Finance

Loan Credit Default Swap (LCDS) Definition

Published: December 19, 2023

Learn about the definition of Loan Credit Default Swap (LCDS) and its significance in the world of finance.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Understanding Loan Credit Default Swap (LCDS)

When it comes to the world of finance, there are various complex instruments and terms that may leave even the most knowledgeable individuals scratching their heads. One such term is Loan Credit Default Swap, commonly referred to as LCDS. In this article, we will delve into the definition of LCDS, explaining its purpose and how it functions within the financial industry.

Key Takeaways:

- Loan Credit Default Swap (LCDS) is a derivative instrument used in the financial market to protect against the risk of default on certain loans.

- LCDS allows investors to transfer the credit risk associated with a particular loan or a portfolio of loans to another party in exchange for regular payments.

What is Loan Credit Default Swap?

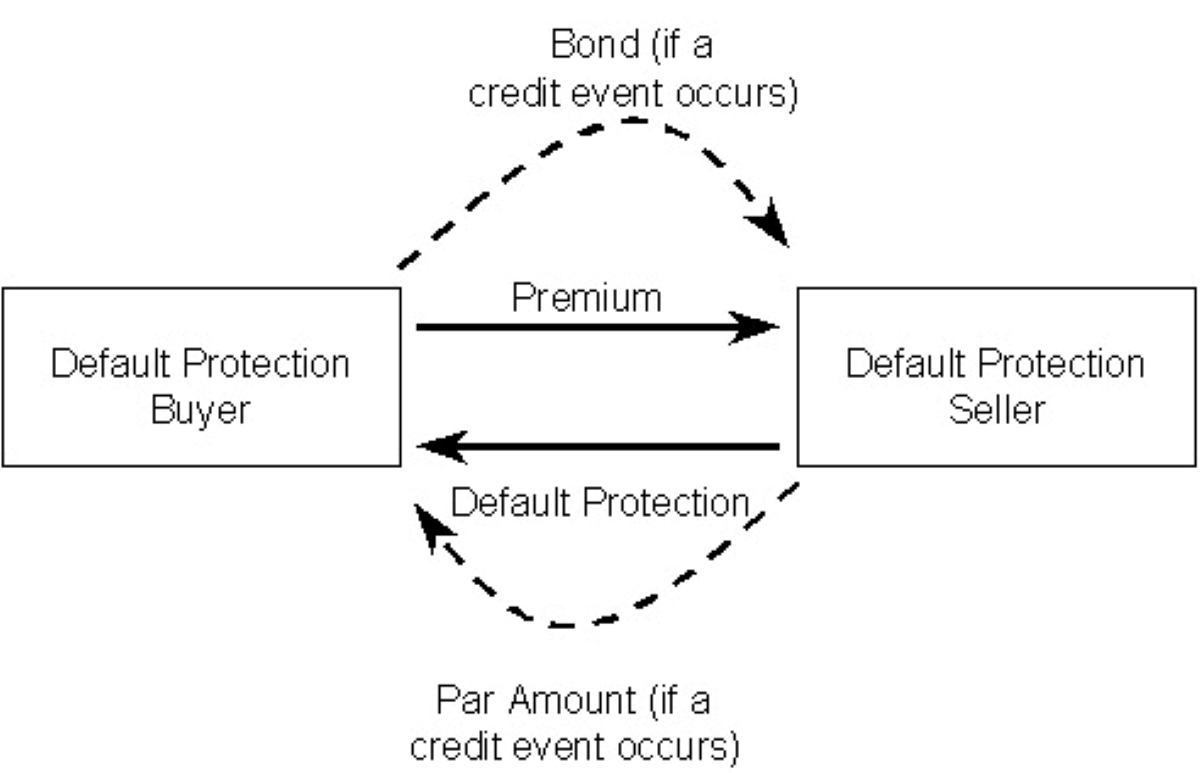

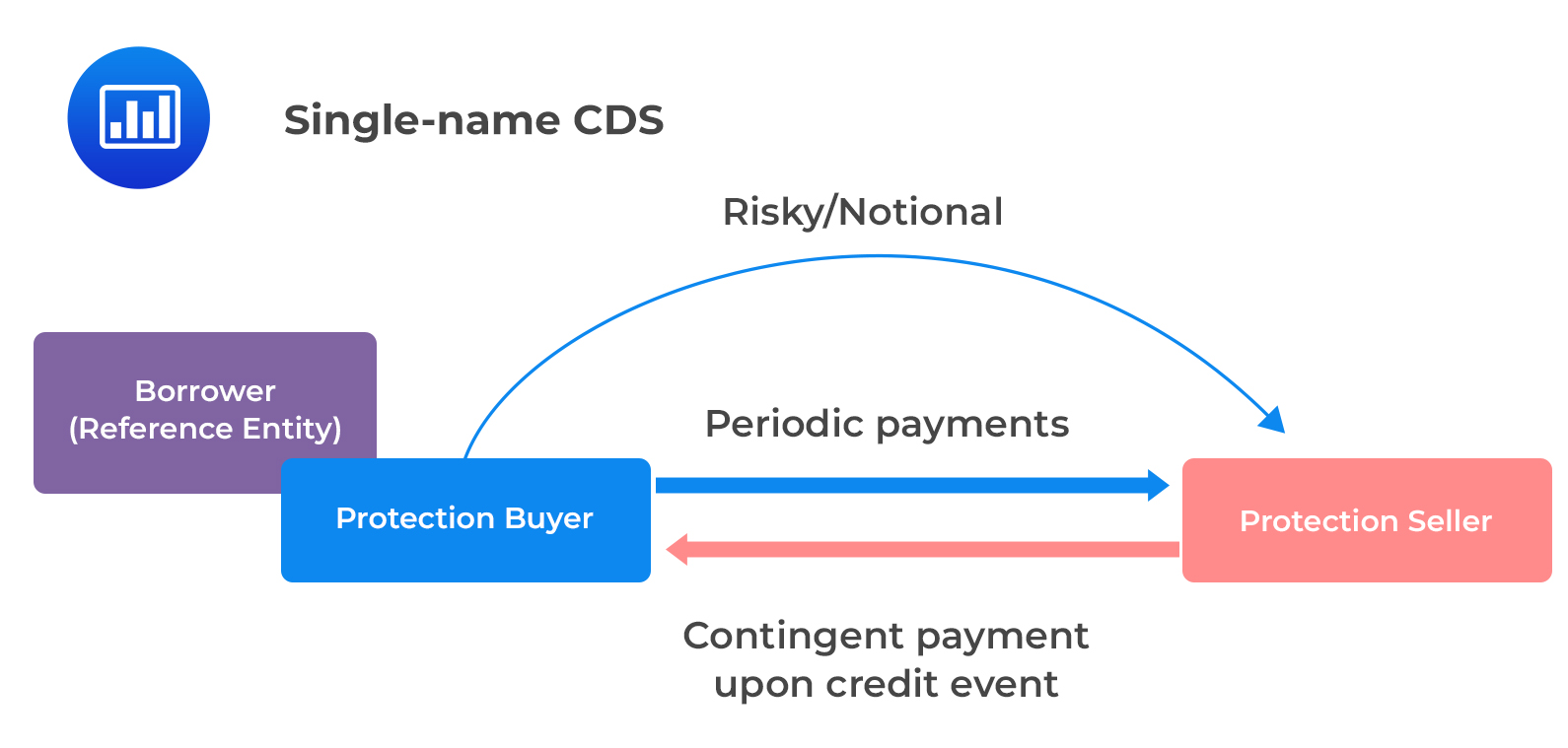

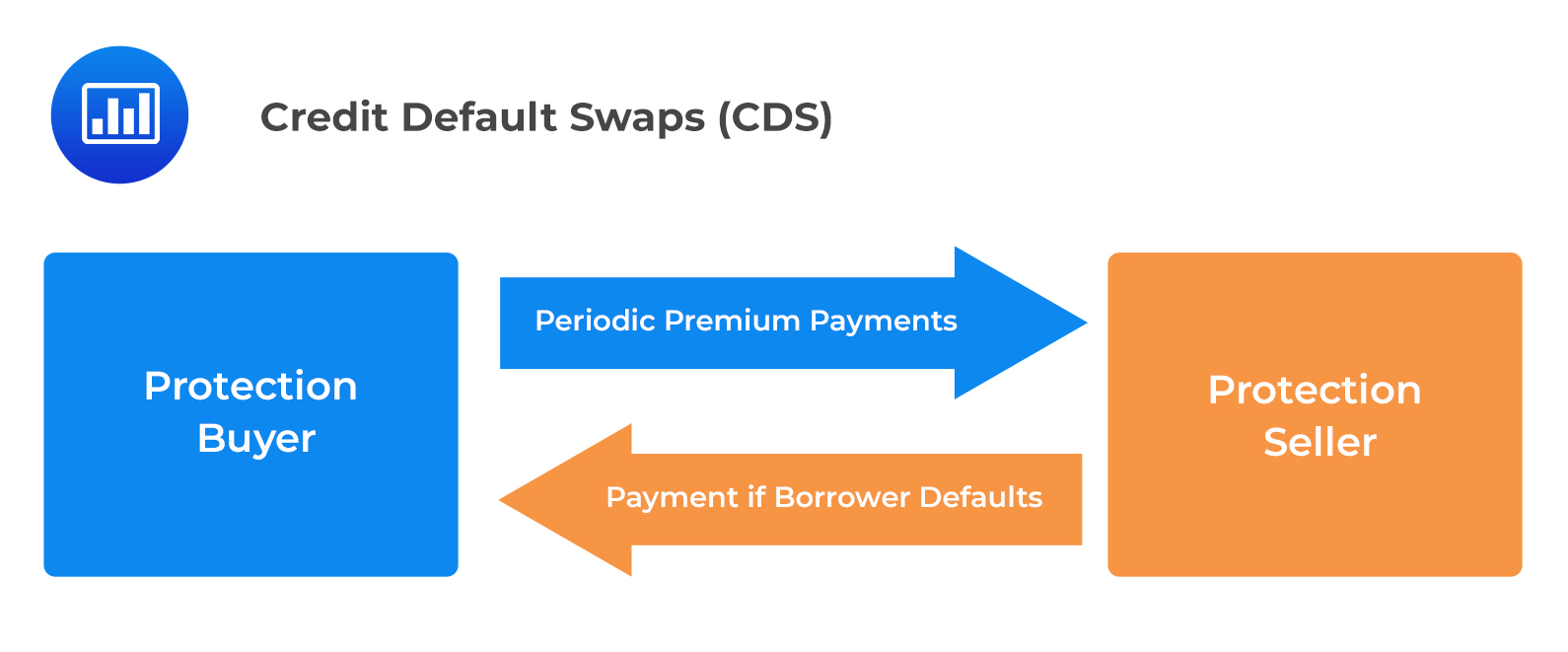

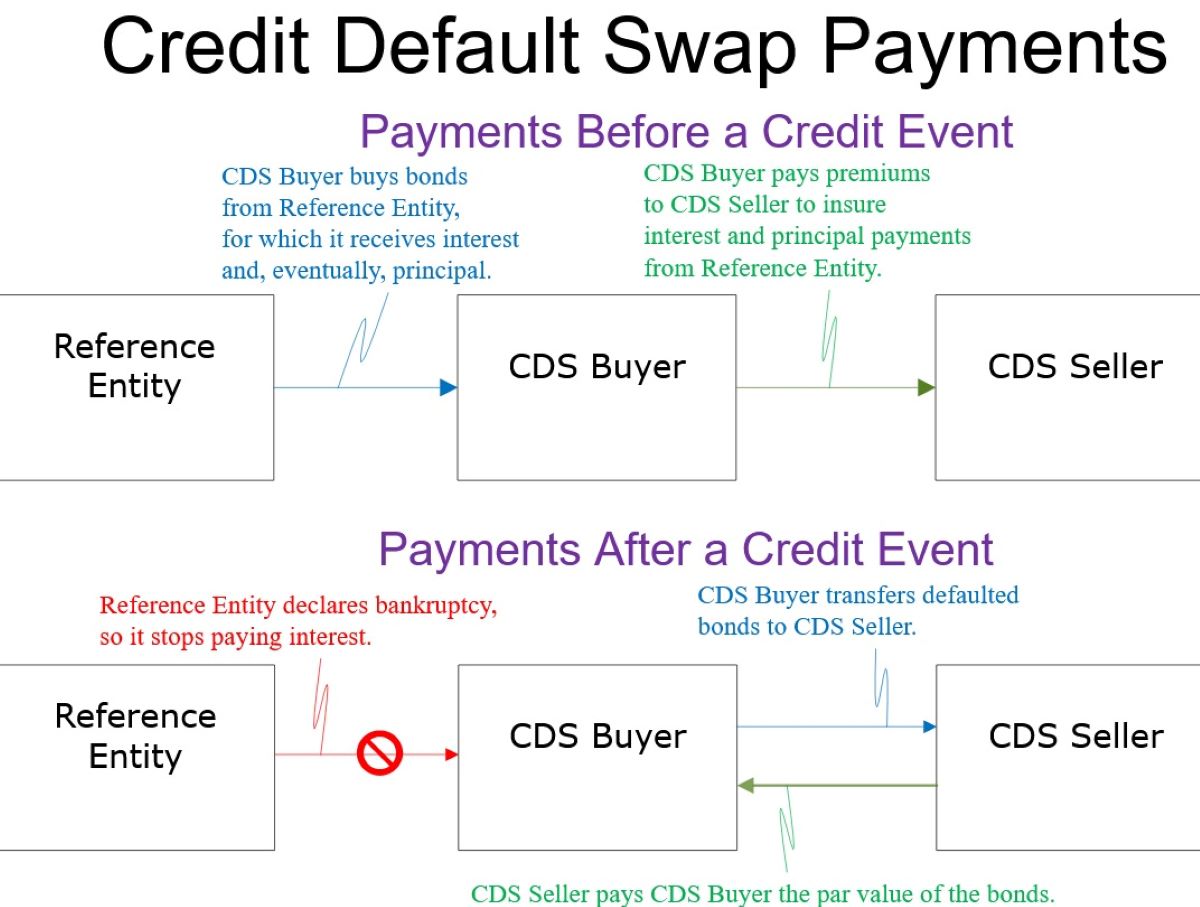

Loan Credit Default Swap, or LCDS, is a financial derivative that serves as a form of insurance against the risk of default on specific loans. It is an agreement between two parties, where one party agrees to compensate the other in the event of a specified loan or loans defaulting. In essence, LCDS functions as a credit default insurance policy.

LCDS is typically used by investors who have concerns about the creditworthiness of a particular loan or a portfolio of loans. By entering into an LCDS, these investors transfer the credit risk associated with those loans to another party, often a financial institution or hedge fund. In return for assuming this risk, the party receiving the credit risk payments will make regular payments to the party transferring the risk.

The terms of an LCDS contract specify the conditions under which a default would be considered to have occurred, as well as the settlement mechanism and the amount of compensation to be paid in case of default. This provides investors with a level of protection and reduces their exposure to potential losses in the event of a default.

How Does Loan Credit Default Swap Work?

To illustrate how LCDS works, let’s consider a hypothetical scenario:

- An investor holds a portfolio of loans and is concerned about the possibility of defaults.

- The investor enters into an LCDS contract with a financial institution.

- In exchange for transferring the credit risk to the financial institution, the investor receives regular payments.

- If a default occurs according to the terms of the LCDS contract, the financial institution compensates the investor for the loss.

By utilizing an LCDS, investors can mitigate their exposure to credit risk, adding an extra layer of protection to their investment portfolios. It allows them to transfer the risk associated with default to parties with the expertise and resources to manage it effectively.

Conclusion

Loan Credit Default Swap (LCDS) is a complex financial instrument used by investors to hedge against the risk of default on specific loans or loan portfolios. By transferring the credit risk to another party in exchange for regular payments, investors can gain an additional level of protection and reduce their exposure to potential losses. LCDS serves as a valuable tool in managing credit risk, allowing investors to navigate the complex world of finance with confidence.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance