Finance

What Is Capital Markets In Banking

Modified: December 30, 2023

Learn about capital markets in banking and the role of finance. Explore various aspects of this financial system and understand its importance in the banking industry.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to the world of capital markets in banking! In this article, we will explore the role and significance of capital markets in the banking industry. Whether you’re a finance professional or someone just curious about the complex workings of the financial world, understanding capital markets is essential.

Capital markets play a vital role in facilitating the flow of funds between individuals, corporations, and governments. They provide a platform for buying and selling financial securities such as stocks, bonds, and derivatives. This article will delve into the definition, purpose, and functioning of capital markets, and how they influence the banking sector.

Capital markets are where vast amounts of money are raised, invested, and traded. They enable businesses and governments to finance their operations and projects by issuing stocks and bonds to investors. Banks, as intermediaries in the financial system, facilitate this process through various activities such as underwriting, trading, and advising clients on capital market transactions.

Understanding capital markets is crucial because they have a significant impact on the overall economy. They contribute to economic growth by providing a channel for the efficient allocation of capital, enabling businesses to expand, innovate, and create job opportunities. Capital markets also provide individuals with opportunities to invest their savings and grow their wealth.

Throughout this article, we will explore the types of capital market instruments and their role in the banking industry. We will also delve into the benefits that capital markets offer to banks and the associated risks and challenges. Furthermore, we will touch upon the regulation and oversight of capital markets to ensure transparency and stability in financial systems.

So, whether you’re a banking professional looking to expand your knowledge or simply intrigued by the inner workings of the financial world, grab a cup of coffee and join us on this informative journey into the world of capital markets in banking!

Definition of Capital Markets

In order to understand the role of capital markets in banking, it’s important to have a clear understanding of what capital markets are. Capital markets refer to the platforms where individuals and institutions trade financial securities such as stocks, bonds, and derivatives.

These markets enable the buying and selling of these securities, providing a means for companies and governments to raise capital. Investors can participate in capital markets by purchasing these securities, either directly from the issuer or through intermediaries such as banks and brokerage firms.

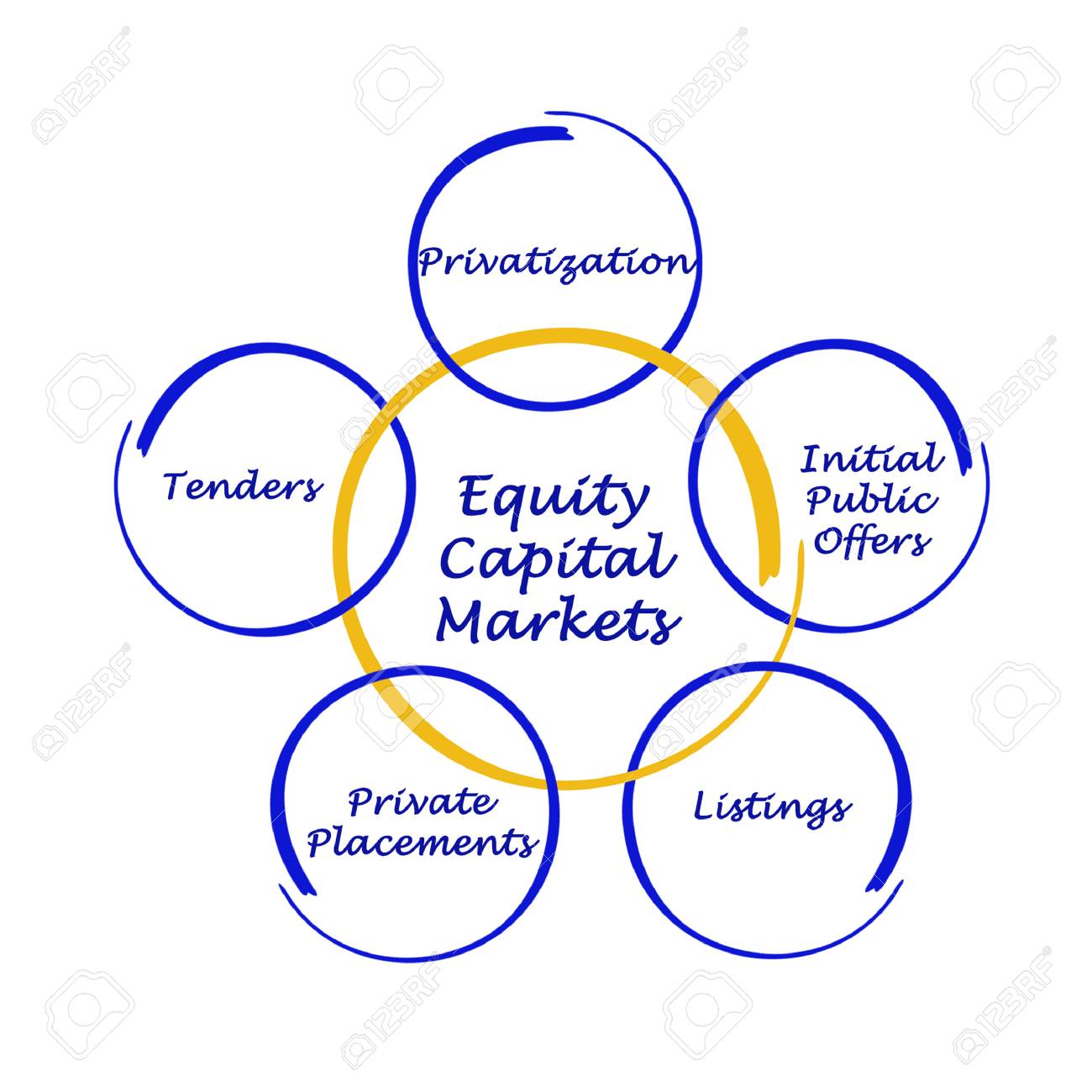

Capital markets can be categorized into two main types: primary markets and secondary markets. The primary market is where new securities are issued and sold to investors for the first time. This is typically done through initial public offerings (IPOs) for stocks or bond issuances. In the primary market, companies and governments raise capital by selling their securities directly to investors.

The secondary market, on the other hand, is where previously issued securities are traded among investors. This is where most of the buying and selling of stocks and bonds takes place. The secondary market provides liquidity to investors, allowing them to easily buy and sell securities, even after the initial offering.

Capital markets are characterized by their openness and transparency, ensuring fair and efficient trading. They provide a platform for price discovery, as the value of securities is determined by the interaction of supply and demand in the market. Additionally, capital markets play a crucial role in determining the cost of capital for businesses and governments, as the interest rates on bonds and the valuation of stocks are influenced by market conditions.

Overall, capital markets serve as an essential component of the financial system, facilitating the flow of funds and enabling economic growth. They provide opportunities for investors to allocate their capital in various securities, based on their risk appetite and return expectations. For banks, capital markets offer avenues for revenue generation through activities such as underwriting, trading, and providing advisory services to clients participating in capital market transactions.

Now that we have a solid understanding of the definition of capital markets, let’s explore the role they play in the banking industry.

Role of Capital Markets in Banking

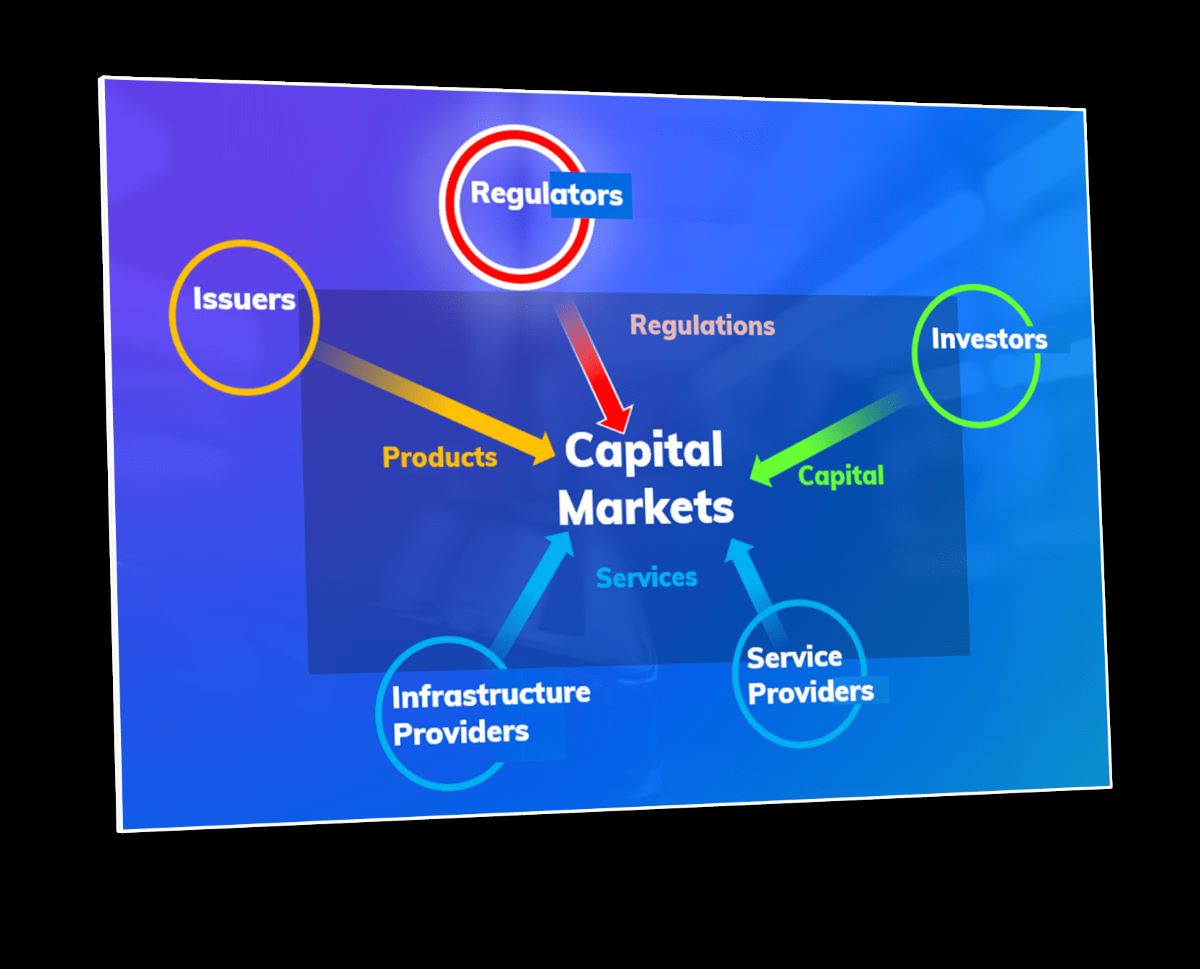

Capital markets play a significant role in the banking industry, serving as a crucial link between borrowers and lenders. Banks engage in various activities related to capital markets, facilitating the flow of funds and providing essential services to clients. Here are some key roles of capital markets in banking:

1. Capital Raising: Capital markets provide banks with avenues to raise funds for their operations and lending activities. Banks can issue debt securities, such as bonds, to investors in the capital markets. These funds can be used to finance loans, invest in new projects, or strengthen the bank’s balance sheet. By accessing capital markets, banks can diversify their funding sources and reduce their reliance on traditional deposits.

2. Underwriting and Distribution: Banks often play a crucial role in underwriting new securities issued by companies and governments. This involves assessing the risks associated with the securities, pricing them, and then distributing them to investors. Banks earn fees for their underwriting services, enabling them to generate income from capital market transactions.

3. Trading: Capital markets provide banks with opportunities for trading various financial instruments, such as stocks, bonds, and derivatives. Banks have specialized trading desks that engage in buying and selling securities on behalf of clients or for their own proprietary trading activities. Trading in capital markets allows banks to generate profits from price fluctuations and market trends.

4. Advisory Services: Banks offer advisory services to clients participating in capital market transactions. This includes providing strategic advice on capital raising, mergers and acquisitions, and other financial matters. Banks with expertise in capital markets can assist clients in navigating the complexities of the market and achieving their financial objectives.

5. Risk Management: Capital markets can be volatile and subject to risks such as market fluctuations, credit risk, and liquidity risk. Banks play a crucial role in managing these risks for themselves and their clients. Through risk management techniques and hedging strategies, banks can mitigate the potential negative impact of capital market volatility on their balance sheets.

Overall, capital markets are a vital component of the banking industry, providing banks with opportunities to raise funds, generate income, and offer valuable services to clients. The integration of capital markets and banking enables the efficient allocation of capital, promotes economic growth, and supports the functioning of the broader financial system.

Now that we understand the role of capital markets in banking, let’s explore the different types of instruments traded in capital markets.

Types of Capital Markets Instruments

Capital markets offer a wide range of instruments that are traded among investors and institutions. These instruments provide investment opportunities and serve various purposes for both issuers and investors. Let’s explore some of the key types of capital market instruments:

1. Stocks (Equities): Stocks represent ownership shares in a company. When investors purchase stocks, they become shareholders and have a claim on the company’s assets and earnings. Stocks can be traded on stock exchanges and allow investors to participate in the company’s growth and success through capital appreciation and dividends.

2. Bonds (Debt Securities): Bonds are fixed-income securities issued by governments, municipalities, and corporations to raise capital. When investors purchase bonds, they are essentially lending money to the issuer in exchange for regular interest payments and the return of the principal amount at maturity. Bonds have different characteristics such as coupon rates, maturity dates, and credit ratings, which determine their attractiveness to investors.

3. Commodities: Commodities are raw materials or primary agricultural products that can be bought and sold in capital markets. Examples of commodities include crude oil, gold, wheat, and coffee. Investors can trade commodity futures contracts, allowing them to speculate on the price movements of these commodities without physically owning the underlying assets.

4. Derivatives: Derivatives are financial instruments whose value is derived from an underlying asset. Common types of derivatives include options, futures, forwards, and swaps. Derivatives provide investors with the opportunity to speculate on the price movements of assets or to hedge their risks. They can be highly complex and involve leverage, making them suitable for advanced investors and institutions.

5. Exchange-Traded Funds (ETFs): ETFs are investment funds that are traded on stock exchanges, offering investors exposure to a diversified portfolio of assets. ETFs can track various indexes, sectors, or asset classes, allowing investors to gain broad market exposure or target specific investment strategies. ETFs provide liquidity and flexibility to investors, as they can be bought and sold throughout the trading day.

6. Real Estate Investment Trusts (REITs): REITs are investment vehicles that own and operate income-generating real estate properties. Investors can buy shares of REITs, which provide them with exposure to real estate assets without the need for direct ownership. REITs offer regular dividend payments and potential capital appreciation based on the performance of the underlying properties.

These are just a few examples of the capital market instruments available. Each instrument has its own unique characteristics, risks, and potential returns, catering to the diverse needs and preferences of investors. Banks play a crucial role in the trading and distribution of these instruments, providing liquidity and advisory services to clients.

Now that we’ve explored the different types of capital market instruments, let’s delve into the benefits that capital markets offer to banks.

Benefits of Capital Markets for Banks

Capital markets offer various benefits to banks, enhancing their capabilities and contributing to their overall performance. Here are some key benefits that capital markets provide to banks:

1. Diversification of Funding Sources: Capital markets enable banks to diversify their funding sources beyond traditional deposits. By accessing capital markets, banks can raise funds through debt issuances, such as bonds, and equity offerings, such as IPOs. This diversification reduces dependence on a single funding channel and provides greater flexibility in managing liquidity and funding needs.

2. Revenue Generation: Capital market activities generate significant revenue for banks. Banks earn fees and commissions from providing underwriting services for new securities issuances. They also generate income from trading activities, including buying and selling securities for clients or proprietary trading. By participating in capital markets, banks can expand their revenue streams and enhance their profitability.

3. Enhanced Advisory Services: Capital markets provide an opportunity for banks to offer comprehensive advisory services to their clients. Banks with expertise in capital market transactions can advise businesses and governments on capital raising strategies, mergers and acquisitions, and other financial matters. These advisory services not only generate revenue but also strengthen relationships with clients.

4. Liquidity Provision: Banks play a crucial role in providing liquidity in capital markets. They act as market makers, facilitating the buying and selling of securities. By offering competitive bid and ask prices, banks add liquidity and depth to the market, making it easier for investors to transact. This liquidity provision enhances market efficiency and encourages active participation.

5. Risk Management: Capital markets help banks manage risks through hedging and risk transfer mechanisms. Banks can use derivatives, such as futures and options, to hedge against potential losses or fluctuations in interest rates, foreign exchange rates, or commodity prices. By effectively managing risks, banks can protect their balance sheets and ensure stability in their operations.

6. Market Intelligence: Participating in capital markets provides banks with valuable market intelligence. Banks closely monitor market trends, investor sentiment, and regulatory developments to stay informed and make informed decisions. This market intelligence helps banks identify new opportunities, assess risks, and adapt their strategies to changing market conditions.

Overall, capital markets offer numerous benefits to banks, ranging from revenue generation and diversification of funding sources to enhanced advisory services and risk management capabilities. These benefits contribute to the overall strength and competitiveness of banks in the financial industry.

Nevertheless, it is important to note that participation in capital markets also comes with risks and challenges. Let’s explore some of these risks and challenges in the next section.

Risks and Challenges in Capital Markets

While capital markets offer various benefits, they also come with inherent risks and challenges that banks and investors must navigate. Understanding these risks and challenges is essential for effective risk management and decision-making. Let’s explore some of the key risks and challenges in capital markets:

1. Market Volatility: Capital markets can be prone to significant price fluctuations and volatility. Changes in economic conditions, geopolitical events, and investor sentiment can greatly impact the value of securities. Banks and investors must be prepared for market volatility and have contingency plans to manage potential losses and mitigate risks associated with price movements.

2. Credit Risk: Banks face credit risk when investing in or trading securities. This risk arises from the possibility of default by the issuer of the security or counterparty in a transaction. To manage credit risk, banks employ rigorous credit assessment and risk analysis frameworks. They also diversify their portfolios and monitor the creditworthiness of counterparties on an ongoing basis.

3. Liquidity Risk: Liquidity risk refers to the risk of not being able to buy or sell securities at desired prices due to insufficient market liquidity. Banks may face challenges in liquidating their positions or fulfilling the trading needs of clients during times of illiquidity. To manage liquidity risk, banks maintain adequate liquidity buffers and engage in prudent risk-taking practices.

4. Regulatory and Compliance Risks: Capital markets are subject to extensive regulations and oversight to ensure fairness, transparency, and stability. Banks operating in capital markets must comply with numerous regulations related to disclosures, trading practices, risk management, and client protection. Failure to comply with these regulations can lead to reputational damage, financial penalties, or even legal consequences.

5. Technology and Cybersecurity Risks: The increasing use of technology in capital markets introduces additional risks. Banks must be vigilant in protecting their systems, data, and client information from cyber threats, such as hacking and unauthorized access. Banks must also continuously invest in technology infrastructure to keep pace with advancements and ensure efficient and secure market operations.

6. Complexity and Information Asymmetry: Capital markets can be complex and difficult to understand, especially for retail investors. There is often a significant information asymmetry between market participants, with certain players having access to more information and resources than others. Banks must ensure that they provide clear and transparent information to clients, promote financial literacy, and act in the best interests of their clients.

Successfully navigating these risks and challenges requires banks to have robust risk management frameworks, strong internal controls, and a deep understanding of market dynamics. It also necessitates continuous monitoring, timely adaptation, and adherence to regulatory requirements and industry best practices.

Now that we’ve explored the risks and challenges in capital markets, let’s dive into the regulation and oversight that governs these markets.

Regulation and Oversight of Capital Markets

The regulation and oversight of capital markets are crucial to ensure fair, transparent, and efficient functioning of these markets. Regulatory frameworks are designed to protect investors, maintain market integrity, and promote financial stability. Let’s explore the key aspects of regulation and oversight in capital markets:

1. Securities and Exchange Commissions: In many jurisdictions, capital markets are regulated by Securities and Exchange Commissions or similar regulatory bodies. These organizations are responsible for creating and enforcing regulations that govern the issuance, trading, and disclosure of securities. They oversee the activities of market participants, including banks, to ensure compliance with rules and regulations.

2. Investor Protection: Investor protection is a fundamental objective of capital market regulations. Regulatory bodies establish rules to safeguard the interests of investors, such as requiring companies to disclose relevant information to the public. These regulations aim to prevent fraudulent activities, ensure fair treatment of investors, and promote transparency in the capital markets.

3. Listing Requirements: Stock exchanges typically have listing requirements for companies wishing to list their securities for trading. These requirements include financial reporting standards, corporate governance practices, and compliance with certain regulatory guidelines. Banks play a role in assessing whether companies meet these listing requirements and helping them navigate the process.

4. Market Surveillance: Regulatory bodies employ market surveillance mechanisms to monitor capital markets for potential misconduct and manipulation. They analyze trading data and patterns to detect insider trading, market abuse, and other illegal activities. Banks must cooperate with regulatory bodies by providing information and maintaining robust internal controls to prevent market misconduct.

5. Capital Adequacy and Risk Management: Regulatory frameworks set capital adequacy requirements for banks participating in capital markets. These requirements ensure that banks have sufficient capital to handle potential risks arising from their market activities. Regulators also establish risk management guidelines to govern how banks identify, measure, and manage risks associated with capital market operations.

6. Cross-Border Regulations: Capital markets often involve cross-border transactions, requiring coordination between regulatory bodies across different jurisdictions. International agreements and organizations, such as the International Organization of Securities Commissions (IOSCO), facilitate the harmonization of regulations, cross-border supervision, and the exchange of information among regulatory authorities.

Effective regulation and oversight of capital markets promote investor confidence, maintain market stability, and prevent systemic risks. Banks operating in capital markets must comply with regulatory requirements, maintain robust internal controls, and adhere to anti-money laundering and counter-terrorism financing regulations.

It is important to note that regulatory frameworks are continuously evolving to keep pace with market developments and address emerging risks. Regular updates and amendments to regulations reflect the dynamic nature of capital markets and aim to maintain their integrity and resilience.

Now that we have explored the regulation and oversight of capital markets, let’s conclude our discussion.

Conclusion

Capital markets play a vital role in the banking industry, serving as a platform for the buying and selling of financial securities. They facilitate the flow of funds, enable capital raising for companies and governments, and provide investment opportunities for individuals. Banks play a crucial role in capital markets by offering services such as underwriting, trading, and advisory, and benefit from the revenue generated through these activities.

The diverse range of capital market instruments, including stocks, bonds, commodities, derivatives, ETFs, and REITs, offers investors various opportunities for growth, income generation, and risk management. Banks, along with other market participants, contribute to the liquidity and efficiency of capital markets, providing valuable services to clients and supporting economic growth.

While capital markets offer significant benefits, they also come with inherent risks and challenges. Market volatility, credit risk, liquidity risk, regulatory compliance, technology risk, and information asymmetry are some of the risks that banks and investors must navigate. Effective risk management and adherence to regulatory frameworks are crucial for mitigating these risks and maintaining market stability.

Regulation and oversight play a key role in ensuring the fair and transparent functioning of capital markets. Regulatory bodies, such as Securities and Exchange Commissions, establish rules and standards that promote investor protection, market integrity, and financial stability. Collaboration between regulators and market participants is essential for effective surveillance and compliance with regulatory requirements.

In conclusion, capital markets are integral to the banking industry, providing banks with opportunities for revenue generation, diversification of funding sources, enhanced advisory services, and risk management capabilities. By participating in capital markets and adhering to regulatory frameworks, banks can contribute to the efficient allocation of capital and support economic growth.

Understanding the dynamics of capital markets and their interaction with the banking sector is crucial for professionals in the finance industry and individuals interested in the workings of the financial world. By staying informed about developments, market trends, and regulatory changes, stakeholders can make informed decisions and navigate the complexities of capital markets successfully.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance