Finance

What Do I Need To Cash Savings Bonds

Published: January 16, 2024

Learn what you need to know about cashing savings bonds and managing your finances. Get expert advice on handling your savings bonds and maximizing your returns.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

When it comes to saving for the future, many individuals turn to savings bonds as a reliable investment option. Savings bonds are a type of debt security issued by the U.S. Department of the Treasury. They provide a safe and relatively low-risk way to grow your money over time.

However, there may come a time when you need to cash in your savings bonds. Whether it’s to cover unexpected expenses, fund a major purchase, or simply access your savings, understanding the process of cashing savings bonds is essential.

In this article, we will delve into the requirements, steps, and tax implications involved in cashing savings bonds. We will also explore alternative options to consider if you find yourself in need of funds but don’t want to cash in your savings bonds just yet.

Before we dive into the details, let’s first gain a better understanding of what savings bonds are and the different types available.

Understanding Savings Bonds

Savings bonds are a type of government-issued debt security that individuals can purchase as a long-term investment. They are considered a safe and secure way to save money because they are backed by the U.S. Department of the Treasury. Savings bonds offer a fixed interest rate that is typically higher than traditional savings accounts.

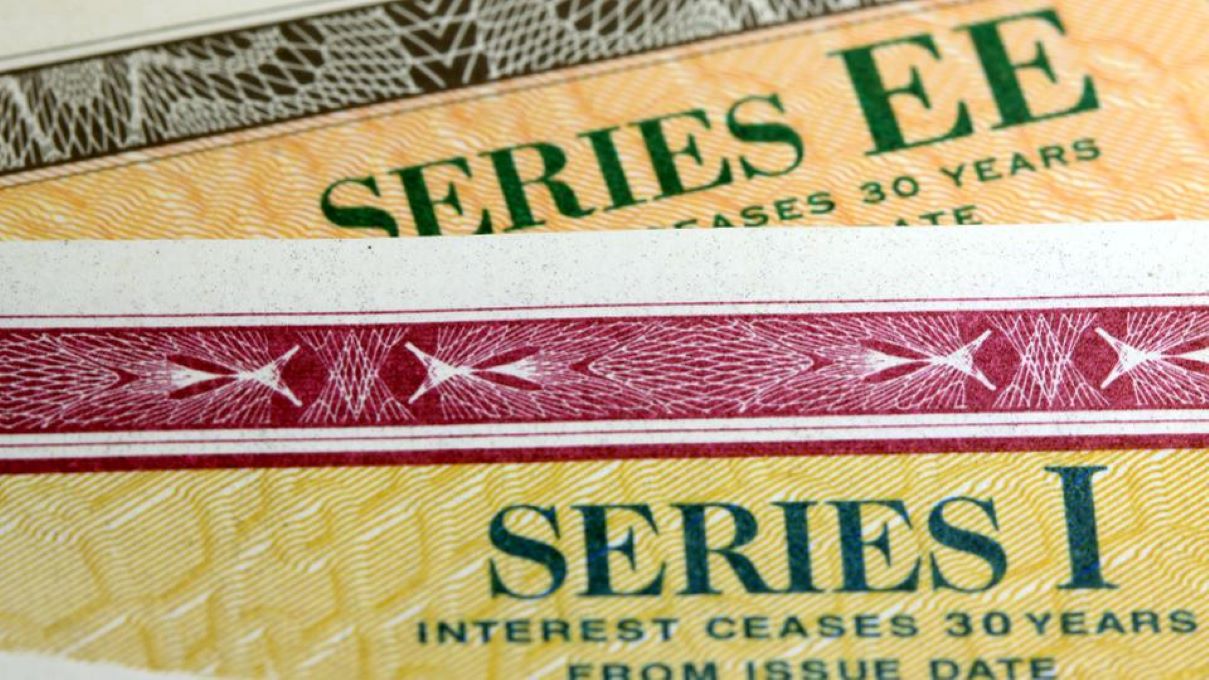

There are two main types of savings bonds: Series EE bonds and Series I bonds.

Series EE Bonds: Series EE bonds are low-risk, fixed-rate bonds. They are purchased at face value and accrue interest over time. The interest on these bonds is typically compounded semiannually, meaning that it is added to the bond’s value twice a year. Series EE bonds have a maturity period of 20 years, but they can be cashed in as early as one year after purchase, though doing so before five years will result in a penalty.

Series I Bonds: Series I bonds are inflation-protected bonds that offer a combination of a fixed interest rate and an inflation rate component. The interest rate is determined at the time of purchase and remains fixed for the life of the bond. The inflation component, on the other hand, adjusts every six months based on changes in the Consumer Price Index for All Urban Consumers (CPI-U). Series I bonds have a minimum holding period of one year and can be cashed in after five years without penalty.

It’s important to note that savings bonds are not intended for short-term investing or quick cash withdrawals. They are designed as long-term investment vehicles, with a focus on preserving capital and earning modest interest over time.

Now that we have a basic understanding of savings bonds, let’s explore the requirements for cashing in these bonds.

Types of Savings Bonds

When it comes to savings bonds, there are two main types: Series EE bonds and Series I bonds. Let’s take a closer look at each type and their features:

Series EE Bonds: Series EE bonds are the most common type of savings bond. These bonds are sold at face value and accrue interest over time. The interest rates on Series EE bonds are fixed and guaranteed, meaning they will not change throughout the life of the bond. The interest on these bonds is typically compounded semiannually.

Series I Bonds: Series I bonds are inflation-protected savings bonds. These bonds offer a combination of a fixed interest rate and an inflation rate component. The fixed interest rate is determined at the time of purchase and remains constant for the life of the bond. The inflation component, on the other hand, is adjusted every six months based on changes in the Consumer Price Index for All Urban Consumers (CPI-U).

Both types of savings bonds have certain advantages and considerations. Series EE bonds are a low-risk investment option that provide a steady and predictable return. They are an excellent choice for individuals who want a stable investment with a guaranteed interest rate. On the other hand, Series I bonds are designed to provide protection against inflation. The inflation rate component of these bonds ensures that your investment keeps pace with the rising cost of living.

It’s important to note that Series EE bonds have a maturity period of 20 years, whereas Series I bonds have a minimum holding period of one year before they can be cashed in. Additionally, if you cash in your bonds before five years from the date of purchase, you may be subject to a penalty, which can amount to three months’ worth of interest earnings on the bonds.

Understanding the differences between these types of savings bonds is essential when it comes to deciding which option is best for your financial goals. Now that we’ve covered the various types of savings bonds, let’s explore the requirements for cashing in these bonds.

Requirements for Cashing Savings Bonds

Before you can cash your savings bonds, there are a few requirements that you need to be aware of. These requirements ensure a smooth and efficient process when it comes to redeeming your bonds. Let’s take a look at what you need to have in order to cash in your savings bonds:

- Ownership: You must be the owner or co-owner of the savings bonds in order to cash them. If you are the sole owner, you can cash the bonds without any additional steps. However, if you are a co-owner, both owners must be present or provide written authorization for the redemption.

- Identification: You will need a valid form of identification to cash in your savings bonds. This can include a valid driver’s license, passport, or other government-issued identification. Make sure that your identification is current and not expired.

- Social Security Number (SSN): You will need to provide your Social Security Number (SSN) at the time of redemption. This is required for tax reporting purposes. If you do not have an SSN, you will need to provide an Individual Taxpayer Identification Number (ITIN) instead.

- Bond Information: You will need to have the relevant bond information available when cashing in your savings bonds. This includes the bond series, serial number, and issue date. This information can be found on the physical bond certificates or in your online TreasuryDirect account.

- Bank Account: In most cases, you will need to have a bank account to receive the funds when cashing in your savings bonds. You can choose to have the funds deposited directly into your bank account or receive a check from the Treasury Department.

It’s important to note that the requirements may vary slightly depending on where you choose to cash in your savings bonds. Banks, credit unions, and financial institutions can have their own specific procedures and documentation requirements. It’s best to contact the institution in advance to confirm their specific requirements and make an appointment if necessary.

Now that you know the requirements for cashing savings bonds, let’s move on to the step-by-step process for redeeming your bonds.

Step-by-Step Process for Cashing Savings Bonds

When you’re ready to cash in your savings bonds, following a step-by-step process will help ensure a smooth and hassle-free experience. While the specific steps may vary depending on the institution where you choose to redeem your bonds, here is a general guide to help you through the process:

- Gather Your Bond Information: Collect all the necessary information about your savings bonds, including the bond series, serial number, and issue date. This information can be found on the physical bond certificates or in your online TreasuryDirect account.

- Confirm Bond Eligibility: Determine if your bonds are eligible for redemption. Some savings bonds may have restrictions on when they can be cashed in. Check the maturity date or any early redemption penalties associated with your bonds.

- Choose Redemption Method: Decide how you would like to redeem your savings bonds. You can typically choose between having the funds directly deposited into your bank account or receiving a check from the Treasury Department.

- Complete Redemption Form: Fill out the necessary redemption form provided by the institution where you are cashing in your bonds. The form will require your personal information, bond details, and payment instructions.

- Provide Identification: Present a valid form of identification, such as a driver’s license or passport, to verify your identity. The institution may make a copy of your identification for their records.

- Verify Ownership: If you are a co-owner of the savings bonds, ensure that all co-owners are present or have provided written authorization for the redemption.

- Submit the Required Documents: Submit the completed redemption form, bond certificates, and any additional supporting documents required by the institution. This may include your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

- Review and Confirm: Carefully review the information on the redemption form and confirm that everything is accurate. Ensure that you have provided the correct bank account information if you have chosen direct deposit.

- Receive Payment: Once the institution verifies your information and processes the redemption request, you will receive payment for your savings bonds. This can be done through a direct deposit into your bank account or by receiving a check in the mail.

- Record the Transaction: Keep a record of the transaction for your own records, including the confirmation number, redemption date, and the amount of the redeemed savings bonds.

It’s important to note that the process may take some time, especially if you are redeeming a large number of savings bonds. It is always recommended to contact the institution in advance, make an appointment, and inquire about any specific requirements or additional documentation needed.

Now that you are familiar with the step-by-step process for cashing in savings bonds, let’s delve into the tax implications of redeeming these investments.

Tax Implications of Cashing Savings Bonds

When you cash in your savings bonds, it’s important to understand the tax implications. Here are the key points to keep in mind:

Interest Income: The interest earned on savings bonds is subject to federal income tax, but it is exempt from state and local taxes. This means you will need to report the interest income on your federal tax return in the year you cash in the bonds.

Taxable or Tax-Free: The tax treatment of savings bond interest depends on how the bonds were used. If the proceeds from the bonds were used to pay for qualified higher education expenses, the interest may be tax-free. However, there are income limits and other eligibility criteria that must be met to qualify for this tax exemption.

Tax-Deferred Option: If you decide not to include the interest income on your tax return at the time of redemption, you have the option to defer reporting the interest until the bonds mature, you redeem them, or you dispose of them. This can be beneficial if you expect to be in a lower tax bracket in the future.

Form 1099-INT: When you cash in your savings bonds, you may receive a Form 1099-INT from the institution where you redeemed the bonds. This form reports the amount of interest income you received and is used to report the income on your tax return.

Tax Planning: If you are considering cashing in a substantial amount of savings bonds, it may be wise to consult with a tax professional or financial advisor. They can help you understand the tax implications and strategize the best approach to minimize your tax liability.

It’s important to note that the tax rules and regulations can change, so it’s wise to stay updated with the latest information from the Internal Revenue Service (IRS) or consult a tax professional to ensure compliance with current tax laws.

Now that we’ve covered the tax implications, let’s explore some alternative options to consider before cashing in your savings bonds.

Alternatives to Cashing Savings Bonds

If you find yourself in need of funds but don’t want to cash in your savings bonds just yet, there are some alternatives you can consider. These options allow you to access the money you need while still maintaining the benefits of your savings bonds. Here are a few alternatives to keep in mind:

1. Emergency Fund: Before cashing in your savings bonds, assess your financial situation and determine if you have an emergency fund in place. An emergency fund provides a financial safety net for unexpected expenses or income disruptions. Consider using your emergency fund first before tapping into your savings bonds.

2. Personal Loans: If you need funds for a specific purpose, such as home improvements or debt consolidation, you might consider applying for a personal loan. Personal loans typically have fixed interest rates and repayment terms, allowing you to borrow a specific amount of money and repay it over time.

3. Line of Credit: If you have a good credit history, you may be eligible for a line of credit. This allows you to borrow money up to a set limit whenever you need it. You only pay interest on the amount you borrow, providing you with flexible access to funds without needing to liquidate your savings bonds.

4. Temporary Reduced Payments: If you have savings bonds that are earning interest and you’re facing a temporary financial setback, consider exploring options to reduce or defer payments for a specific period. Many lenders offer temporary hardship programs that allow you to lower or pause payments until you regain financial stability.

5. Balance Transfer Credit Cards: If you have high-interest debt, consider transferring your balances to a credit card with a 0% introductory APR offer. This gives you a certain period (usually 12 to 18 months) to pay off your debt without accruing interest. By freeing up your cash flow, you may be able to avoid cashing in your savings bonds.

6. Financial Assistance Programs: Depending on your financial situation, you may qualify for various financial assistance programs. These programs can provide temporary relief for housing, utilities, medical expenses, or other essential needs, allowing you to allocate your savings bonds for longer-term financial goals.

Before exploring these alternatives, it’s important to carefully consider their implications and weigh the potential benefits and drawbacks. It’s also advisable to seek the guidance of a financial advisor to help you make the best decision based on your individual circumstances.

Now that we’ve discussed the alternatives, let’s wrap up our article.

Conclusion

Cashing in savings bonds can be a strategic financial decision when you need access to funds. However, it’s crucial to understand the requirements, process, and tax implications before redeeming your bonds. By following the step-by-step process and familiarizing yourself with the necessary documents and identification, you can ensure a smooth and efficient redemption experience.

Before cashing in your savings bonds, consider exploring alternatives to meet your financial needs. Building an emergency fund, exploring personal loans or lines of credit, and taking advantage of financial assistance programs are all viable options to consider. These alternatives allow you to access funds while still keeping your savings bonds intact, preserving their long-term benefits.

Remember to consult with a tax professional or financial advisor to fully understand the tax implications of redeeming your savings bonds. Taking the time to plan and strategize can help minimize your tax liability and maximize your overall financial situation.

In conclusion, savings bonds provide a stable and secure way to save and invest for the future. By understanding the requirements, exploring alternatives, and considering the tax implications, you can make informed decisions when it comes to cashing in your savings bonds. Whether you choose to redeem your bonds now or explore other options, the goal is to make financial decisions that align with your unique circumstances and goals.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: Erika Danniel • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance