Finance

Why Is Available Credit Less Than Credit Limit

Published: March 5, 2024

Learn why your available credit may be less than your credit limit and how it affects your finances. Get valuable insights on managing your credit effectively.

(Many of the links in this article redirect to a specific reviewed product. Your purchase of these products through affiliate links helps to generate commission for LiveWell, at no extra cost. Learn more)

Table of Contents

Introduction

Understanding the dynamics of available credit and credit limits is essential for managing personal finances effectively. Whether you're applying for a credit card, seeking a loan, or aiming to improve your credit score, comprehending the relationship between these two factors is crucial. Available credit refers to the portion of your credit limit that remains untapped, representing the funds you can still access. On the other hand, the credit limit signifies the maximum amount you can borrow or spend using a particular credit account.

Exploring the nuances of available credit and credit limits unveils the factors influencing their values and the impact they have on your financial well-being. By delving into this subject, you'll gain valuable insights into how these elements can shape your credit score and overall financial health. Furthermore, understanding the strategies to optimize available credit empowers you to make informed decisions and leverage this aspect of your financial profile to your advantage.

Let's delve deeper into the world of available credit and credit limits, unraveling their significance and exploring the strategies to manage them effectively. Understanding these concepts will not only enhance your financial literacy but also equip you with the knowledge to navigate the complex landscape of personal finance with confidence and clarity.

Understanding Credit Limit and Available Credit

When you open a credit account, such as a credit card or a line of credit, the issuer assigns a credit limit, which represents the maximum amount you can borrow or spend using that account. This limit is determined based on various factors, including your credit history, income, and overall creditworthiness. It serves as a safeguard for both the lender and the borrower, ensuring that the borrower does not overextend their finances and that the lender can manage their risk effectively.

Available credit, on the other hand, refers to the portion of your credit limit that remains unused. It represents the funds you can still access without surpassing the prescribed limit. For instance, if your credit card has a limit of $5,000 and you have a current balance of $2,000, your available credit would be $3,000. This available credit can fluctuate as you make purchases, pay off balances, or incur interest charges.

Understanding the distinction between credit limit and available credit is crucial for managing your finances responsibly. It enables you to gauge your borrowing capacity, make informed spending decisions, and avoid situations where you inadvertently exceed your credit limit. Moreover, being mindful of your available credit empowers you to maintain a healthy credit utilization ratio, a key factor in determining your credit score.

By keeping a close eye on your available credit and credit limit, you can navigate the realm of credit with prudence and foresight. This awareness allows you to leverage your available credit strategically, ensuring that you can access funds when needed while maintaining a favorable credit utilization ratio.

Factors Affecting Available Credit

Several factors can influence the amount of available credit on your accounts, impacting your financial flexibility and credit utilization. Understanding these factors is crucial for managing your available credit effectively and optimizing your overall financial health.

- Credit Utilization Ratio: One of the primary factors affecting available credit is your credit utilization ratio, which is the percentage of your total credit limit that you are currently using. Maintaining a low credit utilization ratio, ideally below 30%, can positively impact your available credit. When your credit utilization is high, it may signal financial strain to lenders, potentially leading to a reduction in your available credit.

- Payment History: Your history of making timely payments on your credit accounts can significantly impact your available credit. Consistently paying your bills on time demonstrates financial responsibility and may lead to increases in your credit limits, thereby expanding your available credit.

- Credit History Length: The length of your credit history also plays a role in determining your available credit. Lenders may consider longer credit histories as more stable and reliable, potentially resulting in higher credit limits and increased available credit.

- Income and Employment Status: Your income and employment status can influence the amount of credit available to you. Lenders may be more inclined to extend higher credit limits and available credit to individuals with steady incomes and secure employment.

- Debt-to-Income Ratio: Lenders assess your debt-to-income ratio to evaluate your ability to manage additional credit. A lower debt-to-income ratio can signal financial stability and may lead to higher available credit.

By being mindful of these factors and their impact on available credit, you can take proactive steps to manage your finances effectively. Maintaining a positive payment history, keeping your credit utilization in check, and demonstrating financial stability can contribute to an increase in available credit, providing you with greater financial flexibility and borrowing capacity.

Impact of Available Credit on Credit Score

Available credit plays a pivotal role in determining your credit score, influencing your overall creditworthiness and financial standing. Understanding how available credit impacts your credit score is essential for managing your finances and optimizing your credit profile.

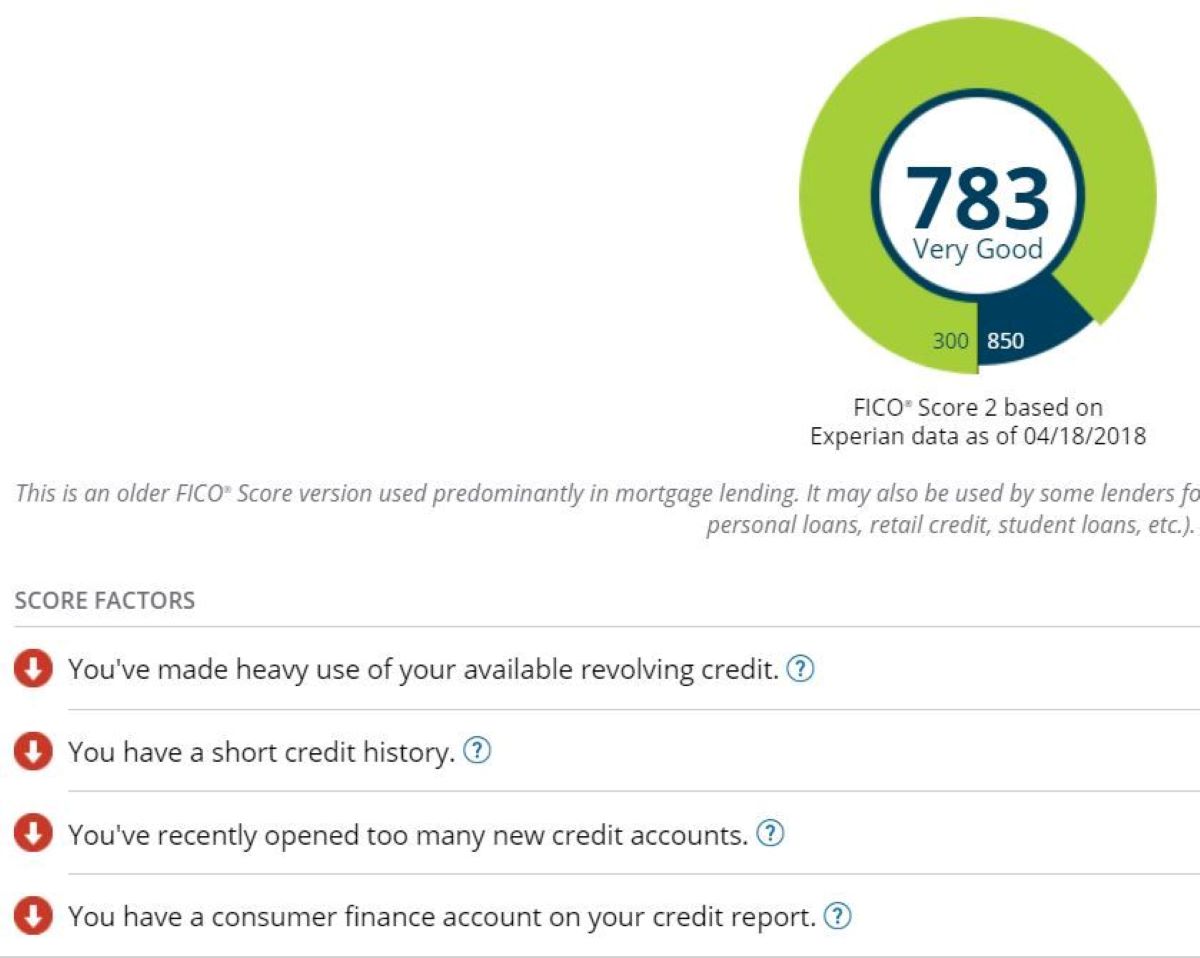

One of the key ways available credit affects your credit score is through the calculation of your credit utilization ratio. This ratio, which compares the amount of credit you are using to your total available credit, is a significant factor in credit scoring models. Maintaining a low credit utilization ratio, typically below 30%, demonstrates responsible credit management and can positively impact your credit score. When your available credit is high relative to your balances, it indicates to lenders that you are not overly reliant on credit, potentially boosting your creditworthiness.

Additionally, having ample available credit provides a buffer that can mitigate the impact of unexpected expenses or financial emergencies. By maintaining a comfortable margin between your balances and your credit limits, you demonstrate prudent financial planning and resilience, factors that can enhance your credit score.

Conversely, a low level of available credit, coupled with high credit utilization, can adversely affect your credit score. It may signal financial strain and an increased likelihood of default, leading to a lower credit score and potential challenges in obtaining favorable credit terms in the future.

Understanding the interplay between available credit and credit scoring empowers you to make informed financial decisions. By optimizing your available credit and keeping your credit utilization in check, you can positively influence your credit score, bolstering your financial prospects and access to credit.

Strategies to Increase Available Credit

Maximizing your available credit can enhance your financial flexibility and strengthen your credit profile. Implementing strategic approaches to increase your available credit empowers you to manage your finances more effectively and improve your overall creditworthiness.

- Requesting a Credit Limit Increase: Contacting your credit card issuer to request a credit limit increase is a proactive way to expand your available credit. Demonstrating responsible credit usage and a positive payment history can bolster your case for a higher credit limit.

- Reducing Outstanding Balances: Paying down existing balances on your credit accounts can effectively increase your available credit. By lowering your credit utilization ratio, you demonstrate responsible credit management, potentially prompting credit issuers to offer you higher credit limits.

- Opening a New Credit Account: Consider opening a new credit account, such as a credit card, to augment your overall available credit. However, exercise caution to avoid excessive applications, which can temporarily impact your credit score.

- Consolidating Debt: Exploring options to consolidate high-interest debt into a single, lower-interest account can free up available credit across your other accounts. This approach can streamline your debt management while increasing your overall available credit.

- Regularly Reviewing Your Credit Report: Monitoring your credit report for inaccuracies and addressing any errors can ensure that your available credit is accurately reflected. Disputing any discrepancies can potentially result in an increase in available credit if inaccurately reported balances are corrected.

By incorporating these strategies into your financial management practices, you can proactively work toward increasing your available credit and fortifying your financial foundation. It’s essential to approach these tactics with prudence and a long-term perspective, aiming to optimize your available credit while maintaining responsible credit usage and financial discipline.

Conclusion

Understanding the intricacies of available credit and credit limits is paramount for navigating the terrain of personal finance with confidence and foresight. These fundamental elements not only dictate your borrowing capacity but also wield significant influence over your credit score and overall financial well-being.

By comprehending the factors that affect available credit and leveraging strategic approaches to increase it, you can fortify your financial flexibility and bolster your creditworthiness. Maintaining a healthy credit utilization ratio, demonstrating responsible payment habits, and exploring opportunities to optimize your available credit empower you to harness this aspect of your financial profile to its fullest potential.

Moreover, recognizing the impact of available credit on your credit score illuminates the profound significance of managing this aspect of your finances judiciously. By maintaining a comfortable margin between your balances and credit limits, you can enhance your creditworthiness and pave the way for favorable credit terms and opportunities in the future.

As you navigate the realm of personal finance, remember that available credit is not merely a numerical value but a dynamic component that reflects your financial prudence and planning. By embracing a proactive approach to managing your available credit, you can cultivate a resilient financial foundation and chart a path toward enduring financial stability and success.

In essence, the interplay between available credit, credit limits, and your overall financial landscape underscores the importance of informed decision-making and prudent financial management. Armed with this knowledge, you are equipped to steer your financial journey with clarity, purpose, and the confidence that comes from mastering this essential aspect of personal finance.

What's Hot

Latest Articles

Related Post

By: • Finance

By: Chelsea • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance

By: • Finance