Home>Finance>What Is The Balance Transfer Fee For A Credit Card

Finance

What Is The Balance Transfer Fee For A Credit Card

Published: February 18, 2024

Learn about the balance transfer fee for credit cards and how it impacts your finances. Discover ways to minimize costs and manage your finances effectively.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

In the realm of personal finance, the concept of balance transfer fees holds significant relevance for individuals seeking to manage their credit card debt effectively. When considering the utilization of balance transfer options, understanding the associated fees is crucial for making informed decisions. This article aims to demystify the intricacies of balance transfer fees, offering comprehensive insights into their calculation, influencing factors, and strategies for minimizing their impact.

By delving into the fundamental aspects of balance transfer fees, readers will gain a deeper understanding of this financial mechanism and its implications. Whether you're a seasoned credit card user or someone exploring debt management solutions, the knowledge gleaned from this article will empower you to navigate the realm of balance transfer fees with confidence and clarity.

Through an exploration of the calculation methods, influencing variables, and comparative analysis of balance transfer fees, readers will be equipped to make informed decisions tailored to their financial circumstances. Furthermore, practical tips for minimizing balance transfer fees will be provided, offering actionable strategies for optimizing the benefits of this financial tool while mitigating associated costs.

Join us on this enlightening journey as we unravel the intricacies of balance transfer fees, empowering you to make sound financial choices and embark on a path towards enhanced fiscal well-being.

Understanding Balance Transfer Fees

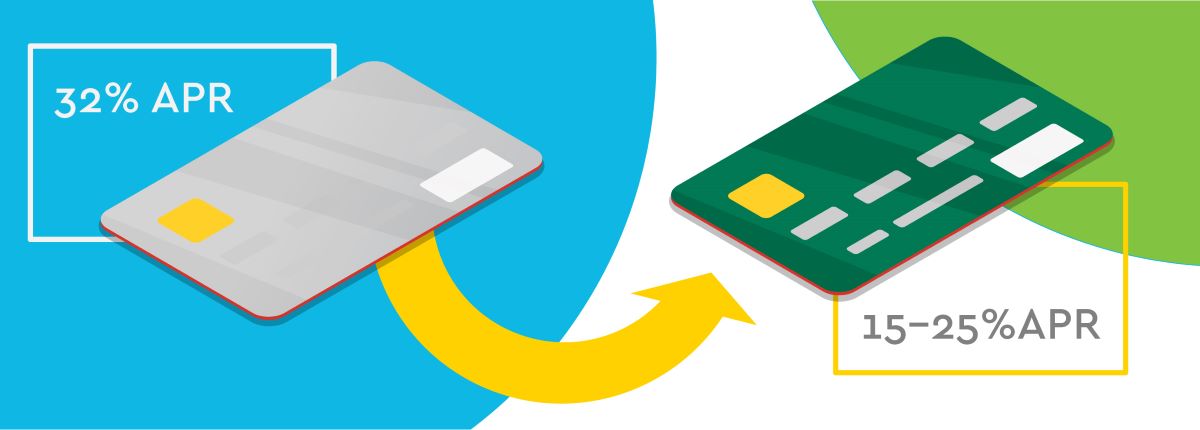

Balance transfer fees are a vital aspect of credit card management, particularly for individuals seeking to consolidate and manage their outstanding card balances effectively. When transferring a balance from one credit card to another, a balance transfer fee is typically charged by the receiving card issuer. This fee is usually calculated as a percentage of the transferred amount, often ranging from 3% to 5% of the total sum.

It’s essential to comprehend that balance transfer fees are separate from the interest rates applied to the transferred balance. While the interest rate dictates the cost of carrying a balance on the card, the balance transfer fee is an upfront cost incurred at the time of the transfer. As such, individuals evaluating the feasibility of a balance transfer should consider both the transfer fee and the ongoing interest rates to assess the overall cost implications.

Moreover, understanding the specific terms and conditions associated with balance transfer fees is imperative. Some credit card issuers may offer promotional periods with reduced or waived transfer fees, providing an opportunity for individuals to optimize their debt management strategies. By familiarizing oneself with the nuances of balance transfer fees, cardholders can make informed decisions aligned with their financial objectives.

By comprehending the role of balance transfer fees in the broader context of credit card management, individuals can harness this financial tool effectively to streamline their debt repayment process. This understanding empowers cardholders to navigate the intricacies of balance transfers with confidence, enabling them to make informed choices that align with their long-term financial well-being.

How Balance Transfer Fees Are Calculated

Balance transfer fees are typically calculated as a percentage of the total amount being transferred from one credit card to another. The exact percentage varies among card issuers but commonly ranges from 3% to 5% of the transferred sum. For example, if an individual transfers $5,000 from one card to another and the balance transfer fee is 3%, the fee incurred would amount to $150.

It’s important to note that the balance transfer fee is applied at the time of the transfer, meaning it is added to the total amount being transferred. As a result, the fee contributes to the overall balance that will be subject to the applicable interest rates. This upfront cost should be factored into the decision-making process when evaluating the feasibility of a balance transfer as a debt management strategy.

Furthermore, some credit card issuers may impose a minimum fee threshold for balance transfers, ensuring that the fee meets a predetermined minimum amount regardless of the transferred sum. Understanding these calculation methodologies is crucial for individuals considering the utilization of balance transfers to consolidate and manage their credit card debt effectively.

By gaining insights into the calculation of balance transfer fees, individuals can make informed assessments of the associated costs and weigh them against the potential benefits of consolidating their card balances. This knowledge empowers cardholders to approach balance transfers strategically, leveraging this financial tool to optimize their debt repayment journey while minimizing unnecessary expenses.

Factors that Affect Balance Transfer Fees

Several factors influence the magnitude of balance transfer fees, shaping the cost implications for individuals seeking to consolidate their credit card debt. Understanding these determinants is pivotal for evaluating the feasibility of a balance transfer and making informed financial decisions.

1. Credit Card Issuer Policies: Different credit card issuers may impose varying balance transfer fee structures, with some offering promotional periods featuring reduced or waived fees. It’s essential for individuals to familiarize themselves with the specific policies of their card issuer to leverage potential cost-saving opportunities.

2. Transferred Amount: The total sum being transferred directly impacts the balance transfer fee, as it is typically calculated as a percentage of the transferred amount. Consequently, larger transfers incur higher fees, influencing the overall cost-effectiveness of the consolidation strategy.

3. Minimum Fee Thresholds: Some card issuers enforce minimum fee thresholds for balance transfers, ensuring that the fee meets a predetermined minimum amount regardless of the transferred sum. This policy can affect the fee calculations, particularly for smaller transfer amounts.

4. Creditworthiness: The creditworthiness of the individual initiating the balance transfer can also influence the fee structure. Those with stronger credit profiles may be eligible for more favorable terms, potentially including lower balance transfer fees.

5. Market Conditions: External market dynamics and industry trends can impact balance transfer fee offerings by card issuers. During certain periods, promotional incentives or competitive pressures within the credit card landscape may lead to fluctuations in fee structures.

By recognizing the multifaceted factors that shape balance transfer fees, individuals can make informed assessments of the associated costs and optimize their debt management strategies accordingly. This comprehensive understanding empowers cardholders to navigate the intricacies of balance transfer fees strategically, aligning their financial decisions with their overarching goals of debt consolidation and fiscal prudence.

Comparing Balance Transfer Fees

When considering a balance transfer as a means of consolidating credit card debt, comparing the balance transfer fees across different card issuers is instrumental in identifying the most cost-effective and advantageous options. By conducting a thorough comparison, individuals can discern the fee structures, promotional offerings, and potential savings associated with various credit cards, enabling them to make informed decisions aligned with their financial objectives.

Key aspects to consider when comparing balance transfer fees include:

- Fee Percentage: Evaluate the percentage charged for balance transfers by different card issuers. While the industry standard often ranges from 3% to 5%, variations in this percentage can significantly impact the overall cost of transferring balances.

- Promotional Periods: Some credit card issuers may feature promotional periods during which they offer reduced or waived balance transfer fees. Assessing the availability and duration of such promotions is crucial for maximizing potential savings.

- Minimum Fee Thresholds: Understand the existence of minimum fee thresholds, as these can influence the fee calculations, particularly for smaller transfer amounts. Comparing these thresholds across different cards provides insights into the cost implications for varying transfer sums.

- Additional Benefits: Beyond the fee structure, consider the supplementary benefits offered by different credit cards, such as rewards programs, cashback incentives, or low ongoing interest rates. These perks contribute to the overall value proposition of the card and should be factored into the comparison.

By meticulously comparing balance transfer fees and associated terms across multiple credit card offerings, individuals can identify the most advantageous options tailored to their specific financial circumstances. This discerning approach empowers individuals to leverage the potential cost savings and benefits inherent in strategic balance transfers, optimizing their debt management endeavors while minimizing unnecessary expenses.

Tips for Minimizing Balance Transfer Fees

Maximizing the benefits of a balance transfer while minimizing associated fees requires a strategic approach and careful consideration of various factors. By implementing the following tips, individuals can optimize their debt management strategies and reduce the impact of balance transfer fees:

- Seek Promotional Offers: Explore credit card issuers’ promotional periods that feature reduced or waived balance transfer fees. Capitalizing on these offers can lead to substantial cost savings, making the consolidation process more financially favorable.

- Compare Fee Structures: Conduct a comprehensive comparison of balance transfer fees across different credit card issuers. By identifying cards with lower fee percentages or attractive promotional terms, individuals can select the most cost-effective options.

- Consider Minimum Fee Thresholds: Be mindful of minimum fee thresholds imposed by card issuers. If planning to transfer a smaller balance, opt for a card with a lower or waived minimum fee threshold to minimize upfront costs.

- Factor in Ongoing Interest Rates: While focusing on balance transfer fees, also assess the ongoing interest rates of the target credit cards. A lower interest rate can offset the impact of a higher balance transfer fee over time, enhancing the overall cost-effectiveness of the transfer.

- Utilize Rewards and Incentives: Select a credit card that offers rewards programs or cashback incentives, effectively offsetting the balance transfer fee with accrued benefits over time. This approach maximizes the card’s long-term value proposition.

- Opt for Shorter Repayment Periods: If feasible, aim to repay the transferred balance within a shorter timeframe. By minimizing the duration over which interest accrues on the transferred amount, individuals can mitigate the impact of the balance transfer fee.

- Maintain Good Credit Standing: Upholding a strong credit profile can position individuals to qualify for more favorable balance transfer terms, including lower fees. Responsible credit management and timely payments contribute to a positive credit standing, potentially unlocking cost-saving opportunities.

By integrating these tips into their debt management approach, individuals can navigate the realm of balance transfers with astuteness and financial prudence. This proactive stance enables them to capitalize on potential cost savings, optimize the consolidation process, and embark on a path towards enhanced fiscal well-being.

Conclusion

As we conclude our exploration of balance transfer fees, it becomes evident that these charges play a pivotal role in the realm of credit card debt management. Understanding the intricacies of balance transfer fees empowers individuals to make informed decisions that align with their financial goals, optimizing the potential benefits while mitigating unnecessary expenses.

By delving into the calculation methods, influencing factors, and strategies for minimizing balance transfer fees, we have equipped readers with the knowledge to navigate this financial landscape astutely. The comprehension of fee structures, promotional offerings, and cost-saving opportunities enables individuals to approach balance transfers strategically, leveraging this tool to streamline their debt repayment journey.

Furthermore, the comparative analysis of balance transfer fees across different credit card issuers underscores the importance of discerning assessment. By meticulously evaluating fee percentages, promotional terms, and supplementary benefits, individuals can identify the most advantageous options tailored to their specific financial circumstances.

It is essential to underscore the proactive measures that individuals can undertake to minimize balance transfer fees, such as seeking promotional offers, comparing fee structures, and leveraging rewards programs to offset costs. These strategic approaches empower individuals to optimize their debt management strategies and embark on a path towards enhanced fiscal well-being.

Ultimately, the knowledge gleaned from this exploration serves as a beacon of financial empowerment, guiding individuals towards prudent and informed decisions in their pursuit of effective credit card debt consolidation. By integrating these insights into their financial endeavors, individuals can harness the potential of balance transfers as a strategic tool for achieving greater financial stability and freedom.

As we part ways, armed with a deeper understanding of balance transfer fees, let us embark on our respective financial journeys with confidence, clarity, and a steadfast commitment to fiscal well-being.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance