Home>Finance>What Is A Modified Whole Life Insurance Policy?

Finance

What Is A Modified Whole Life Insurance Policy?

Published: October 16, 2023

Learn about modified whole life insurance policies and how they can benefit your financial security. Find out what makes them different from traditional policies in this comprehensive guide

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Insurance plays a crucial role in protecting individuals and their loved ones from unexpected financial hardships. One type of insurance that offers long-term coverage and a cash value component is whole life insurance. Whole life insurance provides a death benefit to beneficiaries upon the policyholder’s demise, ensuring financial security even in the face of unfortunate circumstances.

However, within the realm of whole life insurance, there are different variations and options to choose from. One such option is a modified whole life insurance policy, which offers a unique set of features and benefits.

In this article, we will explore the concept of modified whole life insurance and delve into its features, benefits, and drawbacks. We will also discuss the factors that individuals should consider when deciding whether a modified whole life insurance policy is the right fit for their financial needs and goals.

So, whether you’re a seasoned insurance shopper looking to gain a deeper understanding of modified whole life insurance, or a first-time buyer exploring your options, read on to discover what makes this type of policy stand out from the crowd.

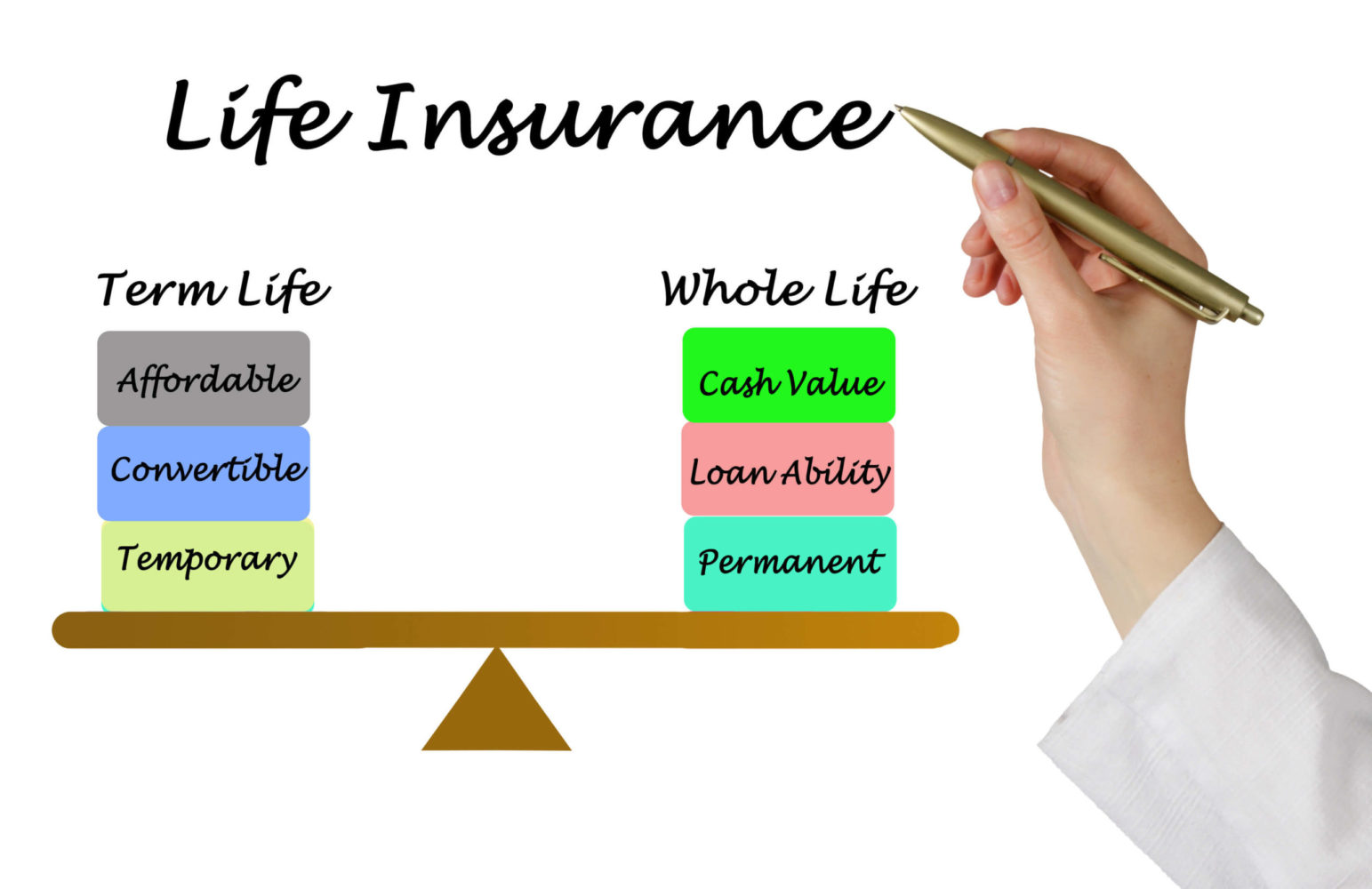

Definition of Whole Life Insurance

Before diving into the specifics of modified whole life insurance, it’s important to have a solid understanding of what whole life insurance is. Whole life insurance is a type of permanent life insurance that provides coverage for the entirety of the policyholder’s life, as long as premiums are paid up to date.

One defining characteristic of whole life insurance is the cash value component. As the policyholder pays their premiums, a portion of the payment goes towards the death benefit, while the remaining amount is allocated to the cash value account. This cash value grows over time and can be accessed by the policyholder through policy loans or withdrawals.

One of the key advantages of whole life insurance is the guarantee of a death benefit payout to the policy’s beneficiaries. This payout can provide financial security to loved ones and help cover expenses such as funeral costs, outstanding debts, and even income replacement.

Additionally, whole life insurance policies often come with a level premium, meaning that the premium amount remains constant throughout the life of the policy. This can provide peace of mind for policyholders, as they can budget their expenses without worrying about increasing premiums as they age.

It’s important to note that while whole life insurance offers lifetime coverage, it tends to have higher premiums compared to other types of life insurance, such as term life insurance. This is due to the cash value component and the guarantee of a death benefit payout.

Now that we have a clear understanding of what whole life insurance entails, let’s take a closer look at modified whole life insurance and how it differs from traditional whole life policies.

Understanding Modified Whole Life Insurance

Modified whole life insurance is a variation of traditional whole life insurance that offers some flexibility in premium payments and coverage. This type of policy is designed to accommodate individuals who may have fluctuating income or specific financial needs at different stages of their lives.

With modified whole life insurance, the policyholder has the option to pay lower premiums during the initial years of the policy. These lower premiums, also known as “modified” premiums, are typically set for a specific period, often the first five to ten years. After this initial period, the premium amount increases to a higher level, which remains fixed for the rest of the policy’s duration.

During the modified premium period, the death benefit of the policy may be lower than what is typically offered with traditional whole life insurance. However, once the policy transitions to the higher premium payments, the death benefit returns to the full amount initially agreed upon.

This flexibility in premium payments can be beneficial for individuals who may have temporary financial constraints but expect their income to increase in the future. It allows them to secure life insurance coverage while managing their current budget effectively.

In addition to flexible premiums, modified whole life insurance policies also offer the same cash value component as traditional whole life insurance. The cash value grows over time and can be accessed by the policyholder, providing a source of funds that can be used for various purposes such as emergencies, education expenses, or supplementing retirement income.

It’s important to note that modified whole life insurance policies may have specific guidelines and rules regarding the payment periods, premium amounts, and death benefit adjustments in different stages of the policy. Policyholders should thoroughly review the terms and conditions of the policy before making a decision.

Now that we have a grasp on the concept of modified whole life insurance, let’s explore some of the features and benefits that make this type of policy appealing to certain individuals.

Features and Benefits of Modified Whole Life Insurance

Modified whole life insurance offers several features and benefits that make it an enticing option for individuals seeking life insurance coverage. Let’s take a closer look at some of the key advantages of this type of policy:

1. Flexibility in Premium Payments: One of the primary benefits of modified whole life insurance is the flexibility it offers in premium payments. During the initial years, policyholders have the option to pay lower premiums, which can be especially helpful when facing financial constraints. This allows individuals to secure life insurance coverage while managing their current budget effectively.

2. Cash Value Growth: Like traditional whole life insurance, modified whole life insurance policies accumulate a cash value over time. This cash value grows on a tax-deferred basis and can be accessed by policyholders through policy loans or withdrawals. This feature provides individuals with a source of funds that can be used for emergencies, education expenses, or supplementing retirement income.

3. Guaranteed Death Benefit: Modified whole life insurance policies provide a guaranteed death benefit to the policy’s beneficiaries upon the policyholder’s demise. This assurance ensures that loved ones will receive a financial payout, offering peace of mind and financial protection during difficult times.

4. Lifetime Coverage: As with traditional whole life insurance, modified whole life insurance provides coverage for the entirety of the policyholder’s life, as long as premium payments are made as agreed. This ensures that individuals have consistent life insurance protection throughout their lifetime.

5. Potential Dividends: Some modified whole life insurance policies may participate in dividend payments. Dividends are a share of the insurance company’s profits and can be used to increase the cash value of the policy, enhance the death benefit, or even reduce future premium payments.

It’s important to note that the specific features and benefits can vary depending on the insurance company and policy terms. Individuals should carefully review the policy details and consult with an insurance professional to fully understand the benefits and limitations of a particular modified whole life insurance policy.

Now that we have explored the features and benefits of modified whole life insurance, let’s examine some of the drawbacks and considerations that individuals should be aware of before deciding on this type of policy.

Drawbacks of Modified Whole Life Insurance

While modified whole life insurance has its advantages, it is essential to consider the potential drawbacks before making a decision. Here are some key drawbacks to be aware of:

1. Increased Premiums: A significant drawback of modified whole life insurance is the increase in premium payments after the initial modified premium period. The premium amount can rise significantly, which may pose financial challenges for policyholders, especially if their income does not increase as expected.

2. Lower Death Benefit during Modified Premium Period: During the modified premium period, the death benefit of the policy may be reduced compared to traditional whole life insurance. This means that if the policyholder were to pass away during this period, the beneficiaries would receive a lower payout, which may not provide sufficient financial protection for their needs.

3. Limited Flexibility: Once the policy transitions to the higher premium payments, policyholders are locked into the fixed premium amount for the remainder of the policy’s duration. This may limit financial flexibility and make it challenging to adjust premiums based on changing circumstances or financial goals.

4. Potential Risk of Policy Lapse: The increase in premium payments can pose a risk of policy lapse if the policyholder is unable to meet the higher financial obligations. If the policy lapses, the coverage and accumulated cash value could be lost, potentially leaving the policyholder without the desired life insurance protection.

5. Limited Investment Potential: While modified whole life insurance does build cash value over time, the growth potential may be lower than other investment options. Individuals seeking higher returns or greater investment flexibility may find other investment vehicles more suitable for their financial goals.

It’s essential to carefully evaluate these drawbacks in light of your individual financial situation and long-term objectives. Consider speaking with a knowledgeable insurance professional who can provide guidance and help you weigh the pros and cons of modified whole life insurance.

Now that we have examined the drawbacks, let’s move on to discuss the factors to consider when choosing a modified whole life insurance policy.

Factors to Consider when Choosing a Modified Whole Life Insurance Policy

When considering a modified whole life insurance policy, it’s crucial to take various factors into account to ensure it aligns with your financial goals and circumstances. Here are some key factors to consider when choosing a modified whole life insurance policy:

1. Premium Affordability: Evaluate your budget and determine if you can comfortably afford the higher premium payments that will come into effect after the initial modified premium period. Consider your current and future income prospects to ensure you can meet the financial obligations of the policy without straining your finances.

2. Coverage Needs: Assess your coverage needs and determine the amount of death benefit that would adequately protect your loved ones. Consider factors such as outstanding debts, future financial obligations, and the financial well-being of your dependents when deciding on the appropriate coverage amount.

3. Cash Value Accumulation: Examine the projected growth of the cash value component over time and assess if it aligns with your investment objectives. If you are looking for higher investment returns or more flexibility in accessing funds, you may want to explore other investment options outside of a modified whole life insurance policy.

4. Policy Duration: Consider the length of the modified whole life insurance policy and how it aligns with your long-term financial plans. Some policies may have a specific duration, while others provide coverage until the policyholder reaches a certain age. Ensure the policy duration matches your coverage goals and financial plans.

5. Company Reputation and Financial Stability: Research the insurance company offering the modified whole life insurance policy. Consider their reputation, financial stability, and track record of handling claims. A reputable and financially stable company will provide peace of mind, knowing that the policy will be honored and the death benefit will be paid out to your beneficiaries when the time comes.

6. Professional Advice: Seek guidance from an experienced insurance professional who can provide personalized advice based on your specific needs. They can help you understand the nuances of different policy options, explain the terms and conditions, and assist in comparing policies from various insurers.

By carefully considering these factors, you can make an informed decision when choosing a modified whole life insurance policy that suits your financial situation and long-term objectives.

Now, let’s wrap up everything we’ve discussed in this article.

Conclusion

Modified whole life insurance offers a unique combination of flexibility and long-term coverage, making it an attractive option for individuals seeking life insurance. This type of policy allows for lower initial premiums during a specified period, which can be beneficial for those with fluctuating income or specific financial needs at different stages of life.

While modified whole life insurance provides advantages such as cash value growth, a guaranteed death benefit, and lifetime coverage, there are also drawbacks to consider. The increase in premiums after the initial period and the potential risk of policy lapse require careful evaluation of your financial situation and long-term objectives.

When choosing a modified whole life insurance policy, it’s important to consider factors such as premium affordability, coverage needs, cash value accumulation, policy duration, and the reputation and financial stability of the insurance company. Seeking professional advice from an experienced insurance professional can also help guide you in making an informed decision.

Ultimately, the decision to choose a modified whole life insurance policy should align with your financial goals, risk tolerance, and circumstances. It’s crucial to thoroughly assess the features, benefits, and drawbacks of each policy before making a commitment.

Remember, insurance is a crucial element of financial planning, providing peace of mind and protection for your loved ones. Take the time to research and understand your options to ensure you select a modified whole life insurance policy that suits your needs and provides the long-term financial security you desire.

Now that you have a better understanding of modified whole life insurance, you can make an informed decision about whether it is the right choice for you and your loved ones.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance