Finance

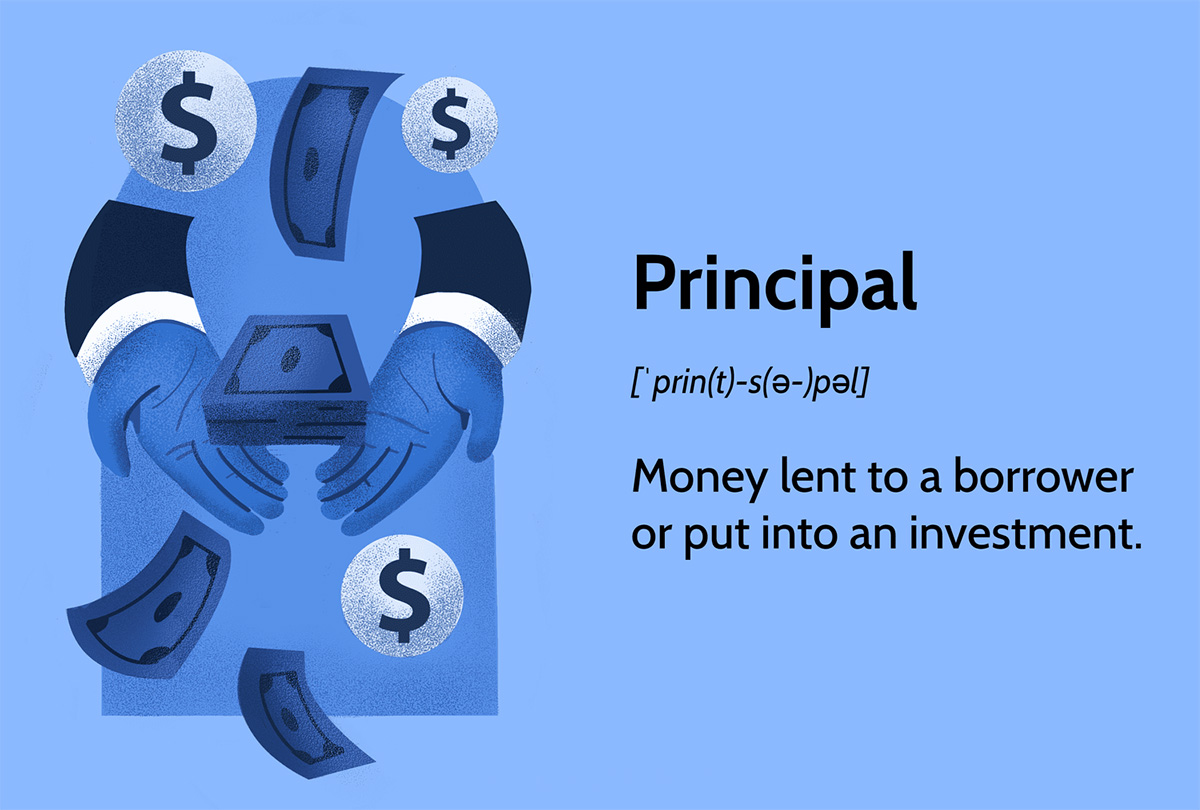

What Is Principal In Banking

Published: October 11, 2023

Discover what principal means in banking and how it relates to finance. Gain insights into the role of principal in managing financial transactions and investments.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Welcome to the world of banking, where financial transactions take place on a daily basis. In this dynamic industry, it is essential to have a thorough understanding of various banking terms and concepts to navigate the complex landscape with ease. One such concept that holds great significance is the principle in banking.

The principle in banking refers to the initial amount of money that is invested or borrowed. It is the foundation upon which banking transactions are built. Whether it’s a personal loan, a mortgage, or an investment in a savings account, the principle plays a crucial role in determining the financial implications of these transactions.

Understanding the principle in banking is not limited to financial professionals or bankers. It is a concept that holds relevance for individuals, businesses, and governments alike. From managing personal finances to making informed investment decisions, having a clear understanding of the principle helps individuals make well-informed choices.

So, in this article, we will delve deeper into the concept of the principle in banking, exploring its definition, importance, role in banking transactions, and its distinction from interest. We will also discuss the various factors that can affect the principle amount in banking transactions. By the end, you will have a comprehensive understanding of this fundamental concept in the banking industry.

Definition of Principal in Banking

In the world of banking and finance, the term “principal” refers to the initial amount of money that is either invested or borrowed in a financial transaction. It serves as the foundation or base amount upon which interest, fees, and other charges are calculated.

When an individual or an organization invests money in a bank, the principal is the initial amount deposited. This can be in the form of a savings account, fixed deposit, or any other type of investment product offered by the bank. The principal amount may increase over time due to the interest earned on the investment, but it remains the base value that was initially invested.

On the other hand, when someone borrows money from a bank, the principal is the amount initially borrowed. For example, when obtaining a mortgage to purchase a home, the principal amount is the loan amount that is used to buy the property. This is the amount that needs to be repaid to the bank over a specific period of time, along with any interest and fees that may be charged.

The principal amount plays a crucial role in determining the overall cost and terms of a financial transaction. It forms the basis for calculating interest payments, loan repayments, and investment returns. The higher the principal amount, the higher the potential returns or costs associated with the transaction.

It’s important to note that while the principal amount remains constant throughout the duration of a transaction, the interest and fees associated with it can vary. In the case of investments, the interest earned on the principal may be fixed or fluctuating, depending on the type of investment product. Similarly, when borrowing money, the interest charged may be fixed or variable, which can impact the total amount repaid.

Importance of Principal in Banking

The principal in banking holds significant importance in several aspects of financial transactions. Understanding its importance is crucial for both individuals and institutions involved in banking activities. Here are some key reasons why the principal is essential in the banking industry:

- Calculation of Interest: The principal amount is used as the baseline for calculating interest payments. Whether it’s a loan or an investment, the interest is usually calculated as a percentage of the principal. Thus, the principal directly impacts the interest payable or earned, influencing the overall cost or return on the financial transaction.

- Determining Loan Repayments: When borrowing money, the principal amount forms the basis for calculating the loan repayments. The repayment amount often includes a portion towards the principal and the interest charged. A higher principal amount means higher monthly repayments, while a lower principal decreases the repayment burden.

- Assessing Investment Returns: For investors, the principal amount invested determines the potential returns on investment. The interest or returns earned are typically a percentage of the principal. Therefore, a higher principal can lead to increased investment returns, providing an opportunity for capital growth or income generation.

- Budgeting and Financial Planning: Understanding the principal amount is crucial for effective budgeting and financial planning. It helps individuals and businesses forecast their financial commitments, calculate loan repayments, and estimate investment returns. By considering the principal amount, individuals can make informed decisions regarding their financial goals and objectives.

- Managing Risk: The principal amount also plays a role in managing risk in banking transactions. Lenders often assess the borrower’s ability to repay the principal along with the interest. The risk associated with the principal is assessed based on factors such as credit history, income, and collateral, to ensure that the borrower can meet their financial obligations.

In summary, the principal in banking holds significant importance as it forms the foundation for calculating interest, loan repayments, investment returns, and helps in budgeting and risk management. Understanding the role of the principal is essential for individuals and institutions to make informed financial decisions and navigate the banking landscape effectively.

Role of Principal in Banking Transactions

The principal in banking transactions plays a crucial role in determining the financial implications of various activities. Whether it’s borrowing money, investing, or managing personal finances, the principal amount serves as a key factor in these transactions. Let’s explore the specific roles of the principal in different banking activities:

- Borrowing Money: When individuals or businesses borrow money from a bank, the principal amount represents the initial loan amount received. It determines the total amount that needs to be repaid, along with any interest and fees, over a specified period. The principal provides the borrower with the necessary funds for their intended purposes, such as buying a home, starting a business, or funding educational expenses.

- Investing: In the context of investments, the principal amount is the initial sum of money invested. It serves as the basis for calculating potential returns. The interest or dividends earned on the principal contribute to the overall investment performance. Investors aim to maximize their principal through capital appreciation, dividend payments, or interest income.

- Calculating Interest: The principal amount is used to calculate the interest payable or earned in various banking transactions. For borrowers, the interest is calculated as a percentage of the principal, determining the interest payments along with the loan repayment amount. On the other hand, for investors, the principal influences the calculation of interest or returns earned on investments.

- Loan Amortization: Amortization refers to the process of gradually reducing the principal amount owed on a loan through regular payments. The principal plays a key role in the amortization process as the payments made are primarily used to reduce the outstanding principal balance. Gradually reducing the principal through regular payments leads to a decrease in the interest charged over time.

- Calculating Balances: The principal amount is used to calculate the various account balances in banking transactions. For instance, in a savings account, the principal represents the initial deposit, while interest earned is added to the principal to calculate the account balance. Similarly, in a loan or credit card account, the principal is reduced by regular payments made by the borrower.

The principal amount plays a vital role in determining the financial implications of banking transactions. It provides the basis for interest calculations, loan repayment calculations, investment returns, and account balances. Understanding the role of the principal helps individuals and businesses make informed decisions about borrowing, investing, and managing their financial resources effectively.

Principal vs. Interest in Banking

When it comes to banking transactions, it’s important to understand the distinction between principal and interest. While these terms are closely related, they represent different aspects of financial transactions. Let’s explore the differences between principal and interest in banking:

Principal: The principal amount refers to the initial sum of money that is either invested or borrowed in a financial transaction. It serves as the base amount upon which interest and other calculations are made. For borrowing transactions, the principal represents the loan amount, while for investments, it denotes the initial investment amount. The principal amount remains constant throughout the duration of the transaction unless further investments or withdrawals are made.

Interest: Interest, on the other hand, is the additional amount charged or earned on top of the principal in a financial transaction. When borrowing money, interest is the cost of borrowing and represents the fee paid to the lender for the use of their funds. For investments, it is the return earned on the principal amount. Interest is typically calculated as a percentage of the principal, and it can be fixed or variable, depending on the terms of the transaction or the prevailing market conditions.

The key distinctions between principal and interest are as follows:

- Role: The principal amount represents the base value of the transaction, whereas interest is an additional charge or return on top of the principal.

- Calculation: The principal remains constant throughout the transaction, while the interest is calculated based on the principal and the applicable interest rate.

- Financial Implications: The principal amount determines the total amount borrowed or invested and influences the overall cost or potential returns. Interest, on the other hand, affects the monthly loan repayments or the investment returns earned.

- Payment Allocations: When making loan repayments, a portion of the payment is allocated towards reducing the principal, while the remaining portion goes towards interest. Over time, the principal amount decreases, leading to a reduction in the interest charged.

- Legal Considerations: The principal amount is the legally obligated amount that needs to be repaid in borrowing transactions. Interest, on the other hand, is subject to legal regulations and can have specific terms and conditions.

Understanding the distinction between principal and interest is crucial for borrowers and investors alike. It allows individuals to accurately assess the total cost or potential returns of a transaction, make informed financial decisions, and effectively manage their finances.

Factors Affecting Principal in Banking

Several factors can affect the principal amount in banking transactions. These factors can impact the initial investment or borrowing amount and subsequently influence the overall financial implications of the transaction. Let’s explore some key factors that can affect the principal in banking:

- Interest Rates: Fluctuations in interest rates can directly impact the principal amount in banking transactions. Changes in interest rates can affect the cost of borrowing or the returns earned on investments. Higher interest rates can increase the cost of borrowing, leading to a larger principal amount in loan transactions. Similarly, higher interest rates can result in higher returns on investments, increasing the principal amount in investment transactions.

- Market Conditions: Market conditions, including economic stability, inflation rates, and stock market performance, can affect the principal amount in investment transactions. Positive market conditions, such as strong economic growth or bullish stock markets, can lead to increased investment returns, resulting in a higher principal amount. Conversely, unfavorable market conditions can result in lower investment returns and a decrease in the principal amount.

- Creditworthiness: Borrowers’ creditworthiness plays a significant role in determining the principal amount in loan transactions. Lenders assess the creditworthiness of borrowers based on factors such as credit history, income, and debt-to-income ratio. A higher creditworthiness may result in a larger principal amount offered by the lender, while lower creditworthiness may restrict the borrowing amount.

- Collateral: In secured loan transactions, the presence of collateral can affect the principal amount. Collateral is an asset pledged by the borrower to secure the loan. It provides a level of protection for the lender in case of default. If the borrower offers valuable collateral, such as a property or a vehicle, the lender may be more willing to offer a higher principal amount.

- Loan Term: The term or duration of a loan can impact the principal amount. Longer loan terms can result in higher principal amounts, as the repayment period is extended, and more interest accumulates over time. Conversely, shorter loan terms often come with lower principal amounts, as the repayment period is shorter, leading to less interest accumulation.

It’s important to consider these factors when engaging in banking transactions, as they can significantly impact the principal amount and the overall financial implications. Individuals and businesses should carefully assess and evaluate these factors to make informed decisions related to investing, borrowing, and managing their finances effectively in the banking industry.

Conclusion

The principal in banking is a fundamental concept that plays a crucial role in various financial transactions. Whether it’s borrowing money, investing, or managing personal finances, understanding the principal is essential for making informed decisions and navigating the complex world of banking effectively.

In this article, we explored the definition of the principal in banking and its importance. We learned that the principal represents the initial amount of money invested or borrowed in a financial transaction and serves as the base value for calculating interest, loan repayments, investment returns, and account balances.

We also explored the role of the principal in different banking transactions. From borrowing money and investing to calculating interest and amortization, the principal plays a significant role in determining the financial implications of these activities.

Additionally, we discussed the distinction between principal and interest in banking. While principal remains constant throughout the transaction, interest represents the additional charge or return on top of the principal. Understanding this distinction is crucial in accurately assessing the total cost or potential returns of a banking transaction.

Lastly, we explored the factors that can affect the principal in banking transactions. Variables such as interest rates, market conditions, creditworthiness, collateral, and loan terms can impact the initial amount invested or borrowed, influencing the overall financial implications of the transaction.

By understanding the concept of the principal in banking and considering the factors that affect it, individuals and businesses can make well-informed decisions to manage their finances effectively. Whether it’s optimizing loan repayments, maximizing investment returns, or planning for financial goals, a solid understanding of the principal is vital for navigating the banking landscape with confidence.

So, as you engage in banking transactions or explore opportunities to grow your finances, remember the importance of the principal and how it shapes your financial journey.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance