Finance

How To Get A Car No Credit

Modified: February 21, 2024

Learn how to finance a car even with no credit. Find out the best ways to get a car loan without a credit history and start driving today!

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When it comes to purchasing a car, having no credit history can make the process seem daunting. Without a credit score, traditional lenders may be hesitant to provide you with a car loan. However, it is not impossible to get a car with no credit. In this article, we will explore strategies and tips for obtaining a car loan and buying the car you need, even if you have no credit history.

Having no credit can be a result of various factors, such as being a recent graduate, an immigrant, or simply not having any previous borrowing history. While having no credit can pose challenges, it can also be an opportunity to establish a positive credit history with responsible borrowing.

Before diving into the world of car financing, it’s important to understand the basics. Car financing involves borrowing money from a lender to purchase a vehicle and paying it back over a predetermined period of time, typically through monthly installments. The lender, whether it’s a bank, credit union, or dealership, will charge interest on the loan amount, which you’ll need to consider when budgeting for your car purchase.

Now, let’s get started on your journey to getting a car with no credit. We will discuss how to build your credit, research loan options, gather necessary documents, apply for a car loan, negotiate loan terms, and finally, how to purchase your desired car. By following these steps, you can increase your chances of successfully obtaining a car loan and driving away in the car of your dreams.

Understanding Car Financing with No Credit

When you have no credit history, it’s important to understand how car financing works and the options available to you. While it may be more challenging to secure a car loan without credit, it is not impossible. Here are a few key points to consider:

1. Interest Rates: Lenders may offer higher interest rates to applicants with no credit history. This is because they consider you a higher risk borrower. It’s essential to shop around and compare rates from different lenders to ensure you’re getting the best deal possible.

2. Down Payment: Making a larger down payment can often improve your chances of getting approved for a car loan. Not only does it show lenders that you are committed to the purchase, but it also reduces the loan amount, making it less risky for lenders.

3. Co-Signer: If possible, consider asking a family member or trusted friend with a good credit history to be a co-signer on the loan. This can provide additional assurance to lenders, increasing your chances of getting approved.

4. Alternative Lenders: If traditional lenders are reluctant to grant you a car loan, explore alternative lending options. There are specialized lenders who work with individuals who have no credit or poor credit history. These lenders may have different approval criteria and interest rates, so be sure to do your research.

5. Online Lenders: Online lenders have become increasingly popular in recent years, providing convenient and accessible car financing options. Many online lenders specialize in assisting individuals with no credit history. You can compare rates and terms from different online lenders to find the best fit for your needs.

Remember, while it may be more challenging to obtain a car loan without credit, it is not impossible. By understanding the unique circumstances of financing without credit, you can navigate the process more effectively and increase your chances of securing a car loan that fits your needs and budget.

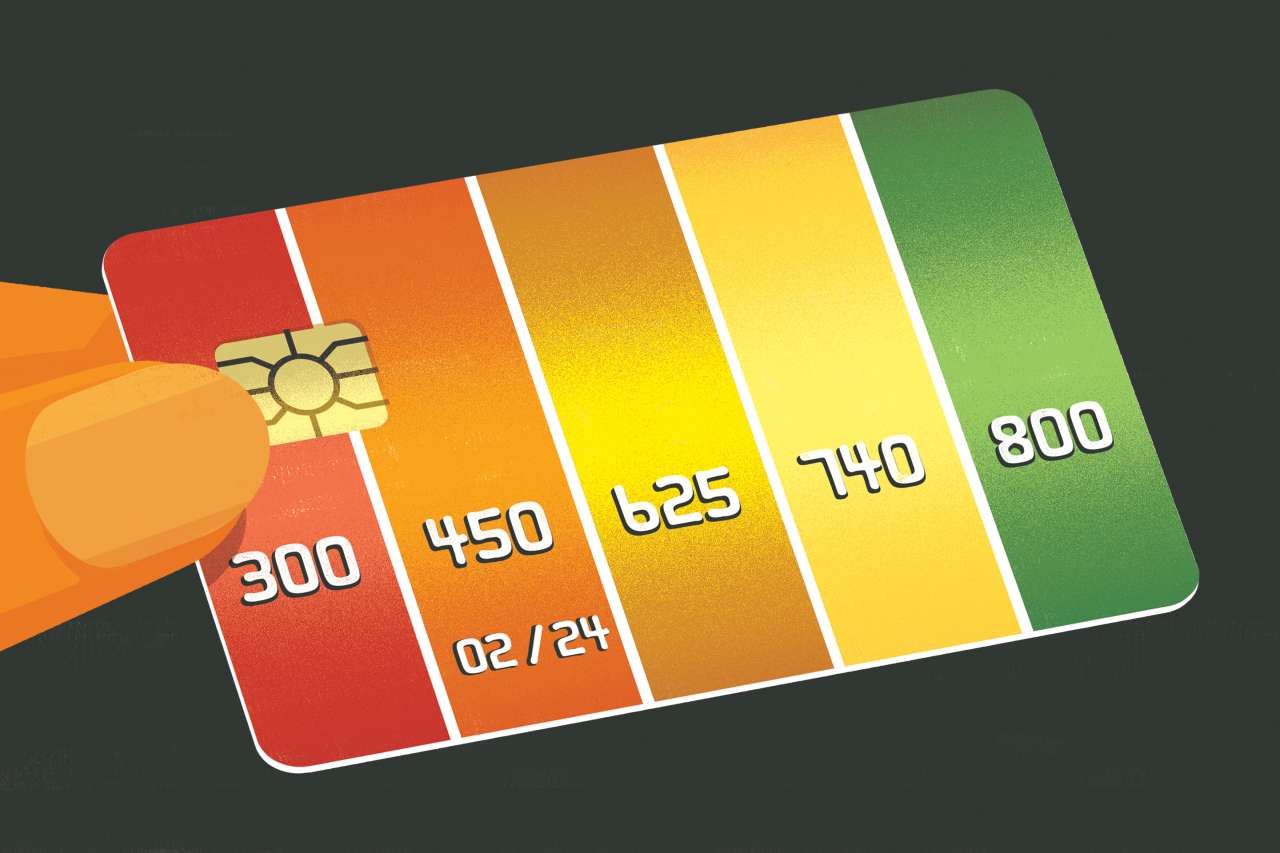

Building Your Credit

If you have no credit history, it’s essential to start building your credit profile. Having a good credit score not only increases your chances of getting approved for a car loan but also opens up opportunities for better interest rates and loan terms. Here are some steps you can take to build your credit:

1. Open a Secured Credit Card: A secured credit card is a great tool for establishing credit. With a secured credit card, you deposit a certain amount of money as collateral, and this becomes your credit limit. Be sure to make small purchases and pay off the balance in full each month to demonstrate responsible credit behavior.

2. Become an Authorized User: If you have a trusted family member or friend with good credit, ask them to add you as an authorized user on one of their credit cards. This allows their positive payment history to be reported on your credit report, helping you build credit.

3. Pay Bills on Time: Consistently paying your bills on time, such as rent, utilities, and student loans, helps establish a positive payment history. Late payments can negatively impact your credit score, so make it a priority to pay all your bills by the due date.

4. Keep Credit Utilization Low: Your credit utilization ratio is the percentage of your available credit that you are using. It’s generally recommended to keep your credit utilization below 30%. Keeping this ratio low shows lenders that you are responsibly managing your credit.

5. Diversify Your Credit: Having a mix of credit types, such as credit cards, installment loans, and student loans, can positively impact your credit score. Aim to have a balanced mix of credit accounts to showcase your ability to handle different types of credit responsibly.

6. Regularly Check Your Credit Report: It’s important to regularly review your credit report for any errors or discrepancies. You can obtain a free copy of your credit report from each of the three major credit bureaus – Equifax, Experian, and TransUnion – once a year. If you find any errors, report them and have them corrected promptly.

Building credit takes time, so it’s crucial to be patient and consistent in your efforts. By demonstrating responsible credit behavior and maintaining a positive credit history, you can improve your creditworthiness and increase your chances of securing a car loan at favorable terms.

Researching Loan Options

When you have no credit history, it’s crucial to thoroughly research your loan options to find the best fit for your circumstances. Here are some key factors to consider when researching car loan options:

1. Traditional Lenders: Start by exploring loan options from traditional lenders such as banks and credit unions. While they may have stricter approval requirements, they often offer competitive interest rates and favorable terms.

2. Specialized Lenders: Look for lenders who specialize in working with individuals who have no credit or poor credit history. These lenders understand your unique situation and may have more flexible approval criteria and tailored loan options.

3. Online Lenders: Online lenders offer convenience, quick application processes, and competitive rates. They often have a variety of loan programs available, including options for borrowers with no credit history.

4. Dealership Financing: Many car dealerships offer financing options to customers. While dealership financing can be convenient, it’s important to carefully review the terms, interest rates, and any additional fees associated with the loan. Be cautious of dealerships that offer excessive interest rates or add-ons that might not be necessary.

5. Comparison Shopping: Take the time to compare loan offers from different lenders. Look at the interest rates, loan terms, and any other fees associated with the loan. Doing thorough research and comparison shopping can help you secure the best loan terms available.

6. Loan Pre-Approval: Consider getting pre-approved for a loan before going to the dealership. Pre-approval gives you an idea of the loan amount you qualify for and the interest rate you can expect. This allows you to shop for a car within your budget and negotiate with confidence.

7. Loan Terms: When reviewing loan options, pay attention to the loan term. While longer loan terms may result in lower monthly payments, they often come with higher interest rates and can end up costing you more in the long run. Choose a loan term that allows you to comfortably afford the monthly payments without stretching your budget.

Remember to consider not only the interest rates and loan terms but also the reputation and customer service of the lender. Reading reviews and seeking recommendations can provide valuable insights into the lender’s reputation and customer experience.

By thoroughly researching your loan options and being aware of the various lenders available to you, you can make an informed decision that aligns with your financial goals and helps you get the best car loan with no credit.

Gathering the Necessary Documents

When applying for a car loan with no credit, it’s important to gather the necessary documents to present to potential lenders. Having all the required documentation ready can streamline the application process and increase your chances of approval. Here are the key documents you may need to gather:

1. Proof of Identity: Lenders will require proof of your identity, such as a valid driver’s license or passport. Make sure your identification documents are current and valid.

2. Proof of Income: Lenders need to verify your ability to repay the loan. Gather documents that demonstrate your income, such as recent pay stubs, bank statements, or tax returns for self-employed individuals. If you receive any additional sources of income, such as alimony or rental income, include documentation for these as well.

3. Employment Verification: Lenders may want to confirm your employment status and stability. Prepare documents such as employer contact information, recent employment letters, or W-2 forms to provide evidence of regular employment.

4. Proof of Address: Lenders will usually ask for proof of your residence. Provide documents such as utility bills, rental agreements, or mortgage statements that show your current address.

5. Banking Information: Be prepared to provide your banking information, including bank account statements and account numbers. This information helps lenders assess your financial stability and the availability of funds for down payments or loan repayments.

6. Personal References: Some lenders may request personal references to vouch for your character and reliability. Prepare a list of references with their contact information, such as friends or family members who can speak positively about you.

7. Car Information: If you have already identified a specific car you wish to purchase, gather the necessary information, such as the make, model, year, and VIN (Vehicle Identification Number). This information will be required during the application process.

It’s essential to have both physical and digital copies of the documents ready for submission. Organize your documents in a folder or file to keep them easily accessible throughout the loan application process.

Remember, lenders may have specific requirements and ask for additional documents based on their lending policies. It’s always a good idea to contact potential lenders beforehand to confirm the exact documents they need for a car loan application.

By having all the necessary documents prepared and organized, you can demonstrate your readiness and professionalism to lenders, increasing your chances of a successful car loan application process.

Applying for a Car Loan

Once you have gathered all the necessary documents and conducted thorough research on loan options, it’s time to apply for a car loan. Here are the steps to follow when applying for a car loan with no credit:

1. Choose the Right Lender: Based on your research, select the lender that offers the most favorable terms and conditions for your situation. Consider factors such as interest rates, loan terms, and customer reviews.

2. Online Application or In-Person: Most lenders offer the option to apply for a car loan online or in-person at a dealership or lending institution. Choose the method that is most convenient for you. If applying online, ensure that the website is secure and your personal information is protected.

3. Complete the Application Form: Fill out the car loan application form with accurate and up-to-date information. Double-check all the details to avoid any errors that could delay the application process.

4. Provide the Necessary Documentation: Submit all the required documents along with your application form. This may include proof of identity, proof of income, employment verification, proof of address, and car information.

5. Review and Submit: Before submitting your application, review all the information you have provided. Ensure that everything is accurate and complete. Submit the application along with the required documents as per the lender’s instructions.

6. Wait for Approval: After submitting your application, the lender will review it and assess your eligibility for a car loan. This process may take a few days, so be patient and avoid applying for multiple loans simultaneously, as this can negatively impact your credit.

7. Negotiate if Needed: If you receive a loan offer that is not aligned with your expectations, consider negotiating with the lender. You may be able to negotiate for better interest rates, loan terms, or additional benefits. Be prepared to provide any additional information or documentation that the lender may request.

8. Read and Understand the Loan Agreement: If your loan application is approved, carefully review the loan agreement before signing it. Pay close attention to the terms and conditions, including the interest rate, monthly payments, repayment period, and any penalties or fees associated with the loan.

9. Close the Loan: Once you are satisfied with the loan terms, sign the loan agreement and complete any additional documentation required by the lender. This final step officially closes the loan process, and you can proceed with purchasing your desired car.

Remember, obtaining a car loan with no credit requires patience and perseverance. If you receive multiple loan offers, take the time to compare them carefully before making a decision. By following these steps and being diligent throughout the application process, you can secure a car loan that meets your needs and helps you establish a positive credit history.

Negotiating the Terms of the Loan

When applying for a car loan with no credit, it’s important to remember that the terms of the loan are not set in stone. Negotiating with the lender can help you secure more favorable terms and potentially save you money in the long run. Here are some tips for negotiating the terms of the loan:

1. Do Your Research: Prior to negotiating, research current interest rates, loan terms, and offers from different lenders. This will give you a better understanding of what is reasonable and competitive in the market.

2. Use Online Loan Comparisons: Utilize online tools that allow you to compare loan offers from multiple lenders. This will give you a clear idea of what options are available and help you negotiate based on these comparisons.

3. Highlight Your Financial Strengths: If you have a stable income, a good employment history, or significant savings for a down payment, make sure to highlight these strengths to the lender. This can help showcase your ability to handle the loan responsibly and potentially strengthen your negotiating position.

4. Get Pre-Approved Offers: It’s advantageous to have pre-approved offers from multiple lenders. This allows you to use the pre-approved offers as leverage during negotiations, as the lenders compete for your business.

5. Negotiate the Interest Rate: The interest rate is one of the primary factors determining the cost of your loan. If you have researched and received pre-approved offers with lower interest rates, use these offers as a starting point for negotiating a lower rate with the lender.

6. Negotiate the Loan Term: The loan term affects both the monthly payments and the overall cost of the loan. If you prefer a longer-term to keep your monthly payments affordable, negotiate for a lower interest rate to offset the extended repayment period.

7. Consider Additional Fees and Charges: Be aware of any additional fees or charges associated with the loan, such as origination fees or prepayment penalties. If you encounter such fees, negotiate to have them reduced or waived altogether.

8. Be Willing to Walk Away: If the lender is not willing to negotiate on the terms, be prepared to walk away and explore other options. Remember that you have the power as the borrower, and there are alternative lenders who may offer more favorable terms.

9. Seek Professional Advice: If you are unsure about the negotiation process or need assistance, consider seeking advice from a financial advisor or consultant. They can provide insights and guidance to help you navigate the negotiation process effectively.

Remember, negotiation is a give-and-take process. Be polite but firm in expressing your expectations and requirements. With proper research, preparation, and confidence, you can negotiate a car loan with terms that better align with your financial goals and needs.

Buying a Car with No Credit

Buying a car with no credit may seem challenging, but with proper planning and research, it is entirely possible. Here are some key steps to consider when purchasing a car with no credit:

1. Set a Realistic Budget: Determine how much you can afford to spend on a car. Consider factors such as your income, expenses, and future financial goals. It’s important to choose a vehicle that fits within your budget to avoid overextending yourself.

2. Research Car Options: Begin by researching different makes and models that suit your needs and budget. Consider factors such as fuel efficiency, reliability, safety features, and maintenance costs. Look for used cars that are known for retaining their value and have a good track record.

3. Consider Financing Options: Explore your financing options, including car loans for individuals with no credit. Look for lenders who offer flexible terms and competitive interest rates. Consider both traditional banks and credit unions as well as online lenders who specialize in working with borrowers with less credit history.

4. Save for a Down Payment: If possible, save for a down payment. A higher down payment can reduce the loan amount and potentially improve your chances of getting approved for a loan with favorable terms. It can also help to lower your monthly payments and overall interest costs.

5. Beware of Predatory Lending Practices: As a borrower with no credit, you might be targeted by predatory lenders who offer extremely high-interest rates or unnecessary add-ons. Be cautious and carefully read through loan terms and agreements. If something seems too good to be true or feels suspicious, trust your instincts and consider alternative options.

6. Secure Insurance Coverage: Before purchasing a car, make sure to obtain car insurance coverage. Insurance is not only a legal requirement in most places, but it also protects you financially in case of accidents or damages to the vehicle.

7. Consider a Co-Signer: If you’re having trouble getting approved for a car loan on your own, you can seek a co-signer. A co-signer is someone with a good credit history who agrees to take on the responsibility of the loan if you default. This can increase your chances of loan approval and potentially help you secure a better interest rate.

8. Negotiate the Purchase Price: When visiting car dealerships or negotiating with private sellers, don’t be afraid to negotiate the price. Research the value of the car and use that information to guide your negotiation. Be firm but reasonable in your negotiations, and be prepared to walk away if the price is not right.

Remember to read and understand all contracts and agreements before signing. If you’re unsure about any terms, don’t hesitate to seek legal or financial advice.

Buying a car with no credit may require a bit of extra effort, but it is certainly possible. With careful planning, thorough research, and smart financial decisions, you can successfully purchase a car that meets your needs and sets you on a path to building a positive credit history.

Tips for Maintaining Good Credit

Building and maintaining good credit is essential for long-term financial success. Here are some tips to help you maintain a positive credit history:

1. Make Payments on Time: Paying your bills and loan installments on time is crucial for maintaining good credit. Late or missed payments can have a negative impact on your credit score and make it difficult to qualify for future loans or credit.

2. Keep Credit Utilization Low: Aim to keep your credit utilization ratio, which is the amount of credit you use compared to your available credit, below 30%. Keeping this ratio low demonstrates responsible credit management and can positively impact your credit score.

3. Avoid Taking on Excessive Debt: Be cautious about taking on too much debt, as lenders consider your debt-to-income ratio when assessing your creditworthiness. Keep your debt levels manageable and only borrow what you can comfortably afford to repay.

4. Monitor Your Credit Reports: Regularly check your credit reports from the major credit bureaus (Equifax, Experian, and TransUnion) to ensure they are accurate and free of errors. If you notice any discrepancies, report them and have them corrected promptly.

5. Limit Credit Applications: Avoid applying for multiple lines of credit within a short period as this can negatively impact your credit score. Each application typically triggers a hard inquiry on your credit report, which can lower your score temporarily.

6. Maintain a Mix of Credit: A healthy credit mix, including different types of credit accounts (e.g., credit cards, loans), can positively impact your credit score. This shows lenders that you can manage various credit responsibilities effectively.

7. Keep Old Accounts Open: Closing old credit accounts can shorten your credit history and lower your credit score. Consider keeping older accounts open, even if you no longer use them, to maintain a longer credit history.

8. Use Credit Responsibly: Use credit cards and loans responsibly by making regular, on-time payments and avoiding excessive debt. It’s essential to use credit as a tool to build a positive credit history rather than relying on it for unnecessary purchases.

9. Educate Yourself: Stay informed about personal finance and credit management. Understand the terms and conditions of your credit agreements, including interest rates, fees, and penalties. By being knowledgeable, you can make informed decisions and protect your creditworthiness.

10. Seek Professional Assistance: If you find yourself struggling to manage your credit, consider seeking advice from a credit counselor or financial advisor. They can provide guidance on budgeting, debt management, and credit improvement strategies.

Remember, maintaining good credit is an ongoing process that requires responsible financial habits. By implementing these tips and taking control of your credit, you can build and preserve a solid credit history that opens doors to future financial opportunities.

Conclusion

Purchasing a car with no credit may seem daunting, but it is entirely possible with the right strategies and mindset. By understanding the car financing process, building credit, researching loan options, gathering the necessary documents, and effectively negotiating the terms of the loan, you can successfully buy a car and establish a positive credit history.

Remember to set a realistic budget, research car options, and consider financing options from both traditional and specialized lenders. Use your newfound knowledge to negotiate the terms of the loan, including the interest rate, loan term, and additional fees. Be diligent in gathering all the necessary documents and carefully review all agreements before signing.

Maintaining good credit is essential for long-term financial success. Make payments on time, keep your credit utilization low, and avoid taking on excessive debt. Regularly monitor your credit reports and be mindful of your credit applications. By using credit responsibly and educating yourself on credit management, you can maintain a positive credit history.

While the journey of buying a car with no credit may have its challenges, it is an opportunity to establish a solid foundation for your financial future. By following the tips and strategies outlined in this article, you can overcome obstacles, secure a car loan, and embark on the road to financial success.

Remember, building credit takes time, and it’s important to be patient and consistent in your efforts. With responsible borrowing and diligent credit management, you can pave the way for future financial opportunities and achieve your goals.

So, take the leap and confidently navigate the car financing process. With determination and the right knowledge, you can get behind the wheel of the car you need and build a strong credit history along the way.

What's Hot

Latest Articles

Related Post

By: Sunny • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance