Finance

How Many Days Until A Late Fee Charged

Published: February 22, 2024

Find out how many days you have until a late fee is charged, and manage your finances effectively. Don't miss any payment deadlines.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Late fees are a common aspect of financial transactions, impacting various sectors such as credit cards, loans, rent payments, and utility bills. Understanding the implications of late fees is crucial for maintaining financial stability and avoiding unnecessary expenses. This article aims to delve into the intricacies of late fees, shedding light on the factors influencing their imposition and providing insights into how individuals can navigate this aspect of financial management.

Late fees can often catch individuals off guard, resulting in unexpected financial burdens. By gaining a comprehensive understanding of the dynamics surrounding late fees, individuals can proactively manage their finances, ensuring timely payments to avoid incurring such penalties.

In the subsequent sections, we will explore the nuances of late fees, including the factors that influence their imposition, the specific timelines within which late fees are typically charged, and practical tips to sidestep these penalties. By the end of this article, readers will be equipped with the knowledge needed to navigate the realm of late fees with confidence, thereby safeguarding their financial well-being.

Understanding Late Fees

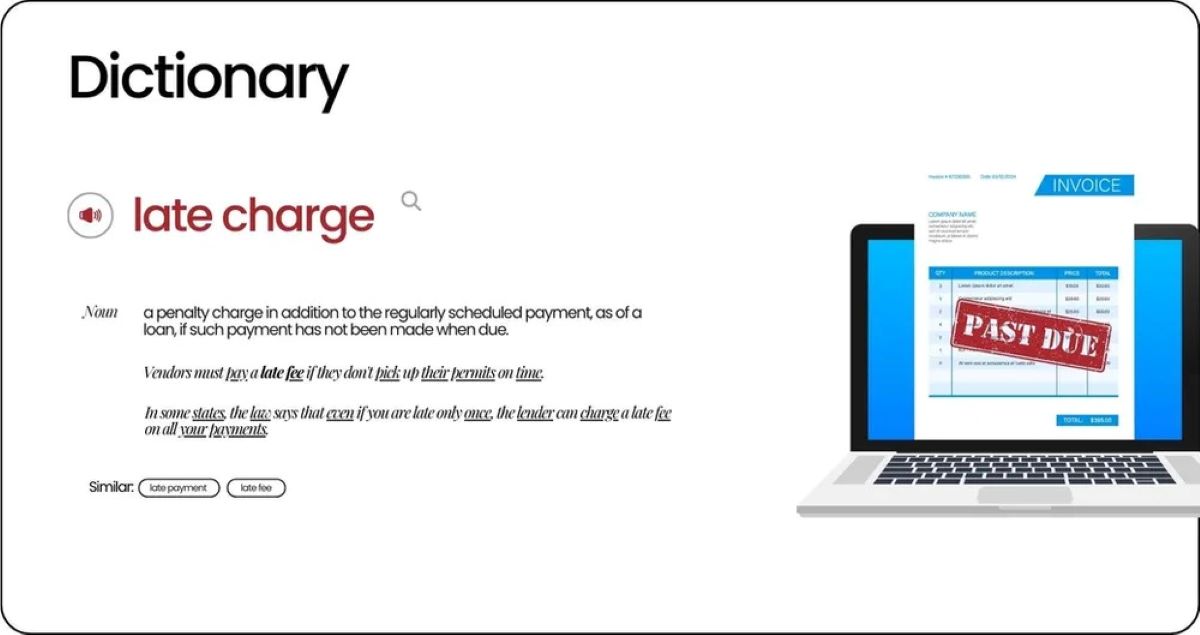

Late fees represent the financial penalties imposed for failing to make payments within the stipulated timeframe. These charges are prevalent across various financial obligations, such as credit card bills, loan repayments, rent, and utility payments. Typically, late fees are expressed as a fixed amount or a percentage of the overdue payment, and they serve as a deterrent against delayed payments.

From a financial institution’s perspective, late fees act as a form of compensation for the additional administrative costs and the increased risk associated with delayed payments. Moreover, these penalties serve to encourage responsible financial behavior, incentivizing individuals to prioritize timely payments.

It is important to note that the specifics of late fees, including the amount charged and the grace period provided, vary across different financial products and service providers. Understanding the terms and conditions outlined in the respective agreements or contracts is essential for individuals to grasp the implications of late fees in their specific financial engagements.

Furthermore, late fees can have broader ramifications beyond the immediate financial impact. For instance, consistently incurring late fees may result in a negative impact on an individual’s credit score, potentially hindering their ability to secure favorable terms for future credit or loan applications.

By comprehending the underlying rationale behind late fees and their potential repercussions, individuals can make informed decisions regarding their financial commitments. The subsequent sections will delve into the specific factors that influence the imposition of late fees, shedding light on the timelines within which these penalties are typically applied.

Factors Affecting Late Fee Charges

The imposition of late fee charges is influenced by a multitude of factors, each contributing to the overall dynamics of financial penalties. Understanding these factors is crucial for individuals seeking to navigate their financial obligations effectively and minimize the risk of incurring late fees.

One of the primary determinants of late fee charges is the specific terms outlined in the contractual agreements or terms of service. Different financial products and service providers have varying policies regarding late fees, encompassing aspects such as the grace period for payments, the calculation method for late fees, and the maximum penalty amount. It is imperative for individuals to familiarize themselves with these terms to anticipate and mitigate the risk of late fee charges.

Additionally, the type of financial obligation also plays a pivotal role in determining late fee charges. For instance, credit card companies may have distinct late fee structures compared to landlords or utility providers. Loan agreements, whether for mortgages, personal loans, or auto loans, often delineate specific provisions related to late payments and associated penalties.

The individual’s payment history and creditworthiness can also impact the application of late fees. For instance, individuals with a history of timely payments and a favorable credit score may be afforded certain leniencies or opportunities to negotiate late fee waivers in certain scenarios.

Furthermore, the regulatory environment and legal frameworks governing financial transactions can influence the imposition of late fees. Consumer protection laws and financial regulations may impose restrictions on the magnitude of late fees or mandate specific disclosures regarding late fee policies, thereby shaping the landscape within which late fee charges are administered.

By comprehending these factors, individuals can proactively manage their financial commitments, mitigate the risk of late fees, and engage with financial service providers from an informed standpoint. The subsequent section will delve into the specific timeline within which late fees are typically charged, providing actionable insights for individuals to navigate this aspect of financial management effectively.

How Many Days Until A Late Fee Is Charged

The timeline within which a late fee is charged varies depending on the specific financial obligation and the terms outlined by the service provider or financial institution. Typically, there is a grace period provided after the due date, during which the payment can be made without incurring a late fee. This grace period is often expressed in terms of days past the due date.

For credit card payments, the grace period commonly ranges from 21 to 25 days after the billing cycle ends. If the payment is not received within this period, a late fee is typically charged. However, it is essential for credit cardholders to refer to the terms and conditions provided by their card issuer to ascertain the exact grace period and late fee structure applicable to their account.

In the case of rent payments, landlords may stipulate a specific number of days past the due date before a late fee is imposed. This duration can vary, with some landlords allowing a grace period of five to seven days, while others may have a more stringent policy with a grace period of only two to three days.

Similarly, loan agreements, such as those for mortgages or personal loans, specify the grace period and the subsequent imposition of late fees. This grace period can range from 10 to 15 days past the due date, after which late fees may be applied. It is imperative for borrowers to familiarize themselves with the terms of their loan agreements to understand the specific timeline governing late fee charges.

Utility bill payments, including electricity, water, and gas bills, also adhere to distinct timelines for late fee imposition. The grace period for these payments may vary, with some utility providers allowing up to 20 days past the due date before late fees are applied.

Understanding the specific timelines for late fee charges is paramount for individuals to proactively manage their financial obligations. By being cognizant of these timelines, individuals can ensure timely payments, thereby avoiding the unnecessary burden of late fees and potential repercussions on their credit standing.

Tips to Avoid Late Fees

Effectively managing financial commitments and avoiding late fees necessitates a proactive approach and diligent financial stewardship. Here are several actionable tips to help individuals sidestep late fees and maintain financial stability:

- Set Up Automated Payments: Leveraging automated payment systems offered by banks or service providers can streamline the payment process, ensuring that payments are made on time without the need for manual intervention.

- Calendar Reminders: Utilize digital calendars or scheduling applications to set reminders for bill due dates, empowering individuals to stay abreast of their financial obligations and submit payments punctually.

- Establish Emergency Funds: Building an emergency fund can serve as a safety net, providing individuals with the financial buffer needed to address unexpected expenses or cash flow disruptions that may otherwise lead to late payments.

- Negotiate Waivers: In instances where a late payment is an anomaly, reaching out to the service provider or financial institution to request a one-time waiver of the late fee can yield positive outcomes, particularly for individuals with a strong payment history.

- Monitor Credit Card Balances: Keeping track of credit card balances and ensuring that the available credit aligns with upcoming payments can prevent inadvertent delays in payments and the subsequent imposition of late fees.

- Communicate Proactively: In situations where meeting payment deadlines becomes challenging, communicating proactively with the relevant parties can facilitate the exploration of alternative payment arrangements or the provision of extensions, mitigating the risk of late fees.

- Review Terms and Conditions: Regularly reviewing the terms and conditions associated with financial products and services can provide individuals with insights into late fee structures, grace periods, and potential avenues for mitigating late fee charges.

- Utilize Mobile Banking Apps: Mobile banking applications offer convenient access to account information and payment functionalities, empowering individuals to manage their finances on-the-go and submit timely payments.

By integrating these tips into their financial management practices, individuals can fortify their ability to navigate financial commitments effectively, mitigate the risk of late fees, and uphold a sound financial standing.

Conclusion

Managing financial obligations and navigating the realm of late fees necessitates a blend of vigilance, strategic planning, and proactive engagement. By comprehending the underlying mechanisms of late fees and the factors influencing their imposition, individuals can empower themselves to make informed decisions and mitigate the risk of incurring these penalties.

Understanding the specific timelines within which late fees are charged for various financial obligations, such as credit card payments, rent, loans, and utility bills, is pivotal for ensuring timely payments and averting unnecessary financial burdens. Moreover, leveraging practical tips, such as setting up automated payments, establishing calendar reminders, and proactively communicating with service providers, can fortify individuals’ ability to sidestep late fees and uphold financial stability.

Ultimately, the proactive management of financial commitments, coupled with a nuanced understanding of late fee structures and grace periods, can empower individuals to navigate their financial landscape with confidence. By integrating these insights into their financial management practices, individuals can safeguard their financial well-being, maintain a favorable credit standing, and cultivate a proactive approach to financial stewardship.

Embracing these principles and strategies can equip individuals with the resilience and foresight needed to steer clear of late fees, thereby fostering a robust financial foundation and promoting sustainable financial health.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance