Home>Finance>What Interest Rate Does Macy’s Charge After The Minimum Payment

Finance

What Interest Rate Does Macy’s Charge After The Minimum Payment

Published: February 26, 2024

Find out the current interest rate charged by Macy's after making the minimum payment. Get all the finance details you need to manage your Macy's credit card.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

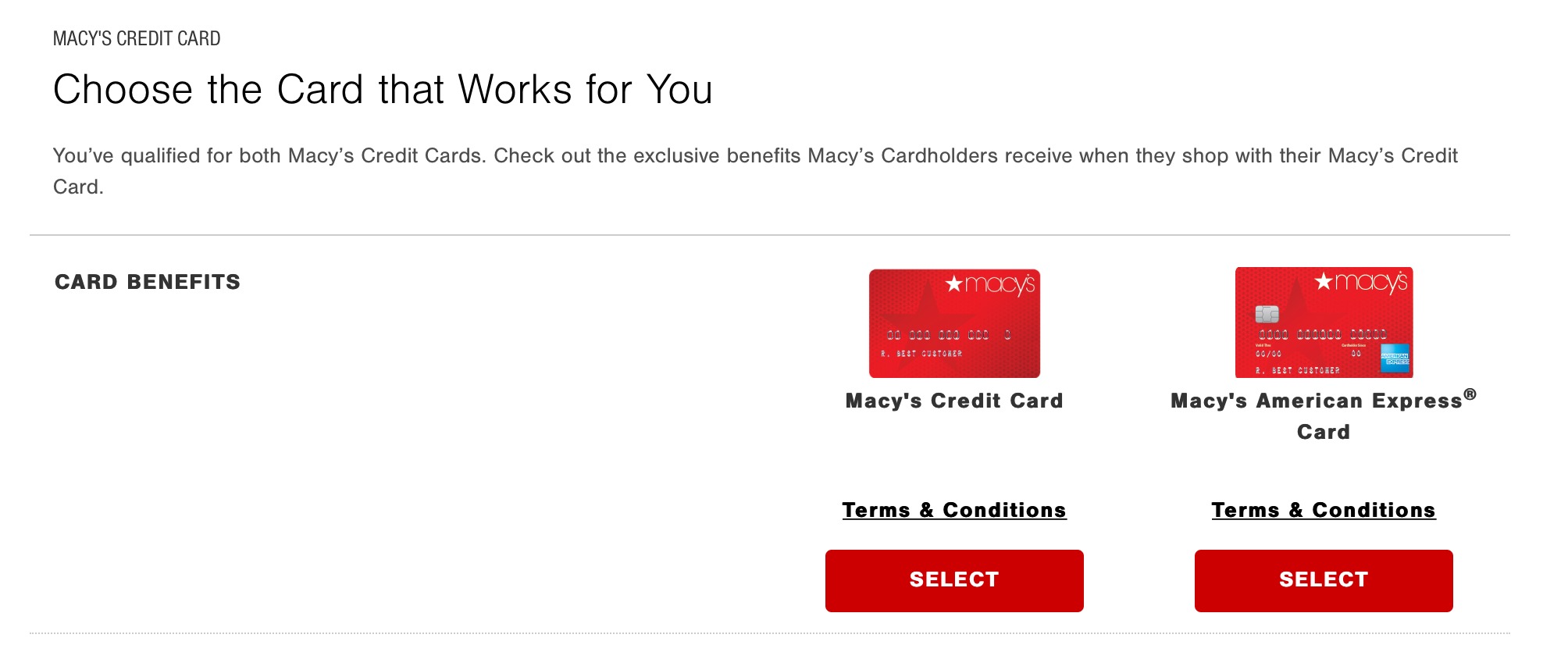

Understanding Macy's Credit Card Interest Rates

When it comes to managing finances, understanding the intricacies of credit card interest rates is crucial. Macy’s, a renowned department store, offers its customers a credit card that comes with its own set of interest rates and payment terms. Navigating the world of credit card interest rates can be daunting, but with the right knowledge, you can make informed decisions that will benefit your financial well-being.

In this article, we will delve into the specifics of Macy’s credit card interest rates, particularly focusing on the interest rate charged after making the minimum payment. By gaining a comprehensive understanding of how these interest rates work, you can take proactive steps to manage your credit card payments effectively and avoid incurring unnecessary interest charges.

Join us as we explore the nuances of Macy’s credit card interest rates, minimum payments, and strategies to minimize interest costs. Whether you’re a Macy’s cardholder or simply seeking to broaden your financial knowledge, this article will provide valuable insights to help you navigate the world of credit card interest rates with confidence.

Understanding Macy’s Credit Card Interest Rates

Before delving into the specifics of Macy’s credit card interest rates, it’s essential to grasp the fundamental concepts that underpin how these rates are structured. When you apply for a Macy’s credit card, you are essentially entering into a financial agreement with the company. As part of this agreement, Macy’s outlines the interest rates that will apply to any outstanding balances on your credit card.

Macy’s credit card interest rates typically fall within a certain range, with the exact rate being determined based on various factors, including your creditworthiness and the prevailing market conditions. It’s important to note that credit card interest rates are often expressed in terms of an annual percentage rate (APR), which represents the annualized cost of borrowing funds through the credit card.

Furthermore, Macy’s may offer promotional interest rates for specific periods, providing cardholders with the opportunity to enjoy lower or even zero interest on qualifying purchases for a limited time. These promotional rates can be advantageous for those looking to make substantial purchases and pay off the balance over a specified promotional period without incurring standard interest charges.

Understanding the nuances of Macy’s credit card interest rates empowers you to make informed decisions regarding your spending and repayment strategies. By familiarizing yourself with the terms and conditions associated with the credit card, you can leverage this knowledge to minimize interest costs and optimize your financial management.

Next, we will explore the relationship between minimum payments and interest rates, shedding light on how these elements intersect to impact your overall credit card obligations.

Minimum Payment and Interest Rates

When it comes to credit card payments, understanding the correlation between the minimum payment and interest rates is paramount. The minimum payment represents the smallest amount you are required to pay each month to keep your account in good standing. This amount is typically calculated as a percentage of your total outstanding balance, subject to a minimum dollar value.

It’s important to recognize that while making the minimum payment helps you avoid late fees and maintain a positive payment history, it may not be sufficient to prevent the accrual of substantial interest charges. When you carry a balance beyond the billing cycle, interest charges apply to the remaining amount, contributing to the overall cost of borrowing.

As for Macy’s credit card, the interest rate that applies after making the minimum payment is determined by the outstanding balance and the prevailing APR. This means that even after meeting the minimum payment requirement, the remaining balance continues to accrue interest based on the applicable rate. Consequently, failing to pay more than the minimum amount can result in a prolonged repayment period and higher overall interest costs.

It’s crucial to recognize that while the minimum payment helps you fulfill the basic obligation, it’s in your best interest to pay more than the minimum whenever possible. By doing so, you can expedite the reduction of your outstanding balance and minimize the long-term impact of interest charges.

Moreover, understanding the relationship between minimum payments and interest rates empowers you to devise a proactive repayment strategy. Whether it involves allocating additional funds toward your credit card payments or exploring alternative payment structures, being mindful of these dynamics can significantly influence your financial well-being.

Next, we will explore effective strategies to avoid high interest rates and optimize your credit card management.

How to Avoid High Interest Rates

Effectively managing your Macy’s credit card to minimize interest costs involves implementing strategic measures that align with your financial circumstances and goals. Here are several actionable strategies to help you avoid high interest rates:

- Pay More Than the Minimum: While the minimum payment fulfills the basic requirement, allocating additional funds toward your credit card balance can expedite the reduction of interest charges. By paying more than the minimum, you can make significant strides in lowering your outstanding balance and mitigating the impact of accruing interest.

- Take Advantage of Promotional Rates: If Macy’s offers promotional interest rates for specific purchases or balance transfers, consider leveraging these opportunities to minimize interest costs. Making qualifying purchases during promotional periods can enable you to manage your expenses more efficiently while benefiting from reduced or waived interest charges for a predetermined duration.

- Monitor Your Spending: Keeping a close eye on your credit card expenditures can help you maintain control over your balance and avoid carrying high levels of debt. By practicing prudent spending habits and staying within your budget, you can mitigate the need for extensive credit card borrowing and the associated interest expenses.

- Explore Balance Transfer Options: If you have balances on other credit cards with higher interest rates, exploring the possibility of transferring these balances to your Macy’s credit card, especially during promotional periods, can be a strategic move. This consolidation can streamline your repayment efforts and potentially reduce the overall interest burden.

- Seek Financial Counseling: If you find yourself grappling with substantial credit card debt and high interest rates, seeking guidance from a financial counselor or advisor can provide valuable insights and tailored strategies to alleviate your financial challenges. These professionals can offer personalized recommendations to help you navigate your credit card obligations more effectively.

By incorporating these proactive measures into your financial management approach, you can take meaningful steps to avoid high interest rates and optimize the utilization of your Macy’s credit card. Empowering yourself with the knowledge and resources to make informed financial decisions will contribute to a more secure and sustainable financial future.

Conclusion

Navigating the realm of credit card interest rates, particularly within the context of Macy’s credit card offerings, presents both challenges and opportunities for consumers. By gaining a comprehensive understanding of how these interest rates operate and intersect with minimum payments, individuals can make informed decisions to manage their credit card obligations effectively.

Throughout this exploration, we’ve underscored the significance of comprehending the relationship between minimum payments and interest rates, emphasizing the potential impact on overall borrowing costs. While making the minimum payment is a fundamental obligation, it’s essential to recognize that carrying a balance beyond this threshold can lead to the accrual of substantial interest charges, ultimately prolonging the repayment period.

Furthermore, we’ve highlighted actionable strategies to avoid high interest rates, including paying more than the minimum, capitalizing on promotional rates, monitoring spending habits, exploring balance transfer options, and seeking professional financial guidance when needed. These strategies empower individuals to take proactive steps in managing their Macy’s credit card effectively and minimizing the long-term impact of interest costs.

Ultimately, by arming yourself with knowledge and implementing prudent financial practices, you can navigate the intricacies of credit card interest rates with confidence and foresight. Whether it involves optimizing your repayment strategies, leveraging promotional opportunities, or seeking expert advice, the proactive approach to credit card management can yield significant benefits in terms of interest cost reduction and overall financial well-being.

As you continue your financial journey, remember that staying informed and proactive is key to making sound financial decisions. By applying the insights gleaned from this article, you can harness the potential of your Macy’s credit card while mitigating the impact of high interest rates, paving the way for a more secure and sustainable financial future.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance