Home>Finance>How Many Days Should A Credit Card Charge For A Late Fee

Finance

How Many Days Should A Credit Card Charge For A Late Fee

Published: February 22, 2024

Learn about late fees on credit cards and how many days it takes for a credit card to charge a late fee. Get expert advice on managing your finances.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to the world of credit cards, where the convenience of making purchases often comes with the responsibility of timely payments. Late fees are one of the aspects that credit card users need to be aware of, as they can have a significant impact on their financial well-being. In this article, we will delve into the factors that affect late fees, industry standards, legal regulations, and best practices for managing late payments on credit cards.

Understanding the dynamics of late fees is crucial for anyone who holds a credit card or is considering obtaining one. By gaining insights into the various elements that influence late fees, individuals can make informed decisions and take proactive steps to avoid unnecessary financial penalties.

Whether you are a seasoned credit card user or someone who is new to the world of personal finance, this article will provide valuable information to help you navigate the complexities of credit card late fees. Let’s explore the nuances of late fees and empower ourselves with the knowledge needed to make sound financial choices.

Factors Affecting Late Fees

Several factors come into play when determining the late fees associated with credit card payments. Understanding these factors can shed light on the reasons behind the imposition of late fees and how individuals can mitigate their impact. Here are the key factors that influence late fees on credit cards:

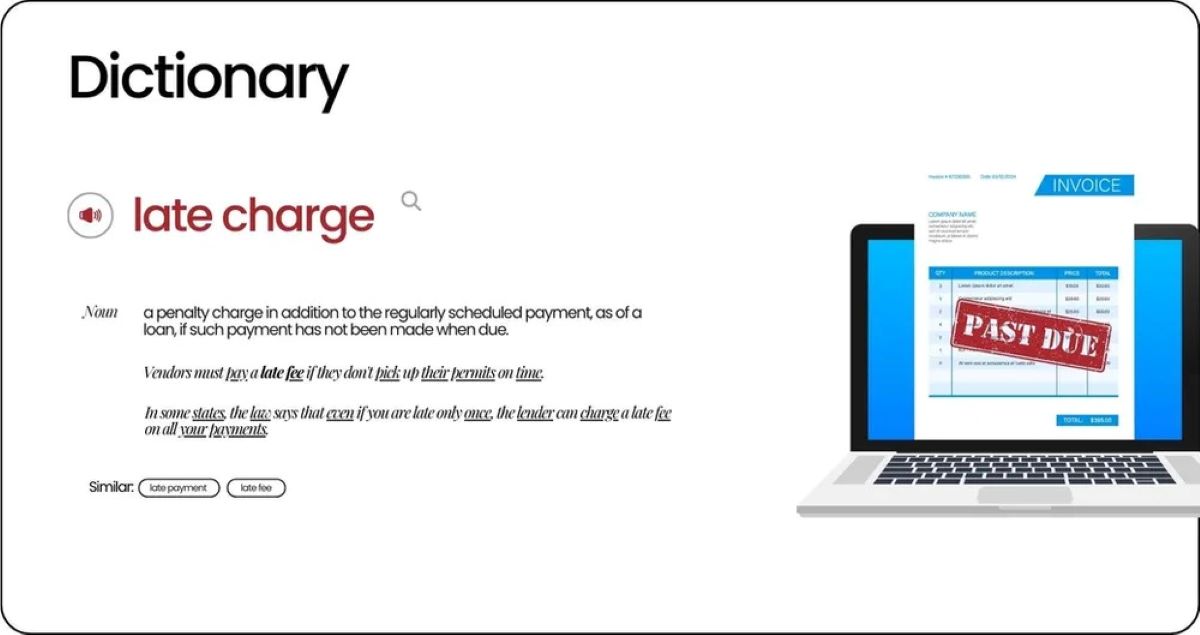

- Payment History: Your payment history plays a crucial role in determining late fees. Consistently missing payments or making late payments can result in higher late fees and may also lead to an increase in the annual percentage rate (APR) on your credit card.

- Outstanding Balance: The outstanding balance on your credit card can impact the late fees. Higher balances may lead to higher late fees, as the potential risk to the credit card issuer increases with a larger outstanding amount.

- Credit Card Terms and Conditions: Each credit card comes with its own set of terms and conditions, including specific provisions related to late fees. It is essential to review these terms and conditions to understand the late fee structure associated with your credit card.

- Minimum Payment Requirements: Failing to meet the minimum payment requirements can trigger late fees. It is important to be aware of the minimum amount due and ensure timely payments to avoid incurring late fees.

- Grace Period: The presence or absence of a grace period can impact late fees. A grace period allows cardholders to make payments without incurring interest or late fees. Understanding the terms of the grace period is crucial for managing credit card payments effectively.

By considering these factors, credit card users can gain a comprehensive understanding of the elements that contribute to the calculation of late fees. Being mindful of these factors empowers individuals to take proactive measures to avoid late fees and maintain a healthy financial standing.

Industry Standards

Within the credit card industry, late fees are subject to certain standards and practices that are upheld by credit card issuers. These standards encompass the maximum late fees that can be charged, as well as the disclosure of late fee policies to cardholders. Understanding industry standards can provide insight into the framework within which late fees are administered. Here are key aspects of industry standards related to late fees:

- Maximum Late Fees: Credit card issuers are typically bound by industry regulations that set a cap on the maximum late fees that can be imposed. These limits are in place to protect consumers from exorbitant late fees and ensure fair practices within the industry.

- Disclosure Requirements: Credit card issuers are required to clearly disclose their late fee policies to cardholders. This includes providing information about the amount of the late fee, the circumstances under which it is charged, and any potential impacts on the cardholder’s account, such as increased interest rates.

- Consistency in Application: Industry standards emphasize the consistent application of late fees across cardholders. This means that late fees should be administered in a uniform manner, without discrimination or preferential treatment based on factors unrelated to the cardholder’s payment behavior.

- Regulatory Compliance: Credit card issuers must adhere to regulatory guidelines set forth by governing bodies to ensure that their late fee practices align with consumer protection laws and industry regulations. Compliance with these regulations is essential for maintaining ethical and transparent late fee policies.

By adhering to industry standards, credit card issuers aim to promote fairness, transparency, and consumer protection in the administration of late fees. Cardholders can benefit from these standards by having clear expectations regarding late fees and knowing their rights in relation to late fee practices within the credit card industry.

Legal Regulations

Legal regulations play a pivotal role in shaping the landscape of late fees within the credit card industry. These regulations are designed to safeguard consumers from unfair practices and ensure that credit card issuers adhere to established guidelines when imposing late fees. Understanding the legal framework surrounding late fees is essential for both credit card users and issuers. Here are key aspects of legal regulations pertaining to late fees:

- Consumer Financial Protection Bureau (CFPB): The CFPB oversees and enforces regulations related to consumer financial products, including credit cards. It sets guidelines for the fair and transparent treatment of consumers in matters such as late fees and billing practices.

- Truth in Lending Act (TILA): Enacted to protect consumers in credit transactions, TILA requires credit card issuers to disclose key terms and costs associated with credit, including late fees. This transparency enables cardholders to make informed decisions and understand the implications of late payments.

- Fair Credit Billing Act (FCBA): The FCBA provides protections to consumers in cases of billing errors, unauthorized charges, and disputes, which can impact late fees. It outlines the procedures for addressing billing disputes and ensures that cardholders are not unfairly penalized for errors beyond their control.

- State-Specific Regulations: In addition to federal regulations, individual states may have specific laws governing late fees and consumer protections. These state-level regulations can further enhance the safeguards for credit card users and impose additional requirements on credit card issuers.

By abiding by legal regulations, credit card issuers are held accountable for their late fee practices, and consumers are provided with essential protections and avenues for recourse in the event of disputes or unfair treatment. Familiarizing oneself with these regulations can empower individuals to assert their rights and advocate for fair treatment in their credit card transactions.

Best Practices

When it comes to managing credit card payments and avoiding late fees, adopting best practices can significantly contribute to financial stability and responsible credit card usage. By implementing these practices, individuals can minimize the risk of incurring late fees and maintain a positive payment history. Here are some best practices for effectively managing credit card payments:

- Set Up Payment Reminders: Utilize payment reminders through mobile apps, email alerts, or calendar notifications to ensure that payment due dates are not overlooked. Setting up automatic payments can also provide a convenient way to stay on top of credit card obligations.

- Monitor Spending and Budget Wisely: Keeping track of expenses and adhering to a well-defined budget can help prevent overspending and ensure that funds are allocated for timely credit card payments. Responsible budgeting is integral to maintaining a consistent payment schedule.

- Understand Grace Periods: Familiarize yourself with the grace period offered by your credit card issuer. Knowing the duration of the grace period and the conditions for interest-free and fee-free payments can aid in strategic payment planning.

- Communicate with the Issuer: In the event of unforeseen circumstances that may affect your ability to make timely payments, proactively communicate with the credit card issuer. Exploring options for temporary hardship programs or alternative payment arrangements can help mitigate the impact of late fees.

- Regularly Review Terms and Conditions: Stay informed about changes to the terms and conditions of your credit card, especially those related to late fees and payment policies. Being aware of any updates enables you to adjust your payment strategy accordingly.

By incorporating these best practices into their financial routines, individuals can cultivate responsible credit card management habits and minimize the likelihood of incurring late fees. These proactive measures contribute to a positive credit card experience and support overall financial well-being.

Conclusion

Navigating the realm of credit card late fees involves a nuanced understanding of the factors, standards, regulations, and best practices that shape this aspect of personal finance. By recognizing the influence of payment history, outstanding balances, credit card terms, and grace periods, individuals can make informed decisions to avoid late fees and maintain a healthy financial standing. Industry standards and legal regulations serve as crucial frameworks that promote fairness, transparency, and consumer protection within the credit card industry.

Embracing best practices such as setting up payment reminders, monitoring spending, understanding grace periods, and proactive communication with credit card issuers empowers individuals to manage credit card payments effectively and mitigate the risk of incurring late fees. By adhering to these best practices, individuals can cultivate responsible credit card management habits and foster a positive financial outlook.

Ultimately, staying informed about late fee dynamics and integrating prudent financial practices into daily routines not only minimizes the impact of late fees but also contributes to overall financial wellness. By proactively engaging with the intricacies of credit card late fees and leveraging industry standards and legal protections, individuals can navigate the credit card landscape with confidence and ensure a positive and sustainable financial journey.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance