Home>Finance>What Is The Difference Between Whole Life And Universal Life Insurance?

Finance

What Is The Difference Between Whole Life And Universal Life Insurance?

Published: October 15, 2023

Explore the difference between whole life and universal life insurance and make informed financial decisions. Protect your future with the right insurance policy.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Overview of Whole Life Insurance

- Features and Benefits of Whole Life Insurance

- Comparison of Whole Life and Universal Life Insurance

- Overview of Universal Life Insurance

- Features and Benefits of Universal Life Insurance

- Key Differences Between Whole Life and Universal Life Insurance

- Factors to Consider When Choosing Between Whole Life and Universal Life Insurance

- Conclusion

Introduction

Life insurance is an essential financial product that provides financial protection to individuals and their loved ones. It serves as a safety net, offering coverage in the event of an untimely death. There are various types of life insurance policies available, each offering different benefits and features.

In this article, we will focus on two popular options: whole life insurance and universal life insurance. While both types of policies offer lifelong coverage, they differ in terms of flexibility, premium payments, cash value accumulation, and death benefit options.

Understanding the differences between whole life insurance and universal life insurance is crucial for individuals looking to make an informed decision when choosing the right policy for their needs.

In this comprehensive guide, we will take a closer look at the features, benefits, and key differences between whole life insurance and universal life insurance. By the end of this article, you will have a clear understanding of these two types of policies, enabling you to make an informed decision about which one is the best fit for your financial goals and circumstances.

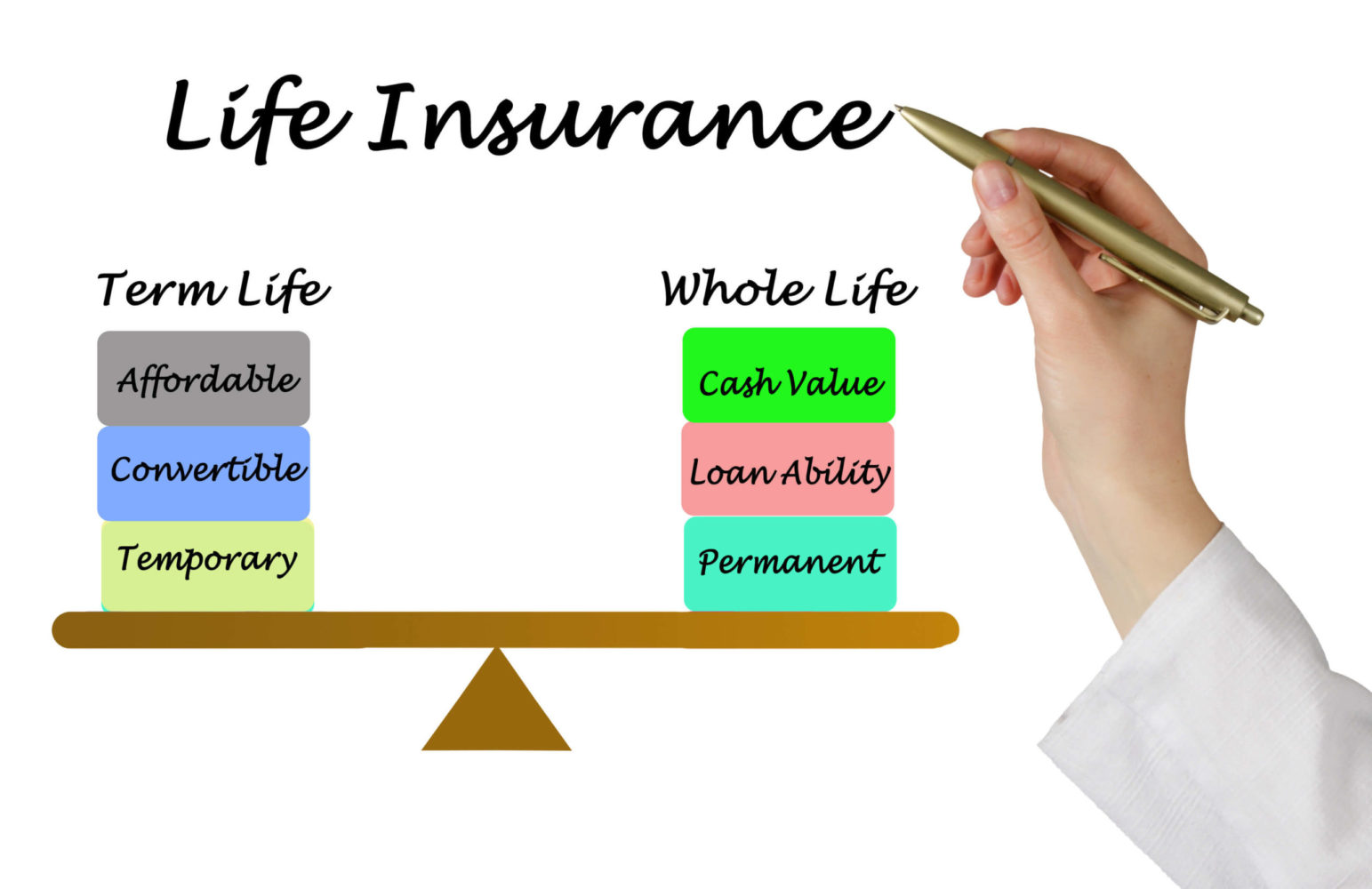

Overview of Whole Life Insurance

Whole life insurance is a type of permanent life insurance policy that provides coverage for the entire duration of the insured’s life. It offers guaranteed death benefit protection, meaning that the beneficiaries of the policy will receive a payout upon the insured’s death, regardless of when it occurs. In addition to the death benefit, whole life insurance also builds cash value over time, which can be accessed or borrowed against during the insured’s lifetime.

One of the key features of whole life insurance is its fixed premium payments. With whole life insurance, the premium amount is set at the time the policy is purchased and remains unchanged for the entire life of the policy. This provides stability and predictability as the policyholder knows exactly how much they need to pay each year.

Another important aspect of whole life insurance is the cash value accumulation. A portion of each premium payment is allocated towards the cash value component of the policy. Over time, the cash value grows tax-deferred and can be accessed by the policyholder through policy loans or withdrawals. The ability to tap into the cash value can provide financial flexibility for various needs, such as paying for education expenses or supplementing retirement income.

Whole life insurance also offers several additional benefits. It provides a death benefit that is typically income tax-free for the beneficiaries, which can help protect loved ones from financial hardship in the event of the insured’s passing. Some whole life policies also offer the ability to receive dividends, which can be used to reduce premiums, increase the death benefit, or accumulate additional cash value.

Overall, whole life insurance combines lifelong coverage with the potential for cash value accumulation and additional benefits. It is a suitable option for individuals who value the security of a guaranteed death benefit, stable premiums, and the potential for cash value growth.

Features and Benefits of Whole Life Insurance

Whole life insurance offers a range of features and benefits that make it an attractive option for many individuals seeking lifelong coverage and financial security.

1. Lifelong Coverage: One of the primary advantages of whole life insurance is that it provides coverage for the entire duration of the insured’s life. As long as the premiums are paid, the policy remains in force, ensuring that the beneficiaries will receive a death benefit whenever the insured passes away.

2. Fixed Premiums: Whole life insurance policies generally have fixed premium payments. This means that the premium amount is determined at the time of purchase and remains unchanged throughout the life of the policy. Having consistent premiums provides predictability and makes it easier to budget for insurance expenses.

3. Cash Value Accumulation: Whole life insurance builds cash value over time. A portion of each premium payment is allocated towards the cash value component of the policy. The cash value grows tax-deferred, meaning that it is not subject to income tax until it is accessed. Policyholders can borrow against the cash value or use it to supplement their retirement income or meet other financial needs.

4. Guaranteed Death Benefit: Whole life insurance guarantees a death benefit payout to the beneficiaries upon the insured’s passing. This ensures financial protection for loved ones, providing them with a tax-free lump sum of money. The death benefit can be used to cover funeral expenses, pay off debts, replace lost income, or fulfill any other financial obligations.

5. Dividend Payments: Some whole life insurance policies are eligible to receive dividends from the insurance company. Dividends are typically distributed when the insurer performs better than expected or experiences lower mortality rates. Policyholders have the choice to either take the dividends as cash, use them to reduce premiums, increase the death benefit, or grow the cash value.

6. Estate Planning: Whole life insurance can be a useful tool for estate planning purposes. By naming a beneficiary, the policy proceeds can be passed directly to the intended recipient without going through probate, which can save time and reduce estate settlement costs.

In summary, whole life insurance offers lifelong coverage, guaranteed death benefit protection, tax-deferred cash value accumulation, and additional benefits such as dividends. These features make whole life insurance a popular choice for individuals looking for a long-term financial safety net and potential cash value growth.

Comparison of Whole Life and Universal Life Insurance

While both whole life insurance and universal life insurance offer lifelong coverage, they differ in several key aspects. Understanding these differences is crucial in choosing the right policy that aligns with your financial goals and priorities. Let’s compare the two.

Premium Payments: Whole life insurance policies typically have fixed premiums, meaning the premium amount remains the same throughout the life of the policy. In contrast, universal life insurance policies offer more flexibility when it comes to premium payments. Policyholders have the option to adjust their premium amount or even skip payments, as long as there is sufficient cash value to cover the policy expenses.

Cash Value Accumulation: Both whole life insurance and universal life insurance build cash value over time. However, universal life insurance policies offer greater flexibility in terms of cash value growth. Policyholders can choose between a fixed interest rate or a variable interest rate tied to specific investment options. This flexibility allows for potentially higher cash value accumulation in universal life insurance compared to whole life insurance.

Death Benefit Options: Whole life insurance policies offer a guaranteed death benefit, meaning the beneficiaries will receive a predetermined amount upon the insured’s death. Universal life insurance policies, on the other hand, provide more flexibility with death benefit options. Policyholders can choose to increase or decrease the death benefit amount, as well as adjust the timing of when the death benefit is paid out, subject to policy terms and conditions.

Flexibility: Universal life insurance offers more flexibility than whole life insurance. In addition to premium flexibility and death benefit options, universal life insurance policies also generally allow for adjustments to the policy coverage and face amount over time. This can be advantageous for individuals whose financial circumstances change or have specific needs that may require modifications to their insurance coverage.

Investment Component: One notable difference between whole life insurance and universal life insurance is the presence of an investment component. Universal life insurance often includes an investment element, which allows policyholders to allocate a portion of their premium towards investment vehicles, such as stocks, bonds, or mutual funds. This potential for higher returns comes with increased risk and requires careful monitoring of the investment performance.

In summary, while both whole life insurance and universal life insurance offer lifelong coverage, they differ in terms of premium payments, cash value accumulation, death benefit options, flexibility, and the inclusion of an investment component. Understanding these differences is crucial in selecting the right policy that aligns with your financial objectives.

Overview of Universal Life Insurance

Universal life insurance is a type of permanent life insurance that provides lifelong coverage while offering more flexibility than traditional whole life insurance. This type of policy consists of two main components: a death benefit and a cash value component that grows over time.

One of the key features of universal life insurance is its flexibility in premium payments. Policyholders have the option to adjust the amount and timing of premium payments, as long as there is sufficient cash value in the policy to cover insurance costs. This allows individuals to tailor their premium payments to their financial situation or adjust payments during times of financial hardship.

Like whole life insurance, universal life insurance also accumulates cash value over time. A portion of each premium payment is allocated to the cash value component of the policy, which grows on a tax-deferred basis. The cash value can be accessed by the policyholder through withdrawals or policy loans and can be used to supplement income, fund education expenses, or meet other financial needs.

Universal life insurance also offers flexibility in terms of death benefits. Policyholders have the ability to adjust the death benefit amount as well as the timing of when the death benefit will be paid out. This flexibility can be beneficial for individuals who want the option to decrease or increase the death benefit based on their changing financial circumstances or beneficiary needs.

Another notable feature of universal life insurance is the presence of an investment component. Policyholders can allocate a portion of their premium payments to different investment options, such as stocks, bonds, or mutual funds. This gives individuals the opportunity to potentially earn higher returns on their cash value, although it also carries a higher level of risk compared to traditional whole life insurance.

Overall, universal life insurance provides a combination of lifelong coverage, flexible premium payments, cash value accumulation, and the potential for higher investment returns. This type of policy is suitable for individuals who value flexibility in premium payments, the ability to adjust the death benefit, and the potential for cash value growth through investment opportunities.

Features and Benefits of Universal Life Insurance

Universal life insurance offers several features and benefits that set it apart from other types of life insurance policies. Let’s explore some of the key features and advantages of universal life insurance:

1. Flexibility in Premium Payments: Universal life insurance provides flexibility when it comes to premium payments. Policyholders have the option to adjust the amount and timing of their premium payments, as long as there is sufficient cash value in the policy to cover the insurance costs. This flexibility makes it easier to adapt the policy to changes in financial circumstances or budget constraints.

2. Cash Value Accumulation: Similar to other permanent life insurance policies, universal life insurance accumulates cash value over time. A portion of each premium payment is allocated towards the cash value component, which grows on a tax-deferred basis. The policyholder can access the cash value through withdrawals or policy loans, providing a source of funds that can be used for various financial needs.

3. Adjustable Death Benefit: Universal life insurance allows policyholders to adjust the death benefit amount. This flexibility can be particularly useful during major life events like marriage, the birth of a child, or changes in financial circumstances. The ability to increase or decrease the death benefit ensures that the policy aligns with the policyholder’s changing needs and priorities.

4. Investment Component: Universal life insurance often includes an investment component, allowing policyholders to allocate a portion of their premium towards various investment options. This feature provides potential for higher returns on the cash value, as it can be invested in stocks, bonds, or mutual funds. However, it’s important to note that investment performance is not guaranteed and carries inherent risks.

5. Potential for Tax Advantages: Universal life insurance offers potential tax advantages. The cash value growth is tax-deferred, meaning that policyholders are not required to pay taxes on the growth until they withdraw funds from the policy. Additionally, the death benefit is generally received tax-free by the beneficiaries, providing a financial safety net without incurring income tax obligations.

6. Estate Planning Tool: Universal life insurance can be an effective tool for estate planning. By naming a beneficiary, the policy proceeds can bypass probate, providing a seamless transfer of assets to the intended recipient. This can help simplify the estate settlement process and potentially reduce estate taxes.

In summary, universal life insurance offers flexibility in premium payments, cash value accumulation, adjustable death benefits, potential for investment growth, tax advantages, and estate planning benefits. These features make it a versatile and customizable option for individuals seeking lifelong coverage and financial security.

Key Differences Between Whole Life and Universal Life Insurance

While both whole life insurance and universal life insurance offer permanent coverage, there are several key differences between these two types of policies. Understanding these differences is crucial in choosing the right insurance option that aligns with your financial goals and priorities. Let’s explore the key distinctions:

Premium Payments: Whole life insurance policies typically have fixed premiums that remain constant throughout the life of the policy. In contrast, universal life insurance offers more flexibility in premium payments. Policyholders can adjust their premium amounts or even skip payments, as long as there is sufficient cash value to cover the policy’s expenses.

Cash Value Accumulation: Both whole life insurance and universal life insurance build cash value over time. However, the way in which cash value accumulates differs between the two. Whole life insurance policies have a predetermined cash value growth rate set by the insurance company. On the other hand, universal life insurance policies often have a variable interest rate tied to specific investment options, allowing for potentially higher cash value growth.

Death Benefit Options: Whole life insurance policies offer a guaranteed death benefit payout to beneficiaries upon the insured’s death. Universal life insurance provides more flexibility in terms of death benefit options. Policyholders can adjust the death benefit amount as well as the timing of when the death benefit will be paid out, subject to policy terms and conditions.

Flexibility: Universal life insurance offers greater flexibility compared to whole life insurance. In addition to premium flexibility and death benefit options, universal life insurance policies may allow policyholders to make changes to the coverage amount or face value. This flexibility can be advantageous for individuals whose financial circumstances change or have specific needs that require adjustments to their insurance coverage.

Investment Component: One key difference between whole life insurance and universal life insurance is the presence of an investment component in universal life insurance. Universal life policies often offer investment options that allow policyholders to allocate a portion of their premiums towards investments such as stocks, bonds, or mutual funds. This introduces the potential for higher cash value growth, but it also carries higher risk and requires active management.

Level of Risk: Whole life insurance offers a more conservative and predictable approach with fixed premiums and guaranteed cash value growth. Universal life insurance, particularly those with investment options, carries more risk due to the potential volatility of the underlying investments. Policyholders must carefully monitor and manage their investments to ensure they align with their risk tolerance and financial objectives.

It is important to consider these factors when choosing between whole life insurance and universal life insurance. The decision should be based on your individual needs, risk tolerance, and long-term financial goals.

Factors to Consider When Choosing Between Whole Life and Universal Life Insurance

Choosing between whole life insurance and universal life insurance requires careful consideration of several factors. The decision should be based on your individual financial goals, risk tolerance, and specific needs. Here are some key factors to consider when making this important decision:

1. Premium Payments: Evaluate your ability to consistently pay premiums. If you prefer a fixed premium that remains the same throughout the life of the policy, whole life insurance may be the better choice. Conversely, if you desire flexibility in premium payments, such as adjusting the premium amount or skipping payments when necessary, universal life insurance may be more suitable.

2. Cash Value Growth: Assess your preferences for cash value accumulation. Whole life insurance provides guaranteed cash value growth, while universal life insurance offers potentially higher growth through variable interest rates and investment options. Consider your risk tolerance and investment knowledge when deciding which approach aligns with your financial objectives.

3. Death Benefit Options: Determine the flexibility you require for death benefit options. Whole life insurance offers a fixed death benefit payout, whereas universal life insurance allows policyholders to adjust the death benefit amount and the timing of when beneficiaries receive the payout. Consider the financial needs of your beneficiaries and potential changes in circumstances over time.

4. Flexibility: Consider your need for policy flexibility. If you anticipate changes in your financial situation, such as fluctuating income or the need for adjustments in coverage, universal life insurance may be the better option due to its flexibility in premium payments, death benefit options, and potential changes to the coverage amount or face value.

5. Risk Appetite: Evaluate your risk tolerance. Whole life insurance offers a conservative approach with guaranteed cash value growth and fixed premiums. In contrast, universal life insurance introduces an investment component that carries higher risk but also the potential for higher cash value growth. Assess your ability and willingness to actively manage investments or prefer a more stable and predictable approach.

6. Long-Term Needs: Consider your long-term financial goals and needs. Determine if you require lifelong coverage, cash value accumulation, and potential access to policy funds for supplemental income or specific financial goals. Assess if you have any estate planning considerations, such as bypassing probate or tax-efficient wealth transfer, which may influence your decision between whole life insurance and universal life insurance.

Ultimately, the choice between whole life insurance and universal life insurance depends on your individual circumstances and financial objectives. It is advisable to discuss your specific needs with a qualified insurance professional to ensure you make an informed decision that aligns with your long-term financial goals and provides the necessary financial protection for you and your loved ones.

Conclusion

Choosing the right life insurance policy is a critical decision that deserves careful consideration. Both whole life insurance and universal life insurance offer lifelong coverage, cash value accumulation, and financial protection for your loved ones. The key is to understand the differences between the two and assess which one aligns best with your specific needs and goals.

Whole life insurance provides stability with fixed premiums, guaranteed cash value growth, and a predetermined death benefit. It is an excellent option for individuals seeking lifelong coverage and a conservative approach to cash value accumulation.

On the other hand, universal life insurance offers greater flexibility in premium payments, adjustable death benefit options, and the potential for higher cash value growth through investments. This type of policy suits individuals who value premium payment flexibility, the ability to adjust the death benefit, and the opportunity for greater cash value accumulation.

When making your decision, consider factors such as your risk tolerance, financial goals, and long-term needs. Evaluate your ability to consistently pay premiums and whether you would benefit from premium payment flexibility. Assess your comfort level with investment risk and your desire for potentially higher cash value growth. Also, consider your preferences for death benefit options and the flexibility to modify your coverage in the future.

To make an informed decision, consult with a trusted insurance professional who can guide you through the options, provide personalized advice, and help you choose the policy that fits your unique circumstances.

Remember, life insurance is an essential part of your overall financial plan. It offers protection and peace of mind to you and your loved ones. By carefully considering the features, benefits, and differences between whole life insurance and universal life insurance, you can select the policy that best meets your needs and provides financial security for the long term.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance