Home>Finance>What Do Disability Insurance And Life Insurance Have In Common?

Finance

What Do Disability Insurance And Life Insurance Have In Common?

Modified: December 30, 2023

Discover the similarities between disability insurance and life insurance in the world of finance. Protect your future with the right coverage for your needs.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Definition of Disability Insurance

- Definition of Life Insurance

- Importance of Disability Insurance

- Importance of Life Insurance

- Similarities between Disability Insurance and Life Insurance

- Differences between Disability Insurance and Life Insurance

- Factors to Consider when Choosing Disability Insurance

- Factors to Consider when Choosing Life Insurance

- Conclusion

Introduction

When it comes to financial security and protection, two types of insurance often come to mind: disability insurance and life insurance. While both serve the purpose of providing coverage in the event of unplanned circumstances, they differ in their approach and focus. Understanding the similarities and differences between disability insurance and life insurance can help individuals make informed decisions about their financial well-being.

Disability insurance is designed to protect individuals against the loss of income due to a disabling injury or illness. It provides a steady source of income during the period that a person is unable to work. On the other hand, life insurance is intended to provide financial support to dependents in the event of the policyholder’s death.

In this article, we will explore the definitions of disability insurance and life insurance, discuss their importance, highlight the similarities and differences between the two, and provide key factors to consider when choosing each type of insurance. By understanding these aspects, individuals will be better equipped to make informed decisions about their financial protection strategies.

Definition of Disability Insurance

Disability insurance, also known as income protection insurance, is a type of insurance coverage that provides financial support to individuals in the event that they become disabled and are unable to work. It is designed to replace a portion of the policyholder’s income, typically a percentage of their pre-disability earnings, during the period of disability.

Disability insurance policies can vary in their terms and coverage options. There are two main types of disability insurance: short-term disability insurance and long-term disability insurance. Short-term disability insurance typically covers a temporary disability, providing benefits for a specified period, often ranging from a few weeks to a few months. Long-term disability insurance, on the other hand, covers disabilities that extend beyond the short-term period, typically providing benefits until the policyholder is able to return to work or until they reach a certain age, such as retirement.

To qualify for disability insurance benefits, individuals must meet the specific criteria outlined in their policy. This usually includes providing medical documentation to prove the disability and demonstrating that the disability prevents them from performing their occupational duties. Different policies may have different definitions of disability, ranging from the inability to perform any job to the inability to perform the policyholder’s specific occupation.

Disability insurance can be obtained through various sources. Some individuals may have access to employer-sponsored group disability insurance, which is typically more affordable but may have limitations on coverage amounts and terms. Others may choose to purchase individual disability insurance policies to supplement or replace employer-provided coverage. Individual disability insurance policies offer greater flexibility and customization options, such as choosing the benefit amount, waiting period, and duration of coverage.

Overall, disability insurance provides a safety net for individuals and their families in the event of a disability that prevents them from earning an income. It offers financial security and peace of mind by ensuring that individuals can maintain their standard of living and meet their financial obligations even when faced with a disability that hinders their ability to work.

Definition of Life Insurance

Life insurance is a financial product designed to provide a sum of money, known as a death benefit, to designated beneficiaries upon the death of the insured individual. It offers a way for individuals to protect their loved ones financially by providing support and covering various expenses in the event of their passing.

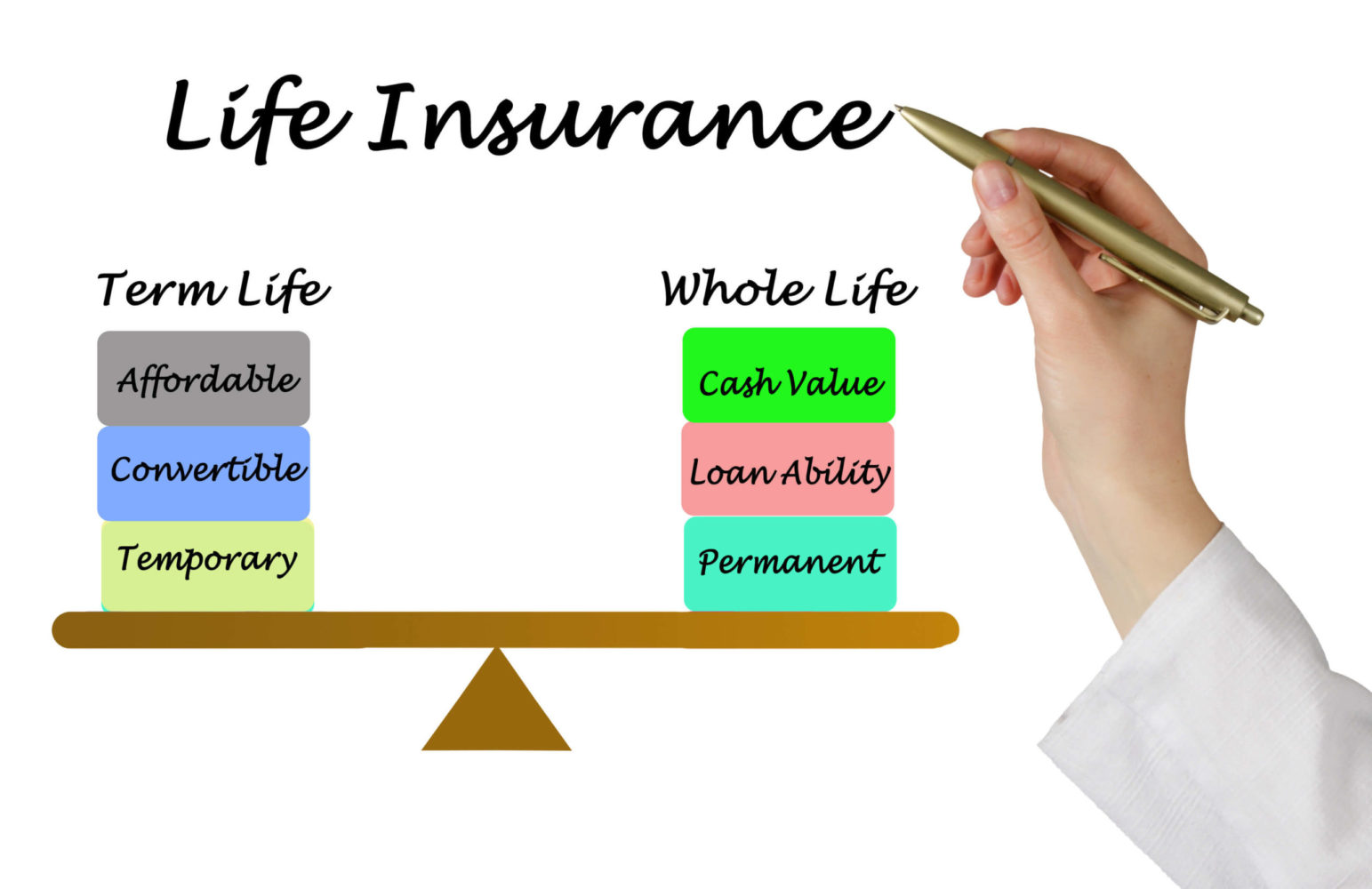

Life insurance policies come in different forms, including term life insurance and permanent life insurance. Term life insurance provides coverage for a specified term, such as 10, 20, or 30 years. If the insured individual passes away during the term of the policy, the beneficiaries receive the death benefit. If the policy expires without a claim, no benefit is paid out. Permanent life insurance, on the other hand, provides coverage for the entire lifetime of the insured individual and includes a cash value component that grows over time.

Life insurance can serve multiple purposes. It can be used to replace lost income and provide financial support for dependents, ensuring that they can maintain their standard of living in the absence of the insured individual. It can also be utilized to cover funeral expenses, pay off debts, provide for educational expenses, or leave a legacy to future generations.

When applying for life insurance, individuals typically undergo a process that involves completing an application, answering health-related questions, and potentially undergoing a medical examination. The premium for life insurance is determined based on several factors, including the applicant’s age, health condition, occupation, lifestyle, and the desired coverage amount.

Life insurance can be purchased from various sources, including insurance companies, financial institutions, and independent agents. It is important for individuals to carefully assess their needs and consider factors such as their financial obligations, dependents, and long-term goals when choosing the right life insurance policy. Regularly reviewing and updating life insurance coverage as circumstances change is also crucial to ensure adequate protection.

In summary, life insurance provides a financial safety net for loved ones in the event of the insured individual’s death. It serves as a means of providing support, covering expenses, and easing the financial burden that may arise during a difficult time. By securing life insurance, individuals can have peace of mind knowing they have taken steps to protect their family’s future financial well-being.

Importance of Disability Insurance

Disability insurance plays a crucial role in ensuring financial stability and security in the face of unexpected circumstances. Here are some key reasons why disability insurance is important:

- Protecting your income: Your ability to earn a living is often your most valuable asset. Disability insurance provides a safety net by replacing a portion of your income if you become disabled and are unable to work. This ensures that you can continue to meet your financial obligations, such as mortgage or rent payments, utility bills, and other living expenses.

- Covering medical expenses: Disabilities often come with medical costs, including doctor’s visits, surgeries, medications, and therapy. Disability insurance can help offset these expenses, allowing you to focus on your recovery rather than worrying about the financial impact of your disability.

- Maintaining your lifestyle: A disability can lead to a significant decrease in your standard of living. With disability insurance, you can help maintain your current lifestyle by replacing a portion of your lost income. This ensures that you can continue to afford the things that are important to you and your family.

- Supporting your dependents: If you have dependents who rely on your income, disability insurance becomes even more important. It provides a much-needed financial safety net for your loved ones, ensuring that they are taken care of if you are unable to provide for them due to a disability.

By having disability insurance in place, you can focus on your recovery and rehabilitation without the added stress of financial uncertainty. It provides peace of mind and protects you and your loved ones from the potential financial consequences of a disability. Keep in mind that disabilities can happen to anyone, regardless of age or occupation, so having disability insurance is a prudent step to take.

When considering disability insurance, it’s important to carefully review the policy terms, coverage limits, waiting periods, and definitions of disability. Factors such as the length of coverage, elimination periods, and the ability to customize the policy to suit your specific needs should also be taken into account. Working with a knowledgeable insurance professional can help you navigate through the options and select the best disability insurance policy for your circumstances.

Importance of Life Insurance

Life insurance is an essential component of a comprehensive financial plan. It provides valuable protection and peace of mind for you and your loved ones. Here are some reasons why life insurance is so important:

- Financial security for dependents: One of the primary purposes of life insurance is to provide financial support to your dependents in the event of your death. The death benefit can help cover daily living expenses, mortgage payments, debts, and even educational expenses for your children. It ensures that your loved ones are not burdened with financial hardship during an already challenging time.

- Estate planning: Life insurance can play a vital role in estate planning. It can help provide liquidity to cover estate taxes, ensuring that your beneficiaries receive the full value of your assets. It can also facilitate the equitable distribution of assets among multiple heirs and help preserve family wealth for future generations.

- Debt repayment: If you have outstanding debts such as a mortgage, car loan, or student loans, life insurance can help ensure that your loved ones are not left with the burden of repaying those debts. The death benefit can be used to settle any outstanding financial obligations, providing financial security and peace of mind to your family.

- Business continuity: For business owners, life insurance can be instrumental in ensuring the continuity of the business in the event of the owner’s death. It can provide funds to cover business expenses, repay loans, and even facilitate the transfer of ownership to a successor. This helps protect the business and the employees who rely on it for their livelihoods.

- Legacy and charitable giving: Life insurance can also be used as a tool for leaving a legacy or making charitable donations. By naming beneficiaries or charitable organizations as recipients of the death benefit, you can support causes that are important to you, leaving a lasting impact even after your lifetime.

Life insurance offers a way to provide financial security and support for your loved ones when they need it most. It helps ensure that your family’s well-being and future goals are protected, even if you are no longer there to provide for them. The type and amount of life insurance coverage you need will depend on your specific circumstances, financial goals, and the needs of your dependents. Consulting with a knowledgeable insurance professional can help you navigate the options and determine the most appropriate life insurance policy for you.

Similarities between Disability Insurance and Life Insurance

While disability insurance and life insurance serve different purposes, there are some notable similarities between the two. Understanding these similarities can help individuals recognize the common elements and considerations in both types of insurance. Here are some key similarities between disability insurance and life insurance:

- Protection against financial loss: Both disability insurance and life insurance aim to provide financial protection in the face of unexpected events. Disability insurance protects individuals and their families by replacing their income if they become disabled and cannot work. Life insurance provides a death benefit to beneficiaries upon the insured individual’s death, offering financial support and protection for their loved ones.

- Insurance premiums: Both disability insurance and life insurance require individuals to pay regular premiums in exchange for coverage. The cost of premiums typically depends on various factors such as age, health condition, occupation, coverage amount, and policy terms. In both cases, it’s crucial to budget for insurance premiums to maintain coverage and ensure the policies remain in force.

- Policy customization: Both disability insurance and life insurance policies often allow individuals to customize their coverage to suit their specific needs and requirements. Factors such as the coverage amount, waiting periods, policy duration, optional riders, and additional benefits can usually be tailored to align with individual circumstances and preferences.

- Policy limitations and exclusions: Both disability insurance and life insurance policies have limitations and exclusions that individuals should be aware of. These may include pre-existing conditions, specified waiting periods before benefits are payable, and exclusions for certain types of disabilities or deaths. It’s important to carefully review the policy terms to understand the coverage scope and any potential limitations or exclusions.

- Financial impact assessment: In both disability insurance and life insurance, it’s essential to assess the potential financial impact and needs of individuals and their dependents. Evaluating one’s income, financial obligations, lifestyle, and future goals can help determine the appropriate coverage amounts and types of policies needed to adequately protect against financial loss.

Understanding these similarities can help individuals develop a holistic approach to their insurance needs. By recognizing the commonalities between disability insurance and life insurance, individuals can make informed decisions, ensure proper coverage, and protect themselves and their loved ones from significant financial setbacks in challenging times.

Differences between Disability Insurance and Life Insurance

Although disability insurance and life insurance share some similarities in terms of providing financial protection, there are significant differences between the two. These differences arise from the specific risks they address and the circumstances under which they provide coverage. Here are the key differences between disability insurance and life insurance:

- Triggering event: The primary difference between disability insurance and life insurance lies in the triggering event for coverage. Disability insurance provides benefits when an individual becomes disabled and is unable to work due to injury or illness. Life insurance, on the other hand, provides a death benefit to beneficiaries upon the insured individual’s death.

- Income replacement vs. lump sum payment: Disability insurance is designed to replace a portion of the insured individual’s income if they become disabled. It provides regular payments to help cover living expenses and financial obligations during the disability period. Life insurance, on the other hand, typically pays out a lump sum death benefit to beneficiaries after the insured’s death.

- Policy terms and duration: Disability insurance policies can have varying terms and durations. Short-term disability insurance generally covers temporary disabilities for a few weeks to a few months, while long-term disability insurance provides coverage for extended periods, often until retirement or the individual’s recovery. Life insurance policies can have specific term lengths, such as 10, 20, or 30 years, or can be permanent and provide coverage for the entire lifespan of the insured.

- Underwriting process: The underwriting process for disability insurance and life insurance differs. Disability insurance underwriting focuses more on the individual’s health condition, occupation, and ability to perform their specific job duties. Life insurance underwriting also considers health factors but may place more emphasis on age, lifestyle habits, and family medical history. The underwriting process for life insurance tends to be more extensive and may require a medical examination.

- Premium costs: The cost of disability insurance premiums is generally higher compared to life insurance premiums. This is because disability insurance policies are more likely to pay out benefits due to the higher incidence of disabilities compared to death. Factors such as age, health condition, occupation, and coverage amount also influence the cost of premiums for both types of insurance.

Understanding these differences is crucial when considering disability insurance and life insurance. It helps individuals make informed decisions based on their unique circumstances, needs, and financial goals. By evaluating the risks they are most exposed to and the protection required, individuals can select the most suitable insurance policies to safeguard themselves and their loved ones.

Factors to Consider when Choosing Disability Insurance

Choosing the right disability insurance policy requires careful consideration of various factors to ensure that it aligns with your specific needs and provides adequate coverage. Here are key factors to consider when selecting disability insurance:

- Income protection: Evaluate the percentage of your income that the disability insurance policy will replace if you become disabled. Consider whether the coverage amount will be sufficient to meet your financial obligations and maintain your standard of living during a disability.

- Definition of disability: Understand how the policy defines disability. Some policies may have stricter definitions that require you to be unable to work in any occupation, while others may focus on your inability to perform your specific job duties. Choose a policy that aligns with your job requirements and provides adequate coverage for your occupation.

- Elimination period: The elimination period is the time that needs to pass after becoming disabled before you start receiving benefits. Consider your financial resources and how long you can sustain without income during this waiting period. Shorter elimination periods may result in higher premiums.

- Benefit period: The benefit period is the length of time that benefits will be paid if you remain disabled. Consider how long you would need coverage in the event of a prolonged disability and choose a benefit period that aligns with your requirements.

- Additional riders: Look into optional riders that can enhance your coverage, such as cost of living adjustments (COLA) that increase benefit amounts to account for inflation, residual disability coverage that provides partial benefits if you can work but at a reduced capacity, and future purchase options that allow you to increase coverage as your income grows.

- Occupation-specific coverage: Some disability insurance policies offer coverage tailored to specific occupations. If you have a specialized or high-risk occupation, consider policies that provide coverage for the unique risks associated with your profession.

- Policy exclusions and limitations: Carefully review any exclusions or limitations on coverage, such as pre-existing conditions or exclusions for certain disabilities. Understand the situations in which benefits may not be payable, and make sure they align with your needs and expectations.

- Premiums and affordability: Compare the premiums of different disability insurance policies and consider how they fit into your budget. Keep in mind that lower-cost policies may offer less comprehensive coverage, so strike a balance between affordability and adequate protection.

Additionally, it’s essential to work with a knowledgeable insurance professional who can guide you through the process, explain policy details, and help you navigate the options available. They can assist in assessing your needs, comparing policies, and selecting the disability insurance coverage that best suits your individual circumstances.

Factors to Consider when Choosing Life Insurance

Choosing the right life insurance policy requires careful consideration of several factors to ensure that it aligns with your financial goals and provides adequate coverage. Here are some key factors to consider when selecting life insurance:

- Coverage amount: Determine the amount of coverage needed to meet your financial obligations and provide financial support to your dependents. Consider factors such as outstanding debts, mortgage payments, future education expenses, and the income replacement needs of your loved ones.

- Policy type: Decide between term life insurance and permanent life insurance. Term life insurance offers coverage for a specified term (e.g., 10, 20, or 30 years) and is typically more affordable. Permanent life insurance, such as whole life or universal life, provides coverage for your entire life and includes a cash value component.

- Policy duration: If you choose term life insurance, consider the duration of coverage that aligns with your specific needs. Evaluate your financial goals, anticipated financial obligations, and the period during which your dependents will require significant financial support.

- Underwriting process: Be prepared for the underwriting process, which may include answering health-related questions and potentially undergoing a medical examination. Understand that your health and lifestyle factors may impact the premiums and coverage options available to you.

- Premium costs: Evaluate the affordability of the premiums. Compare quotes from different insurers and consider how the premiums fit into your budget. Be mindful that premiums can vary based on factors such as age, health condition, coverage amount, and policy type.

- Beneficiary designation: Choose your beneficiaries carefully and update your beneficiary designation as needed. Consider who will rely on the life insurance benefit and ensure that the policy clearly outlines how the death benefit will be distributed.

- Policy riders: Understand the optional riders available with the life insurance policy and assess whether they complement your needs. Riders may include features such as accelerated death benefit, which allows you to access a portion of the death benefit if diagnosed with a terminal illness.

- Financial stability of the insurer: Research the financial stability and reputation of the insurance company you are considering. Look into their ratings from independent rating agencies to ensure that they will be able to fulfill their obligations in the event of a claim.

It is recommended to consult with a knowledgeable insurance professional who can help assess your specific needs, explain policy details, and guide you in making an informed decision. They can provide personalized recommendations based on your financial situation, goals, and the needs of your beneficiaries.

Conclusion

In summary, both disability insurance and life insurance are crucial components of a comprehensive financial protection strategy. Disability insurance provides income replacement in the event of a disability, ensuring that you can maintain your financial obligations and standard of living. Life insurance, on the other hand, offers financial support to your loved ones in the event of your death, helping them cover expenses and maintain their quality of life.

While disability insurance focuses on protecting your income during a disability, life insurance provides a lump sum payment to beneficiaries after your passing. Both types of insurance require careful consideration of factors such as coverage amount, policy terms, premiums, and beneficiaries.

When choosing disability insurance, factors such as income protection, elimination periods, benefit periods, and policy customization options should be taken into account. For life insurance, considerations include the coverage amount, policy type (term or permanent), premiums, underwriting process, and beneficiary designation.

It is important to work with an experienced insurance professional who can guide you through the process, explain the details of each policy, and help you make a well-informed decision based on your unique circumstances and financial goals.

By carefully selecting and maintaining disability insurance and life insurance policies, you can ensure financial security and peace of mind for yourself and your loved ones. These types of insurance provide a valuable safety net, protecting you and your family from the potentially devastating financial consequences of disability or unexpected death.

Remember to regularly review and update your insurance coverage as your circumstances change. This will help maintain adequate protection and ensure that your insurance policies continue to align with your needs and goals.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance