Home>Finance>How Many Points Does Your Credit Drop When Applying For A Car

Finance

How Many Points Does Your Credit Drop When Applying For A Car

Published: January 13, 2024

Find out how applying for a car loan affects your credit score. Understand the point drop and ensure your finances are in order before taking this step.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When it comes to financing a car, one of the important factors that lenders consider is your credit score. Your credit score provides lenders with an indication of your creditworthiness and the likelihood of you repaying your debts. Applying for a car loan can impact your credit score, but exactly how many points will it drop?

In this article, we will explore the relationship between applying for a car loan and the subsequent drop in your credit score. We will delve into the factors that affect credit score reduction, typical credit score decreases for car loan applications, and steps you can take to recover from a credit score drop. Understanding these nuances can help you make informed decisions when it comes to financing a car and safeguarding your creditworthiness.

It is important to acknowledge that every individual’s credit situation is unique, and credit score changes may vary depending on the specific circumstances. However, by gaining a general understanding of the impact of car loan applications on credit scores, you can navigate the process more confidently.

So, let’s dive into the world of credit scores and explore the impact of applying for a car loan!

Understanding Credit Scores

Before we delve into the impact of car loan applications on credit scores, it’s crucial to understand what credit scores are and how they are calculated. A credit score is a numerical representation of an individual’s creditworthiness and is determined based on various factors.

One of the commonly used credit scoring models is the FICO score, which ranges from 300 to 850. The higher the score, the better your creditworthiness. The FICO score is calculated based on several factors, including:

- Payment history: This factor considers whether you have made your payments on time, any missed or late payments, and the severity of any defaults or bankruptcies.

- Amounts owed: This factor takes into account the total amount of debt you have, your credit utilization ratio (the percentage of available credit being utilized), and the number of revolving accounts with balances.

- Length of credit history: This factor considers the age of your accounts, the average age of all your accounts, and the time since your most recent account activity.

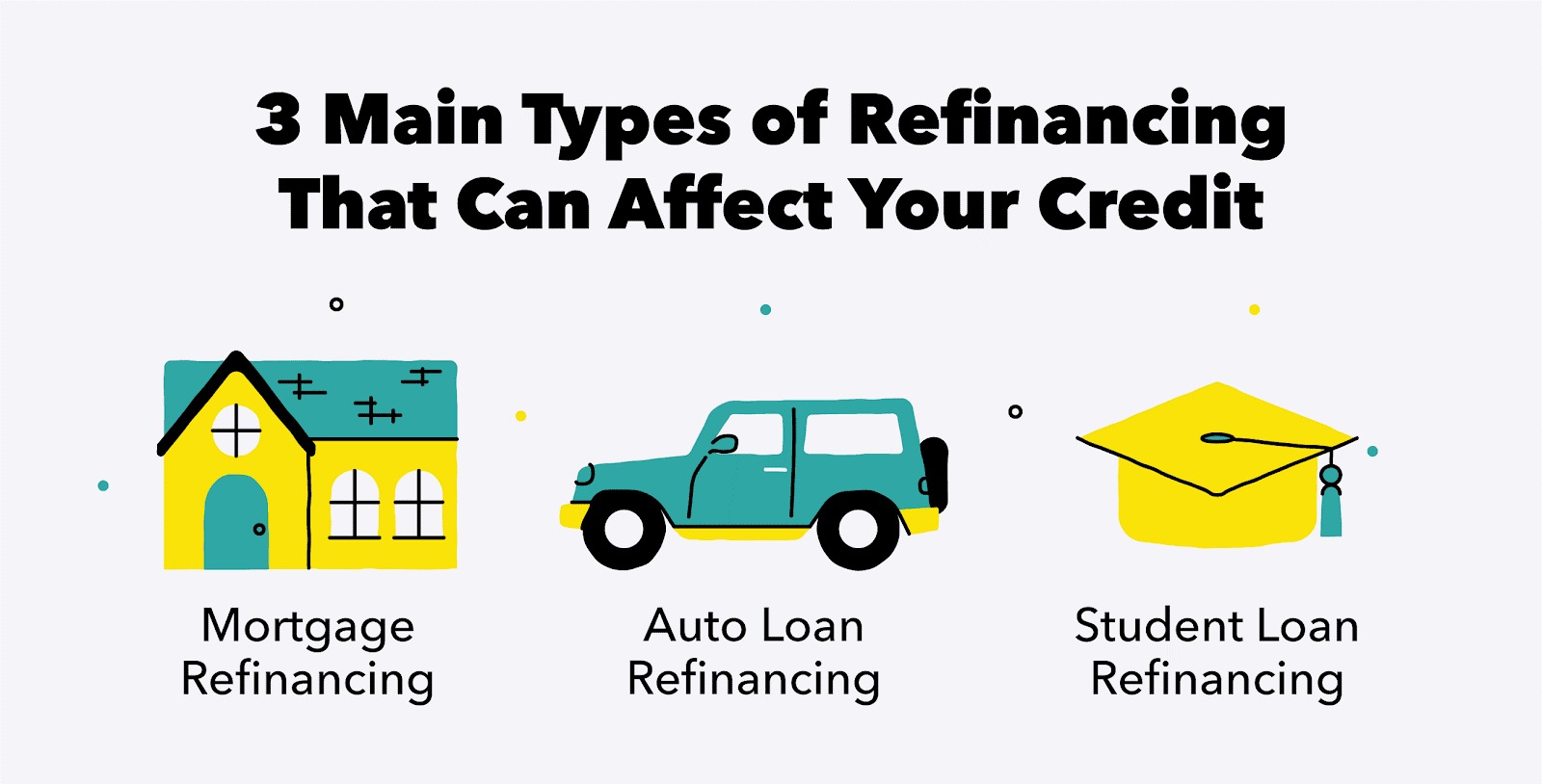

- Credit mix: This factor evaluates the types of credit accounts you have, including credit cards, mortgages, car loans, and student loans.

- New credit: This factor analyzes your recent credit inquiries, new accounts opened, and the proportion of new accounts to total accounts.

These factors, along with their respective weights, are used to calculate your credit score. It is important to note that credit scoring models may differ slightly between different credit bureaus or lenders.

Now that we have a basic understanding of credit scores, let’s explore how applying for a car loan can impact your credit score and what factors contribute to the credit score drop.

The Impact of Credit Inquiries

When you apply for a car loan, the lender will typically pull your credit report to assess your creditworthiness. This is known as a “hard inquiry” or a “hard pull.” Hard inquiries can have an impact on your credit score.

Each hard inquiry can generally cause a small decrease in your credit score, typically around 5-10 points. However, the impact of a single hard inquiry is usually minimal and temporary. The credit bureaus understand that consumers may need to shop around for the best loan terms, so multiple inquiries for the same type of loan made within a certain time frame (usually 14-45 days) are often treated as a single inquiry.

It’s important to note that not all credit inquiries affect your credit score. “Soft inquiries” or “soft pulls” are inquiries that occur when a person or entity checks your credit report for non-lending purposes, such as when you check your own credit or when a potential employer conducts a background check. Soft inquiries do not impact your credit score.

While the impact of hard inquiries on your credit score is generally small, it’s essential to be mindful of the number of inquiries you accumulate over a short period. A large number of inquiries can signal to lenders that you may be taking on too much debt or that you are financially unstable, which could negatively impact your creditworthiness.

Now that we understand the impact of credit inquiries on your credit score, let’s explore the factors that can further affect the drop in your credit score when applying for a car loan.

Factors Affecting Credit Score Drop

When applying for a car loan, several factors can contribute to the drop in your credit score. By understanding these factors, you can be better prepared and make informed decisions about your credit.

- Number of inquiries: The number of inquiries made within a short period can impact your credit score. Multiple inquiries can indicate a higher risk for lenders, potentially resulting in a more significant drop in your credit score.

- Credit utilization: Your credit utilization ratio, which is the amount of credit you are using compared to your total credit limit, plays a role in determining your credit score. Applying for a car loan and acquiring additional debt can increase your credit utilization and potentially lower your credit score.

- Length of credit history: The length of your credit history is an important factor in credit scoring. When you apply for a car loan, you may be opening a new account, which can decrease the average age of your credit history and potentially lower your credit score.

- Types of credit: Having a diverse mix of credit types, such as credit cards, mortgages, and car loans, can positively impact your credit score. However, applying for a car loan may not have a significant impact on this factor unless there is limited credit diversity in your current credit profile.

- Past credit behavior: If you have a history of late payments, defaults, or other negative credit events, your credit score may be more affected when applying for a car loan compared to someone with a clean credit history.

It’s important to keep in mind that the impact of these factors on your credit score can vary depending on your unique credit profile. For instance, someone with a well-established credit history and low credit utilization may experience a smaller credit score drop compared to an individual with limited credit history and high credit utilization.

Now that we have explored the factors that can affect the drop in your credit score when applying for a car loan, let’s take a look at the typical credit score reduction you can expect.

Typical Credit Score Reduction for Car Loan Applications

The exact credit score reduction you may experience when applying for a car loan can vary based on individual circumstances. However, there are some general guidelines to consider when it comes to the typical credit score reduction.

On average, a single hard inquiry from a car loan application can result in a credit score drop of around 5-10 points. As mentioned before, multiple inquiries for the same type of loan within a specific time frame are often treated as a single inquiry and have a lesser impact on your credit score.

The impact of a car loan application on your credit score may not only come from the hard inquiry but also from factors such as increased credit utilization, opening a new credit account, or a change in the average age of your credit history.

It’s important to note that the credit score reduction from a car loan application is temporary and often recovers within a few months, assuming you manage your credit responsibly going forward. This means making timely payments on all your obligations, minimizing new credit applications, and keeping your credit utilization ratio low.

Additionally, it’s important to remember that lenders consider various factors when evaluating your creditworthiness, not just your credit score. Your income, debt-to-income ratio, employment history, and other factors may also influence loan approval and terms.

Understanding the typical credit score reduction for car loan applications is beneficial for managing your expectations. However, it’s important to focus on maintaining a healthy overall credit profile rather than obsessing over a temporary drop in your credit score.

Now that we have explored the typical credit score reduction for car loan applications, let’s discuss the steps you can take to recover from a credit score drop.

Recovering from a Credit Score Drop

If you experience a credit score drop due to a car loan application or other factors, there are steps you can take to recover and improve your creditworthiness over time.

1. Pay your bills on time: Consistently making timely payments on all your credit obligations, including your car loan, can positively impact your credit score over time. Late payments can have a detrimental effect on your credit, so make it a priority to pay your bills by their due dates.

2. Reduce your credit utilization: Lowering your credit utilization ratio by paying down your debts can help improve your credit score. Aim to keep your credit card balances below 30% of your credit limit, if possible.

3. Limit new credit applications: Continuously applying for new credit can be seen as a sign of financial instability, and multiple hard inquiries can lower your credit score. Be selective and only apply for credit when necessary.

4. Review your credit report: Regularly checking your credit report allows you to identify any errors or discrepancies that could be negatively impacting your credit score. If you find any inaccuracies, report them to the credit bureaus immediately to have them corrected.

5. Build a positive credit history: If your credit history is limited, consider establishing a positive credit history by responsibly managing a credit card or a small installment loan. By making timely payments and demonstrating responsible credit management, you can gradually improve your credit score.

6. Be patient: It’s important to remember that credit score improvements take time. As you practice good credit habits and maintain a positive credit profile, your score will recover gradually over time.

Recovering from a credit score drop requires discipline and consistency in managing your credit. Remember, building a good credit score is a long-term process that involves responsible credit usage and maintaining a healthy financial lifestyle.

Now that you have learned about recovering from a credit score drop, let’s summarize what we have covered.

Conclusion

Applying for a car loan can have an impact on your credit score, but the exact number of points it will drop varies based on individual factors. Understanding the relationship between car loan applications and credit score decreases is essential for making informed financial decisions and safeguarding your creditworthiness.

We have learned that hard inquiries from car loan applications can result in a temporary drop in your credit score. However, the impact is typically minimal and recovers within a few months, assuming responsible credit behavior. Factors such as increased credit utilization, opening new credit accounts, and changes in the length or diversity of your credit history can also contribute to the credit score reduction.

To recover from a credit score drop, it is crucial to maintain good credit practices. This includes making timely payments, reducing credit utilization, limiting new credit applications, regularly reviewing your credit report for errors, and building a positive credit history.

Remember that your credit score is just one aspect lenders consider when evaluating your creditworthiness. Other factors like income, employment history, and debt-to-income ratio also play a crucial role.

By understanding the impact of car loan applications on credit scores and taking appropriate steps to manage your credit responsibly, you can navigate the car financing process with confidence and work towards improving your creditworthiness in the long run.

So, the next time you consider applying for a car loan, keep in mind the potential impact on your credit score and take proactive measures to maintain a healthy credit profile.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance