Home>Finance>Non-Cash Charge: Definition And Examples In Accounting

Finance

Non-Cash Charge: Definition And Examples In Accounting

Published: December 31, 2023

Learn the definition and examples of non-cash charges in accounting. Understand how these charges affect financial statements and the overall financial health of a company. Gain insights into finance and accounting concepts.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Non-Cash Charge: Definition and Examples in Accounting

Finance can be a complex and ever-changing field, and it’s important to stay informed about the various concepts and terms that are used in accounting. One such term that you might come across is “non-cash charge.” But what exactly does it mean, and how does it impact a company’s financial statements? In this blog post, we will dive deep into the definition of a non-cash charge, discuss some examples, and explore its significance in accounting.

Key Takeaways:

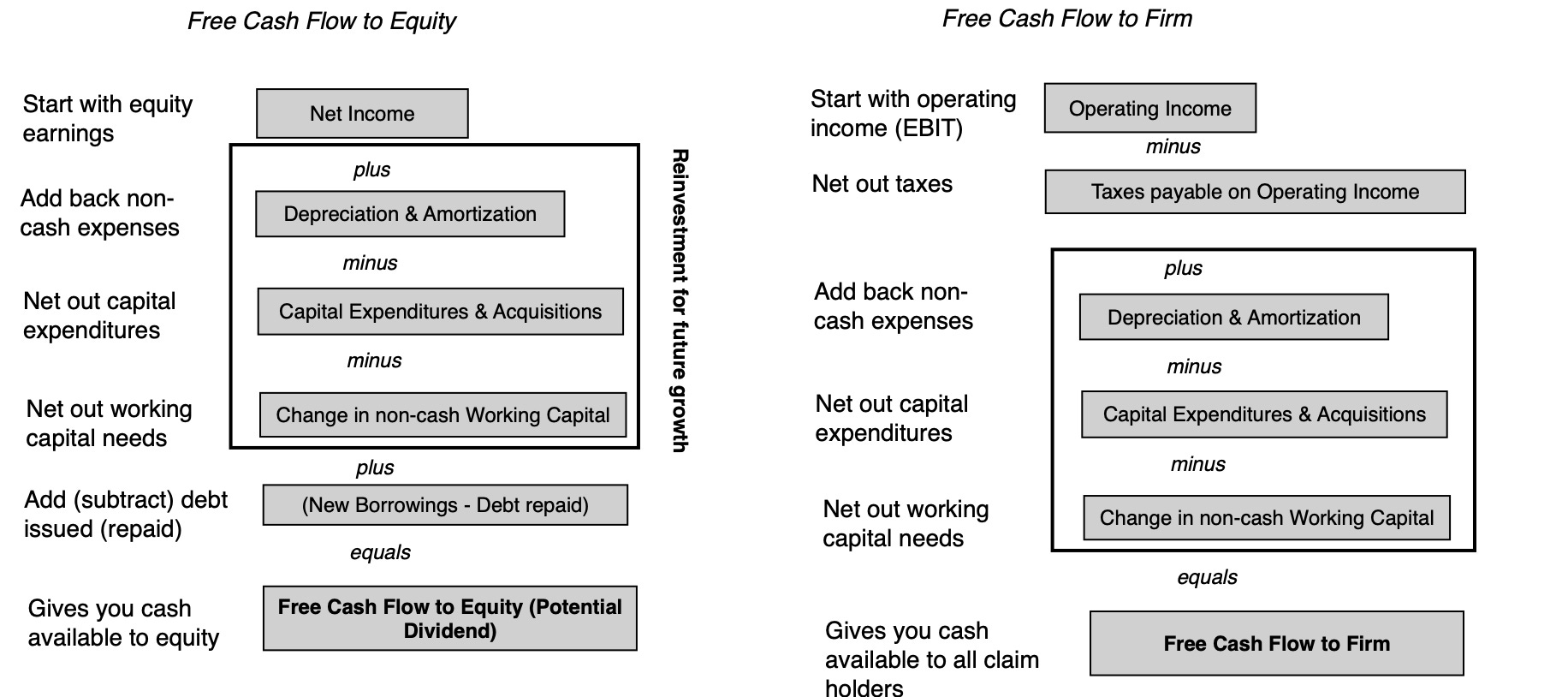

- A non-cash charge is an expense that affects a company’s profit but does not involve an actual outflow of cash.

- Examples of non-cash charges include depreciation, amortization, and impairment write-offs.

What is a Non-Cash Charge?

A non-cash charge, sometimes referred to as a non-cash expense, is an expense that affects a company’s profit or loss statement but does not require the company to pay with actual cash. While this might sound perplexing at first, it is actually a common occurrence in the world of accounting. Non-cash charges are typically associated with certain accounting practices, such as the allocation of costs over time or the recognition of a decrease in an asset’s value.

One of the primary reasons for non-cash charges is the concept of accrual accounting. In accrual accounting, revenues and expenses are recorded when they are earned or incurred, regardless of when the cash is actually received or paid. This allows for a more accurate depiction of a company’s financial performance over time. Non-cash charges play a significant role in accounting for expenses that do not involve an immediate cash outflow.

Examples of Non-Cash Charges

Now that we have a better understanding of what non-cash charges are, let’s take a look at some examples:

- Depreciation: Depreciation is a common non-cash charge that reflects the decrease in value of an asset over time. It is typically applied to tangible assets, such as buildings, vehicles, or machinery. By allocating the cost of the asset over its useful life, companies can account for its gradual wear and tear without affecting their cash flow.

- Amortization: Amortization is similar to depreciation, but it is typically used for intangible assets, such as patents, copyrights, or trademarks. Like depreciation, amortization allows companies to spread out the cost of an asset over its useful life, recognizing the expense over time rather than in one lump sum.

- Impairment Write-offs: An impairment write-off is a non-cash charge that occurs when the value of an asset suddenly decreases. This may be due to factors such as obsolescence, loss of value, or a decline in market conditions. By recognizing the impairment as an expense, companies can adjust their financial statements to reflect the true value of the asset.

The Significance of Non-Cash Charges in Accounting

You might be wondering why non-cash charges are important in accounting if they don’t involve actual cash transactions. Well, non-cash charges provide crucial insights into a company’s financial health and performance. By including these charges in the profit and loss statement, businesses can accurately measure their profitability and generate more informative financial statements.

Furthermore, non-cash charges help investors and analysts evaluate a company’s financial strength and make informed decisions. By stripping out non-cash charges from the financials, investors can better understand the company’s cash-generating ability, which is a critical aspect of assessing its overall value.

Conclusion

Overall, non-cash charges are an essential aspect of accounting. They might not involve an actual outflow of cash, but they play a crucial role in accurately measuring a company’s financial performance and providing valuable insights to investors and analysts. By understanding what non-cash charges are and how they impact financial statements, you can gain a deeper knowledge of the intricate world of finance and accounting.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance