Finance

What Is Purchase APR On A Credit Card?

Published: March 3, 2024

Learn what purchase APR is on a credit card and how it impacts your finances. Understand the importance of managing your credit card's finance charges.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Understanding Purchase APR on Credit Cards

Credit cards have become an integral part of modern-day financial transactions, offering convenience and flexibility to users. However, the world of credit cards is often accompanied by complex terminologies and intricacies that can be overwhelming for many individuals. One such crucial aspect of credit cards is the Purchase Annual Percentage Rate (APR). Understanding what Purchase APR entails is essential for making informed financial decisions and effectively managing one's credit card usage.

The Purchase APR represents the annualized interest rate that applies to outstanding balances resulting from purchases made using a credit card. This rate significantly influences the cost of carrying a balance on the card, thereby impacting the overall financial health of the cardholder. It is crucial to comprehend how Purchase APR is calculated, its implications on credit card users, and strategies for effectively managing it to mitigate financial burdens.

In the following sections, we will delve deeper into the concept of Purchase APR, explore its calculation methodology, analyze its impact on credit card users, and provide insights into managing Purchase APR effectively. By gaining a comprehensive understanding of Purchase APR, individuals can navigate the realm of credit cards with confidence and make prudent financial choices aligned with their long-term goals.

Understanding Purchase APR

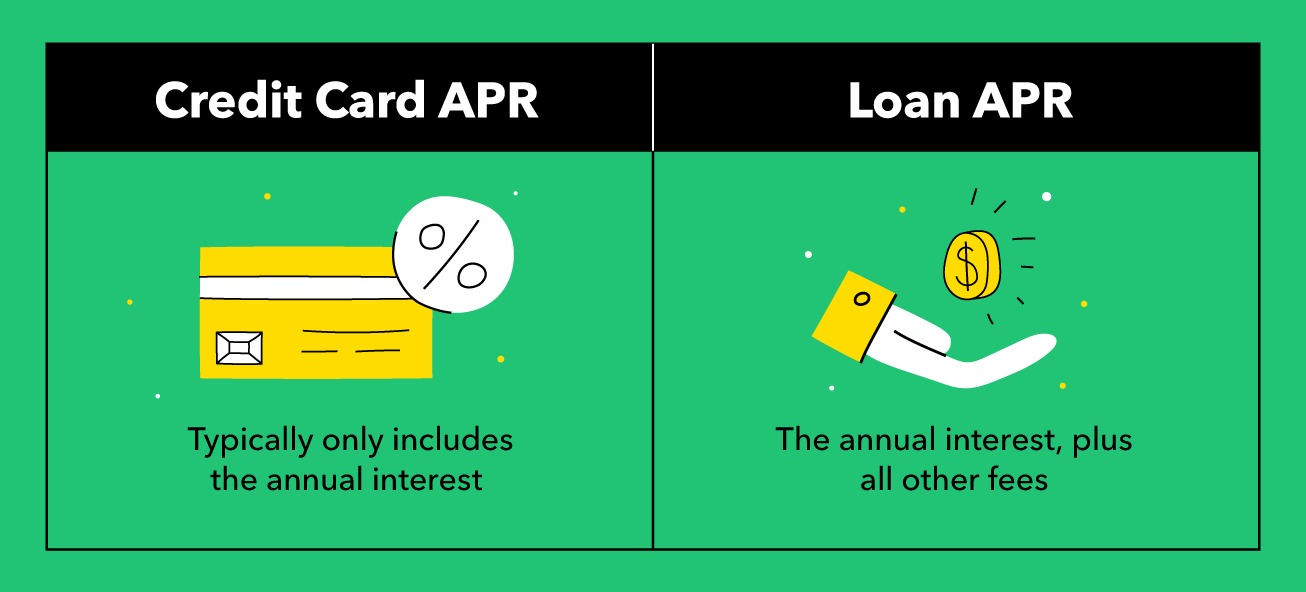

Purchase APR, an acronym for Purchase Annual Percentage Rate, is a critical factor that influences the cost of carrying a balance on a credit card. This annualized interest rate applies to the outstanding balances resulting from purchases made using the card. Unlike other types of APR, such as balance transfer APR or cash advance APR, the Purchase APR specifically pertains to the interest charged on purchases.

When a credit card user carries a balance on their card by not paying the full statement balance by the due date, the Purchase APR comes into play. This rate determines the additional amount, in the form of interest, that the cardholder must pay on the remaining balance. It is important to note that the Purchase APR can vary among different credit cards and is often influenced by factors such as the cardholder’s creditworthiness, prevailing market conditions, and the prime rate set by the Federal Reserve.

Furthermore, credit card companies typically offer a grace period during which cardholders can avoid paying interest on their purchases by paying the full statement balance by the due date. However, if the entire balance is not settled within this grace period, the Purchase APR becomes applicable to the remaining amount.

Understanding the nuances of Purchase APR is crucial for individuals who rely on credit cards for their day-to-day expenses or major purchases. It empowers cardholders to make informed decisions regarding their spending habits and repayment strategies, ultimately contributing to their overall financial well-being.

How Purchase APR is Calculated

The calculation of Purchase APR involves several factors that determine the amount of interest charged on outstanding balances resulting from credit card purchases. While the specific methodologies may vary slightly among credit card issuers, the fundamental principles underlying the calculation remain consistent.

Typically, credit card companies compute the Purchase APR by starting with the prime rate, which serves as the foundation for many variable interest rates, including those on credit cards. To this prime rate, the card issuer adds a margin, also known as the spread, which is determined based on the cardholder’s creditworthiness and other risk factors. The sum of the prime rate and the margin yields the cardholder’s Purchase APR.

It is important to note that some credit cards feature promotional or introductory APR offers, which may be 0% or significantly lower than the standard Purchase APR for a specified period. After the promotional period ends, the standard Purchase APR, based on the prime rate and the applicable margin, comes into effect.

Moreover, credit card companies utilize various billing methods, such as the average daily balance or the daily periodic rate, to calculate the interest accrued on outstanding balances. These methods determine the amount of interest charged based on the average balance carried over from the previous billing cycle, taking into account any new purchases and payments made during the current cycle.

Understanding the calculation of Purchase APR provides cardholders with insights into the factors influencing the interest charged on their credit card balances. By being aware of how the Purchase APR is derived, individuals can make informed decisions regarding their credit card usage and repayment strategies, thereby optimizing their financial management practices.

Impact of Purchase APR on Credit Card Users

The Purchase Annual Percentage Rate (APR) exerts a substantial impact on credit card users, influencing their financial obligations and overall cost of utilizing credit. Understanding the implications of Purchase APR is crucial for individuals seeking to effectively manage their credit card balances and minimize unnecessary interest expenses.

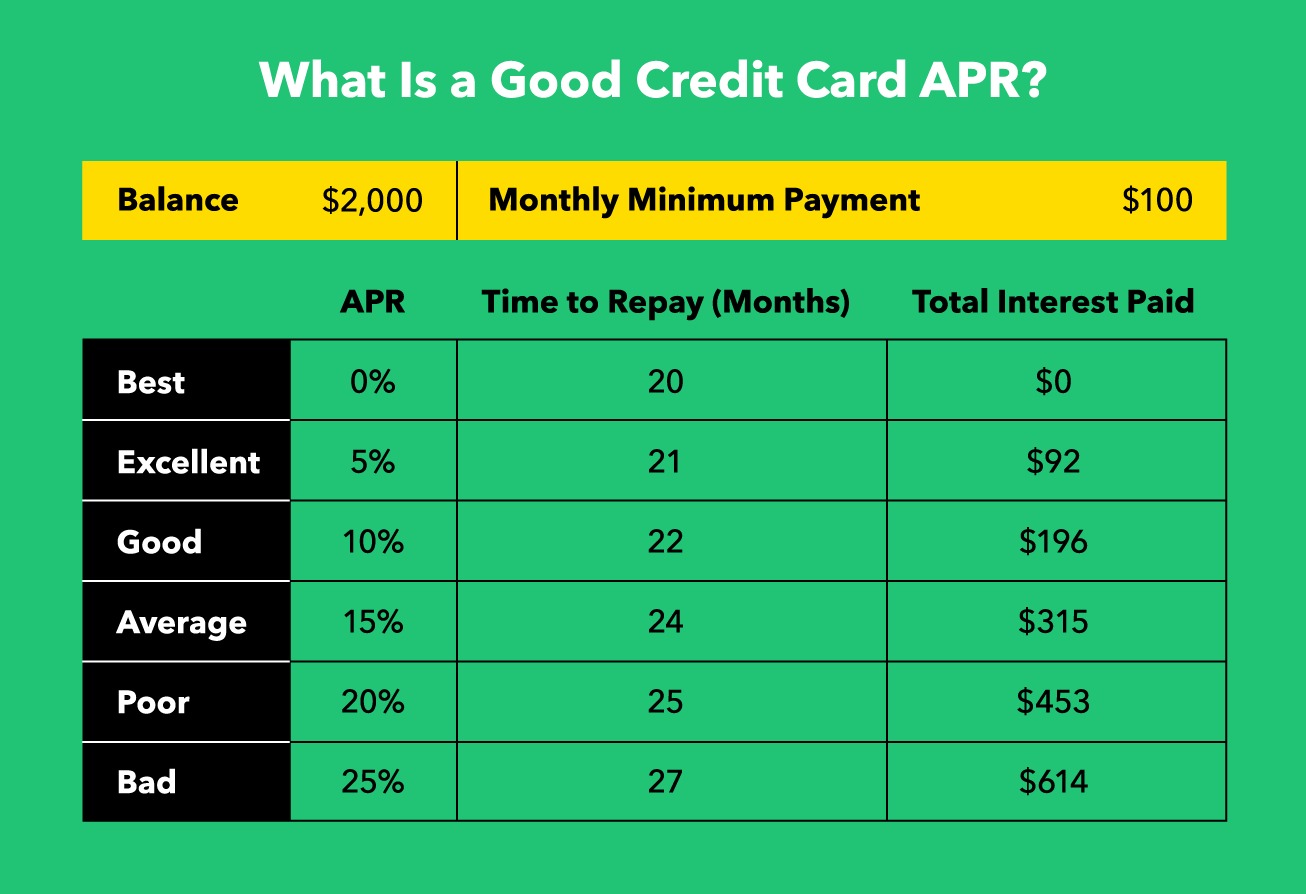

First and foremost, the Purchase APR directly affects the cost of carrying a balance on a credit card. When cardholders do not pay their full statement balance by the due date, the outstanding balance becomes subject to the Purchase APR, leading to the accrual of interest charges. Consequently, individuals carrying balances from month to month may find themselves incurring significant interest expenses, thereby increasing the overall cost of their purchases.

Moreover, the Purchase APR plays a pivotal role in determining the affordability of credit card financing for larger expenses, such as household appliances, electronics, or travel arrangements. Higher Purchase APRs can substantially elevate the total amount repaid for such purchases, making it imperative for consumers to evaluate the long-term financial implications of utilizing credit cards with elevated APRs for major transactions.

Furthermore, the impact of Purchase APR extends to individuals with multiple credit cards, as varying APRs across different accounts can complicate debt repayment strategies. Balances with higher APRs can lead to more significant interest accumulations, potentially impeding efforts to pay off debts efficiently and cost-effectively.

It is essential for credit card users to recognize the significance of the Purchase APR and its potential repercussions on their financial well-being. By comprehending the impact of this interest rate on their balances and overall cost of credit, individuals can make informed decisions regarding their spending habits, repayment priorities, and the selection of credit cards that align with their financial goals.

Managing Purchase APR on Credit Cards

Effectively managing the Purchase Annual Percentage Rate (APR) on credit cards is essential for minimizing interest expenses and maintaining sound financial health. By implementing strategic approaches and prudent financial habits, cardholders can navigate the realm of credit cards while mitigating the impact of Purchase APR on their overall financial well-being.

One of the most impactful strategies for managing Purchase APR is to prioritize timely and full payments of credit card balances. By settling the entire statement balance by the due date, cardholders can avoid incurring interest charges on their purchases, effectively circumventing the application of the Purchase APR.

Furthermore, individuals can explore the option of transferring balances from high-APR credit cards to those offering lower or 0% introductory APRs. Balance transfer offers can provide temporary relief from high interest expenses, allowing cardholders to consolidate their debts and focus on repaying them without the burden of exorbitant APRs.

Another effective approach involves negotiating with credit card issuers to secure lower APRs. Cardholders with strong payment histories and creditworthiness may be well-positioned to request reduced APRs from their card providers. Engaging in open and transparent communication with issuers can yield favorable outcomes, potentially leading to decreased Purchase APRs and enhanced affordability of credit card balances.

Additionally, individuals can proactively monitor their credit card statements and terms to stay informed about any changes in the Purchase APR. Being aware of fluctuations in the APR enables cardholders to adjust their financial strategies accordingly and explore alternative credit options if necessary.

Moreover, maintaining a healthy credit score through responsible credit utilization, timely payments, and prudent financial management can contribute to securing more favorable Purchase APRs on new credit card applications. A strong credit profile enhances the likelihood of accessing credit cards with lower APRs, thereby reducing the long-term cost of carrying balances.

By embracing these proactive measures and adopting disciplined financial practices, credit card users can effectively manage the impact of Purchase APR on their credit card balances, ultimately fostering greater financial stability and minimizing unnecessary interest expenses.

Conclusion

In conclusion, the Purchase Annual Percentage Rate (APR) on credit cards represents a pivotal element that significantly influences the cost of carrying balances and the overall affordability of credit for consumers. Understanding the intricacies of Purchase APR empowers individuals to make informed financial decisions, effectively manage their credit card balances, and minimize unnecessary interest expenses.

By comprehending the calculation methodology of Purchase APR and its implications, credit card users can navigate the complexities of credit card usage with greater confidence. The impact of Purchase APR extends beyond the immediate cost of purchases, influencing the long-term affordability of credit and the financial well-being of consumers.

Effective management of Purchase APR involves prioritizing timely payments, exploring balance transfer options, negotiating for lower APRs, and maintaining a healthy credit profile. These proactive strategies enable individuals to mitigate the impact of Purchase APR on their credit card balances, ultimately fostering sound financial management practices and minimizing the burden of interest expenses.

As individuals strive to optimize their financial health and make prudent credit card choices, the awareness and management of Purchase APR emerge as indispensable components of their financial toolkit. By embracing these principles and implementing strategic approaches, credit card users can harness the benefits of credit cards while minimizing the long-term costs associated with carrying balances and accruing interest charges.

In essence, a comprehensive understanding of Purchase APR empowers individuals to navigate the credit card landscape with astuteness, enabling them to leverage the benefits of credit while mitigating the financial implications of interest expenses. By embracing informed decision-making and proactive financial management, credit card users can effectively manage the impact of Purchase APR, fostering greater financial stability and long-term prosperity.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance