Finance

What Are Share Certificates Credit Union

Modified: February 21, 2024

Learn about share certificates at a credit union and how they can help you achieve your financial goals. Explore the benefits of investing in share certificates and start growing your savings today.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Definition of Share Certificates

- Features of Share Certificates

- Benefits of Share Certificates

- How to Open a Share Certificate at a Credit Union

- Share Certificate Terms and Conditions

- Managing and Accessing Share Certificates

- Fees and Penalties Associated with Share Certificates

- Comparing Share Certificates with Other Investment Options

- Conclusion

Introduction

Welcome to the world of share certificates at credit unions! If you’re looking to grow your savings and diversify your investment portfolio, share certificates are an excellent financial tool to consider. Share certificates, also known as term deposits or time deposits, are a type of savings account offered by credit unions that typically provide higher interest rates compared to regular savings accounts.

Share certificates offer a fixed term, ranging from a few months to several years, during which you agree to keep your money with the credit union. In return, you earn a guaranteed rate of interest that is higher than what you would receive from a regular savings account. This makes share certificates an attractive option for long-term savers who are looking to maximize their returns while maintaining the security of a financial institution.

In this article, we will delve deeper into the world of share certificates at credit unions. We will discuss their definition, features, benefits, and how to open a share certificate at a credit union. Additionally, we will explore the terms and conditions associated with share certificates, the fees and penalties that may apply, and compare them with other investment options. By the end, you’ll have a comprehensive understanding of share certificates and be well-equipped to make informed financial decisions.

So, are you ready to embark on a journey of financial growth? Let’s dive in and explore the world of share certificates at credit unions!

Definition of Share Certificates

A share certificate is a type of savings account offered by credit unions that allows individuals to invest their money for a fixed period of time at a predetermined interest rate. It is often referred to as a term deposit or time deposit. Share certificates are an attractive option for individuals who are looking for a secure and predictable way to grow their savings.

When you open a share certificate, you agree to deposit a specific amount of money with the credit union for a specified term. The minimum deposit required for a share certificate varies depending on the credit union and the terms of the account. The term can range from a few months to several years, giving you the flexibility to choose a timeframe that aligns with your financial goals.

Unlike regular savings accounts where interest rates can fluctuate, share certificates offer a fixed interest rate throughout the term. This means that you can enjoy a guaranteed return on your investment. The interest rate offered on share certificates is typically higher than what you would earn on a regular savings account, making it an attractive option for individuals looking to maximize their savings.

At the end of the term, you have the option to withdraw your funds or roll them over into a new share certificate with updated terms. This gives you the opportunity to reassess your financial goals and choose a new term and interest rate that aligns with your needs.

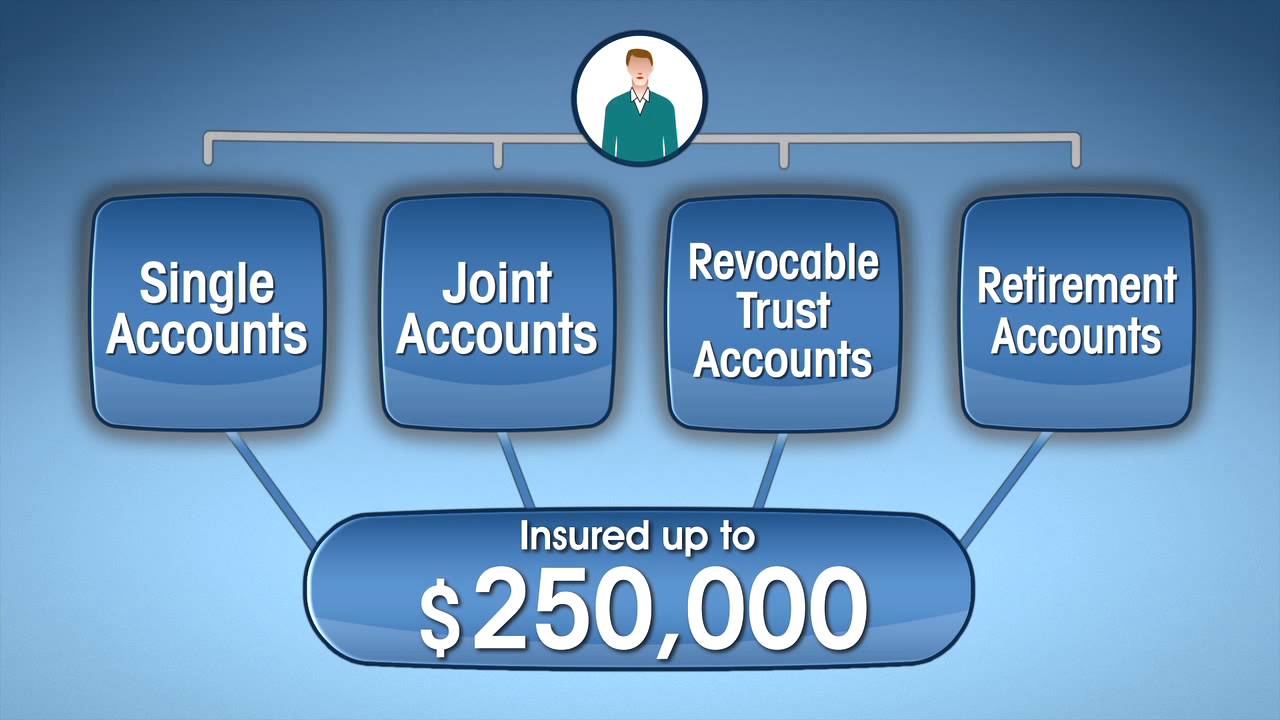

One important thing to note is that share certificates are considered low-risk investments. Since they are issued by credit unions, which are regulated financial institutions, your funds are federally insured up to a certain amount (usually $250,000) by the National Credit Union Administration (NCUA). This provides an additional layer of security and peace of mind.

Now that we have a clear understanding of what share certificates are, let’s delve deeper into the features and benefits they offer.

Features of Share Certificates

Share certificates come with a range of features that make them an appealing investment choice for individuals seeking stability and higher returns on their savings. Let’s explore some of the key features of share certificates:

1. Fixed Term: Share certificates have a predetermined term, ranging from a few months to several years. This means that your money will be invested for a specific period, and you won’t have access to the funds until the term matures. The fixed term provides stability and allows you to plan your finances effectively.

2. Fixed Interest Rate: Unlike regular savings accounts where interest rates can fluctuate, share certificates offer a fixed interest rate for the duration of the term. This ensures that you know exactly how much interest you will be earning on your investment. The fixed rate allows for predictable returns and helps in financial planning.

3. Higher Interest Rates: Share certificates generally offer higher interest rates compared to regular savings accounts. This is because you are committing to keep your money with the credit union for the duration of the term, giving them a longer period to utilize your funds. The higher interest rates help to grow your savings faster.

4. Flexible Term Options: Credit unions offer a variety of term options for share certificates, allowing you to choose a term that fits your financial goals. Whether you’re looking for short-term savings or long-term investment, there are share certificates available to cater to your needs.

5. Minimum Deposit Requirement: Share certificates usually have a minimum deposit requirement. The minimum deposit amount varies among credit unions, but it is generally higher than that of a regular savings account. This requirement ensures that you are committing a certain amount of money for the specified term.

6. Federal Insurance: Share certificates offered by credit unions are federally insured by the National Credit Union Administration (NCUA). This means that even in the unlikely event of a credit union failure, your funds are protected up to a certain amount (usually $250,000). This provides an extra layer of security for your investment.

7. Automatic Renewal: At the end of the term, many credit unions offer the option to automatically renew the share certificate with updated terms and interest rates. This allows you to continue earning interest without the need to go through the hassle of reinvesting your funds manually.

These features of share certificates make them an attractive investment option for individuals who prioritize stability, predictability, and higher returns on their savings. Now let’s move on to exploring the benefits of share certificates.

Benefits of Share Certificates

Investing in share certificates at a credit union comes with a range of benefits that can help you achieve your financial goals. Let’s take a closer look at some of the key advantages of share certificates:

1. Higher Earnings: Share certificates typically offer higher interest rates compared to regular savings accounts. By investing in a share certificate, you can earn more on your savings and watch your money grow faster over time.

2. Guaranteed Returns: Share certificates provide a guaranteed rate of return for the duration of the term. This fixed interest rate allows you to estimate and plan for future earnings, providing peace of mind and financial stability.

3. Low Risk: Share certificates are considered low-risk investments. Credit unions are regulated financial institutions, and share certificates are backed by federal insurance provided by the National Credit Union Administration (NCUA). This means that your funds are protected up to a certain amount, even in the unlikely event of a credit union failure.

4. Financial Discipline: Share certificates promote financial discipline by locking away your funds for a specific term. This can help discourage impulsive spending and encourage long-term savings habits.

5. Diversification: Investing in share certificates allows for diversification of your investment portfolio. By spreading your funds across different types of investments, including share certificates, you can reduce the overall risk and increase the potential for returns.

6. Flexible Terms: Credit unions offer a variety of term options when it comes to share certificates. This flexibility allows you to choose a term that aligns with your financial goals, whether you prefer short-term savings or long-term investment.

7. Automatic Renewal: Many credit unions offer the option to automatically renew your share certificate at the end of the term. This feature simplifies the process of reinvesting your funds and ensures that your savings continue to grow without any interruption.

8. Support for Local Communities: By investing in share certificates at a credit union, you are supporting a local financial institution that often gives back to the community through initiatives such as charitable donations, scholarships, and community development projects.

Overall, share certificates offer a reliable and secure way to grow your savings and earn competitive returns. They provide peace of mind, financial discipline, and the potential for higher earnings. Now that you understand the benefits, let’s explore how to open a share certificate at a credit union.

How to Open a Share Certificate at a Credit Union

If you’re interested in opening a share certificate at a credit union, the process is typically straightforward. Here are the steps to follow:

1. Research Credit Unions: Start by researching credit unions in your area that offer share certificates. Look for credit unions with a good reputation, competitive interest rates, and terms that align with your financial goals.

2. Compare Terms and Rates: Compare the terms and interest rates offered by different credit unions. Consider factors such as the minimum deposit requirement, term length, and whether they offer flexible terms or automatic renewal options.

3. Visit the Credit Union: Visit the credit union of your choice in person or explore their website to gather more information. Make sure to review their eligibility requirements for membership and any additional documentation that may be needed.

4. Membership: If you are not already a member of the credit union, you will need to become one. Each credit union has its own membership criteria, which may include living or working in a specific area or being affiliated with certain organizations. Ensure that you meet their membership requirements before proceeding.

5. Application: Complete the share certificate application form provided by the credit union. This form will require personal information such as your name, address, social security number, and the amount you wish to invest in the share certificate.

6. Submit Funds: Provide the credit union with the deposit amount required to open the share certificate. This can typically be done through a transfer from your existing account or by depositing a check.

7. Review Terms and Conditions: Carefully review the terms and conditions of the share certificate before signing any agreements. Pay attention to details such as the interest rate, term length, any early withdrawal penalties, and automatic renewal options.

8. Confirmation: Once your application and funds have been processed, you will receive confirmation of your new share certificate account. Keep this confirmation for your records.

9. Track Your Investment: Monitor the progress of your share certificate throughout the term. Many credit unions provide online access to your account, allowing you to track your investment and view the interest earned.

Opening a share certificate at a credit union is a simple process that can be completed within a few steps. By choosing a credit union that aligns with your financial goals and following these steps, you’ll be on your way to growing your savings in no time.

Share Certificate Terms and Conditions

When opening a share certificate at a credit union, it’s important to understand the terms and conditions associated with the account. Here are some key terms and conditions you should be aware of:

1. Term Length: The share certificate term refers to the duration for which you agree to keep your funds deposited. It can range from a few months to several years. The longer the term, the higher the interest rate is typically offered.

2. Interest Rate: The interest rate is the percentage at which the credit union will pay you interest on your share certificate. It is typically fixed for the entire term and is higher than what you would earn on a regular savings account.

3. Minimum Deposit: Share certificates have a minimum deposit requirement, which is the minimum amount of money you need to deposit to open the account. The minimum deposit varies among credit unions and may also depend on the term length chosen.

4. Early Withdrawal Penalties: Share certificates are intended to be held until the term maturity. If you withdraw funds before the maturity date, you may incur early withdrawal penalties. These penalties can include a reduction in the interest earned or a forfeit of a portion of the principal invested.

5. Automatic Renewal: Many credit unions offer the option for automatic renewal of the share certificate at the end of the term. This means that if you do not take any action, your funds will automatically be reinvested into a new share certificate with updated terms and interest rates.

6. Grace Period: Some credit unions may provide a grace period at the end of the term during which you can make changes to your share certificate, such as withdrawing funds or changing the term length, without incurring penalties.

7. Joint Accounts: Credit unions may allow you to open a share certificate as a joint account with another individual. This allows both account holders to contribute funds and share in the benefits and responsibilities of the account.

8. Federal Insurance: Share certificates offered by credit unions are federally insured by the National Credit Union Administration (NCUA). This insurance protects your funds up to a certain amount (usually $250,000) in the event of a credit union failure.

It’s important to carefully read and understand the terms and conditions of a share certificate before opening an account. If you have any questions or concerns, don’t hesitate to reach out to the credit union for clarification. By being aware of the terms and conditions, you can make informed decisions about managing your share certificate.

Managing and Accessing Share Certificates

Managing and accessing your share certificate at a credit union is a straightforward process. Here are some important points to keep in mind:

1. Account Monitoring: Stay up to date with the progress of your share certificate by regularly checking your account statements or utilizing online banking services offered by the credit union. This will allow you to track your investment and monitor the interest earned.

2. Accessibility: Share certificates are designed to be held until the maturity date, meaning that your funds are not readily accessible during the term. However, in case of emergency or financial need, some credit unions may offer options for partial withdrawals or early access, although this may come with penalties.

3. Automatic Renewal: If you opt for automatic renewal, the credit union will reinvest your funds into a new share certificate with updated terms and interest rates at the end of the term. This ensures that your savings continue to grow without any interruption. If you do not want to renew, make sure to communicate your decision to the credit union in advance.

4. Changes to Terms: If you wish to make changes to your share certificate, such as extending the term or adjusting the deposit amount, reach out to the credit union to discuss your options. Keep in mind that any modifications may be subject to the credit union’s policies and may require completing additional paperwork.

5. Communication: Maintain open communication with the credit union regarding any questions, concerns, or changes to your share certificate. They will be able to provide assistance and guidance throughout the duration of your account.

6. Account Statements: Review your account statements promptly to ensure accuracy and to track the interest earned on your share certificate. If you notice any discrepancies or have questions about the statements, contact the credit union for clarification.

7. Maturity Date: Make a note of the maturity date of your share certificate. As the maturity date approaches, consider your financial goals, the current interest rate environment, and whether you want to reinvest the funds into a new share certificate or explore other investment options.

Remember, managing and accessing your share certificate involves staying informed, communicating with the credit union, and making decisions based on your financial needs. By taking an active role in managing your account, you can make the most of your share certificate to achieve your savings goals.

Fees and Penalties Associated with Share Certificates

When considering share certificates at a credit union, it is important to be aware of any fees and penalties that may be associated with these accounts. While the specific fees and penalties can vary between credit unions, here are some common ones to keep in mind:

1. Early Withdrawal Penalties: Share certificates are designed to be held until the maturity date. If you need to withdraw funds before the maturity date, you may incur early withdrawal penalties. These penalties can vary depending on the credit union and the term length of the share certificate. It is essential to understand the penalty structure before opening the account.

2. Minimum Balance Fee: Some credit unions may impose a minimum balance requirement on share certificates. If your account balance falls below the minimum threshold, you may be subject to a fee. Make sure to review the credit union’s requirements and determine if there is a minimum balance fee associated with the share certificate.

3. Renewal Fees: If you choose to renew your share certificate at the end of the term, there may be a renewal fee charged by the credit union. This fee covers the administrative costs of processing the renewal and updating the terms and conditions of the account.

4. Account Closure Fee: In the event that you decide to close your share certificate before the maturity date, the credit union may charge an account closure fee. This fee compensates the credit union for any administrative costs associated with closing the account.

5. Excess Withdrawal Fee: Share certificates typically have restrictions on the number of withdrawals you can make. If you exceed the allowed number of withdrawals, the credit union may charge an excess withdrawal fee for each additional withdrawal beyond the limit.

6. Non-Membership Fee: If you are not a member of the credit union when you open a share certificate, you may be required to pay a non-membership fee. This fee covers the administrative costs of processing your membership application and grants you access to the credit union’s services.

7. Additional Services: Credit unions may offer additional services related to share certificates, such as account statement requests or account-related inquiries. There may be fees associated with these services, so it is important to inquire about any additional fees before utilizing them.

It is crucial to carefully review the terms and conditions provided by the credit union to fully understand all fees and penalties associated with their share certificates. By being aware of these potential costs, you can make informed decisions and effectively manage your share certificate account.

Comparing Share Certificates with Other Investment Options

When it comes to investing your money, it’s essential to consider various options and assess their suitability to meet your financial goals. Let’s compare share certificates with other investment options to help you make an informed decision:

1. Savings Accounts: Share certificates typically offer higher interest rates compared to regular savings accounts. While savings accounts provide convenient access to funds, they may not offer the same level of returns as share certificates.

2. Certificates of Deposit (CDs): Share certificates and certificates of deposit have many similarities. Both offer fixed interest rates and terms, with the main difference being that share certificates are offered by credit unions, while CDs are offered by banks. The interest rates may vary, so it’s important to compare rates and terms to find the most favorable option.

3. Stocks and Bonds: Share certificates are considered low-risk investments, especially when compared to the volatility of stocks and bonds. While stocks and bonds may offer the potential for higher returns, they also come with higher levels of risk. Share certificates provide a secure and predictable way to grow your savings.

4. Mutual Funds: Mutual funds pool money from multiple investors to invest in a diversified portfolio of securities. While mutual funds can potentially offer higher returns, they also carry higher levels of risk. Share certificates, on the other hand, have a fixed interest rate and term, providing stability and predictability.

5. Real Estate: Investing in real estate can be profitable in the long term, but it requires a significant upfront investment and involves ongoing maintenance and management. Share certificates offer a more accessible and hassle-free investment option, especially for individuals looking for passive income and a hands-off approach.

6. Government Bonds: Government bonds are considered low-risk investments as they are backed by the government. While they can provide stable returns, the interest rates on government bonds are typically lower compared to share certificates. Share certificates may offer higher yields for individuals seeking higher returns.

7. Retirement Accounts: Retirement accounts, such as IRAs or 401(k)s, offer tax advantages and a range of investment options. While share certificates can be included within retirement accounts, it’s important to evaluate the overall asset allocation and consider diversifying the portfolio with other investments.

When comparing investment options, it’s crucial to assess your risk tolerance, financial goals, and time horizon. Share certificates are a suitable choice for individuals seeking stability, predictable returns, and a low-risk investment. However, it’s important to consider diversifying your portfolio based on your personal circumstances and consulting with a financial advisor if needed.

Conclusion

Share certificates at credit unions provide individuals with a secure and reliable way to grow their savings and earn competitive returns. With their fixed term, guaranteed interest rates, and low-risk nature, share certificates offer stability and financial discipline that aligns with long-term financial goals.

Throughout this article, we have explored the definition of share certificates, their features, benefits, and the process of opening an account at a credit union. We have also discussed the terms and conditions, as well as the fees and penalties associated with share certificates. Additionally, we compared share certificates with other investment options to help you make informed decisions about your financial future.

It is important to remember that every individual’s financial situation and goals are unique, and what works well for one person may not be the best option for another. It is recommended to assess your own preferences, risk tolerance, and financial objectives when considering share certificates or any other investment option.

If you value stability, lower risk, and predictable returns, share certificates can be an attractive investment choice. However, it’s essential to conduct thorough research, compare interest rates and terms offered by different credit unions, and consider your long-term savings goals.

Remember to review the terms and conditions, including any early withdrawal penalties, minimum balance requirements, and automatic renewal options, before opening a share certificate account. Stay engaged with your credit union and regularly review your account statements to monitor your investment progress.

Ultimately, share certificates at credit unions offer a compelling investment opportunity for individuals seeking stable and secure growth of their savings. By carefully considering your financial goals and options, you can make informed decisions to maximize your returns and achieve long-term financial success.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance