Finance

How Fintech Makes Money

Published: October 29, 2023

Discover how the finance industry leverages fintech to generate revenue and stay ahead in the market. Explore the intersection of finance and technology for profitable opportunities.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

In recent years, the financial technology (fintech) industry has revolutionized the way people manage and access their money. Fintech companies leverage technology to provide innovative financial services and solutions, disrupting traditional banking and financial institutions. With the rapid growth of this sector, it is fascinating to explore how fintech companies generate revenue and sustain their business models.

Fintech companies utilize various strategies and revenue streams to monetize their products and services. From payment and transaction fees to data monetization and subscription-based models, these innovative firms have found creative ways to generate income in the digital age. Additionally, partnerships and collaborations with traditional financial institutions, along with interest income from lending and the management of investments, contribute to their revenue pool.

However, while the fintech industry offers tremendous opportunities, it also faces unique challenges. Regulatory compliance, cybersecurity risks, and the need for constant innovation are just a few of the hurdles that fintech companies must navigate to maintain their revenue streams. This article will delve into the various methods through which fintech companies make money and identify some of the challenges they face in this rapidly evolving space.

Importance of Fintech

The rise of fintech has had a significant impact on the finance industry, transforming how individuals and businesses manage their finances. Fintech companies have introduced innovative solutions that enhance convenience, accessibility, and efficiency, ultimately empowering consumers with more control over their financial lives.

One of the key advantages of fintech is its ability to democratize financial services. Traditional banking systems often exclude individuals without access to brick-and-mortar branches or those who do not meet stringent eligibility criteria. Fintech has bridged this gap by offering digital banking services, mobile payment apps, and online investment platforms that are accessible to anyone with a smartphone and an internet connection. This inclusivity ensures that people from all walks of life can participate in the financial ecosystem and access much-needed financial products and services.

Fintech also addresses the issue of inefficiency within the traditional financial system. By leveraging advanced technologies such as artificial intelligence, blockchain, and data analytics, fintech companies streamline processes and eliminate middlemen, resulting in faster and more cost-effective services. For example, peer-to-peer lending platforms connect borrowers directly with lenders, cutting out the need for traditional banks and reducing the time and cost involved in obtaining a loan.

Furthermore, fintech enhances financial literacy and empowers individuals to make better financial decisions. Many fintech applications offer personalized financial planning tools, budgeting apps, and investment guidance, giving users more visibility and control over their money. Through these tools, individuals can track their expenses, set financial goals, and receive real-time insights into their financial health.

The importance of fintech extends beyond individual consumers; it has also fostered innovation within businesses and industries. Small businesses and startups, in particular, benefit from fintech solutions that provide affordable payment processing, accounting software, and online lending platforms. These tools enable businesses to operate more efficiently, access funding, and compete with larger companies on a level playing field. As a result, fintech has become a catalyst for economic growth and entrepreneurship.

In summary, fintech plays a crucial role in society by revolutionizing how people access financial services, improving efficiency, promoting financial inclusion, and fostering innovation. Its importance will continue to grow as technology advances and people increasingly rely on digital solutions to manage their finances in an ever-connected world.

Revenue Streams in Fintech

Fintech companies employ various revenue streams to generate income and sustain their operations. These revenue streams can be categorized into several key areas that are fundamental to their business models. Understanding these revenue streams is crucial for both investors and consumers to comprehend the underlying financial viability of fintech companies.

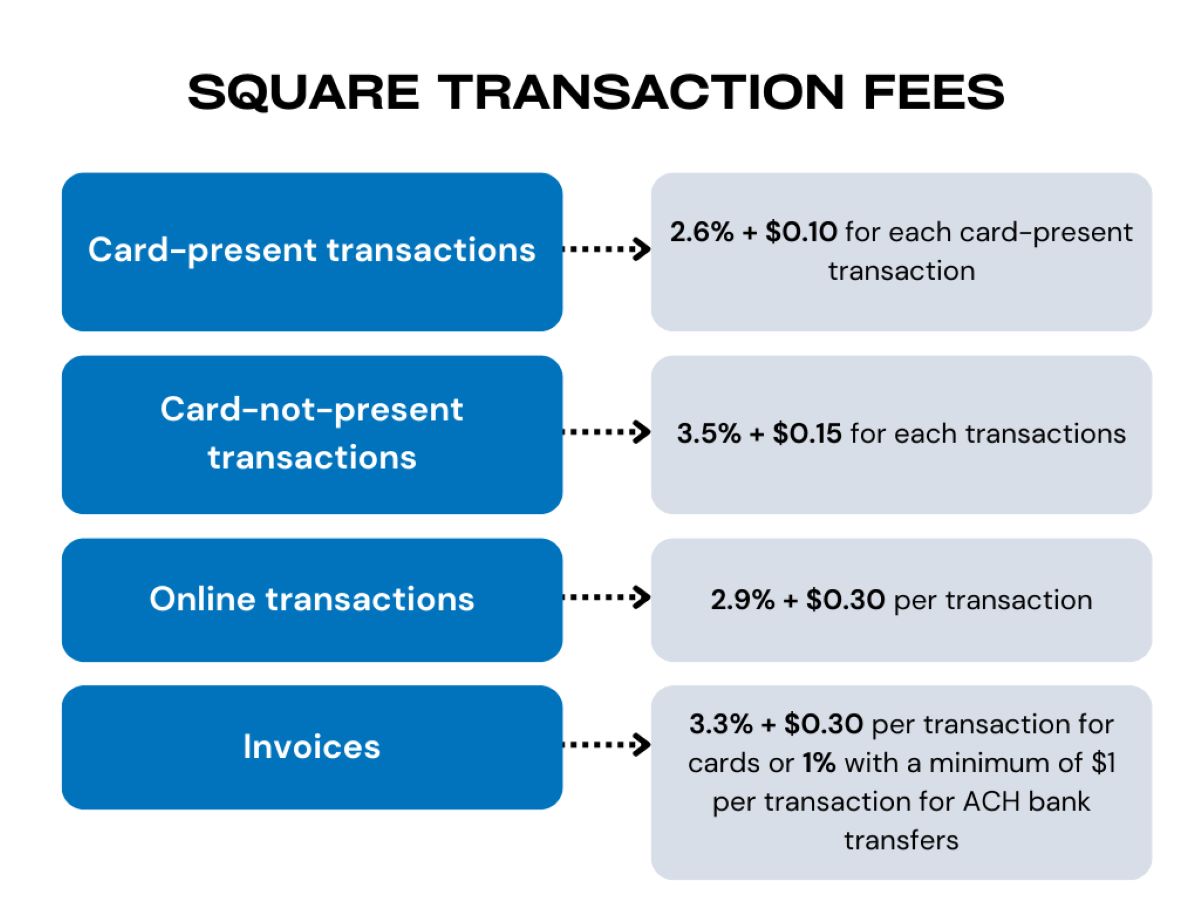

1. Payment and Transaction Fees: One of the primary sources of revenue for fintech companies is payment and transaction fees. Fintech platforms facilitate online payments, money transfers, and peer-to-peer transactions, for which they charge a small fee on each transaction. For example, payment processors like Stripe and Square charge a percentage of the transaction value as a fee. Additionally, mobile payment apps and digital wallets often monetize through transaction fees when users make purchases or transfer money using their platforms.

2. Data Monetization: With the exponential growth of digital transactions and online activities, valuable user data is generated. Fintech companies capitalize on this data by anonymizing and aggregating it to derive meaningful insights and trends. They can then monetize this data by selling it to financial institutions, market research firms, or advertisers, who use it for product development, risk assessment, and targeted marketing campaigns. Data monetization provides a substantial revenue stream for fintech companies, especially those with a large customer base and extensive data analysis capabilities.

3. Subscription-Based Models: Many fintech companies offer premium or subscription-based services to their customers. These services often come with additional features, higher transaction limits, or enhanced customer support, attracting customers willing to pay a recurring fee. For example, investment platforms may offer premium plans with personalized advice and access to exclusive investment options. These subscription-based models guarantee a regular revenue stream for fintech companies while providing customers with added value.

4. Partnership and Collaboration: Fintech companies often collaborate with traditional financial institutions to expand their offerings and reach a broader customer base. These partnerships may involve revenue-sharing agreements, where the fintech company earns a percentage of the revenue generated through the joint services. For instance, a fintech firm specializing in digital loan origination may partner with a bank to offer online loan applications, where the fintech company receives a share of the interest income generated from approved loans.

5. Lending and Interest Income: Some fintech companies engage in direct lending or peer-to-peer lending platforms, where they connect borrowers with lenders. In these cases, fintech companies earn interest income on the loans originated through their platforms. They may also leverage technology to underwrite loans more efficiently and assess credit risk, allowing them to offer competitive interest rates while generating profit from the interest earned on the loans.

Overall, these revenue streams collectively contribute to the financial viability of fintech companies. By diversifying their income sources and embracing innovative strategies, fintech companies can sustain their operations, fuel growth, and continue to provide innovative financial solutions to consumers and businesses alike.

Payment and Transaction Fees

One of the primary revenue streams for fintech companies is through payment and transaction fees. As these companies facilitate online transactions and digital payments, they charge a fee on each transaction, providing a consistent source of income. This revenue model is prevalent across various fintech sectors, including payment processors, mobile wallets, and peer-to-peer payment platforms.

Fintech payment processors act as intermediaries between buyers and sellers, facilitating secure and efficient transactions. They enable businesses of all sizes to accept payments through various channels, such as online platforms, mobile apps, or in-person card readers. These payment processors charge a percentage-based fee or a fixed fee per transaction processed. The fees collected help cover the costs of managing payment infrastructure, security measures, customer support, and platform maintenance.

Mobile payment apps and digital wallets also rely on payment and transaction fees. By enabling users to make purchases or send money seamlessly from their smartphones, these apps simplify the payment process. However, the convenience comes at a cost. Fintech companies typically charge a fee on transactions made through their apps. The fees may vary, depending on factors such as transaction size, transfer speed, or whether the transaction is cross-border. The revenue generated from these fees enables fintech companies to sustain their operations and further develop their payment solutions.

Peer-to-peer payment platforms, such as Venmo or PayPal, have gained popularity as individuals increasingly use them for splitting bills, repaying friends, or making small purchases. These platforms typically charge a fee when users transfer funds from their digital wallets to their bank accounts or vice versa. Additionally, certain transactions, such as instant transfers or international transfers, may incur higher fees. These fees contribute to the revenue stream of the fintech companies behind the peer-to-peer platforms.

Moreover, some fintech companies establish partnerships with merchants, offering them payment solutions that simplify the checkout process. In these cases, fintech companies charge a fee or a small percentage of the transaction amount for each payment processed on behalf of the merchant. This fee covers the cost of processing the transaction, ensuring encryption and security, and providing customer support to the merchant.

Payment and transaction fees facilitate the smooth operation of fintech companies by ensuring a steady stream of revenue. These fees help cover the costs associated with providing secure and efficient payment solutions, maintaining the necessary technological infrastructure, complying with regulatory requirements, and investing in ongoing innovation. Furthermore, as fintech companies continue to introduce new payment technologies and expand their market reach, payment and transaction fees remain a vital component of their sustainable business models.

Data Monetization

In the digital age, data has become a valuable asset, and fintech companies have recognized the potential to monetize the vast amounts of data they collect. Data monetization refers to the process of generating revenue by leveraging the insights derived from analyzing user data. By anonymizing and aggregating this data, fintech companies can offer valuable insights to financial institutions, market research firms, and advertisers, thereby creating a new revenue stream.

Fintech companies collect a wide range of data points as users interact with their platforms. This data includes transaction history, spending patterns, geographic location, and user demographics. By combining this information with advanced analytics and machine learning algorithms, fintech companies can derive valuable insights about consumer behavior, market trends, and financial preferences.

One way fintech companies monetize data is by selling anonymized and aggregated datasets to financial institutions. Banks and credit card companies, for instance, may be willing to purchase this data for market research, product development, and risk assessment purposes. By accessing this data, traditional financial institutions gain valuable insights into consumer preferences, spending habits, and creditworthiness, enabling them to make more informed business decisions.

Moreover, market research firms are interested in purchasing fintech data to understand consumer behavior and market trends. These insights help companies identify new market opportunities, tailor their marketing strategies, and develop innovative products and services that meet customer needs. By leveraging fintech data, market research firms can provide valuable insights to their clients and make data-driven recommendations.

Advertisers also recognize the value of fintech data for targeted marketing campaigns. Fintech companies possess a wealth of information about users’ financial habits, enabling advertisers to create highly personalized and relevant advertisements. For example, a fintech company may partner with an advertiser to deliver tailored credit card offers to users based on their spending patterns. This targeted advertising benefits both the advertiser, who can reach a specific audience, and the fintech company, who earns revenue from the partnership.

Data monetization presents an opportunity for fintech companies to diversify their revenue streams and enhance their profitability. However, it is crucial for these companies to prioritize user privacy and data security. Data must be anonymized and aggregated to protect user identities and comply with data protection regulations. Fintech companies must also be transparent with their users about how their data is used and provide clear opt-out options for those who do not wish to participate in data monetization initiatives.

In summary, data monetization is a significant revenue stream for fintech companies. By leveraging the valuable insights derived from user data, these companies can sell anonymized datasets to financial institutions, market research firms, and advertisers. However, it is essential for fintech companies to approach data monetization ethically and with user consent, ensuring that data privacy and security remain a top priority.

Subscription-Based Models

Subscription-based models have gained popularity in the fintech industry, offering users additional features, enhanced services, and exclusive benefits in exchange for a recurring fee. This revenue stream allows fintech companies to provide a high level of customization and personalized experiences to their customers while ensuring a steady, predictable income flow.

Fintech companies often offer tiered subscription plans, allowing users to choose the level of service that best suits their needs. Basic or free versions of the service may be available, but premium plans unlock additional features and benefits. These plans are designed to cater to different segments of the user base, providing options that align with individual preferences and financial capabilities.

Subscription-based models are prevalent in various fintech sectors, including personal finance management apps, investment platforms, and credit monitoring services. For instance, personal finance apps may offer premium plans that provide advanced budgeting tools, customized financial advice, and expense tracking features. These additional capabilities help users streamline their financial management and make better-informed decisions.

Investment platforms often offer subscription-based plans that provide exclusive investment opportunities, personalized portfolio management, and access to financial advisors. These premium plans ensure that investors receive tailored guidance and insights, helping them navigate the complexities of the financial markets more effectively.

Moreover, credit monitoring services charge a recurring fee to provide users with real-time credit score updates, identity theft protection, and credit report monitoring. These services not only give users peace of mind but also empower them to actively manage and improve their credit health.

The subscription-based model benefits both fintech companies and users. For fintech companies, it creates a stable and predictable revenue stream that helps cover operating costs, invest in technological advancements, and sustain business growth. Additionally, it fosters customer loyalty as users who subscribe to premium plans are more likely to remain engaged and satisfied with the service, reducing customer churn and supporting long-term relationships.

Users, on the other hand, benefit from the added value and convenience that premium subscription plans offer. They have access to advanced features, personalized insights, and dedicated customer support, which can improve their financial decision-making and overall experience using the fintech service.

However, it is crucial for fintech companies to carefully consider the pricing and value proposition of their subscription plans. The offerings should align with user expectations, delivering enough value to justify the recurring cost to users. Regular assessment and adjustment of subscription plans may be necessary to ensure that they remain competitive and compelling to users in a rapidly evolving fintech landscape.

In summary, subscription-based models provide a reliable revenue stream for fintech companies while offering users additional benefits and customized experiences. By successfully implementing and managing these models, fintech companies can build strong customer relationships, drive user engagement, and create sustainable business growth in an increasingly competitive market.

Partnership and Collaboration

Partnerships and collaborations are fundamental strategies employed by fintech companies to expand their reach, enhance their product offerings, and generate revenue. By joining forces with traditional financial institutions, technology companies, and other fintech firms, these collaborations create synergies that benefit all parties involved.

One common form of partnership in the fintech industry is between fintech companies and traditional financial institutions such as banks, insurance companies, or investment firms. These collaborations allow fintech companies to leverage the existing infrastructure, regulatory compliance, and customer base of traditional financial institutions. In return, traditional financial institutions can tap into the innovation and agility offered by fintech companies, offering enhanced digital services to their customers.

For example, a fintech company specializing in digital lending may partner with a bank to offer online loan origination and processing. The fintech company brings its expertise in streamlining the loan application process and leveraging data analytics for credit assessment, while the bank provides the necessary lending capital and the established customer base. In such partnerships, fintech companies often earn a share of the interest income generated from approved loans, creating a revenue stream while expanding their market reach.

Technology companies also frequently collaborate with fintech firms to provide seamless and integrated solutions. For instance, a fintech company may collaborate with a leading tech platform such as a popular e-commerce site or a ride-hailing app to offer payment processing services. By integrating their payment systems, fintech companies can reach a broader customer base and earn transaction fees or a percentage of the payment volume processed through their platforms.

Furthermore, collaborations between fintech companies themselves are becoming more common. Fintech firms may partner to combine their unique capabilities and develop new products or services. For example, a robo-advisory platform may partner with a data analytics firm to offer personalized investment recommendations based on advanced data insights. These partnerships allow fintech companies to leverage each other’s expertise, expand their service offerings, and drive mutual growth.

Partnerships and collaborations in the fintech industry also extend beyond financial institutions and technology companies. Fintech companies often collaborate with other industries, such as e-commerce, healthcare, or real estate, to provide specialized financial services. This integration allows users to access financial services seamlessly within their existing workflows, providing convenience and added value.

In addition to revenue-sharing models, collaborations can create revenue opportunities through referral fees, licensing agreements, or joint marketing efforts. These partnerships allow fintech companies to generate additional income while expanding their customer base and diversifying their product offerings.

However, successful partnerships and collaborations require careful planning, effective communication, and alignment of objectives. Fintech companies must ensure that there is a shared vision, a clear understanding of the roles and responsibilities, and adequate mechanisms for resolving potential issues. Moreover, staying abreast of evolving regulations and ensuring compliance is crucial for maintaining a strong partnership ecosystem.

In summary, partnerships and collaborations play a vital role in the growth and success of fintech companies. By leveraging the strengths of various stakeholders, fintech companies can expand their market reach, enhance their product offerings, and generate revenue through shared resources and expertise. This collaborative approach fosters innovation, drives customer satisfaction, and supports the continued development of the fintech industry.

Lending and Interest Income

Lending and interest income is a key revenue stream for many fintech companies operating in the lending space. By providing loans directly or facilitating peer-to-peer lending, fintech firms can earn interest income on the funds they lend out, contributing to their overall revenue generation.

Fintech companies have disrupted traditional lending models by leveraging technology to streamline loan origination, underwriting, and servicing processes. They have developed sophisticated algorithms and risk assessment models that use alternative data sources and advanced analytics to evaluate borrowers’ creditworthiness. This enables fintech companies to make faster lending decisions and offer loans to individuals and businesses that may have been overlooked or underserved by traditional lenders.

For fintech companies that directly provide loans, interest income is a significant revenue driver. Interest income is earned from the interest charged on the loans issued to borrowers. The interest rate is usually based on factors such as the borrower’s credit profile, loan term, and applicable regulations. Fintech platforms may offer competitive interest rates to attract borrowers while ensuring a profitable margin.

In addition to direct lending, fintech companies may also operate peer-to-peer lending platforms. These platforms connect individual lenders with borrowers, effectively cutting out the traditional financial institutions as intermediaries. Fintech companies earn interest income by charging fees, commonly known as loan origination fees or service fees, on each loan facilitated through their platforms. The fees may be a percentage of the loan amount or a flat fee per loan.

Fintech companies offering lending services are often able to provide better rates and faster loan disbursements due to their efficient processes and technology-driven approach. Moreover, by leveraging data analytics and machine learning, they can better assess credit risk, resulting in reduced default rates. This not only benefits borrowers by providing access to funds but also allows fintech companies to generate more reliable and profitable interest income.

Furthermore, fintech companies in the lending space may also offer additional financial products and services to borrowers. For example, they may provide borrowers with insurance packages, debt consolidation options, or personalized financial planning. These ancillary services contribute to the overall revenue of fintech companies, complementing the interest income earned from lending activities.

However, it is worth noting that lending is subject to various regulations and compliance requirements, varying from region to region. Fintech companies must navigate and ensure compliance with these regulations to mitigate risks and maintain a sustainable lending business.

In summary, lending and interest income is a significant revenue stream for fintech companies involved in lending activities. By leveraging technology and data-driven decision-making, these companies can offer loans to individuals and businesses, earning interest income on the funds they lend out. The efficiency and innovation brought by fintech to the lending space have created opportunities for both borrowers and lenders, fostering growth and financial inclusion in the digital age.

Investment and Assets Under Management (AUM)

Investment and assets under management (AUM) is a significant revenue stream for fintech companies operating in the investment and wealth management space. By offering digital investment platforms, robo-advisory services, or portfolio management solutions, fintech firms can earn fees based on the assets they manage, as well as generate income from investment-related products and services.

Fintech companies have transformed the investment landscape by leveraging technology to provide accessible and user-friendly investment platforms. These platforms often cater to both experienced investors and those who are new to investing, simplifying the investment process and offering a range of investment options.

Robo-advisory platforms, for instance, use algorithms and automated systems to provide investment recommendations and portfolio management. These platforms assess investors’ risk tolerance, financial goals, and other factors to create diversified portfolios that align with their objectives. Fintech companies charge a fee, typically a percentage of AUM, for managing client portfolios. The fee is usually lower than that of traditional human financial advisors, making it more affordable for a wider range of investors to access professional investment management.

In addition to robo-advisory services, fintech companies may offer digital brokerage services, allowing users to buy and sell securities directly through their platforms. These platforms often charge transaction fees or commissions for executing trades. Related services, such as research reports, market analysis, or educational resources, may also generate additional revenue for fintech firms.

Furthermore, some fintech companies offer investment-related products such as exchange-traded funds (ETFs), mutual funds, or alternative investment opportunities. By creating and managing these investment products, fintech firms earn management fees based on the AUM of these funds. Investors who choose to invest in these products pay a percentage-based fee, which contributes to the fintech company’s revenue.

Fintech companies operating in the investment space aim to provide transparent, affordable, and diversified investment options. The technology-driven approach streamlines processes, reduces costs, and enables real-time monitoring of portfolios, enhancing the overall investment experience for users.

It is worth noting that fintech companies need to comply with regulations governing investment advice, financial disclosures, and investor protection. They must provide accurate and comprehensive information to users, ensuring transparency in their operations and fee structures.

In summary, investment and assets under management (AUM) is a substantial revenue stream for fintech companies providing investment services. By offering digital investment platforms, robo-advisory solutions, and related investment products, these firms generate income from managing client portfolios, transaction fees, and management fees. The use of technology in the investment space has democratized access to professional investment management and provided investors with more choices and control over their investment decisions.

Challenges in Fintech Revenue Generation

While the fintech industry offers immense opportunities for revenue generation, it also presents unique challenges that fintech companies must navigate to sustain and grow their business. These challenges stem from various factors including regulatory compliance, cybersecurity risks, market competition, and the need for continuous innovation.

1. Regulatory Compliance: Fintech companies operate in a highly regulated environment, and compliance with financial regulations can be complex and time-consuming. Different jurisdictions have different rules and requirements, making it challenging for fintech firms to operate seamlessly across borders. The cost of regulatory compliance, including obtaining necessary licenses, adhering to customer identification and verification processes, and staying up to date with changing regulations, can significantly impact profitability.

2. Cybersecurity Risks: Fintech companies handle vast amounts of sensitive financial and personal data, making them prime targets for cyberattacks. Data breaches can result in financial loss, damage to reputation, and loss of consumer trust. Investing in robust cybersecurity measures, including encryption, firewalls, and regular security audits, is crucial for protecting customer data and maintaining the integrity of fintech platforms. However, the cost of implementing and maintaining these security measures can be significant.

3. Market Competition: The fintech industry is highly competitive, with numerous companies vying for market share and customer attention. Traditional financial institutions, as well as other fintech startups, pose significant competition in areas where regulatory barriers are relatively low. Differentiating from competitors and attracting and retaining customers can be challenging, requiring continuous innovation and providing unique value propositions.

4. Customer Acquisition and Retention: Acquiring new customers and retaining existing ones is a constant challenge for fintech companies. The digital landscape offers numerous choices, and customer loyalty can be fickle. Fintech companies need to invest in marketing and customer acquisition strategies while simultaneously providing excellent customer experiences, personalized services, and ongoing support to retain their customer base.

5. Technical Complexity and Scalability: Fintech companies rely heavily on technology infrastructure to deliver their services. Managing the technical complexity, ensuring scalability to handle increasing user demands, and maintaining system uptime are critical challenges. Investing in robust technology stacks, cloud computing resources, and technical expertise is essential. However, this requires significant upfront investment and ongoing operational costs.

6. Constant Innovation: In a rapidly evolving landscape, fintech companies must stay ahead of the curve by continuously innovating their products and services. Customer expectations change, new technologies emerge, and market demands evolve. Fintech firms need to allocate resources for research and development, experiment with new ideas, and adapt quickly to market dynamics to remain competitive and capture new revenue opportunities.

Addressing these challenges requires strategic planning, adaptability, and a deep understanding of the market and customer needs. Fintech companies need to foster a culture of innovation, invest in talent and technology, build strong partnerships, and prioritize customer trust and regulatory compliance to navigate these challenges successfully.

In summary, while the fintech industry offers significant revenue opportunities, challenges such as regulatory compliance, cybersecurity risks, market competition, customer acquisition, technical complexity, and the need for continuous innovation must be overcome. By embracing these challenges and implementing effective strategies, fintech companies can position themselves for long-term growth and success in the dynamic and evolving fintech landscape.

Conclusion

The fintech industry has transformed the finance landscape, providing innovative solutions that enhance convenience, accessibility, and efficiency. Fintech companies employ various revenue streams to sustain their operations and drive growth. Payment and transaction fees, data monetization, subscription-based models, partnerships and collaborations, lending and interest income, and investment and assets under management (AUM) all contribute to the financial viability of fintech firms.

However, navigating the fintech landscape comes with its own set of challenges. Fintech companies must comply with regulatory requirements, protect against cybersecurity risks, stay ahead in a highly competitive market, acquire and retain customers, manage technical complexities, and continually innovate to remain relevant and competitive.

Despite these challenges, the importance of fintech cannot be understated. Fintech has democratized financial services, making them accessible to a wider population and fostering financial inclusion. It has introduced efficiencies, improved financial literacy, and empowered individuals and businesses to take control of their finances. Fintech’s collaboration with traditional financial institutions and other industries has resulted in synergistic partnerships that benefit all parties involved.

As the fintech industry continues to evolve, there are boundless opportunities for revenue generation and sustainable business growth. By embracing innovation, leveraging technology, and prioritizing customer needs, fintech companies can create value, build trust, and capture new market opportunities.

In conclusion, fintech companies play a critical role in shaping the future of finance. Their ability to generate revenue through diverse streams positions them as key players in the financial landscape. By overcoming challenges, utilizing effective revenue strategies, and continuing to innovate, fintech companies have the potential to drive positive change, revolutionize financial services, and empower individuals and businesses worldwide.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance