstanding balances into a singular obligation. By doing so, individuals can potentially benefit from a lower interest rate, reduced monthly payments, and a structured timeline for debt clearance.

One common method of debt consolidation is obtaining a consolidation loan, which allows individuals to pay off their existing debts and focus on repaying a single loan. Another approach involves enlisting the services of a debt consolidation company, which negotiates with creditors on behalf of the debtor to secure more favorable terms, such as lower interest rates or reduced fees.

It is important to note that debt consolidation does not eliminate the total amount owed; rather, it restructures the existing debt, making it more manageable and potentially less costly to repay. By consolidating debts, individuals can simplify their financial obligations and gain a clearer perspective on their path to becoming debt-free.

Understanding the principles of debt consolidation empowers individuals to make informed decisions about their financial well-being. By recognizing the potential benefits and implications of debt consolidation, individuals can assess whether it aligns with their financial goals and explore the available options for achieving greater stability and control over their finances.

How Debt Consolidation Companies Make Money

Debt consolidation companies employ various strategies to generate revenue while assisting individuals in managing their debts. Understanding these mechanisms sheds light on the financial dynamics at play and the incentives that drive the operations of these companies.

One of the primary ways debt consolidation companies make money is through fees charged for their services. When individuals enroll in a debt consolidation program, they may incur upfront fees, monthly service charges, or a percentage of the total consolidated debt. These fees contribute to the company’s revenue stream and cover the costs associated with negotiating with creditors, managing the consolidation process, and providing ongoing support to clients.

Additionally, debt consolidation companies may earn commissions by partnering with financial institutions or lenders to provide consolidation loans or other financial products. By facilitating the arrangement of consolidation loans, the companies receive compensation from the lending entities, creating a supplementary source of income.

Furthermore, some debt consolidation companies may receive incentives based on the successful repayment of consolidated debts by their clients. In certain arrangements, these companies may negotiate with creditors to receive a percentage of the amount saved through reduced interest rates or waived fees. This incentivizes the companies to secure favorable terms for their clients, as it directly impacts their own earnings.

It is important for individuals considering debt consolidation to carefully review and understand the fee structures and potential costs associated with these services. By comprehending how debt consolidation companies generate revenue, consumers can make informed decisions and evaluate the overall value proposition offered by these companies.

By comprehending the financial mechanisms underpinning the operations of debt consolidation companies, individuals can navigate the landscape of debt management with a clearer understanding of the associated costs and benefits.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance