Home>Finance>Why Did I Get An ACH Credit From Social Security

Finance

Why Did I Get An ACH Credit From Social Security

Modified: January 15, 2024

Wondering why you received an ACH credit from Social Security? Find answers and explanations about your finances in this informative article.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

- Introduction

- Understanding ACH Credits

- What is Social Security?

- Common Reasons for Receiving an ACH Credit from Social Security

- Direct Deposit for Social Security Benefits

- Changes or Updates to Social Security Payments

- Potential Mistakes or Errors

- Scams or Fraudulent ACH Credits

- Resolving Issues with ACH Credits from Social Security

- Conclusion

Introduction

Have you ever received an ACH credit from Social Security and wondered why? It’s a common question, and understanding the reasons behind these deposits can provide valuable insights into your financial situation. In this article, we’ll delve into the topic of ACH credits from Social Security and explore the various scenarios that may lead to their issuance.

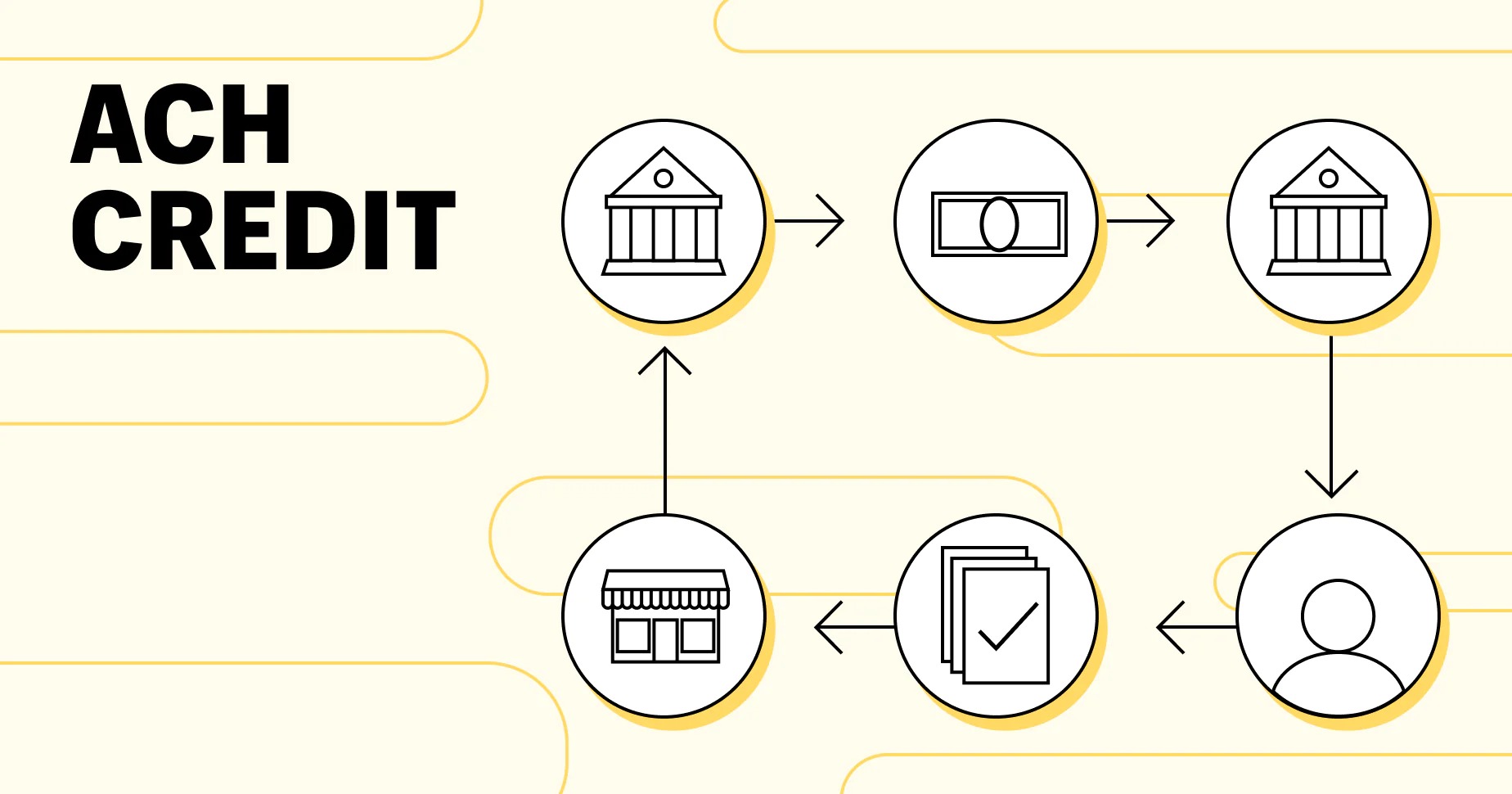

ACH, which stands for Automated Clearing House, is a nationwide electronic payment network that facilitates the secure transfer of funds between financial institutions. ACH credits are deposits made directly into your bank account, often on a recurring basis.

Now, let’s discuss Social Security. It is a federal program administered by the Social Security Administration (SSA) that provides financial benefits to eligible individuals, including retirement, disability, and survivor benefits. If you’re an eligible recipient, you may receive these benefits either through a physical check or via direct deposit into your bank account.

Receiving an ACH credit from Social Security means that your benefits have been directly deposited into your bank account. This method offers convenience, security, and faster access to your funds, eliminating the need to wait for a check to arrive and be deposited manually.

In the following sections, we’ll explore the common reasons for receiving an ACH credit from Social Security and provide insights into various scenarios that may arise, including changes or updates to your Social Security payments, potential errors or mistakes, and even ways to address issues related to scams or fraudulent ACH credits.

It’s important to have a good understanding of how your Social Security benefits are credited to your bank account to ensure you can spot any discrepancies, resolve any problems, and maximize the benefits you’re entitled to. So, let’s dive in and unravel the mystery behind ACH credits from Social Security.

Understanding ACH Credits

Before we delve into the specifics of ACH credits from Social Security, it’s important to have a clear understanding of what ACH credits are and how they work.

ACH credits are electronic payments made directly into your bank account. The Automated Clearing House (ACH) network facilitates these payments, allowing for secure and efficient transfers between financial institutions. This system is widely used for various types of transactions, including direct deposit of paychecks, tax refunds, and government benefits like Social Security.

When you receive an ACH credit, the funds are deposited directly into your bank account. This means you don’t have to worry about physically cashing a check or waiting for it to clear. The electronic transfer of funds allows for quicker access to your money and eliminates the risk of lost or stolen checks.

ACH credits are typically accompanied by an electronic remittance advice (ERA) or explanation letter. This document provides important details about the deposit, such as the date, amount, and purpose of the payment. It’s crucial to review this information carefully to ensure the deposit aligns with your expectations and the funds are being credited for the correct reasons.

Now that we have a basic understanding of ACH credits, let’s explore why you may receive an ACH credit from Social Security and what it means for your financial situation.

What is Social Security?

Social Security is a federal program in the United States that provides financial benefits to eligible individuals and their families. It is administered by the Social Security Administration (SSA). The primary purpose of Social Security is to provide a safety net to retirees, people with disabilities, and survivors of deceased workers. The program is funded through payroll taxes paid by employers and employees.

One of the key benefits provided by Social Security is retirement benefits. Workers who have contributed to Social Security through their payroll taxes are eligible to receive retirement benefits once they reach the designated age of eligibility, typically between 62 and 67 years old, depending on the year of birth. These retirement benefits are designed to replace a portion of the individual’s pre-retirement income and provide a steady source of income in their golden years.

In addition to retirement benefits, Social Security also provides disability benefits. These benefits are available to individuals who are unable to work due to a physical or mental impairment expected to last for at least a year or result in death. Disability benefits offer essential financial support to individuals who are unable to earn a living due to their disability.

Furthermore, Social Security offers survivor benefits to the family members of deceased workers. These benefits provide financial support to eligible spouses, children, and even dependent parents of deceased individuals who had contributed to the Social Security system. The goal is to provide financial stability to the family members left behind.

It’s important to note that Social Security is an entitlement program, meaning that individuals who meet the eligibility criteria are entitled to receive benefits. These benefits are not means-tested, so they are not based on income or assets. However, the amount of benefits received is determined by the individual’s earnings history and the length of time they have contributed to Social Security.

Now that we have a clearer understanding of what Social Security is and the benefits it provides, let’s explore the common reasons why you may receive an ACH credit from Social Security.

Common Reasons for Receiving an ACH Credit from Social Security

If you’ve received an ACH credit from Social Security, there are several common reasons that may explain the deposit. Understanding these reasons can help you better manage your finances and ensure that you are receiving the benefits you are entitled to. Here are some of the most common reasons for receiving an ACH credit from Social Security:

- Retirement Benefits: If you have reached the designated age of eligibility for Social Security retirement benefits, you may receive an ACH credit as your monthly retirement payment. This payment is based on your earnings history and the age at which you choose to begin receiving benefits.

- Disability Benefits: If you have been approved for Social Security disability benefits, you may receive an ACH credit as your monthly disability payment. To qualify for these benefits, you must have a physical or mental impairment that prevents you from engaging in substantial gainful activity.

- Survivor Benefits: If you are the surviving spouse, child, or dependent parent of a deceased worker who was eligible for Social Security benefits, you may receive an ACH credit as survivor benefits. These payments are meant to provide financial support to the surviving family members.

- Supplemental Security Income (SSI): SSI is a program that provides financial assistance to low-income individuals who are aged, blind, or disabled. If you qualify for SSI, you may receive an ACH credit as your monthly SSI payment.

- Special Payments: In some cases, you may receive a one-time or special payment from Social Security. This could be due to a retroactive adjustment, a lump sum payment, or a reimbursement for Medicare premiums.

It’s important to note that the specific reason for receiving an ACH credit may vary based on your individual circumstances. It’s always a good idea to review the electronic remittance advice (ERA) or explanation letter accompanying the deposit to ensure that it aligns with your expectations and the benefits you are entitled to.

Now that we’ve explored the common reasons for receiving an ACH credit from Social Security, let’s move on to understanding the process of direct deposit for Social Security benefits.

Direct Deposit for Social Security Benefits

Direct deposit is the preferred method for receiving Social Security benefits. With direct deposit, your monthly benefit payments are electronically transferred directly into your bank account on a specified date, providing you with convenient and timely access to your funds.

There are several benefits to choosing direct deposit for your Social Security benefits:

- Security: Direct deposit eliminates the risk of lost or stolen paper checks. Your benefit payments are securely deposited into your bank account, reducing the potential for fraud or identity theft.

- Convenience: With direct deposit, you don’t have to worry about manually depositing paper checks or waiting for them to clear. Your funds are automatically available in your bank account on the day they are scheduled to be deposited.

- Reliability: Direct deposit ensures that your benefit payments are not delayed due to postal issues or holidays. You can rely on the consistent and timely arrival of your funds.

- Cost Savings: Direct deposit eliminates the need to pay fees for check cashing services or the cost of potentially lost or stolen paper checks. It is a cost-effective option for accessing your benefits.

Setting up direct deposit for your Social Security benefits is easy. You can do it online through the Social Security Administration’s website, by calling their toll-free number, or by visiting your local Social Security office. You will need to provide your bank account information, including the routing number and account number, to complete the setup process.

Once your direct deposit is set up, your benefit payments will be automatically deposited into your designated bank account on the scheduled payment date. You can check your bank statement or online banking portal to confirm the deposit.

It’s important to keep your bank account information up to date with the Social Security Administration. If you change banks or open a new account, be sure to notify the SSA as soon as possible to avoid any interruptions or delays in receiving your benefits.

Now that we understand the process of direct deposit for Social Security benefits, let’s explore what to do in the event of changes or updates to your Social Security payments.

Changes or Updates to Social Security Payments

Once you have set up direct deposit for your Social Security benefits, it’s important to stay informed about any changes or updates that may occur regarding your payments. Here are some common scenarios that may result in changes or updates to your Social Security payments:

- Cost-of-Living Adjustments (COLA): Each year, the Social Security Administration may make cost-of-living adjustments to ensure that benefits keep pace with inflation. These adjustments are based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If a COLA is approved, your benefit amount may increase to reflect the changes in the cost of living.

- Changes to Earnings: If you continue to work while receiving Social Security benefits, any changes in your earnings may affect the amount you receive. If you reach full retirement age, there are no limits on how much you can earn without a reduction in benefits. However, if you have not reached full retirement age, there are income limits that may impact the amount of benefits you receive.

- Changes to Marital Status: If you get married or divorced, your Social Security benefits may be affected. In the case of marriage, you may be eligible for spousal benefits based on your partner’s earnings history. In the case of divorce, you may be eligible for benefits based on your ex-spouse’s earnings if certain conditions are met.

- Changes in Living Arrangements: If you receive SSI benefits, any changes in your living arrangements or income from other sources may affect the amount you receive. It’s important to report any changes promptly to the Social Security Administration to ensure that your benefits are accurately adjusted.

- Deceased Spouse: If you are receiving benefits as a surviving spouse, it is essential to notify the Social Security Administration in the event of your spouse’s death. The SSA will adjust your benefits accordingly, and you may be eligible for additional survivor benefits.

If there are any changes or updates to your Social Security payments, you will typically receive notification from the Social Security Administration. This could be in the form of a letter or an electronic document informing you of the adjustments made to your benefits.

It’s crucial to review these notifications carefully and contact the SSA if you have any questions or concerns about the changes. By staying informed and proactive, you can ensure that you are receiving the correct amount of benefits and avoid any potential issues.

Now that we’ve covered changes and updates to Social Security payments, let’s explore the potential mistakes or errors that may occur in the process.

Potential Mistakes or Errors

While the Social Security Administration strives to provide accurate and timely benefit payments, mistakes or errors can occasionally occur. It’s important to be aware of potential issues that may arise to ensure that you receive the benefits you are entitled to. Here are some common mistakes or errors that may affect your Social Security payments:

- Incorrect Benefit Amount: There may be instances where the calculated benefit amount is incorrect, resulting in overpayment or underpayment. This could be due to errors in the earnings record, miscalculations, or other administrative issues. It’s crucial to review your benefit statement or contact the Social Security Administration if you suspect any discrepancies.

- Missing or Delayed Payments: There may be occasions where your benefit payment is missing or delayed. This could be due to administrative errors, processing delays, or issues with your direct deposit information. If you do not receive your payment on the expected date, contact the Social Security Administration for assistance.

- Incorrect Personal Information: Errors in personal information such as your name, Social Security number, or date of birth can potentially impact your benefit payments. It’s essential to review your records and notify the Social Security Administration if you identify any incorrect information.

- Failure to Report Changes: If there are changes in your circumstances that could affect your Social Security benefits, such as changes in income, marital status, or living arrangements, it’s crucial to report them to the Social Security Administration promptly. Failure to report changes accurately and in a timely manner can result in incorrect benefit payments.

- Identity Theft or Fraud: In rare instances, your Social Security payments may be affected by identity theft or fraudulent activity. It’s important to stay vigilant and monitor your accounts regularly for any suspicious activity. Report any potential identity theft or fraud to the Social Security Administration immediately.

If you believe there is a mistake or error with your Social Security benefits, it’s essential to contact the Social Security Administration as soon as possible. They can review your case, investigate any discrepancies, and take the necessary steps to correct any errors. Remember to keep detailed records of your communication with the SSA and any supporting documentation you may have.

Now that we’ve discussed potential mistakes or errors, let’s explore the importance of being vigilant about scams or fraudulent ACH credits related to Social Security.

Scams or Fraudulent ACH Credits

Unfortunately, scammers and fraudsters often target Social Security recipients with various schemes to deceive them into providing personal information or access to their bank accounts. It’s essential to be aware of these scams and to protect yourself against fraudulent ACH credits. Here are some common scams related to Social Security and ACH credits:

- Impersonation Scams: Scammers may pose as Social Security Administration representatives and contact you via phone, email, or text message, claiming there is an issue with your benefits. They may request personal information, such as your Social Security number or bank account details. The SSA will never contact you and ask for sensitive information in this manner. Be cautious and avoid sharing personal information with anyone claiming to be from the SSA.

- Phishing Emails or Websites: Fraudsters may send phishing emails or create fake websites that appear to be from the Social Security Administration. These emails or websites may ask you to verify your personal information or click on suspicious links. Always be cautious when providing personal information online and ensure that you are on the official SSA website.

- Unsolicited Direct Deposit Changes: Scammers may attempt to change your direct deposit information without your knowledge or consent, redirecting your benefit payments into their own accounts. If you receive any communication regarding changes to your direct deposit information that you did not initiate, contact the Social Security Administration immediately to report the issue.

- Unauthorized Access to Bank Accounts: Fraudsters may obtain your banking information through various means, such as phishing or hacking, and initiate unauthorized ACH credits from your account. It’s crucial to regularly monitor your bank statements and account activity for any suspicious transactions.

To protect yourself against scams or fraudulent ACH credits, keep the following tips in mind:

- Be skeptical of unsolicited communication regarding your Social Security benefits.

- Do not share your personal information, such as your Social Security number or bank account details, with unknown individuals or organizations.

- Verify the legitimacy of any email or website before providing personal information or clicking on links.

- Regularly review your bank statements and report any unauthorized transactions to your bank immediately.

- Stay informed about common scams and fraud techniques targeting Social Security recipients. The Social Security Administration provides resources and alerts about fraudulent activities on their official website.

If you encounter any suspicious activity or believe you have been a victim of a scam or fraud related to your Social Security benefits or ACH credits, report it to the Social Security Administration and your local authorities as soon as possible.

Now that we’ve discussed scams and fraudulent ACH credits, let’s explore how to resolve any issues that may arise with your Social Security payments.

Resolving Issues with ACH Credits from Social Security

If you encounter any issues or discrepancies with your ACH credits from Social Security, it’s important to take prompt action to resolve the situation. Here are some steps you can take to address and resolve any problems related to your Social Security payments:

- Contact the Social Security Administration: If you notice any errors or issues with your ACH credits, the first step is to reach out to the Social Security Administration. You can contact them by phone, visit your local Social Security office, or utilize their online services. Explain the problem, provide any necessary documentation, and ask for assistance in resolving the issue.

- Provide Supporting Documentation: When reporting an issue or discrepancy, it’s helpful to gather and provide any relevant supporting documentation. This may include bank statements, the electronic remittance advice (ERA) or explanation letter accompanying the ACH credit, or any other documents that can help verify the problem you are experiencing.

- Follow Up Regularly: After reporting the issue, it’s important to follow up with the Social Security Administration regularly. Keep track of the dates and times of your interactions, the names of the representatives you speak to, and any reference numbers provided. This will help ensure that your case is being addressed and progress is being made towards resolving the issue.

- Consider Seeking Legal Assistance: In some cases, particularly if the issue persists or if you believe you have been treated unfairly, it may be beneficial to seek legal assistance. An attorney with expertise in Social Security matters can provide guidance and represent your interests in resolving the issue.

- Keep Detailed Records: Throughout the process of resolving the issue, it’s essential to keep detailed records of all communication, documents, and any other relevant information. This will help you track the progress of your case, provide evidence if necessary, and ensure that you have a clear record of the steps taken to resolve the issue.

Resolving issues with ACH credits from Social Security can sometimes take time and patience. It’s important to stay proactive, persistent, and maintain clear communication with the Social Security Administration throughout the process.

Understanding the common reasons for ACH credits, being aware of potential mistakes or errors, and staying vigilant against scams or fraudulent activities can also help you identify and address any issues that may arise with your Social Security payments.

Now that we’ve discussed how to resolve issues with ACH credits from Social Security, let’s conclude our article.

Conclusion

Receiving an ACH credit from Social Security can be both a convenient and essential aspect of managing your finances. Understanding the reasons behind these deposits and staying informed about potential issues is crucial for ensuring that you receive the correct amount of benefits and protect yourself against scams and fraudulent activities.

In this article, we explored the common reasons for receiving an ACH credit from Social Security, including retirement benefits, disability benefits, survivor benefits, Supplemental Security Income (SSI), and special payments. We also discussed the importance of direct deposit as a secure and convenient method for receiving Social Security payments.

We highlighted the need to stay vigilant about changes or updates that may occur with your Social Security payments, such as cost-of-living adjustments, changes in earnings, or changes in marital status. We also addressed potential mistakes or errors that can affect your benefit payments, emphasizing the importance of promptly reporting any issues to the Social Security Administration.

Furthermore, we discussed the prevalence of scams and fraudulent activities associated with Social Security and ACH credits, urging readers to be cautious and protect themselves against these deceptive practices. We provided tips to stay vigilant and outlined the steps to take if you believe you have been a victim of a scam or fraud.

Finally, we discussed the steps to take in resolving any issues or discrepancies with your ACH credits from Social Security, including contacting the Social Security Administration, providing supporting documentation, and maintaining detailed records. We emphasized the importance of persistence and, if necessary, seeking legal assistance to ensure a fair resolution.

By understanding the processes and potential challenges associated with ACH credits from Social Security, you can effectively manage your benefits, protect yourself from fraud, and ensure that you receive the financial support you are entitled to.

Remember to stay informed, stay proactive, and reach out to the Social Security Administration whenever you have questions or concerns. Your Social Security benefits are an essential part of your financial well-being, so it’s crucial to stay engaged and advocate for your rights.

What's Hot

Latest Articles

Related Post

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance