Finance

How Much Is Auto Insurance In Texas

Published: October 6, 2023

Find out the cost of auto insurance in Texas and explore finance options to secure affordable coverage.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to the world of auto insurance in Texas! Whether you’re a new driver or a long-time resident, understanding the ins and outs of auto insurance can be a daunting task. With so many factors that affect insurance rates and numerous options to choose from, finding the right coverage at an affordable price can seem overwhelming.

Auto insurance is a legal requirement in Texas, and for good reason. It provides financial protection in the event of an accident, ensuring that you and other motorists on the road are financially covered for any damages or injuries that may occur.

However, it’s important to note that auto insurance rates can vary significantly depending on various factors. These factors can include your age, driving record, the type and age of your vehicle, and even your credit history.

In this article, we will explore the various factors that affect auto insurance rates in Texas, delve into the minimum insurance requirements set by the state, analyze the average cost of auto insurance in Texas, discuss the key factors that determine your auto insurance rates, and provide tips on how to save money on auto insurance.

By the end of this article, you’ll have a thorough understanding of the auto insurance landscape in Texas and be equipped with the knowledge to make informed decisions about your coverage.

Factors Affecting Auto Insurance Rates in Texas

When it comes to determining auto insurance rates in Texas, several key factors come into play. Understanding these factors can help you comprehend why your insurance premium may be higher or lower than others.

1. Age and Gender: Younger drivers typically face higher insurance rates due to their lack of driving experience. Men also tend to face higher rates than women, as statistics show that male drivers are more prone to risky behavior on the road.

2. Driving Record: Your driving record plays a crucial role in determining your insurance rates. Drivers with a clean record, without any past accidents or traffic violations, are deemed less risky and can enjoy lower premiums.

3. Vehicle Type: The type of vehicle you drive can impact your insurance rates. Luxury cars or high-performance vehicles often have higher insurance premiums due to increased repair costs and higher chances of theft.

4. Credit History: In Texas, auto insurance companies can use your credit history to help determine your rates. Statistically, individuals with better credit scores are considered more financially responsible and may be eligible for lower insurance premiums.

5. Location: The area where you live and park your vehicle can affect your insurance rates. Urban areas with higher incidents of accidents and vehicle theft may lead to higher premiums compared to rural areas.

6. Coverage Levels: The amount of coverage you choose to purchase will also impact your insurance rates. Opting for higher coverage limits and additional policies, such as comprehensive and collision coverage, will increase your premiums.

7. Deductible Amount: The deductible amount is the portion you are responsible for in the event of a claim. Choosing a higher deductible can lower your rates, but it also means you will have to pay a larger portion out of pocket if you file a claim.

8. Mileage: The number of miles you drive annually can affect your insurance rates. Generally, the more you drive, the higher the risk of being involved in an accident, which can result in higher premiums.

By considering these factors, you can get a clearer idea of why your auto insurance rates may be what they are. It’s essential to review these factors periodically and discuss them with your insurance provider to ensure you have the best coverage at the most competitive rates.

Minimum Auto Insurance Requirements in Texas

In Texas, it is mandatory to carry auto insurance to protect yourself and other drivers on the road in case of an accident. To comply with the state’s regulations, you must have at least the minimum auto insurance coverage as outlined below:

- Bodily Injury Liability Coverage: You must have a minimum of $30,000 per person and $60,000 per accident in bodily injury liability coverage. This coverage pays for medical expenses, lost wages, and other damages if you are at fault in an accident that injures someone else.

- Property Damage Liability Coverage: You are required to have at least $25,000 in property damage liability coverage. This coverage pays for repairs or replacement of other vehicles or properties damaged in an accident where you are at fault.

- Uninsured/Underinsured Motorist Coverage: Texas law also requires drivers to have uninsured/underinsured motorist coverage with the same minimum limits as the bodily injury liability coverage mentioned above. This coverage protects you if you are involved in an accident with a driver who doesn’t have insurance or doesn’t have enough coverage to pay for your damages.

It’s important to note that these are the minimum requirements set by the state. While they are the legal minimum, they may not provide sufficient coverage in the event of a significant accident. Consider purchasing higher coverage limits and additional policies, such as comprehensive and collision coverage, to fully protect yourself and your vehicle.

Failing to maintain the mandatory minimum insurance coverage can result in serious consequences. You may face fines, suspension of your driver’s license, and even vehicle impoundment. It’s crucial to maintain continuous coverage and provide proof of insurance when requested by law enforcement or when registering or renewing your vehicle.

Remember, auto insurance is not just a legal obligation but also a financial safety net. Adequate coverage can help you navigate the aftermath of an accident and protect your assets from being depleted due to costly medical bills and property damage.

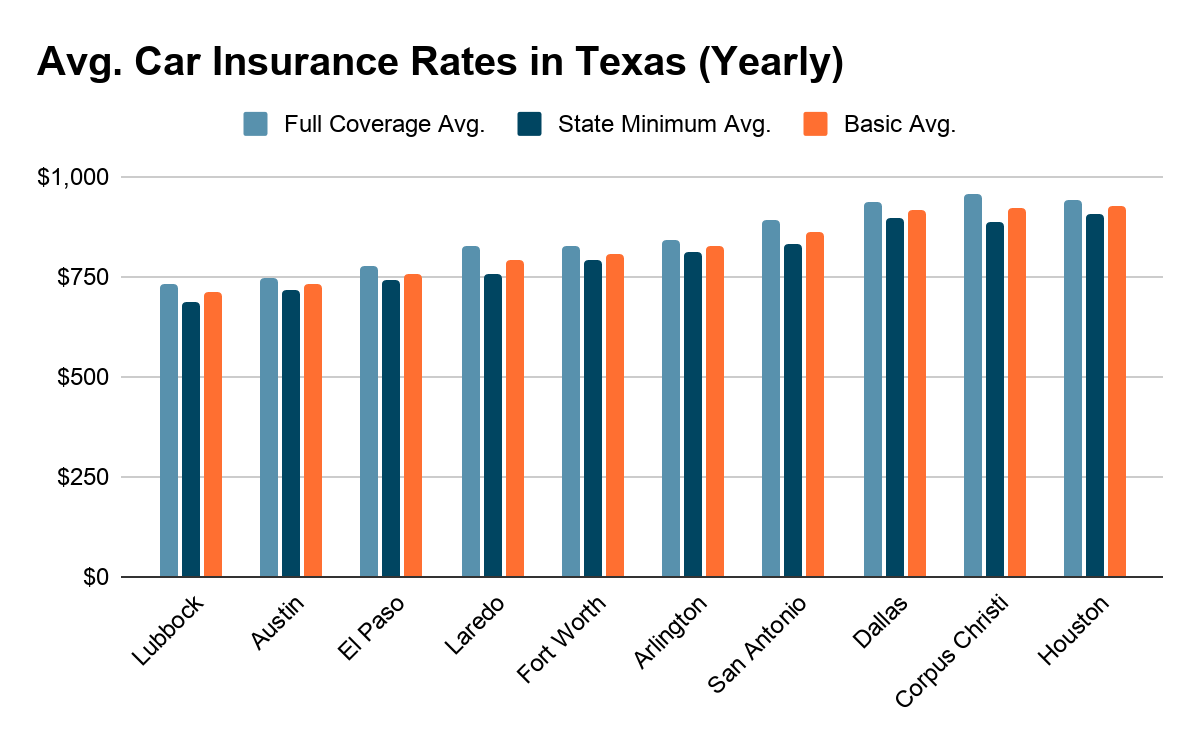

Average Cost of Auto Insurance in Texas

The cost of auto insurance in Texas varies based on several factors, including your age, driving history, location, and the type of coverage you choose. It’s important to have a general understanding of the average costs to help you budget and compare insurance quotes effectively.

According to the Insurance Information Institute, the average cost of auto insurance in Texas is around $1,300 to $1,400 per year. However, it’s crucial to remember that this is just an average, and your individual premiums may be higher or lower based on your unique circumstances.

Several factors contribute to the variation in auto insurance costs. Urban areas like Houston and Dallas tend to have higher premiums due to higher population densities, increased traffic, and higher instances of accidents and theft. On the other hand, rural areas may have lower premiums due to lower risk factors.

Other factors that affect insurance costs include your age and driving record. Younger drivers, especially teenagers, typically pay higher premiums due to their lack of experience behind the wheel. Older drivers with a clean driving record may enjoy lower rates.

The type of coverage you choose also impacts the costs. Opting for minimum coverage requirements will generally be less expensive, but it may not provide adequate coverage for more significant accidents. Adding additional coverage options, such as comprehensive and collision coverage, will increase your premiums but provide more extensive protection.

It’s important to note that these are averages, and individual premiums may vary. The best way to determine the exact cost of auto insurance is to obtain quotes from multiple insurance providers. By comparing quotes, you can find the best coverage at the most competitive rates that suit your specific needs.

Additionally, many insurance providers offer discounts for various reasons, including safe driving habits, completing defensive driving courses, having multiple policies with the same company, and maintaining a good credit score. Be sure to inquire about these discounts to potentially lower your insurance costs.

Remember, while cost is an essential factor when choosing auto insurance, it’s equally important to consider the coverage, customer service, and reputation of the insurance provider. Finding the right balance between cost and quality coverage is key to ensuring you have the protection you need on the road.

Factors That Determine Auto Insurance Rates in Texas

Auto insurance rates in Texas are determined by various factors that insurance companies consider when calculating premiums. Understanding these factors can help you better comprehend why your rates may be higher or lower than others. Here are the key factors that influence auto insurance rates in Texas:

1. Age and Gender: Younger drivers, especially teenagers, typically face higher insurance rates due to their lack of driving experience. On the other hand, older drivers with a clean driving record may enjoy lower rates. Additionally, statistics show that male drivers tend to have higher rates compared to female drivers.

2. Driving Record: Your driving record plays a significant role in determining your insurance rates. Drivers with a history of accidents and traffic violations are considered higher risk and will likely have higher premiums. Conversely, drivers with a clean record are deemed less risky and can enjoy lower rates.

3. Vehicle Type: The type of vehicle you drive can impact your insurance rates. Luxury cars or high-performance vehicles often have higher insurance premiums due to their higher value, increased repair costs, and higher chances of theft.

4. Credit History: In Texas, insurance companies can use your credit history to determine your insurance rates. Individuals with a poor credit score may be deemed higher risk and may face higher premiums. On the other hand, those with a good credit score are considered more financially responsible and may be eligible for lower insurance rates.

5. Location: The area where you live and park your vehicle can influence your insurance rates. Urban areas with higher population densities, more traffic congestion, and a higher incidence of accidents and vehicle theft may lead to higher premiums compared to rural areas.

6. Coverage Levels: The amount of coverage you choose to purchase will impact your insurance rates. Opting for higher coverage limits and additional policies, such as comprehensive and collision coverage, will increase your premiums compared to minimum coverage requirements.

7. Deductible Amount: The deductible amount is the portion you are responsible for paying in the event of a claim. Choosing a higher deductible can lower your insurance rates, but it also means you will have to pay a larger portion out of pocket if you file a claim.

8. Mileage: The number of miles you drive annually can affect your insurance rates. Generally, the more you drive, the higher the risk of being involved in an accident, which can result in higher premiums.

It’s important to note that each insurance company may weigh these factors differently. Some factors, such as age and driving record, tend to have a more significant impact on rates, while others may vary from one insurer to another. To get the best rates, it’s advisable to compare quotes from multiple insurance providers and choose the one that offers the most favorable rates based on your unique circumstances.

Tips for Saving Money on Auto Insurance in Texas

Auto insurance is a necessary expense, but that doesn’t mean you have to break the bank to get the coverage you need. Here are some tips to help you save money on auto insurance in Texas:

- Shop Around and Compare Quotes: Don’t settle for the first insurance quote you receive. Take the time to shop around and compare rates from multiple insurance providers. Each company uses different criteria to calculate premiums, so you may find significant variations in prices.

- Bundle Your Policies: Consider bundling your auto insurance with other insurance policies, such as homeowners or renters insurance, with the same company. Insurance companies often offer discounts for multiple policies.

- Maintain a Good Driving Record: Your driving record plays a crucial role in determining your insurance rates. Avoid accidents and traffic violations to keep your record clean. Some insurance companies offer safe driver discounts for maintaining a good driving record.

- Increase Your Deductible: Opting for a higher deductible can lower your insurance premiums. Just be sure that you can afford to pay the deductible amount out of pocket if you need to file a claim.

- Consider Your Coverage Needs: Assess your coverage needs carefully. While it’s important to have adequate coverage, you may be paying for extras that you don’t need. Adjusting your coverage limits and dropping unnecessary coverage options can help reduce your premiums.

- Ask About Discounts: Inquire with your insurance provider about any available discounts. Many companies offer discounts for things like safe driving habits, completing defensive driving courses, being a good student, or having certain safety features installed in your vehicle.

- Improve Your Credit Score: Maintaining a good credit score can positively impact your insurance rates. Pay your bills on time, reduce outstanding debts, and regularly check your credit report to ensure its accuracy.

- Drive Less: If possible, reduce your annual mileage. Insurance companies often consider lower mileage drivers to be at a lower risk of accidents and may offer lower premiums.

- Review and Update Your Policy Regularly: Periodically review your auto insurance policy to ensure it still meets your needs. As your circumstances change, such as getting married, moving, or purchasing a new car, your insurance needs may change as well.

- Consider Usage-Based or Pay-Per-Mile Insurance: Some insurers offer usage-based or pay-per-mile insurance, where your premium is based on the actual miles you drive or your driving behavior. If you are a low-mileage or safe driver, this type of insurance may help you save money.

Remember, while it’s important to save money on auto insurance, never sacrifice necessary coverage to cut costs. Always prioritize having adequate protection on the road. By implementing these tips and being proactive in seeking out discounts, you can find affordable auto insurance without compromising on quality coverage.

Conclusion

Navigating the world of auto insurance in Texas can be complex, but armed with the right knowledge, you can make informed decisions about your coverage and save money in the process. Understanding the factors that affect your insurance rates, knowing the minimum insurance requirements, and being aware of the average cost of insurance in Texas are essential steps in securing the right coverage for your needs.

Factors such as your age, driving record, location, vehicle type, and coverage levels all play a role in determining your auto insurance rates. By considering these factors and exploring ways to lower your premiums, such as shopping around for quotes, maintaining a good driving record, and taking advantage of available discounts, you can potentially save money on your auto insurance policy.

It’s important to review your insurance policy regularly to ensure it still meets your needs and accommodates any changes in your circumstances. As life events occur, such as buying a new car, moving, or getting married, it’s crucial to reassess your coverage levels and make any necessary adjustments.

Remember, the cost of auto insurance should not be the sole determining factor in choosing a provider. Consider the reputation and customer service of the insurance company, as well as the coverage options they offer. Striking the right balance between affordability and quality coverage is key to ensuring you have the protection you need when you hit the road.

By implementing the tips provided in this article and being proactive in managing your auto insurance, you can navigate the system with confidence, secure the coverage you require, and potentially save money on your premiums. Protecting yourself, your vehicle, and others on the road should always be a top priority, and choosing the right auto insurance policy helps you achieve that peace of mind.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance