Home>Finance>Why Are Life Insurance Companies Pension Funds And Mutual Funds Considered Financial Institution?

Finance

Why Are Life Insurance Companies Pension Funds And Mutual Funds Considered Financial Institution?

Published: January 23, 2024

Learn why life insurance companies, pension funds, and mutual funds are classified as financial institutions and their role in the finance industry. Understand the significance of these institutions in managing financial assets and providing security.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Financial institutions play a pivotal role in the global economy, serving as the backbone of the financial system and providing essential services to individuals, businesses, and governments. These institutions encompass a wide array of entities, including banks, insurance companies, pension funds, and mutual funds, each contributing uniquely to the financial landscape. In this article, we will delve into the significance of life insurance companies, pension funds, and mutual funds as financial institutions, shedding light on their roles and impact.

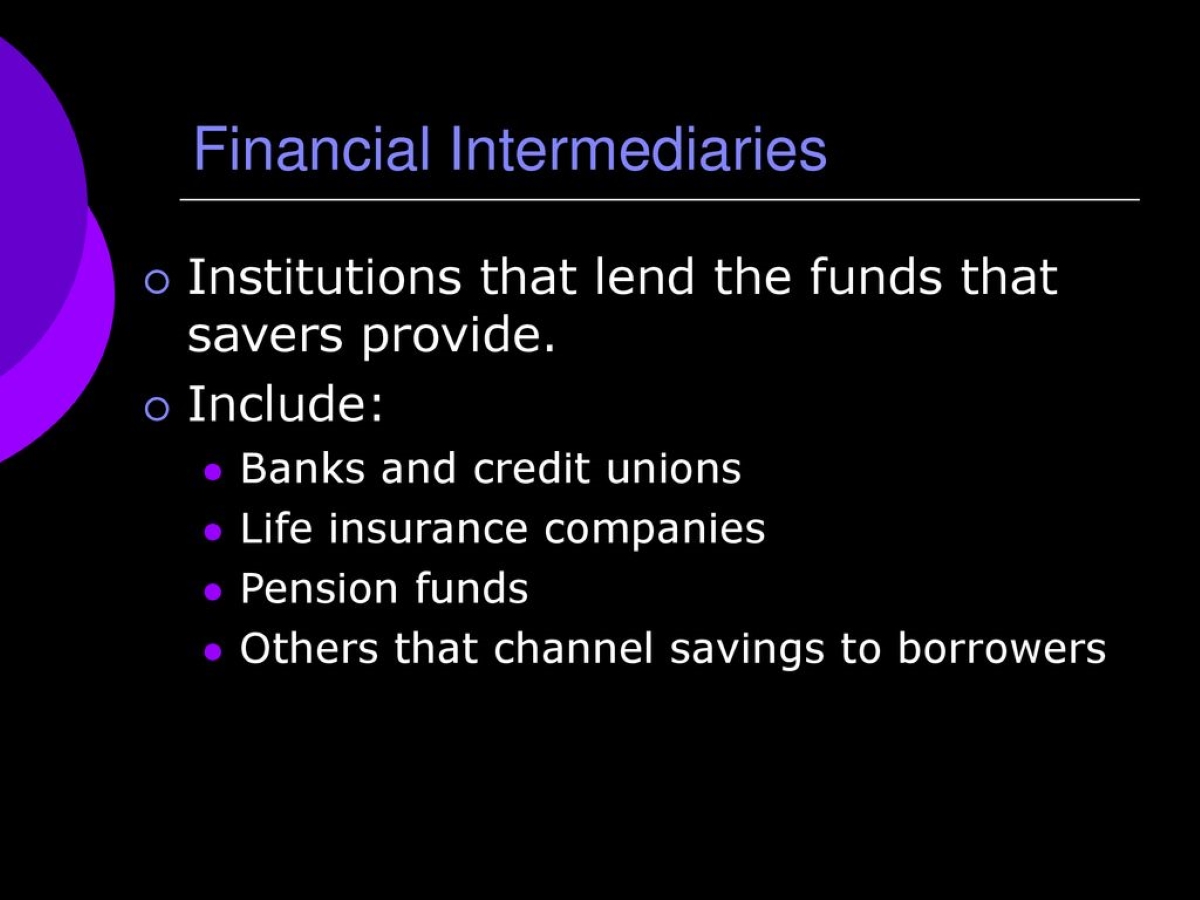

Financial institutions are instrumental in facilitating the flow of funds throughout the economy, channeling savings into investments, providing liquidity, and managing risk. They serve as intermediaries between savers and borrowers, fostering economic growth and stability. Understanding the multifaceted nature of financial institutions is crucial for comprehending their contributions to the financial system and the broader economy.

In the subsequent sections, we will explore the distinctive roles of life insurance companies, pension funds, and mutual funds as financial institutions, unraveling their significance and the value they bring to the financial landscape. By examining their functions and impact, we can gain a deeper appreciation for the interconnectedness of these institutions and their collective influence on the economy.

Definition of Financial Institutions

Financial institutions encompass a diverse range of organizations that serve as intermediaries in the financial markets, facilitating the efficient allocation of capital and the management of financial risks. These entities play a crucial role in the economy by providing essential financial services, including lending, investment management, and risk mitigation. The following are key characteristics that define financial institutions:

- Intermediation: Financial institutions act as intermediaries between savers and borrowers, channeling funds from individuals and businesses with surplus capital to those in need of financing for various purposes, such as investment, consumption, or operating expenses.

- Risk Management: They specialize in managing and diversifying financial risks, offering products and services that help clients mitigate the impact of market fluctuations, credit defaults, and other uncertainties.

- Liquidity Provision: Financial institutions contribute to the liquidity of the financial system by providing accessible avenues for individuals and businesses to deposit and withdraw funds, ensuring the smooth functioning of the economy.

- Capital Formation: Through their activities, financial institutions play a vital role in the formation of capital by mobilizing savings and directing them towards productive investments, fostering economic growth and development.

These defining characteristics underscore the fundamental role of financial institutions in supporting economic activities, promoting financial stability, and enabling the efficient allocation of resources. By serving as intermediaries and risk managers, these institutions contribute to the overall well-being of the economy and play a pivotal role in sustaining the functioning of financial markets.

Role of Life Insurance Companies as Financial Institutions

Life insurance companies serve as integral financial institutions that play a multifaceted role in the economy. Their primary function revolves around providing financial protection to policyholders and their beneficiaries in the event of unforeseen circumstances, such as death or disability. In addition to this core function, life insurance companies fulfill several key roles within the financial system:

- Risk Management: Life insurance companies specialize in assessing and managing mortality and longevity risks. By pooling the premiums paid by policyholders, these institutions can effectively spread the risk of premature death or extended life expectancy across a large and diverse customer base, thereby providing financial security to beneficiaries.

- Investment Intermediation: Life insurance companies channel the premiums they receive into a diverse portfolio of investments, including bonds, equities, and real estate. This intermediation of funds contributes to capital formation and supports economic growth by directing capital to productive ventures.

- Long-Term Savings and Retirement Planning: Life insurance products, such as annuities, offer individuals a means to accumulate savings over the long term and secure a stream of income during retirement. In this capacity, life insurance companies contribute to the financial well-being of individuals and the stability of the retirement system.

- Financial Market Stability: Through their investment activities and risk management practices, life insurance companies contribute to the stability of financial markets, providing liquidity and participating in the efficient functioning of capital markets.

By fulfilling these roles, life insurance companies bolster the financial system, promote long-term savings and risk management, and support the broader economy by facilitating the efficient allocation of capital. Their contributions to financial stability and individual financial security underscore their significance as vital financial institutions.

Role of Pension Funds as Financial Institutions

Pension funds are instrumental financial institutions that play a crucial role in safeguarding the financial well-being of individuals during their retirement years. These entities manage and invest funds contributed by employers and employees, with the objective of generating returns that will support pension payments to retirees. The role of pension funds extends beyond retirement planning, encompassing several key functions within the financial system:

- Long-Term Investment: Pension funds are long-term investors, focusing on building diversified investment portfolios that span various asset classes, including stocks, bonds, real estate, and alternative investments. By allocating capital to long-term ventures, pension funds contribute to capital formation and economic growth.

- Risk Management: Pension funds engage in rigorous risk management practices to ensure the long-term sustainability of pension assets. Through diversification and prudent investment strategies, they aim to mitigate investment risks and preserve the value of pension fund assets.

- Retirement Security: Pension funds play a pivotal role in providing retirement security to workers, offering a reliable source of income during their post-employment years. By effectively managing pension assets, these institutions support the financial well-being of retirees and contribute to social stability.

- Corporate Governance and Stewardship: As significant shareholders in various companies, pension funds often exercise influence through corporate governance practices, advocating for responsible and sustainable business practices that align with the long-term interests of shareholders and society at large.

Through their prudent investment practices, focus on long-term asset growth, and commitment to ensuring retirement security, pension funds serve as vital components of the financial system. Their contributions to capital markets, risk management, and the provision of retirement benefits underscore their significance as key financial institutions that play a pivotal role in supporting the financial well-being of individuals and the broader economy.

Role of Mutual Funds as Financial Institutions

Mutual funds are significant financial institutions that serve as accessible vehicles for individuals and institutional investors to participate in diversified investment portfolios. These funds pool capital from numerous investors and allocate it across a range of securities, such as stocks, bonds, and money market instruments. The role of mutual funds extends beyond investment management, encompassing several key functions within the financial system:

- Investment Diversification: Mutual funds offer investors the opportunity to achieve diversified exposure to various asset classes and market segments, reducing individual investment risk and enhancing portfolio resilience. This diversification is instrumental in promoting financial stability and mitigating investment volatility.

- Professional Investment Management: Mutual funds are managed by experienced investment professionals who conduct in-depth research, execute investment strategies, and monitor portfolio performance. This expertise enables individual investors to benefit from professional asset management tailored to their investment objectives.

- Liquidity Provision: Mutual funds provide investors with liquidity by offering the ability to buy and sell fund shares on a regular basis. This liquidity feature enhances market efficiency and ensures that investors can access their capital as needed, contributing to the smooth functioning of financial markets.

- Accessibility and Inclusivity: Mutual funds cater to a broad investor base, offering individuals with varying levels of wealth the opportunity to participate in professionally managed investment portfolios. This inclusivity promotes financial inclusion and allows a wide spectrum of investors to access diversified investment opportunities.

By fulfilling these roles, mutual funds contribute to the democratization of investment opportunities, provide access to professional asset management, and enhance the efficiency and resilience of financial markets. Their significance as accessible investment vehicles and contributors to investment diversification underscores their pivotal role as financial institutions that support the financial well-being of individuals and the broader economy.

Conclusion

Financial institutions, including life insurance companies, pension funds, and mutual funds, are indispensable components of the global financial system, each playing a distinct yet interconnected role in supporting economic activities and fostering financial well-being. These institutions serve as intermediaries, risk managers, and promoters of financial stability, contributing to the efficient allocation of capital and the management of financial risks.

Life insurance companies, through their risk management expertise and long-term savings products, provide financial security to individuals and support the stability of the retirement system. Pension funds, with their focus on long-term investment and retirement security, play a vital role in ensuring the financial well-being of retirees and contributing to capital formation. Mutual funds, by offering investment diversification, professional asset management, and accessibility, democratize investment opportunities and enhance market efficiency.

Collectively, these financial institutions bolster the financial system, promote long-term savings, and facilitate the efficient allocation of capital, ultimately contributing to economic growth and stability. Their roles as intermediaries, risk managers, and providers of financial security underscore their significance as key pillars of the financial landscape.

Understanding the multifaceted roles of these financial institutions is essential for comprehending their impact on the broader economy and the interconnectedness of the financial system. By recognizing their contributions to capital markets, risk management, and retirement security, we gain a deeper appreciation for their pivotal role in sustaining the functioning of financial markets and supporting the financial well-being of individuals.

In conclusion, life insurance companies, pension funds, and mutual funds stand as vital financial institutions that embody the principles of financial intermediation, risk management, and long-term financial security, shaping the contours of the financial system and underpinning the economic well-being of individuals and societies.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance