Finance

How Much Of A $1500 Credit Limit Should I Use

Published: March 5, 2024

Learn how to manage your $1500 credit limit wisely and improve your financial health. Discover the ideal credit utilization ratio for maximum benefits.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to the world of credit utilization and the pivotal role it plays in managing your finances. As you embark on your journey towards financial well-being, understanding the nuances of credit utilization is paramount. It’s not just about swiping your credit card; it’s about strategically managing your available credit to optimize your financial health.

When it comes to credit cards, the concept of credit utilization refers to the percentage of your available credit that you’re currently using. This metric holds significant weight in the realm of credit scoring and financial management. With a $1500 credit limit at your disposal, it’s essential to comprehend the impact of your credit utilization on your overall financial standing.

Join me as we delve deeper into the intricacies of credit utilization, exploring the factors to consider, the impact on your credit score, and the best practices for optimizing your credit utilization. By the end of this journey, you’ll be equipped with the knowledge and insights to make informed decisions regarding your credit utilization and, ultimately, take control of your financial destiny.

Understanding Credit Utilization

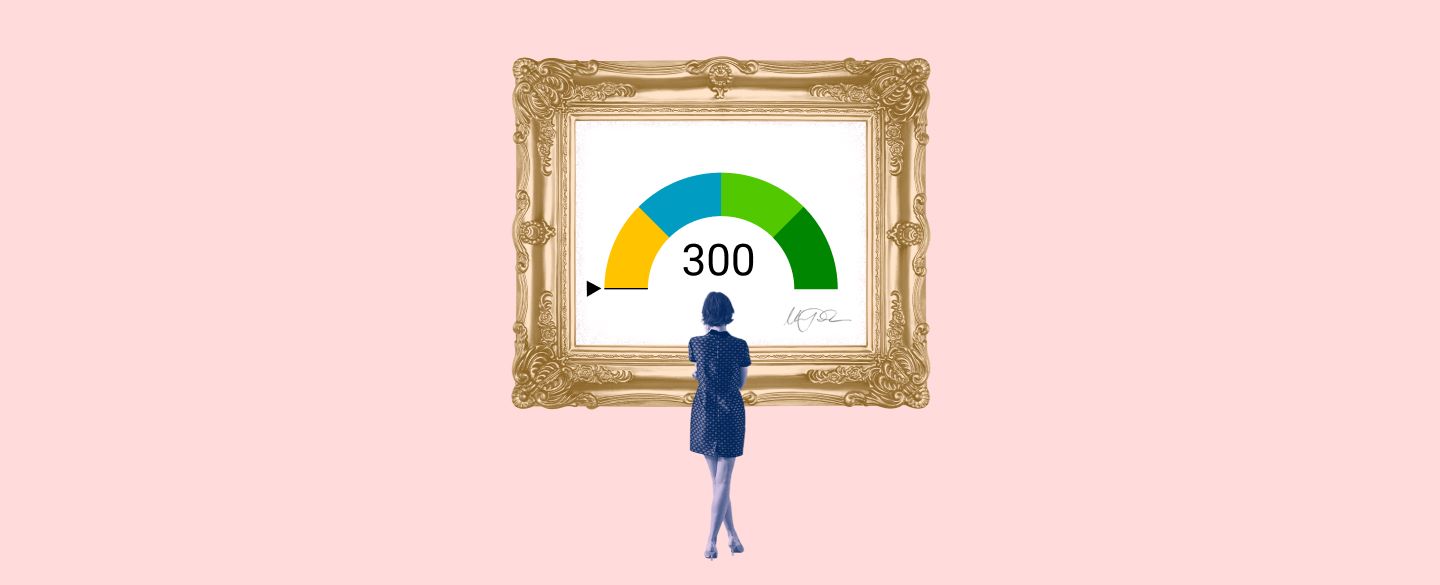

Credit utilization is a fundamental concept that reflects the relationship between your credit card balances and your credit limits. It is calculated by dividing your total credit card balances by your total credit limits, resulting in a percentage that signifies how much of your available credit you are currently using. For instance, if you have a $1500 credit limit and a $500 balance, your credit utilization rate would be 33.33%.

This metric holds significant weight in the determination of your credit score. Lenders and credit bureaus scrutinize your credit utilization to assess your financial responsibility and risk. A lower credit utilization rate is generally perceived favorably, as it indicates that you are not overly reliant on credit and are effectively managing your finances.

Understanding the impact of credit utilization on your financial well-being is crucial. By comprehending the dynamics of this metric, you can make informed decisions regarding your credit usage, thereby optimizing your credit score and overall financial health. Let’s explore the factors that should be taken into account when evaluating your credit utilization.

Factors to Consider

When evaluating your credit utilization, several factors warrant careful consideration to ensure a comprehensive understanding of your financial standing. These factors play a pivotal role in shaping your credit utilization rate and, consequently, your credit score. Let’s delve into the key elements that should be taken into account:

- Credit Limit: The amount of credit available to you significantly influences your credit utilization. With a $1500 credit limit, managing your credit usage within this threshold is vital for optimizing your credit score.

- Outstanding Balances: The balances on your credit accounts directly impact your credit utilization rate. Keeping your balances low in proportion to your credit limits is essential for maintaining a healthy credit utilization ratio.

- Payment Patterns: Your payment history and patterns play a crucial role in managing your credit utilization. Timely payments contribute to a positive credit utilization rate, reflecting responsible financial behavior.

- Credit Card Usage: The frequency and distribution of credit card usage can influence your credit utilization. Strategic use of credit cards and mindful spending habits contribute to an optimal credit utilization ratio.

By considering these factors and their interplay, you can gain valuable insights into your credit utilization and make informed decisions to enhance your financial well-being. Now, let’s explore the impact of credit utilization on your credit score, shedding light on its significance in the realm of credit management.

Impact on Credit Score

Your credit utilization plays a pivotal role in shaping your credit score, exerting a considerable influence on your overall financial standing. Credit scoring models, such as FICO and VantageScore, consider your credit utilization rate as a key factor in assessing your creditworthiness. With a $1500 credit limit, the impact of your credit utilization on your credit score is substantial.

A high credit utilization rate, indicating that you are utilizing a significant portion of your available credit, can adversely affect your credit score. Lenders may perceive high credit utilization as a potential risk, potentially leading to a lower credit score. On the other hand, maintaining a low credit utilization rate, ideally below 30%, can positively impact your credit score, signifying responsible credit management and financial prudence.

It’s important to note that your credit utilization is a dynamic metric, subject to change based on your credit card usage and payment patterns. By vigilantly managing your credit utilization, especially within the confines of your $1500 credit limit, you can proactively influence your credit score, paving the way for enhanced financial opportunities and favorable lending terms.

Now, let’s explore the best practices for optimizing your credit utilization, equipping you with actionable strategies to harness the potential of your available credit while fortifying your financial foundation.

Best Practices for Credit Utilization

Optimizing your credit utilization involves implementing strategic practices to maintain a healthy balance between your credit card balances and credit limits. With a $1500 credit limit at your disposal, adhering to best practices for credit utilization is paramount for fostering a robust financial profile. Let’s explore actionable strategies to effectively manage your credit utilization:

- Monitor Your Credit Utilization: Regularly monitor your credit card balances and credit limits to gauge your credit utilization rate. Awareness of your utilization percentage empowers you to make informed decisions regarding your credit usage.

- Strive for Low Balances: Aim to keep your credit card balances low in relation to your credit limits, ideally below 30% utilization. This practice demonstrates prudent credit management and positively impacts your credit score.

- Pay Balances in Full: Whenever possible, endeavor to pay off your credit card balances in full each month. Responsible and timely payments contribute to a favorable credit utilization rate, bolstering your financial standing.

- Strategic Credit Card Usage: Use your credit cards strategically, aligning your spending with your available credit. Mindful utilization of your credit cards contributes to a balanced credit utilization ratio.

- Consider Credit Limit Increases: Requesting a credit limit increase, if feasible and prudent, can positively impact your credit utilization rate. However, exercise caution to avoid overextending your credit capacity.

By incorporating these best practices into your financial management approach, you can harness the potential of your $1500 credit limit while nurturing a healthy credit utilization rate. These strategies not only contribute to an optimal credit score but also position you for improved financial opportunities and favorable lending terms.

As we conclude this exploration of credit utilization, you are now equipped with a comprehensive understanding of this critical financial metric and actionable insights to navigate the realm of credit management with confidence and prudence.

Conclusion

Credit utilization, with its profound impact on credit scoring and financial well-being, is a cornerstone of responsible credit management. As we reflect on the significance of credit utilization, particularly in the context of a $1500 credit limit, it becomes evident that vigilantly managing your available credit is essential for cultivating a robust financial profile.

By comprehending the dynamics of credit utilization and the factors that influence it, you gain valuable insights into optimizing your credit score and enhancing your financial standing. The interplay between credit limits, outstanding balances, payment patterns, and credit card usage underscores the multifaceted nature of credit utilization, emphasizing the need for strategic and informed decision-making.

Understanding the impact of credit utilization on your credit score empowers you to proactively influence your financial trajectory. By adhering to best practices, such as monitoring your credit utilization, maintaining low balances, and employing strategic credit card usage, you can leverage your $1500 credit limit to fortify your financial foundation and unlock opportunities for financial growth.

As you navigate the landscape of credit utilization, remember that knowledge is your most potent tool. By embracing a proactive and informed approach to credit management, you can harness the potential of your available credit while cultivating a positive credit utilization rate. This, in turn, positions you for enhanced financial prospects and a secure financial future.

Armed with a comprehensive understanding of credit utilization and actionable strategies for optimizing your credit utilization, you are poised to embark on your financial journey with confidence, resilience, and a steadfast commitment to financial well-being.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance